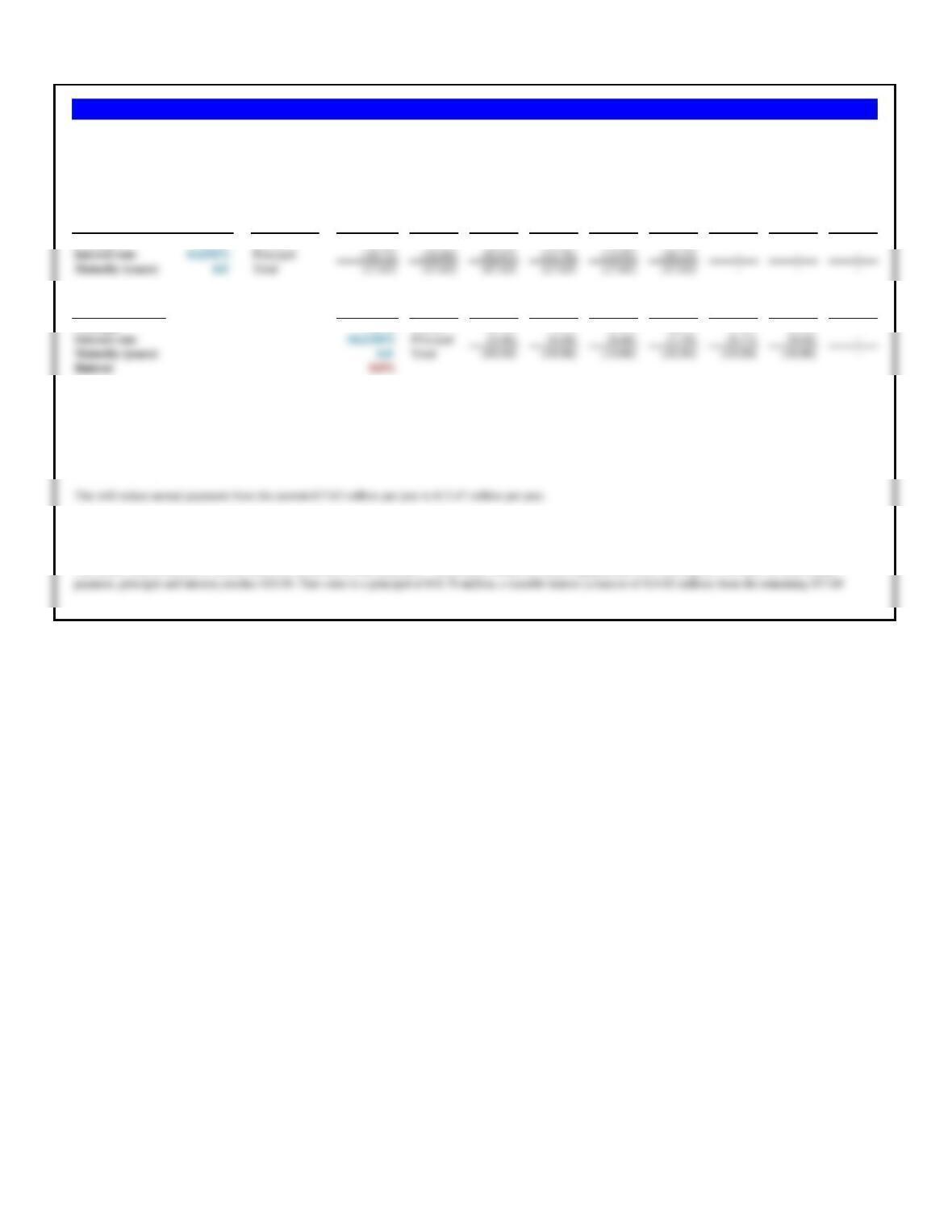

Assumptions 3-Month T-Bill 6-Month T-Bill

Treasury bill, face value $10,000.00 $10,000.00

Price at sale $9,993.93 $9,976.74

b. Simple yield 0.0607% 0.2331%

Discount on sale is the difference between the face value of the security and the

price it is sold at auction.

Problem 8.1 T-Bill Yields 2009

The interest yields on U.S. Treasury securities in early 2009 fell to very low levels

as a result of the combined events surrounding the global financial crisis. Calculate

the simple and annualized yields for the 3-month and 6-month Treasury bills

auctioned on March 9, 2009 listed here.

Simple yield is found by dividing the discount (the dollar return to the investor on

maturity) by the price paid on purchase.

3-month 3-Month TED Overnight 3-month 3-Month 3-month 3-Month TED 3-month 3-Month TED

Date Pound LIBOR UK Bond Yield Spread Date USD LIBOR Pound LIBOR UK Bond Yield Date Pound LIBOR UK Bond Yield Spread Date Pound LIBOR UK Bond Yield Spread

9/8/2008 5.74% 5.10% 0.64% 9/29/2008 6.26% 4.90% 1.36% 9/8/2008 5.74% 5.10% 9/29/2008 6.26% 4.90%

9/9/2008 5.73% 5.10% 0.63% 9/30/2008 6.30% 4.85% 1.45% 9/9/2008 5.73% 5.10% 9/30/2008 6.30% 4.85%

9/10/2008 5.72% 5.09% 0.63% 10/1/2008 6.31% 4.76% 1.55% 9/10/2008 5.72% 5.09% 10/1/2008 6.31% 4.76%

9/18/2008 5.98% 5.06% 0.91% 10/9/2008 6.28% 4.33% 1.96% 9/18/2008 5.98% 5.06% 10/9/2008 6.28% 4.33%

9/19/2008 6.00% 5.04% 0.96% 10/10/2008 6.29% 4.33% 1.96% 9/19/2008 6.00% 5.04% 10/10/2008 6.29% 4.33%

9/22/2008 6.01% 5.03% 0.99% 10/13/2008 6.27% 4.35% 1.92% 9/22/2008 6.01% 5.03% 10/13/2008 6.27% 4.35%

a. Calculate the U.K. Ted spread—the difference between the two market rates shown in the table—in September and October 2008

The spread between overnight 3-month Pound LIBOR and the 3-month U.K. Treasury bond yield are calculated in the two columns above.

b. On what date is the spread the narrowest? The widest?

Problem 8.2 TED Spread in the Global Credit Crisis

During financial crises, short-term interest rates will often change quickly (typically up) as indications that markets are under severe stress. The

interest rates shown in the following table are for selected dates in September-October 2008. Different publications define the TED Spread in

different ways. Here, we focus on the TED spread on U.K. interest rates. One measure is the differential between the 3-month British pound

LIBOR interest rate and the 3-month U.K. Government bond yield.

c. When the spread widens dramatically, presumably demonstrating some sort of financial anxiety, which of the rates moves the most and

why?

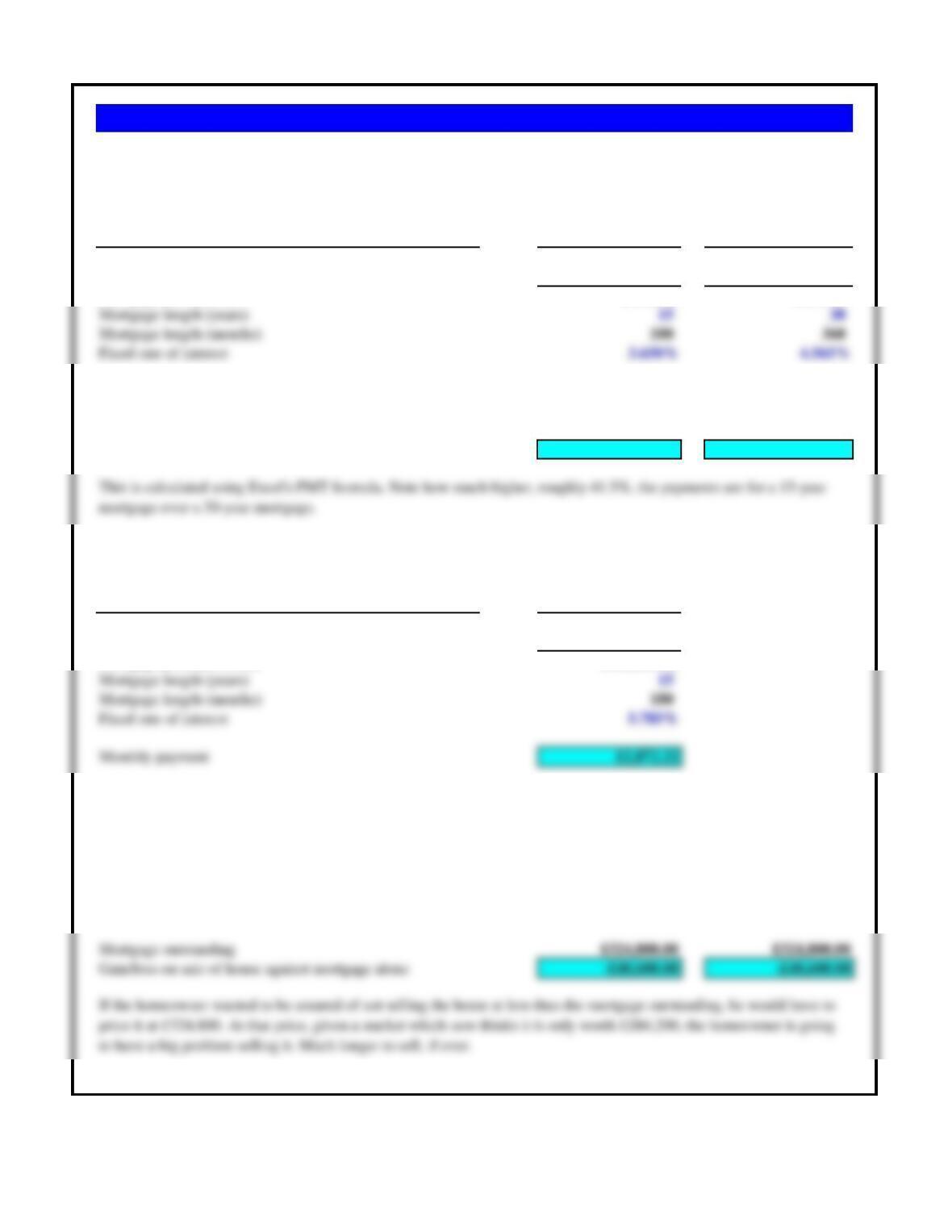

Assumptions 15-Year Mortgage 30-Year Mortgage

Price of house at purchase £406,000 £406,000

Less down-payment (20%) -£81,200 -£81,200

Mortgage principal (£)£324,800 £324,800

Monthly payment (amortizing loan, all equal payments) £2,346 £1,658

Assumptions 15-Year Mortgage

Price of house at purchase £406,000.00

Less down-payment (10%) 15% -£60,900.00

Mortgage principal (US$) £345,100.00

Monthly payment £2,872.22

Home’s original value £406,000.00 £406,000.00

Fall in value -30.0% -30.0%

New home market value £284,200.00 £284,200.00

Problem 8.3 Stapleton’s Mortgage

Frank Stapleton pays £406,000 for a four-bedroom bungalow on the outskirts of Edinburgh, Scotland. He plans to make

a 20% down payment but is having trouble deciding whether he wants a 15-year fixed rate (3.650%) or a 30-year fixed

rate (4.565%) mortgage.

a. What is the monthly payment for both the 15– and 30-year mortgages, assuming a fully amortizing loan of

equal payments for the life of the mortgage? Use a spreadsheet calculator for the payments.

b. Assume that instead of making a 20% down payment, he makes a 15% down payment, finances

the remainder at 5.785% fixed interest for 15 years. What is his monthly payment?

c. Assume that the bungalow’s total value falls by 30%. If Frank sells the house at the new market value, what

will be his gain or loss on the home and mortgage, assuming all the mortgage principal remains? Use the same

assumptions as in part (a).

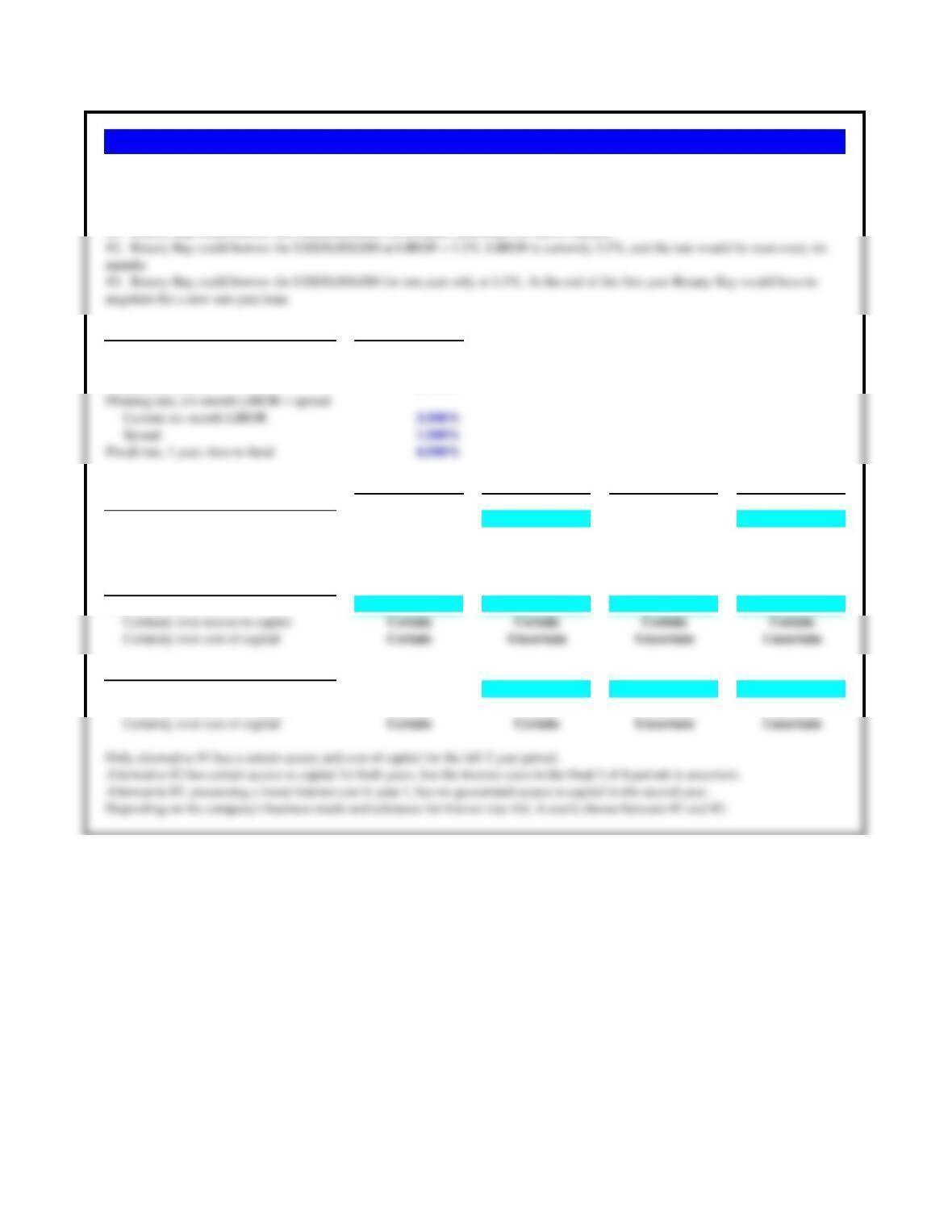

Assumptions Values

Principal borrowing need

30,000,000$

Maturity needed, in years

2.00

Fixed rate, 2 years

5.000%

First 6-months Second 6-months Third 6-months Fourth 6-months

#1: Fixed rate, 2 years

Interest cost per year

1,500,000$ 1,500,000$

Certainty over access to capital

Certain Certain Certain Certain

Certainty over cost of capital

Certain Certain Certain Certain

#2: Floating rate, six-month LIBOR + spread

Interest cost per year

750,000$ 750,000$ 750,000$ 750,000$

Certain Certain Certain Certain

#3: Fixed rate, 1 year, then re-fund

Interest cost per year

1,350,000$ ??? ???

Certainty over access to capital

Certain Certain Uncertain Uncertain

Certain Certain Uncertain Uncertain

#3. Botany Bay could borrow the US$30,000,000 for one year only at 4.5%. At the end of the first year Botany Bay would have to

negotiate for a new one-year loan.

#2. Botany Bay could borrow the US$30,000,000 at LIBOR + 1.5%. LIBOR is currently 3.5%, and the rate would be reset every six

Problem 8.4 BBC (Australia)

Botany Bay Corporation (BBC) of Australia seeks to borrow US$30,000,000 in the Eurodollar market. Funding is needed for two

years. Investigation leads to three possibilities. Compare the alternatives and make a recommendation.

Assumptions Values

Interest rate futures, closing price 93.07

Effective yield on interest rate futures 6.930%

Floating Rate is Floating Rate is

Chrysler’s interest rate payments with futures 6.000% 8.000%

Three Months From Now

Problem 8.5 DaimlerChrysler Debt

Chrysler LLC, the now privately held company sold-off by DaimlerChrysler, must pay floating rate interest

three months from now. It wants to lock in these interest payments by buying an interest rate futures

contract. Interest rate futures for three months from now settled at 93.07, for a yield of 6.93% per annum.

Assumptions Values

Notional principal

5,000,000$

LIBOR, per annum

4.000%

2.000%

7.000%

First Second Third Fourth

Interest & Swap Payments 6-months 6-months 6-months 6-months

a. LIBOR increases 50 basis pts/6 months 0.500%

Expected LIBOR

4.500% 5.000% 5.500% 6.000%

Current loan agreement:

-2.250% -2.500% –2.750% -3.000%

-1.000% -1.000% –1.000% -1.000%

-3.250% -3.500% –3.750% -4.000%

Swap Agreement:

Pay fixed (for 6-months)

-3.500% -3.500% –3.500% -3.500%

Receive floating (LIBOR for 6 months)

2.250% 2.500% 2.750% 3.000%

Net interest (loan + swap) -4.500% -4.500% -4.500% -4.500%

Swap savings?

b. LIBOR decreases 25 basis pts/6 months -0.250%

Expected LIBOR

3.750% 3.500% 3.250% 3.000%

Current loan agreement:

Expected LIBOR (for 6 months)

-1.875% -1.750% –1.625% -1.500%

Spread (for 6 months)

-1.000% -1.000% –1.000% -1.000%

Expected interest payment

-2.875% -2.750% –2.625% -2.500%

Swap Agreement:

-3.500% -3.500% –3.500% -3.500%

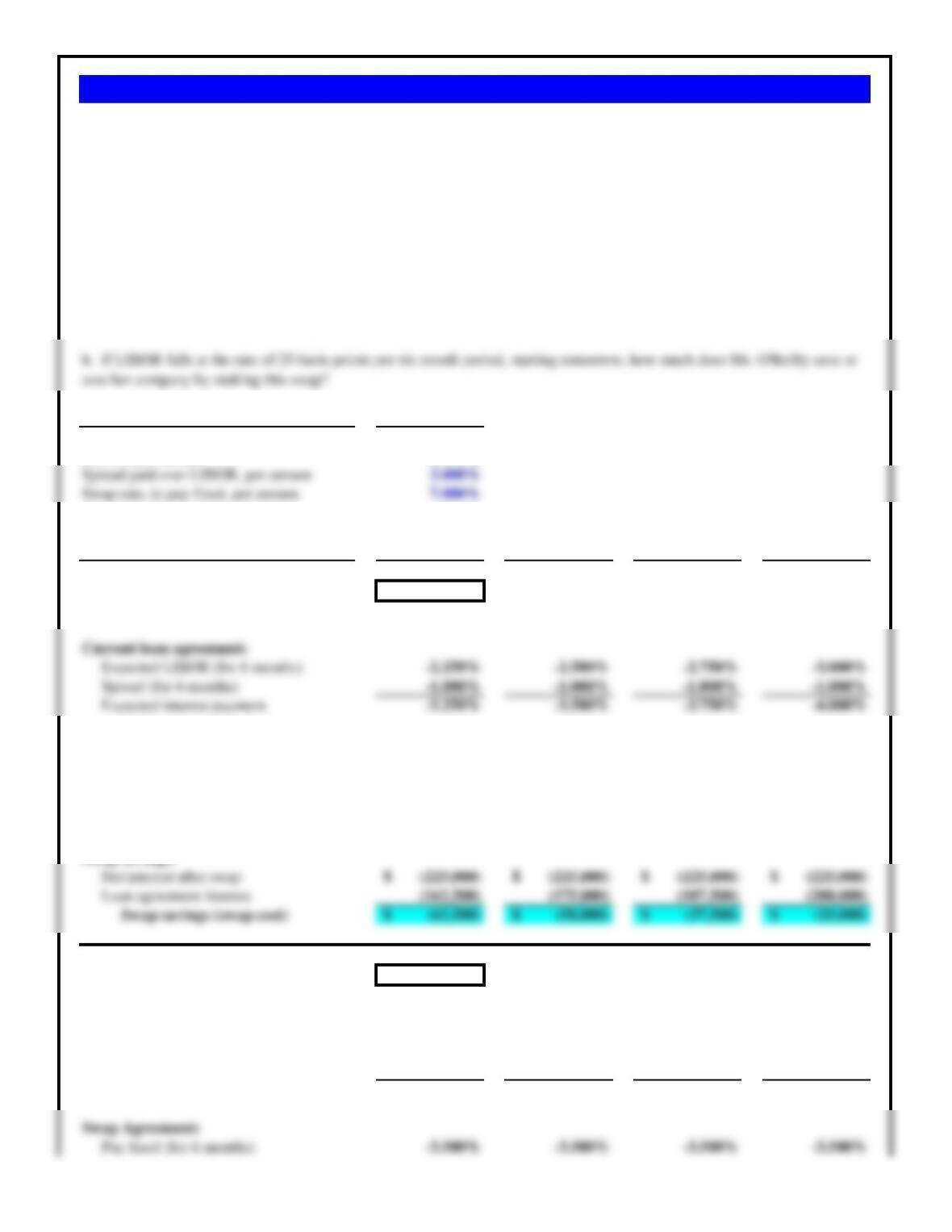

a. If LIBOR rises at the rate of 50 basis points per six month period, starting tomorrow, how much does Ms. O’Reilly save or

cost her company by making this swap?

b. If LIBOR falls at the rate of 25 basis points per six month period, starting tomorrow, how much does Ms. O’Reilly save or

cost her company by making this swap?

Problem 8.6 O’Reilly and CB Solutions

Heather O’Reilly, the treasurer of CB Solutions, believes interest rates are going to rise, so she wants to swap her future

floating rate interest payments for fixed rates. At present she is paying LIBOR + 2% per annum on $5,000,000 of debt for the

next two years, with payments due semiannually. LIBOR is currently 4.00% per annum. Ms. O’Reilly has just made an interest

payment today, so the next payment is due six months from today.

Ms. O’Reilly finds that she can swap her current floating rate payments for fixed payments of 7.00% per annum. (CB

Solution’s weighted average cost of capital is 12%, which Ms. O’Reilly calculates to be 6% per six month period,

compounded semiannually).

Receive floating (LIBOR for 6 months)

1.875% 1.750% 1.625% 1.500%

Net interest (loan + swap) -4.500% -4.500% -4.500% -4.500%

Swap savings?

Net interest after swap

(225,000)$ (225,000)$ (225,000)$ (225,000)$

In both cases CB Solutions is suffering higher total interest costs as a result of the swap.

Loan Payments 1 2 3 4

Principal €150.00 Interest (3.40) (2.58) (1.74) (0.88)

If the interest rate used was 3.45%, the annual payment would be €40.79 million.

Loan Payments 1 2 3 4

Principal €150.00 Interest (5.18) (3.95) (2.68) (1.36)

If the interest rate used was 3.75%, the annual payment would be $32,920,000.

Loan Payments 1 2 3 4

Principal €150.00 Interest (5.63) (4.30) (2.92) (1.48)

Rate Annual Payment Cum Difference

2.269% €39,651,047.32 —–

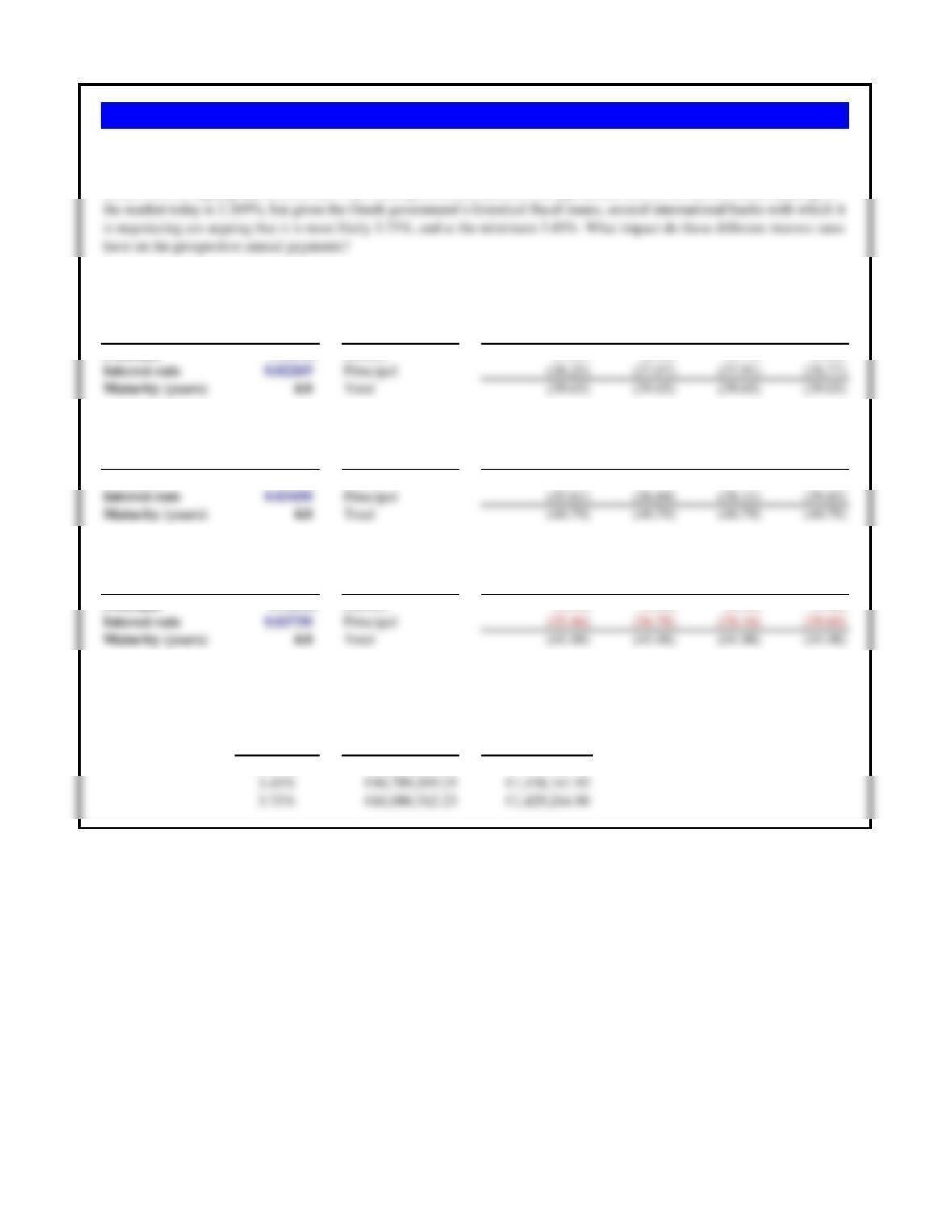

Problem 8.7 Sovereign Debt Negotiations

The Greek government is considering a €150 million loan for a four-year maturity. It will be an amortizing loan, meaning that

the interest and principal payments in total, nnually, to a constant amount over the maturity of the loan. There is, however, a

debate over the appropriate interest rate. The Greek government believes the appropriate rate for its current credit standing in

The sovereign borrower believes the appropriate rate to be 2.269%, which would generate the following amortized (principal

and interest) payments, an annual payment of €39.65 million.

So ‘what impact’ do higher rates have? Well the obvious answer is only a marginal increase in the annual payment, given the

short maturity of the obligation. But if you are a borrower, every little bit matters. And if you are sovereign borrower which is

heavily indebted and in a position of a potential default, every little bit is critical.

Loan 0 Payments 1 2 3 4 5 6

Principal $220 Interest (26.950) (23.650) (19.946) (15.788) (11.120) (5.881)

Interest rate 12.250% Principal (26.939) (30.239) (33.943) (38.101) (42.769) (48.008)

Maturity (years) 6.0 Total (53.889) (53.889) (53.889) (53.889) (53.889) (53.889)

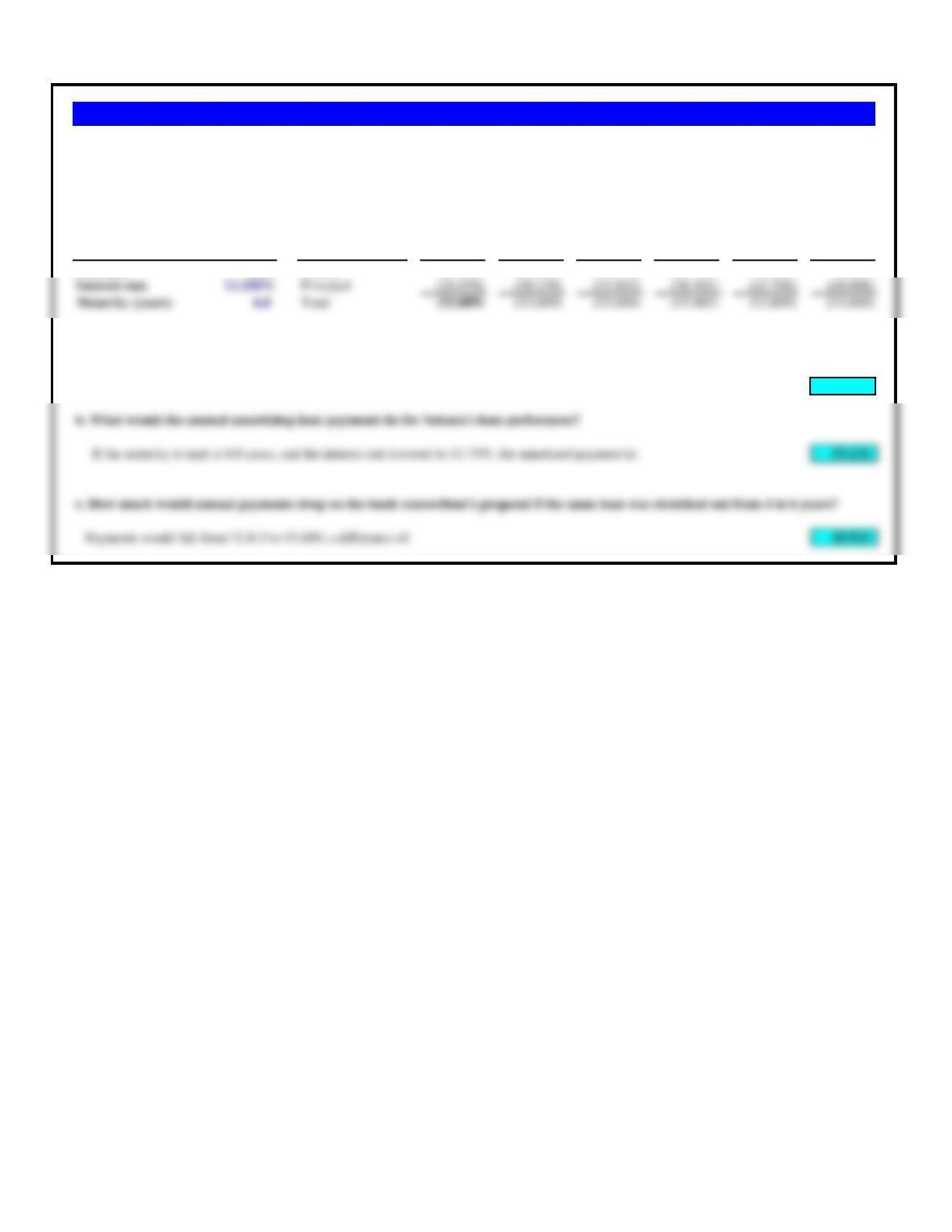

a. What would the annual amortizing loan payments be for the bank consortium’s proposal?

If the maturity in years is shortened to 4.0 years, the amortized payment rises to:

72.813

b. What would the annual amortizing loan payments be for Sahara’s loan preferences?

53.131

18.924

The country of Sahara is negotiating a new loan agreement with a consortium of international banks. Both sides have a tentative agreement on the

principal — $220 million. But there are still wide differences of opinion on the final interest rate and maturity. The banks would like a shorter loan,

4 years in length, while Sahara would prefer a long maturity of 6 years. The banks also believe the interest rate will need to be 12.250% per annum,

but Sahara believes that is too high, arguing for 11.750%.

Problems 8.8 Saharan Debt Negotiations

Loan 0 Payments 1 2 3 4 5 6 7 8 9

Interest rate 8.6250% Principal (10.735) (11.661) (12.666) (13.759) (14.945) (16.234) – – –

Maturity (years) 6.0 Total (17.635) (17.635) (17.635) (17.635) (17.635) (17.635) – – –

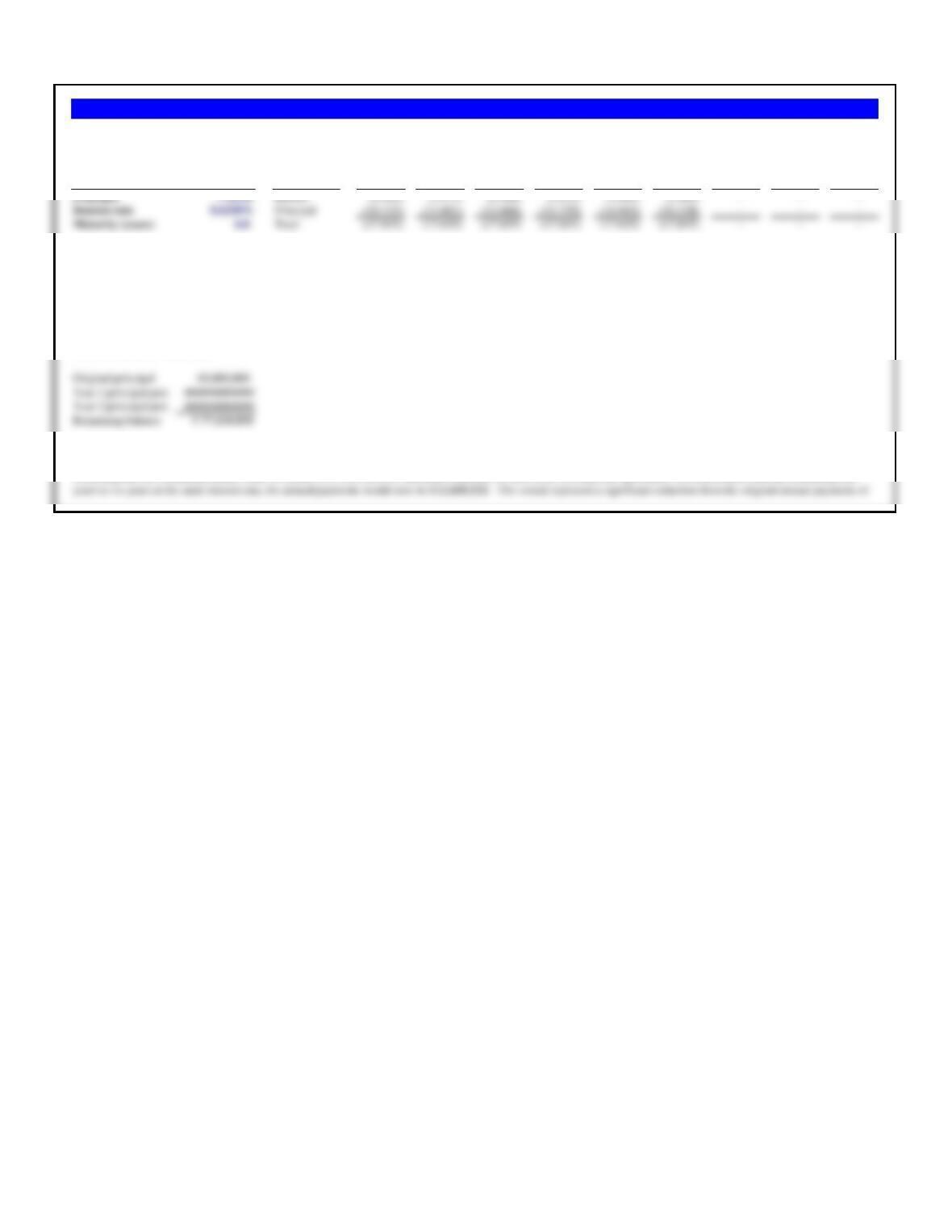

a. What were Delos’s annual principal and interest payments under the original loan agreement?

The original interest and principal payments are shown above, with a constant annual payment for the six-year period of €17.635 million (€17,634,664 to be exact).

b. After two years debt-service, how much of the principal is still outstanding?

c. If the loan was restructured to extend another two years, what would the annual payments — principal and interest — be?

Problems 8.9 Delos Debt Renegotiations (A)

Delos borrowed €80 million two years ago. The loan agreement, an amortizing loan, was for 6 years at 8.625% interest per annum. Delos has successfully completed two years

of debt-service, but now wishes to renegotiate the terms of the loan with the lender to reduce its annual payments.

After two years of regular debt service, the remaining principal would be the original €80,000,000 less the sume of the first year and second year principal payments of

€10,734,664 and €11,660,529.

Loan 0 Payments 1 2 3 4 5 6 7 8 9

Principal € 80.00 Interest (6.90) (5.97) (4.97) (3.88) (2.69) (1.40) – – –

Loan 0 Payments 1 2 3 4 5 6 7

The easiest way to find this is by trial and error in the above loan calculator — continually reduce the remaining principal (first showing €57.60) until the total annual

payment, principal and interest, reaches €10.00. That value is a principal of €42.78 million, a sizeable haircut (a haircut of €14.82 million) from the remaining €57.60

Problem 8.10 Delos Debt Renegotiations (B)

Delos is continuing to renegotiate its prior loan agreement (€80 million for 6 years at 8.625% per annum), two years into the agreement. Delos is now facing serious tax

revenue shortfalls, and fears for its ability to service its debt obligations. So it has decided to get more aggressive, and has gone back to its lenders with a request for a

‘haircut’, a reduction in the the remaining loan amount. The banks have, so far, only agreed to restructure the loan agreement for another two years (new loan of 6 years on

the remaining principal balance) but at an interest rate a full 200 basis points higher, 10.625%.

a. If Delos accepts the current bank proposal of the remaining principal for 6 years (extending the loan an additional 2 years since 2 of the original 6 years have

already passed), but at the new interest rate, what are its annual payments going to be? How much relief does this provide Delos on annual debt-service?

After the the first wo years of the original loan agreement, the principal of €80.00 has been reduced by –€10.73 (year 1) and – €11.66 (year 2), for a remaining principal

balance of €57.60.

b. Delos’s demands for a haircut are based on getting the new annual debt service payments down. If Delos does agree to the new loan terms, what size of haircut

should it try and get from its lenders to get its payments down to €10 million per year?