Assumptions Rate Values

Initial spot rate, 1999 (Sucre/$) S1 5,000

Ending spot rate, 1999 (Sucre/$) S2 25,000

Problem 9.1 Ecuadorian Sucre

The Ecuadorian sucre (S) suffered from hyper-inflationary forces throughout 1999. Its value

moved from S5,000/$ to S25,000/$. What was the percentage change in its value?

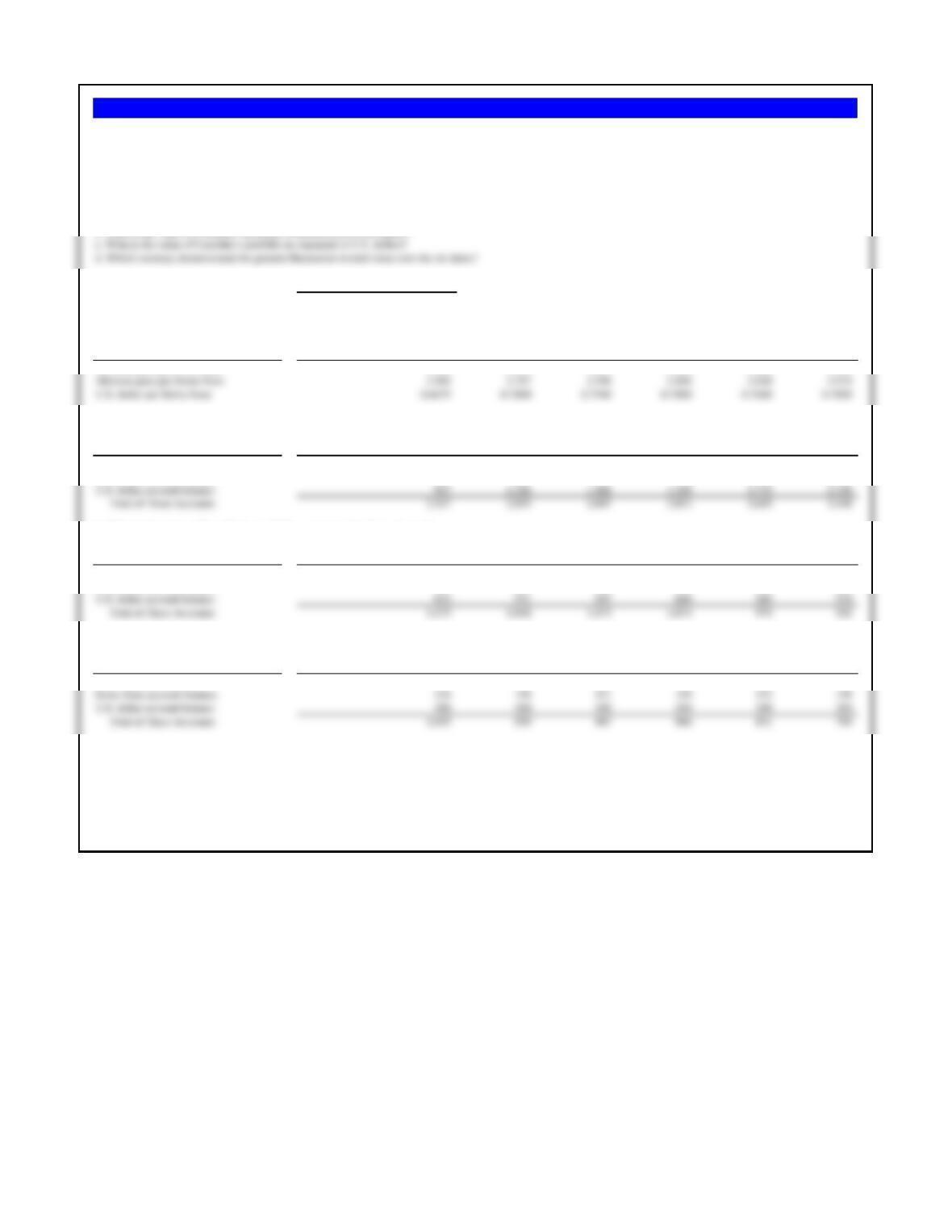

The following values are taken from the graph.

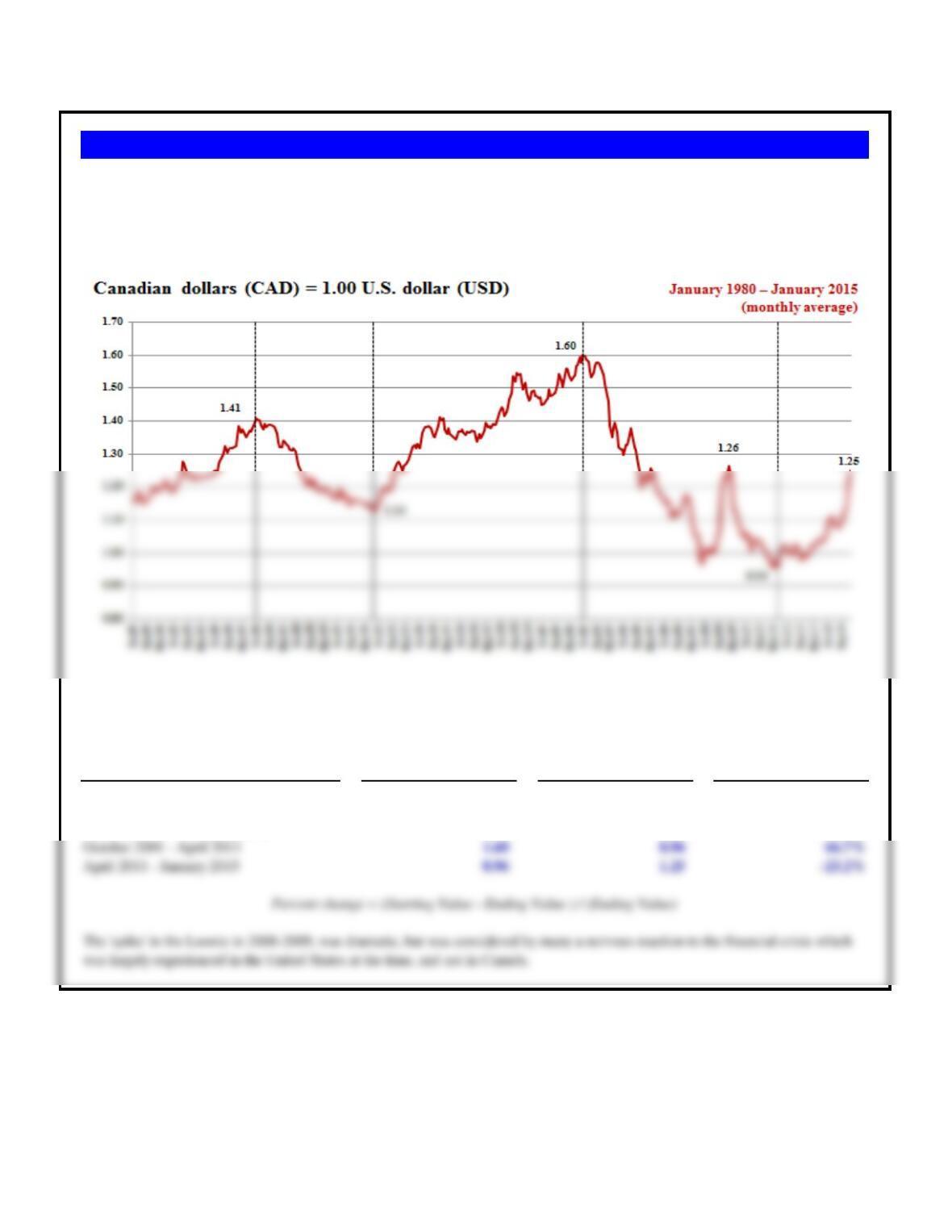

Change in the value

Starting Value Ending Value of the loonie

Time Period (C$/US$) (C$/US$) (percent)

January 1980 – January 1986 1.16 1.41 -17.7%

January 1986 – October 1991 1.41 1.13 24.8%

October 1991 – December 2001 1.13 1.60 -29.4%

The Canadian dollar’s value against the U.S. dollar has seen some significant changes over recent history. Using the following

graph of the C$/US$ exchange rate for the 30 year period between 1980 and end-of-year 2010 to estimate the percentage change in

the Canadian dollar’s value (its affectionately known as the “loonie”) versus the dollar for the following periods.

Problem 9.2 Canadian Dollar

a. What was the percentage change in the value of the Nigerian naira versus the dollar the first trading day?

b. What was the percentage change in the value of the naira versus the dollar by August 18, 2016?

NGN NGN

Assumptions Rate Per USD Per EUR

Initial spot rate, June 17 S1 196.50 221.2001

Closing spot rate, June 20 S2 279.50 316.7294

Closing spot rate, August 17 S3 324.50 347.7721

Calculation of percentage change:

a) and c) Percentage change in the first day of trading -29.70% -30.16%

Problem 9.3 Nigerian Naira’s Nightmare

On Friday June 17, 2016, the Central Bank of Nigeria (CBN) abandoned the Nigerian naira’s (NGN or ₦) fixed exchange

rate and allowed the currency to float. Previously fixed against the U.S. dollar at NGN 196.50 = 1.00 USD, the naira closed

at NGN 279.50/USD on Monday June 20, the first day of trading following the float. The naira quickly quickly floated

(sunk) to NGN 324.50/USD by August 18. Similarly, the naira fell from NGN 221.2001 = 1.00 EUR toNGN316.7294 /EUR

on June 20, and NGN 347.7721/EUR on August 18.

Assumptions Values

Spot rate, February 20, 2001 (TL/$) 68,000

a. What was the exchange rate after devaluation?

Spot rate after devaluation 85,000

Check calculation: percentage change in values -20.0%

b. What was percentage change after falling to TL100,000/$?

Problem 9.4 Istanbul’s Issues

The Turkish lira (TL) was officially devalued by the Turkish government in February 2001

during a severe political and economic crisis. The Turkish government announced on February

21st that the lira would be devalued by 20%. The spot exchange rate on February 20th was

TL68,000/$.

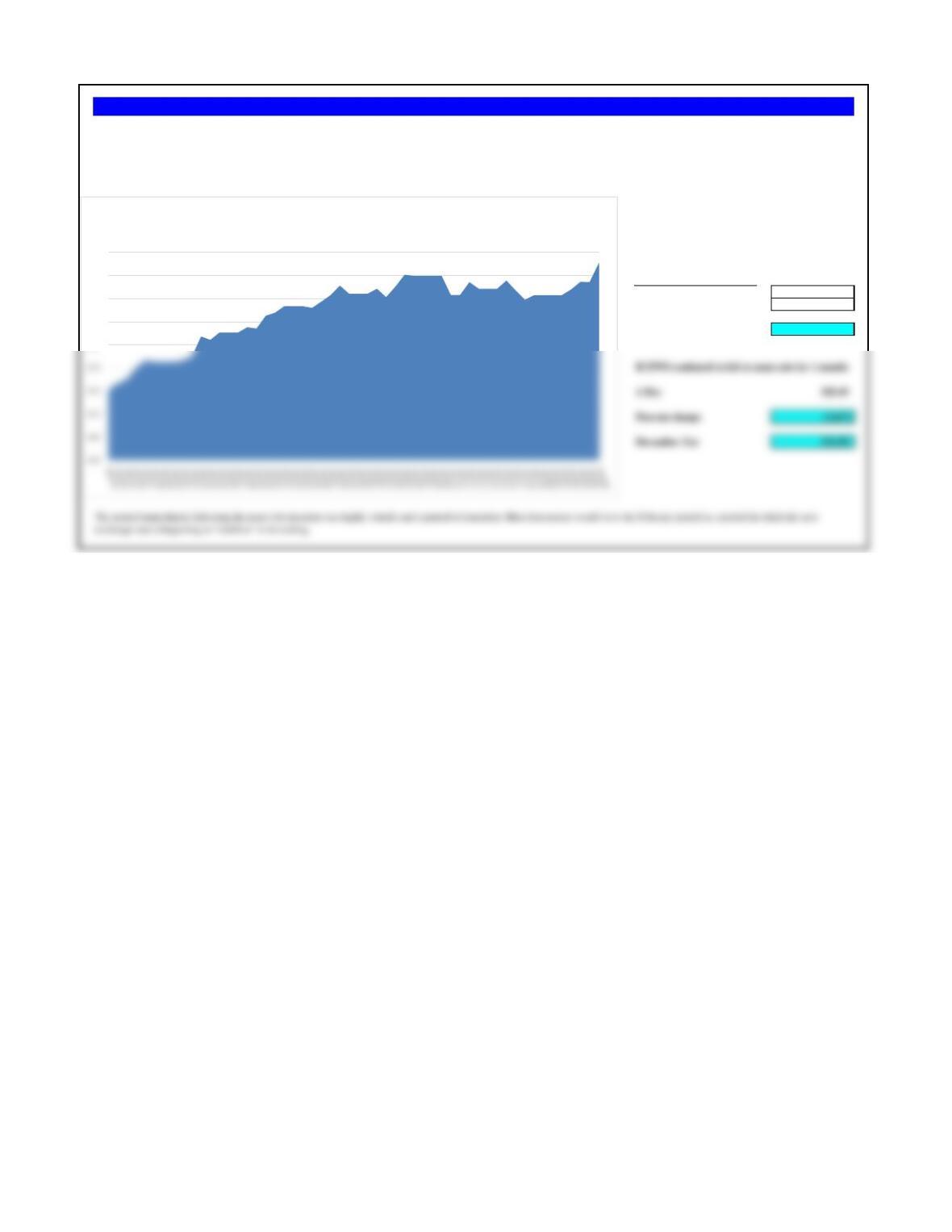

“Eye-balled”

Date Values

October 1st

496.740307

November 4th

515.490775

Percent change -3.64%

exchange rate is beginning to “stabilize” in its trading.

Problem 9.5 Zimbabwean Devaluation

As illustrated in the graph at the top of this page, the Zimbabwe dollar depreciated against the euro from ZWD 460.52 to ZWD 515.49 in a span of three months. After a brief period of high

volatility, the Zimbabwean dollar appeared to settle down into a range varying from 501 to 515 Zimbabwean dollars per euro. If you were forecasting the Zimbabwean dollar further into the

future, to December 5, 2010, how would you use the information in the graphic—the value of the Zimbabwean dollar freely floating in the weeks following devaluation—to forecast its

future value?

490

500

510

520

Problem 9.5: Zimbabwe Devaluation

Zimbabwe dollar (ZWD) = 1.00 Euro (€)

Assumptions Rate Values

Opening spot rate, July 2, 1997 (Bt/$) S1 25.00

Closing spot rate, July 2, 1997 (Bt/$) S2 29.00

Problem 9.6 Bangkok Broken

The Thai baht (Bt) was devalued by the Thai government from BT25/$ to BT29/$ on July 2,

1997. What was the percentage devaluation of the baht?

Assumptions Values

Spot rate, Thursday, January 24, 2008, R$/$ 1.80

Spot rate, Monday, January 26, 2009, R$/$ 2.39

Problem 9.7 Reais Crisis

The Brazilian reais’ (BRL or R$) value was BRL 1.80 to 1.00 USD on Thursday

January 24, 2008, then plunged in value to BRL 2.39 to 1.00 USd on January 26, 2009.

What was the percentage change in its value?

a. What is the value of Conchita’s portfolio as measured in Mexican pesos?

Mikhail’s balances by currency:

(in millions)

US dollars

USD 450

Swiss francs

CHF 200

Mexican pesos

MXN 950.00

Exchange Rates 11/3/1993 11/3/1994 12/5/1994 12/16/1994 12/30/1994 1/30/1995

a. What is the value of Conchita’s portfolio as measured in Mexican pesos?

Portfolio Value as Measured in MXN 11/3/1993 11/3/1994 12/5/1994 12/16/1994 12/30/1994 1/30/1995

MXN account balance 950 950 950 950 950 950

Swiss franc account balance 630 687 689 693 1,000 1,260

b. What is the value of Conchita’s portfolio as measured in Swiss francs?

Portfolio Value as Measured in francs 11/3/1993 11/3/1994 12/5/1994 12/16/1994 12/30/1994 1/30/1995

MXN account balance 302 277 276 274 190 151

Swiss franc account balance 200 200 200 200 200 200

c. What is the value of Conchita’s portfolio as measured in U.S. dollars?

Portfolio Value as Measured in dollars 11/3/1993 11/3/1994 12/5/1994 12/16/1994 12/30/1994 1/30/1995

MXN account balance 452 351 366 366 249 191

d. Which currency demonstrated the greatest fluctuation in total value over the six dates?

Problem 9.8 Conchita’s Dilemma

Conchita Marquez is a famous Mexican entrepreneur with a multi-million-dollar business dealing in copper. In 1994, she decided to take up residence in Switzerland as part of

her longterm retirement plans, which included transferring all her wealth.

In November 1994, Conchita held a portfolio of USD 450 million and CHF 200 million in Swiss banks, in addition to accounts in Mexico holding MXN 950 million. Using the

exchange rate table, answer the following:

Exchange Rates 11/3/1993 11/3/1994 12/5/1994 12/16/1994 12/30/1994 1/30/1995

Mexican peso per U.S. dollar 3.150 3.433 3.443 3.464 5.000 6.300

Mexican peso per Swiss franc 2.104 2.707 2.596 2.598 3.820 4.974

U.S. dollar per Swiss franc 0.6679 0.7880 0.7540 0.7500 0.7640 0.7890

Percentage Change 11/3/1993 11/3/1994 12/5/1994 12/16/1994 12/30/1994 1/30/1995

11/3/1993-12/16/1994

MXN vs Swiss franc, period -45.5%

MXN vs US dollar, period -45.6%

Problem 9.9 La Conquista—The Mexican Dance

Calculate the percentage change in the value of the peso for the three different cross-rates shown in the table for the six dates. Did the peso fall further against

the U.S. dollar or the Swiss franc?

a. Dividend received in USD in Nov 1994 Values

Dividend MXN 30,000,000,000.00

Spot rate, November 1994, MXN = 1 USD 3.44

USD 8,713,331,397.04

Problem 9.10 BP and Mexicana Oil 1995

BP (UK) and Mexicana Oil (Mexico) severed a long-term joint venture in 1993, with Mexicana buying

out BP with $75 billion in cash and a 30% interest (equity interest) in Mexicana itself. Mexicana financed

a large part of the buyout by borrowing heavily. The following year, November 1994, BP received a

dividend on its ownership interest in Mexicana of MXN 30 billion.

But Mexicana’s performance had been declining, as was the Mexican peso. The winter of 1994–1995 in

Europe was a relatively mild one and Europe’s purchases of Mexicana’s oil output had fallen, as had the

price of oil. Mexicana’s total sales were down, and the peso had clearly fallen dramatically (see previous

table). And to add debt to injury, Mexicana was due to make a payment of USD 22.5 billion in 1995 on

its debt from the BP buyout.

a. Assuming a spot rate of RUB 34.78 = 1.00 USD in July 2014, how much was the dividend paid to BP

in U.S. dollars?

b. If Rosneft were to pay the same dividend to BP in July 2015, and the spot rate at that time was RUB

75 = 1.00 USD, what would BP receive in U.S. dollars?

Russian economy into recession, and the spot rate was RUB 75 = 1.00 USD in July 2015, what might

BP’s dividend be in July 2015?

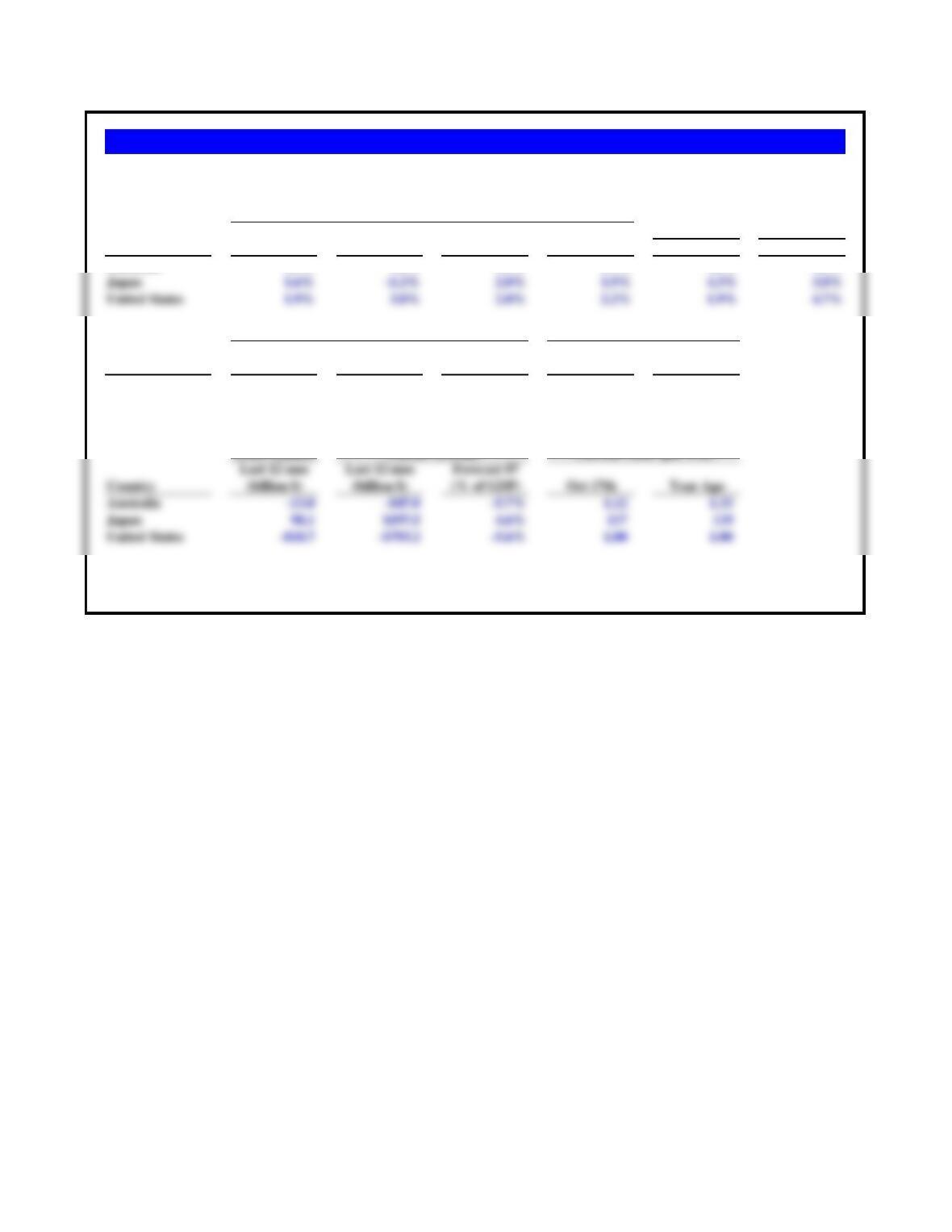

Use the following data in answering problems 9.11-9.16.

Industrial Unemployment

Forecast Forecast Production Rate

Country Latest Qtr Qtr* 2007e 2008e Recent Qtr Latest

Forecast 3-month 1-yr Govt

Country Year Ago Latest 2007e Latest Latest

Australia 4.0% 2.1% 2.4% 6.90% 6.23%

Japan 0.9% -0.2% 0.0% 0.73% 1.65%

United States 2.1% 2.8% 2.8% 4.72% 4.54%

Source: Data abstracted from The Economist , October 20, 2007, print edition. Unless otherwise noted, percentages are percentage changes over one-

year. Rec Qtr = recent quarter. Values for 2007e are estimates or forecasts.

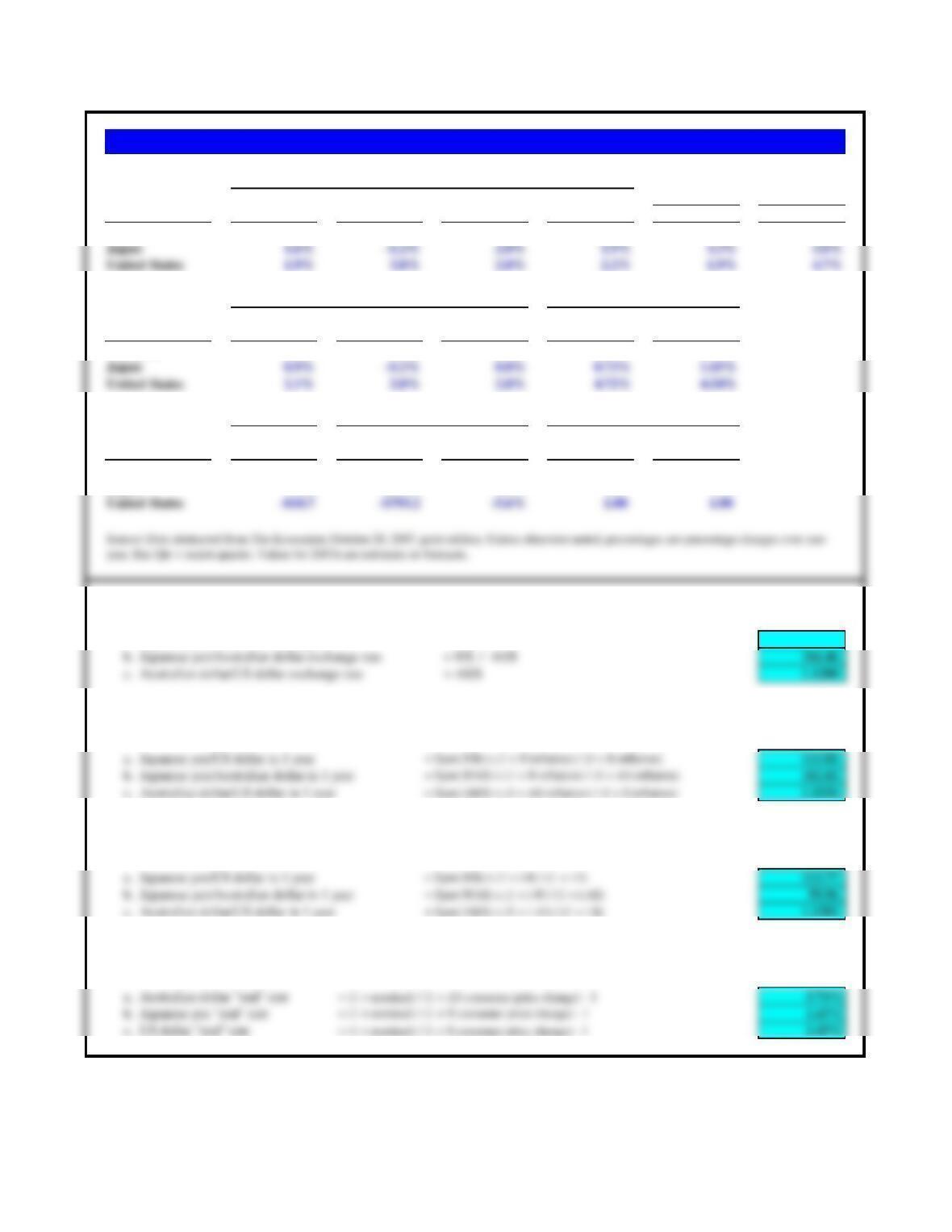

Forecasting the Pan-Pacific Pyramid:

Gross Domestic Product

Consumer Prices

Interest Rates

Industrial Unemployment

Forecast Forecast Production Rate

Country Latest Qtr Qtr* 2007e 2008e Recent Qtr Latest

Australia 4.3% 3.8% 4.1% 3.5% 4.6% 4.2%

Forecast 3-month 1-yr Govt Bond

Country Year Ago Latest 2007e Latest Latest

Australia 4.0% 2.1% 2.4% 6.90% 6.23%

Trade Balance

Last 12 mos Last 12 mos Forecast 07

Country (billion $) (billion $) (% of GDP) Oct 17th Year Ago

Australia -13.0 -$47.0 -5.7% 1.12 1.33

Japan 98.1 $197.5 4.6% 117 119

11. Current spot rates. What are the current spot exchange rates for the following cross rates?

a. Japanese yen/US dollar exchange rate

= ‘¥/$ 117.00

Problems 9.11-9.14 Forecasting the Pan-Pacific Pyramid

Gross Domestic Product

Consumer Prices

Interest Rates

13. International Fischer forecasts. Asssuming International Fisher applies to the coming year, forecast the following future spot

exchange rates using the government bond rates for the respective country currencies:

14. Implied real interest rates. If the nominal interest rate is the government bond rate, and the current change in consumer prices is

used as expected inflation, calculate the implied “real” rates of interest by currency.

Current Account

Current Units (per US$)

12. Purchasing power parity forecasts. Assuming purchasing power parity, and assuming that the forecasted change in consumer

prices is a good proxy of predicted inflation, forecast the following cross rates:

Industrial Unemployment

Forecast Forecast Production Rate

Country Latest Qtr Qtr* 2007e 2008e Recent Qtr Latest

Australia 4.3% 3.8% 4.1% 3.5% 4.6% 4.2%

Japan 1.6% -1.2% 2.0% 1.9% 4.3% 3.8%

United States 1.9% 3.8% 2.0% 2.2% 1.9% 4.7%

Forecast 3-month 1-yr Govt Bond

Country Year Ago Latest 2007e Latest Latest

Trade Balance

Last 12 mos Last 12 mos Forecast 07

Country (billion $) (billion $) (% of GDP) Oct 17th Year Ago

Australia -13.0 -$47.0 -5.7% 1.12 1.33

Japan 98.1 $197.5 4.6% 117 119

15. Forward rates. Using the spot rates and three-month interest rates above, calculate the 90-day forward rates for:

a. Japanese yen/US dollar exchange rate = Spot (¥/$) x (1 + i¥ 3 month) / (1 + i$ 3 month) 115.85

b. Japanese yen/Australian dollar exchange rate = Spot (¥/A$) x (1 + i¥ 3 month) / (1 + iA$ 3 month) 102.88

c. Australian dollar/US dollar exchange rate = Spot (A$/$) x (1 + A$ 3 month) / (1 + i$ 3 month) 1.1260

Note: All interest rates need to be adjusted for a 90 day period of a 360 day year for the calculation.

16. Real economic activity and misery. Calculate the country’s Misery Index (unemployment + inflation) and then use it like interest

differentials to forecast the future spot exchange rate, one year into the future.

Current Account

Current Units (per US$)

year. Rec Qtr = recent quarter. Values for 2007e are estimates or forecasts.

Problems 9.15-9.16 Forecasting the Pan-Pacific Pyramid

Gross Domestic Product

Consumer Prices

Interest Rates

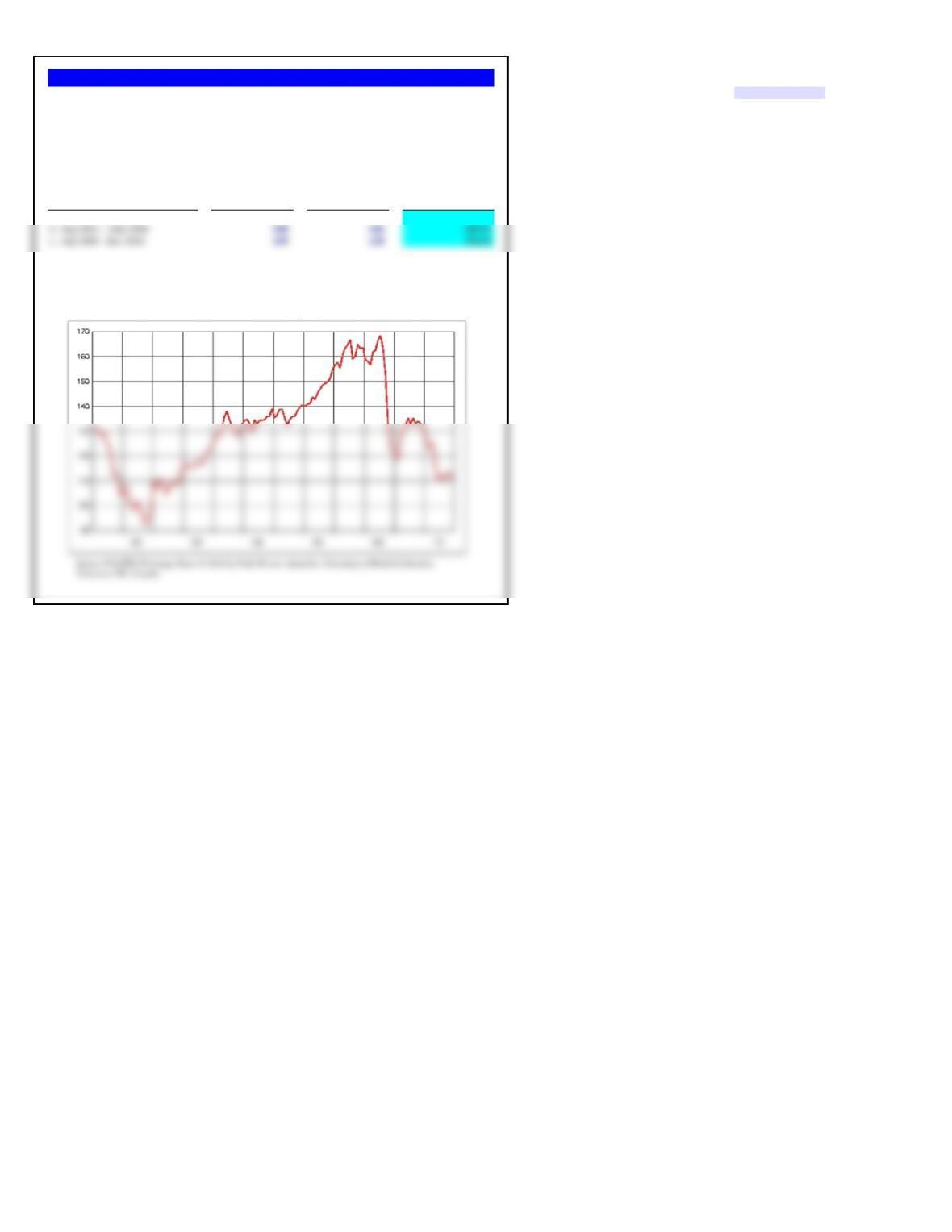

Change in the

Starting Value Ending Value value of the yen

Time Period

(¥/€) (¥/€)(percent)

a. Jan 1999 – Aug 2001 131 109 20.2%

Problem 9.17 The Rising Sun and Europe

Percent change = ( S1 – S2 ) ÷ ( S2 )

The Japanese yen-euro cross rate is one of the more significant currency values for global trade and commerce.

The graphic at right shows this cross-rate from when the euro was launched in January 1999 through the end-of-

year 2010. Estimate the change in the value of the yen over the following three periods of change.

Monthly Average Exchange Rates:

Japanese Yen per European Euro