Expected Chg

Assumptions Values in LIBOR

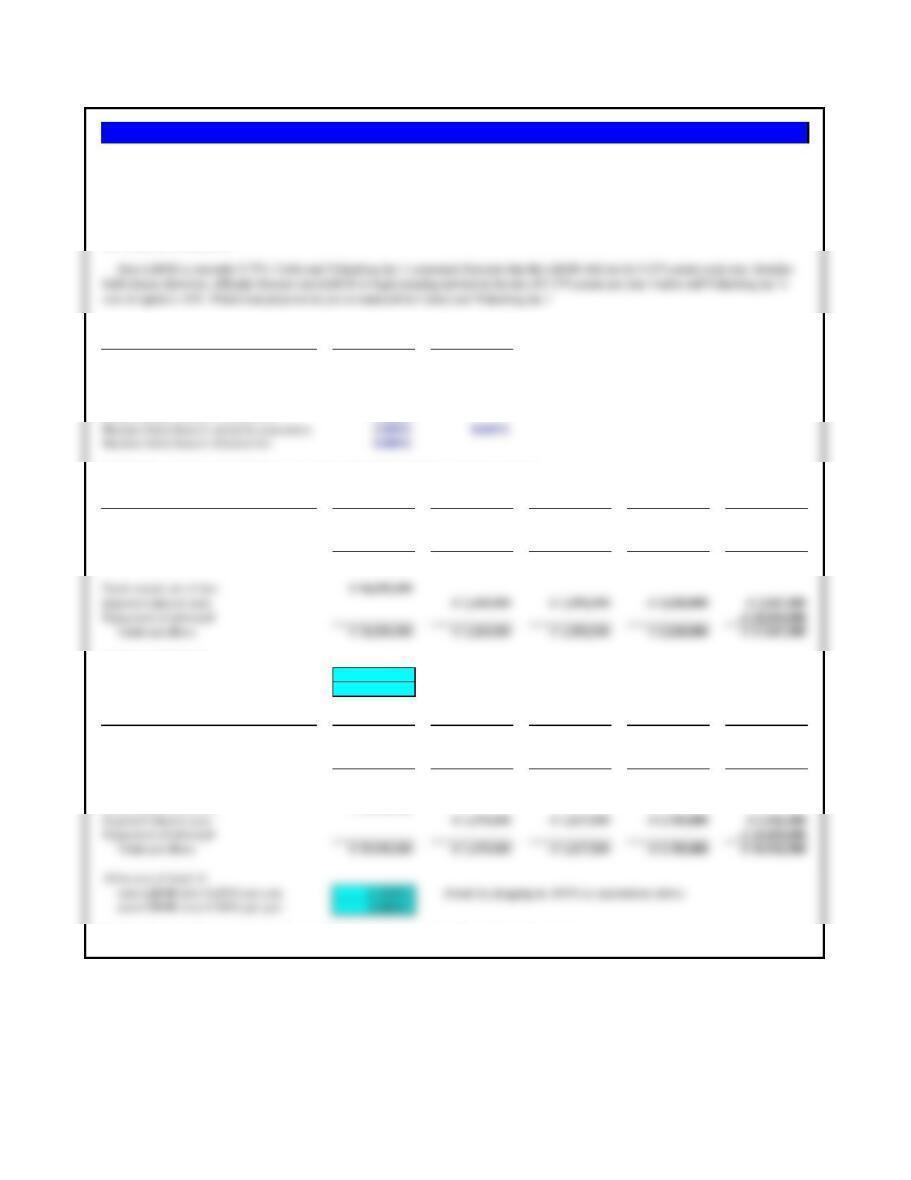

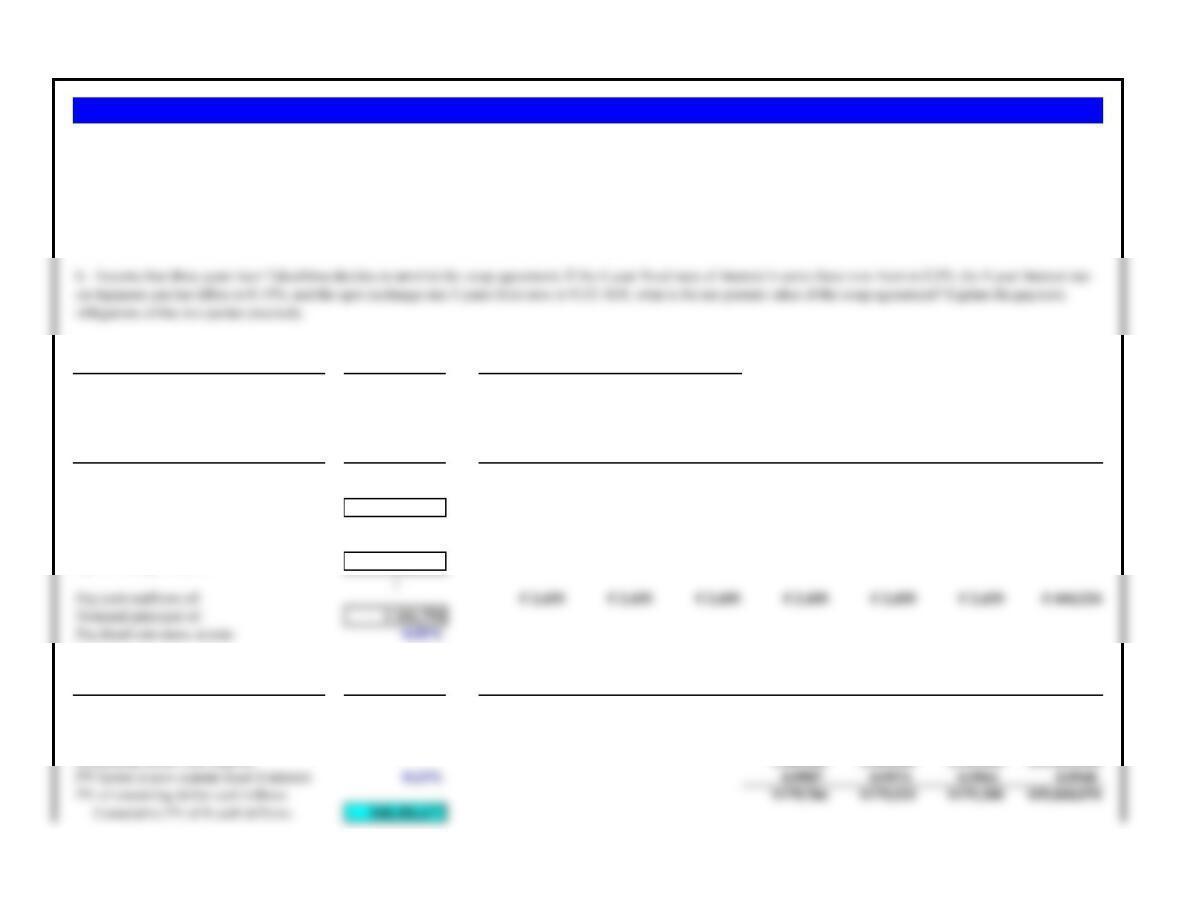

Principal borrowing need

€ 35,000,000

Maturity needed, in years

4.00

Current euro-LIBOR

0.750%

Caixa Brasilia Federal‘s spread & expectation

2.500% 0.650%

2.000%

3.000% 0.450%

0.000%

Raid Gauloises must evaluate both loan proposals under both potential interest rate scenarios.

Caixa Brasilia Federal Loan Proposal Year 0 Year 1 Year 2 Year 3 Year 4

Expected interest rates & payments:

Expected euro-LIBOR

0.750% 1.400% 2.050% 2.700% 3.350%

Bank spread

2.500% 2.500% 2.500% 2.500% 2.500%

Interest rate

3.250% 3.900% 4.550% 5.200% 5.850%

All-in-cost of funds if:

euro-LIBOR rises 0.650% per year

5.4016%

euro-LIBOR rises 0.450% per year

4.9109% Found by plugging in .450% in expectations above.

.

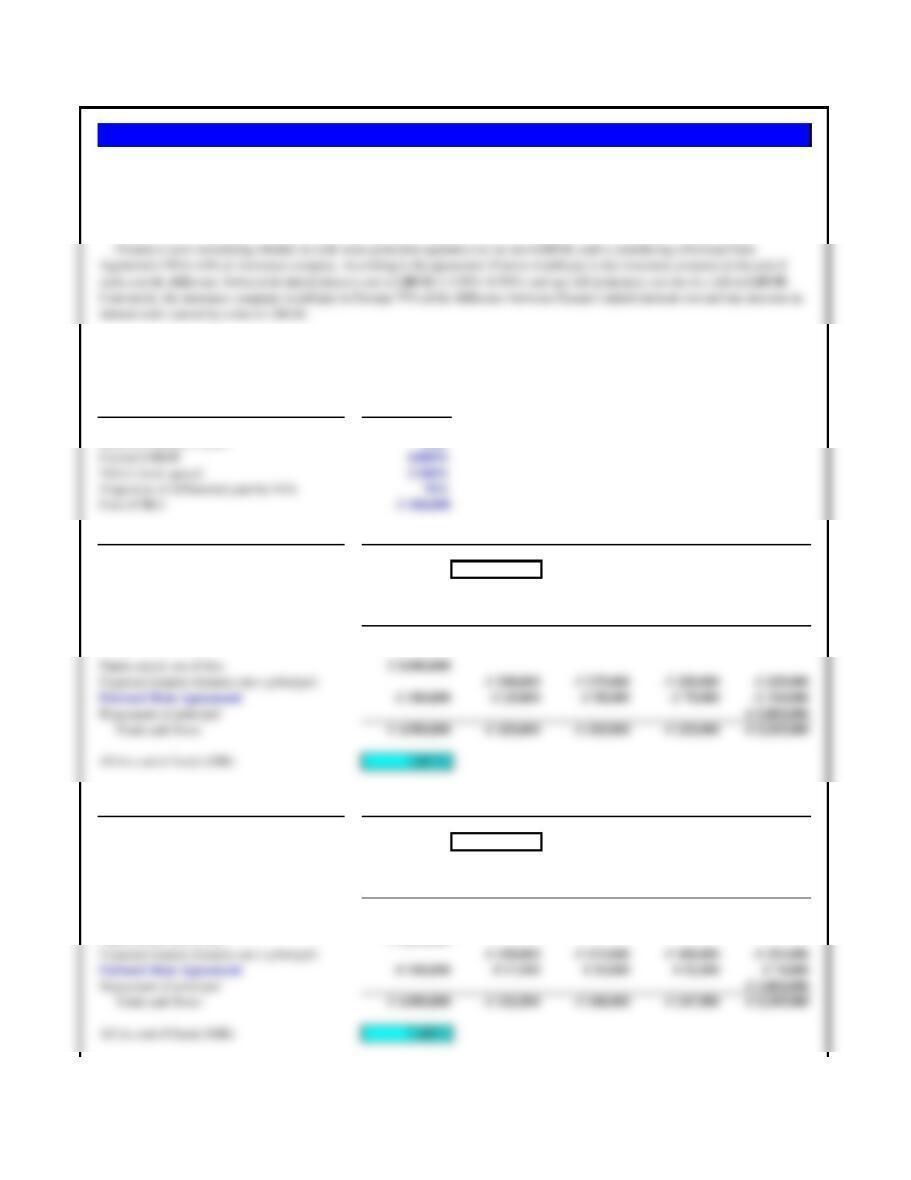

Brasilao Safra Banco Loan Proposal Year 0 Year 1 Year 2 Year 3 Year 4

Expected interest rates & payments:

Expected euro-LIBOR

0.750% 1.200% 1.650% 2.100% 2.550%

Bank spread

3.000% 3.000% 3.000% 3.000% 3.000%

Interest rate

3.750% 4.200% 4.650% 5.100% 5.550%

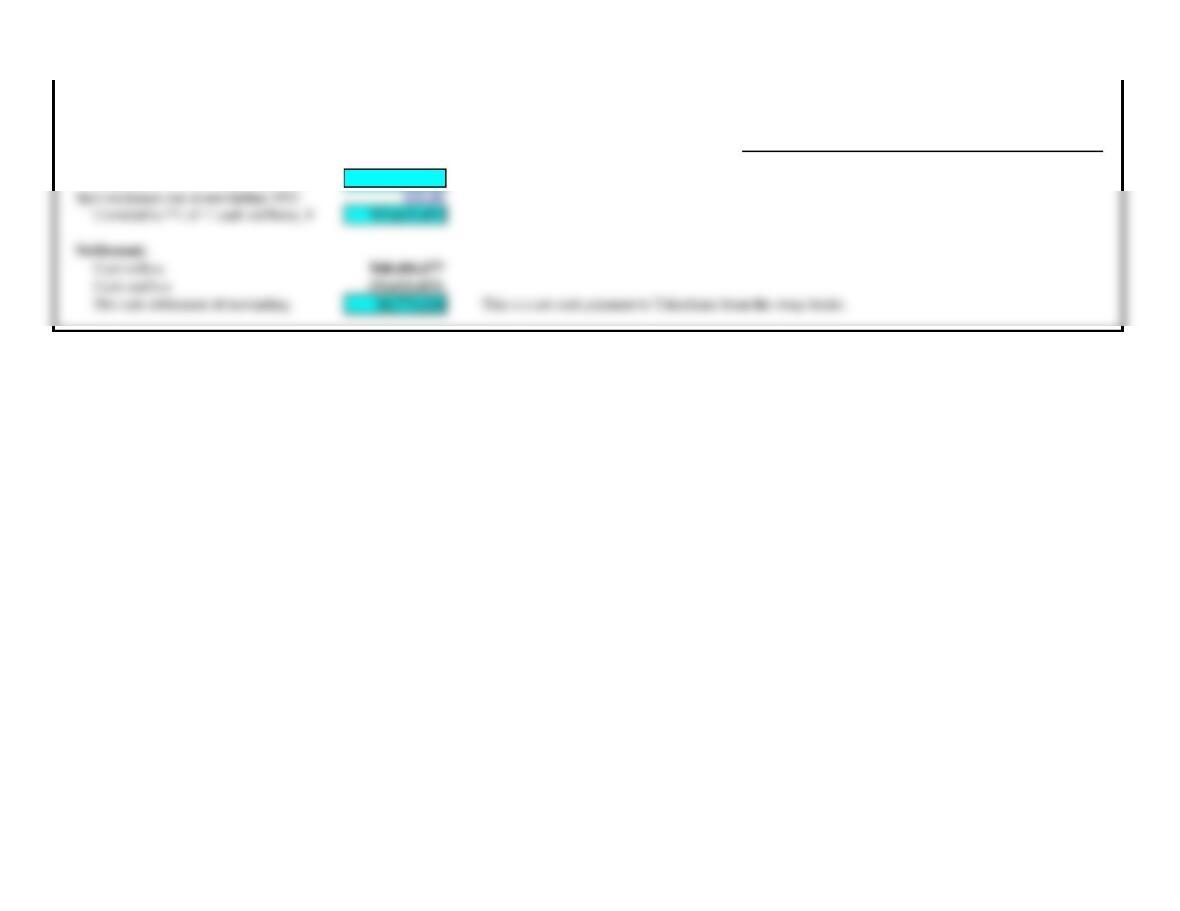

5.3328% Found by plugging in .650% in expectations above.

4.8484%

The Brasilao Safra Banco loan proposal is actually lower all-in-cost under either interest rate scenario.

cost of capital is 10%. Which loan proposal do you recommend for Carlos and Wilmsberg Inc.?

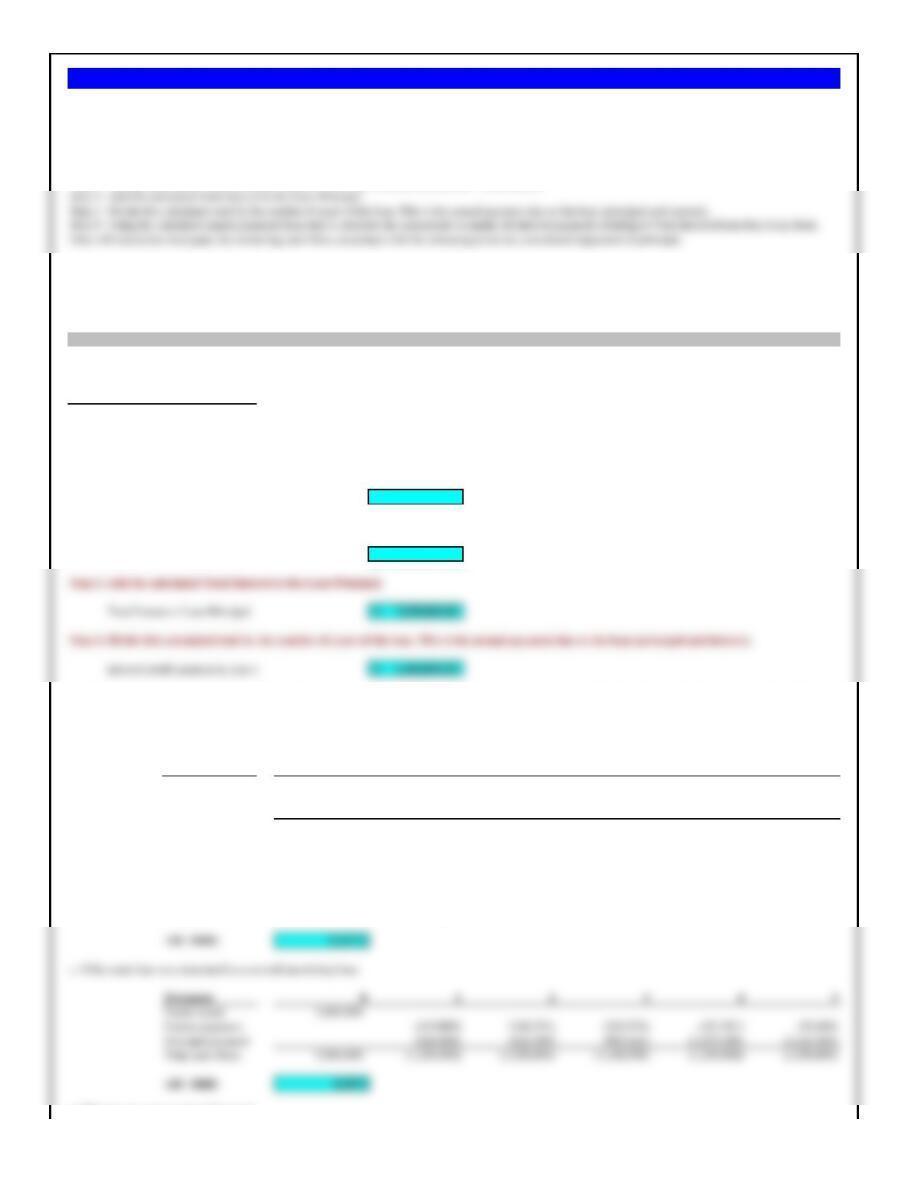

Carlos and Wilmsberg Inc. is a rapidly growing import-export firm. It decided to borrow €35,000,000 via a euro-euro floating-rate loan for 4 years.

Carlos and Wilmsberg Inc. must decide between two competing loan offers from two of its banks.

Problem 8.11 Carlos and Wilmsberg Inc.

Caixa Brasilia Federal has offered the 4-year debt at euro-LIBOR + 2.5% with an up-front initiation fee of 2.0%. Brasilao Safra Banco, however,

has offered euro-LIBOR + 3.0%, a higher spread, but no loan initiation fees up-front, for the same term and principal. Both banks reset the interest

rate at the end of each year.

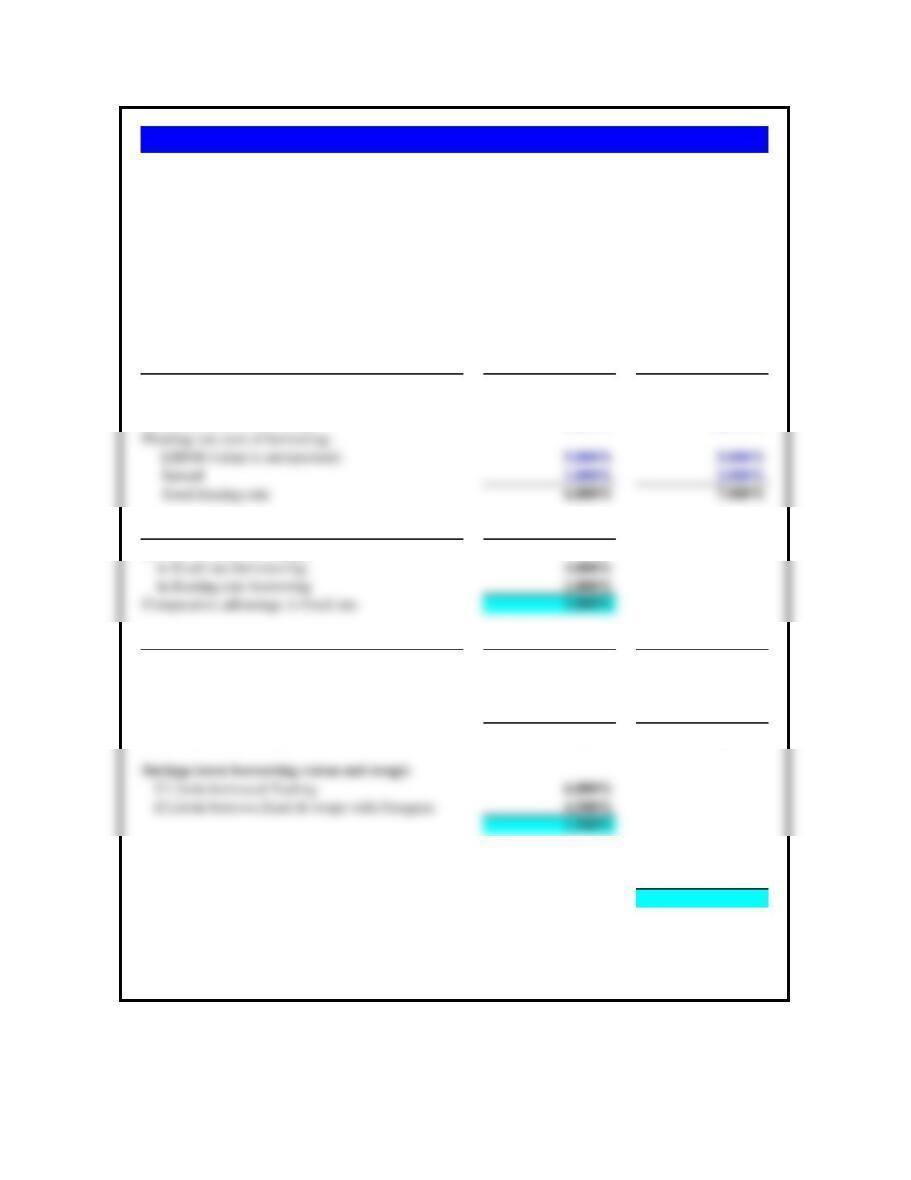

Assumptions Values

Principal borrowing need € 5,000,000

If LIBOR Falls 50 Basis Pts Per Year Year 0 Year 1 Year 2 Year 3 Year 4

Expected annual change in LIBOR -0.500%

LIBOR 4.000% 3.500% 3.000% 2.500% 2.000%

Bank spread 2.500% 2.500% 2.500% 2.500% 2.500%

Interest rate 6.500% 6.000% 5.500% 5.000% 4.500%

If LIBOR Rises 50 Basis Pts Per Year Year 0 Year 1 Year 2 Year 3 Year 4

Expected annual change in LIBOR 0.500%

LIBOR 4.000% 4.500% 5.000% 5.500% 6.000%

Bank spread 2.500% 2.500% 2.500% 2.500% 2.500%

Interest rate 6.500% 7.000% 7.500% 8.000% 8.500%

Purchase of the floating Rate Agreement will cost €100,000, paid at the time of the initial loan. What are Firenza’s annual financing

costs now if LIBOR rises and if LIBOR falls.? Firenza uses 12% as its weighted average cost of capital. Do you recommend that Firenza

purchase the FRA?

Problem 8.12 Firenza Motors (Italy)

Firenza Motors of Italy recently took out a 4-year €5 million loan on a floating rate basis. It is now worried, however, about rising interest

costs. Although it had initially believed interest rates in the Euro-zone would be trending downward when taking out the loan, recent

economic indicators show growing inflationary pressures. Analysts are predicting that the European Central Bank will slow monetary

growth driving interest rates up.

This rather unusual forward rate agreement is somewhat one-sided in the favor of the insurance company. When Firenza is correct,

Firenza pays the full difference in rates to the insurance company. But when interest rates move against Firenza, the insurance company

pays Firenza only 70% of the difference in rates. And all of that is after Firenza paid €100,000 up-front for the agreement regardless of

outcome. Not a very good deal.

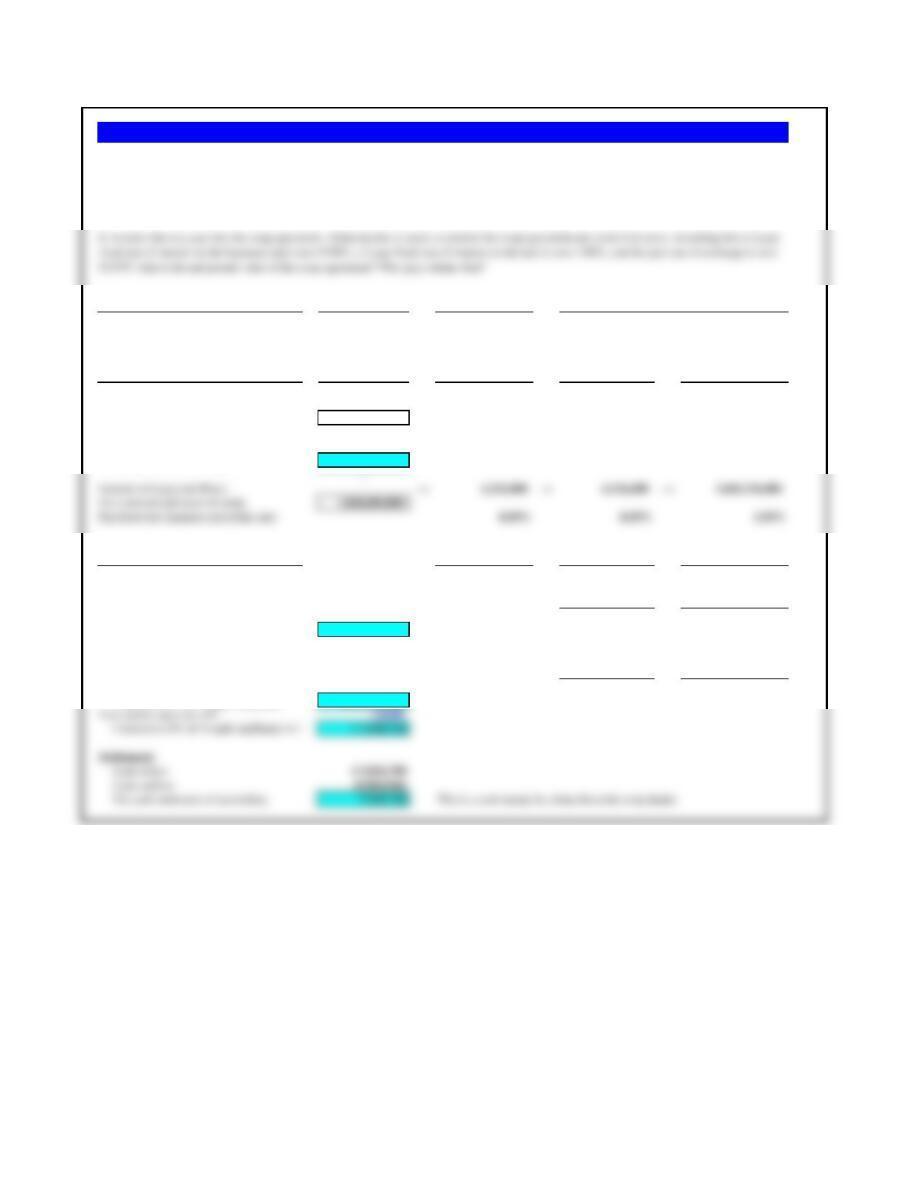

Assumptions Xavier Zulu

Credit rating AAA BBB

Prefers to borrow Floating Fixed

Fixed-rate cost of borrowing 8.000% 12.000%

Comparative Advantage in Borrowing Values

Lluvia’s absolute advantage:

One Possibility Xavier Zulu

Lluvia borrows fixed -8.000% —

Paraguas borrows floating — -7.000%

Lluvia pays Paraguas floating (LIBOR) -5.000% 5.000%

Paraguas pays Lluvia fixed 8.500% -8.500%

Net interest after swap -4.500% –10.500%

If Paraguas borrowes fixed 12.000%

If Paraguas borrows floating & swaps with Lluvia 10.500%

1.500%

Problem 8.13 Lluvia and Paraguas

The 3.0% comparative advantage enjoyed by Lluvia represents the opportunity set for improvement for

both parties. This could be a 1.5% savings for each (as in the example shown) or any other combination

which distributes the 3.0% between the two parties.

Lluvia Manufacturing and Paraguas Products both seek funding at the lowest possible cost. Lluvia

would prefer the flexibility of floating rate borrowing, while Paraguas wants the security of fixed rate

borrowing. Lluvia is the more credit-worthy company. They face the following rate structure. Lluvia,

with the better credit rating, has lower borrowing costs in both types of borrowing.

Lluvia wants floating rate debt, so it could borrow at LIBOR+1%. However it could borrow fixed at

8% and swap for floating rate debt. Paraguas wants fixed rate, so it could borrow fixed at 12%. However

it could borrow floating at LIBOR+2% and swap for fixed rate debt. What should they do?

Assumptions Values Swap Rates 3- year bid 3-year ask

Notional principal

€ 10,000,000 Original: Euro 0.95% 0.98%

Aidan will receive Euros and pay Norwegian kron

Step 1

Year 0

Convert notional principal of €10,000,000 to Norwegian krone at kr9.98/€

€10,000,000 × kr9.98/€ = kr99,800,000

Step 2

Year 1

Receive Euro interest based on 3-year bid rate of 0.95%

So, Year 1 Euro interest received is €10,000,000 × 0.95% = €95,000

Pay Norwegian krone interest based on 3-year ask rate of 2.05%

So, Year 1 Norwegian krone interest paid is kr99,800,000 × 2.05% = kr2,045,900

Problem 8.14 Aidan’s Cross-Currency Swap: Norwegian Krone for Euros.

Aidan Corporation entered into a 3-year crosscurrency interest rate swap to receive euros and pay Norwegian krone. Aidan, however, decided to

unwind the swap after one year—thereby having two years left on the settlement costs of unwinding the swap after one year. Repeat the calculations for

unwinding, but assume that the following rates now apply.

Assumptions Values Swap Rates 3- year bid 3-year ask

Notional principal € 10,000,000 Euros — €3.24% 3.28%

Spot exchange rate, Yen/euro 104.00 Japanese yen 0.56% 0.59%

a) Interest & Swap Payments Year 0 Year 1 Year 2 Year 3

Receive fixed rate euros at this rate: 3.24% 3.24% 3.24%

On a notional principal of: € 10,000,000

Trident will receive cash flows: → € 324,000 → € 324,000 → € 10,324,000

↑

Exchange rate, time of swap (¥/€)104.00

↓

Ganado will pay cash flows: →6,136,000 →6,136,000 →1,046,136,000

On a notional principal of (yen): 1,040,000,000

Pay fixed rate Japanese yen at this rate: 0.59% 0.59% 0.59%

b) Unwinding the swap after one-year Year 1 Year 2 Year 3

Remaining euro cash inflows € 324,000 € 10,324,000

PV factor at now current fixed € interest 3.60% 0.9653 0.9317

PV of remaining € cash inflows € 312,741 € 9,618,968

Cumulative PV of € cash infllows € 9,931,709

Remaining ¥ cash outflows SFr. 6,136,000 SFr. 1,046,136,000

PV factor at now current fixed ¥ interest 0.80% 0.9921 0.9842

PV of remaining ¥ cash outflows SFr. 6,087,302 SFr. 1,029,596,561

Cumulative PV of ¥ cash outflows 1,035,683,862

New current spot rate, ¥/€114.00

Cumulative PV of ¥ cash outflows in €€ 9,084,946

Cash inflow € 9,931,709

Cash outflow (9,084,946)

Net cash settlement of unwinding € 846,763

Use the table of swap rates in the chapter, and assume Aidan enters into a swap agreement to receive eurosand pay Japanese yen, on a notional

principal of €10,000,000. The spot exchange rate at the time of the swap is ¥104/€.

a. Calculate all principal and interest payments, in both euros and Japanese yen, for the life of the swap agreement.

Problem 8.15 Aidan’s Cross-Currency Swap: Yen for Euros

Assumptions Values Swap Rates 7- year bid 7-year ask

Notional principal

¥60,000,000 Yen 0.30% 0.36%

Spot exchange rate, $/€135.81 Euros 0.51% 0.55%

a. Interest & Swap Payments Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

Receive fixed rate yen at rate:

0.30%

Notional principal of:

¥60,000,000

Receive cash inflows of:

¥180,000 ¥180,000 ¥180,000 ¥180,000 ¥180,000 ¥180,000 ¥60,180,000

↑

Spot exchange rate, ¥/€135.81

↓

0.55%

b. Unwinding the Swap Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

If the swap is unwound three years later, there are four years of cash flows remaining:

Problem 8.16 Takashima Auto Parts (Japan)

Takashima Auto Parts is a Japanese-based automotive parts supplier and was spun off from Toyota in 2007. With annual sales of ¥30 billion, the company has expanded its

markets beyond the traditional automobile manufacturers in the pursuit of a more diversified sales base. As part of the general diversification effort, the company wishes to

diversify the currency of denomination of its debt portfolio as well. Assume Takashima enters a ¥60 million 7-year cross-currency interest rate swap to do just that—pay euros

and receive Japanese yen. Also assume that the current spot rate is ¥135.81/€. Using the data in Exhibit 8.13, solve the following:

a. Calculate all the principal and interest payments in both currencies for the life of the swap.

Remaining euro cash outflows

€ 2,430 € 2,430 € 2,430 € 444,224

PV factor at now current fixed € interest 0.50% 0.9950 0.9901 0.9851 0.9802

PV of remaining euro cash outflows

€ 2,418 € 2,406 € 2,394 € 435,449

Cumulative PV of € cash outflows € 442,666

Spot exchange rate at unwinding (¥/€)121.16

The loan was for USD5 million, for five years, with an 8.200% interest rate.

Step 1: Calculate interest on Loan Principal for one year

a. Following the 5 steps described, lay out the principal and interest payments on the loan agreement.

b.Calculate effective cost of funds on the loan agreement (the all-in-cost).

c. Lay out the principal and interest payments on the same loan if it was a ‘normal’ amortizing loan.

d. What is your assessment of the loan?

a. The loan calculations would appear as follows.

Loan 0

Loan Principal 5,000,000.00$

Interest rate 8.2000%

Maturity (years) 5.0

Step 1. Calculate interest on principal for one year.

Interest rate x Loan Principal

410,000.00$

Step 2. Multiply that interest by the number of years of the loan. This is “Total Interest.”

Total Interest = Interest x 5

2,050,000.00$

Step 3. Add the calculated Total Interest to the Loan Principal.

7,050,000.00$

Step 4: Divide this calculated total by the number of years of the loan. This is the annual payment due on the loan (principal and interest).

1,410,000.00$

a. The principal and interest payments on the loan structure described.

Payments 0 1 2 3 4 5

Funds raised 5,000,000

Interest payment (1,410,000) (640,000)

Principal payment – (770,000) (1,410,000) (1,410,000) (1,410,000)

Total cash flows 5,000,000 (1,410,000) (1,410,000) (1,410,000) (1,410,000) (1,410,000)

b. The effective cost of funds, the all-in-cost (AIC) on the loan, is found by finding the IRR of the cash flow series.

Payments 0 1 2 3 4 5

Funds raised 5,000,000

d. What is your assessment of the loan?

Problem 8.17 United Arab Emirates Small Business Loan (A)

Mohammad tried one last time to explain the loan structure offered by the company’s UAE bank. His boss just stared at him. Mo explained the detailed calculation of

annual interest and principal payments, step-by-step, as detailed by the bank.

Step 5: Using the calculated annual payment from step 4, structure the repayments to make all interest payments (totaling to Total Interest from Step 2)

up-front. Once Total Interest has been repaid, the balance on the annual payments are to be considered repayment of principal.

Note that the two payments on interest total to the Total Interest calculated in Step 2. In year 2, since the payment of (640,000) to complete Total Interest does not

consume the entire annual payment, the balance, (770,000), is assigned as a payment on principal.

Well, its certainly bizarre. The AIC, at 12.67%, is much higher than the stated interest rate of the loan. The calculation defies most of financial logic, although the

purveyors of these loans argue they are simply “protecting themselves against default by getting all of their interest up-front, early, in case the borrower defaults.”

Again, this is rather sketchy logic, as a default would mean loss on principal anyways.