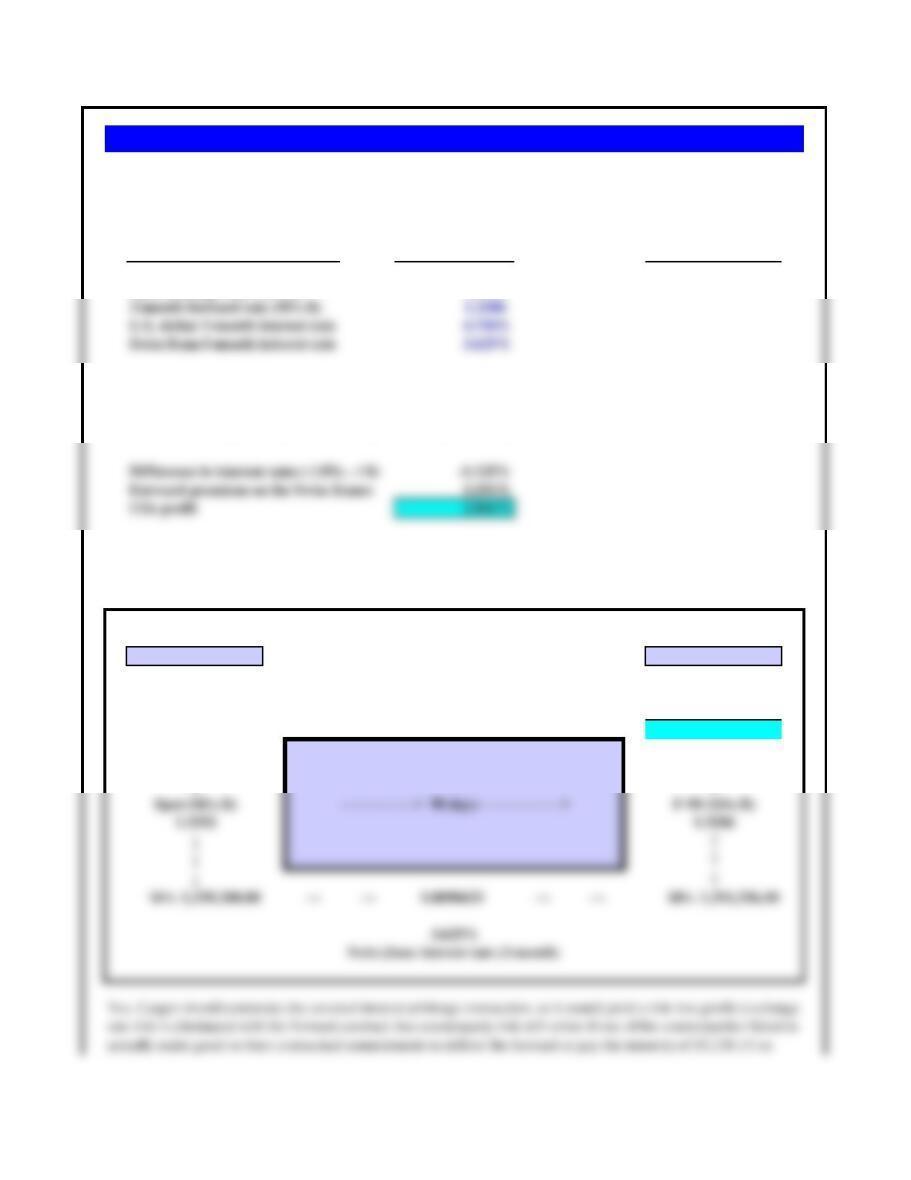

Value SFr. Equivalent

Arbitrage funds available $1,000,000 SFr. 1,339,200

U.S. dollar 3-month interest rate 4.750%

Swiss franc3-month interest rate 3.625%

Difference in interest rates ( i SFr. – i $) -1.125%

Forward premium on the Swiss france 3.191%

CIA profit 2.066%

U.S. dollar interest rate (3-month)

START 4.750% END

$1,000,000 → → 1.011875 → → 1,011,875.00$

↓1,017,113.13

↓5,238.13$

↓ ↑

↓ ↑

↓ ↑

↓ ↑

Swiss franc interest rate (3-month)

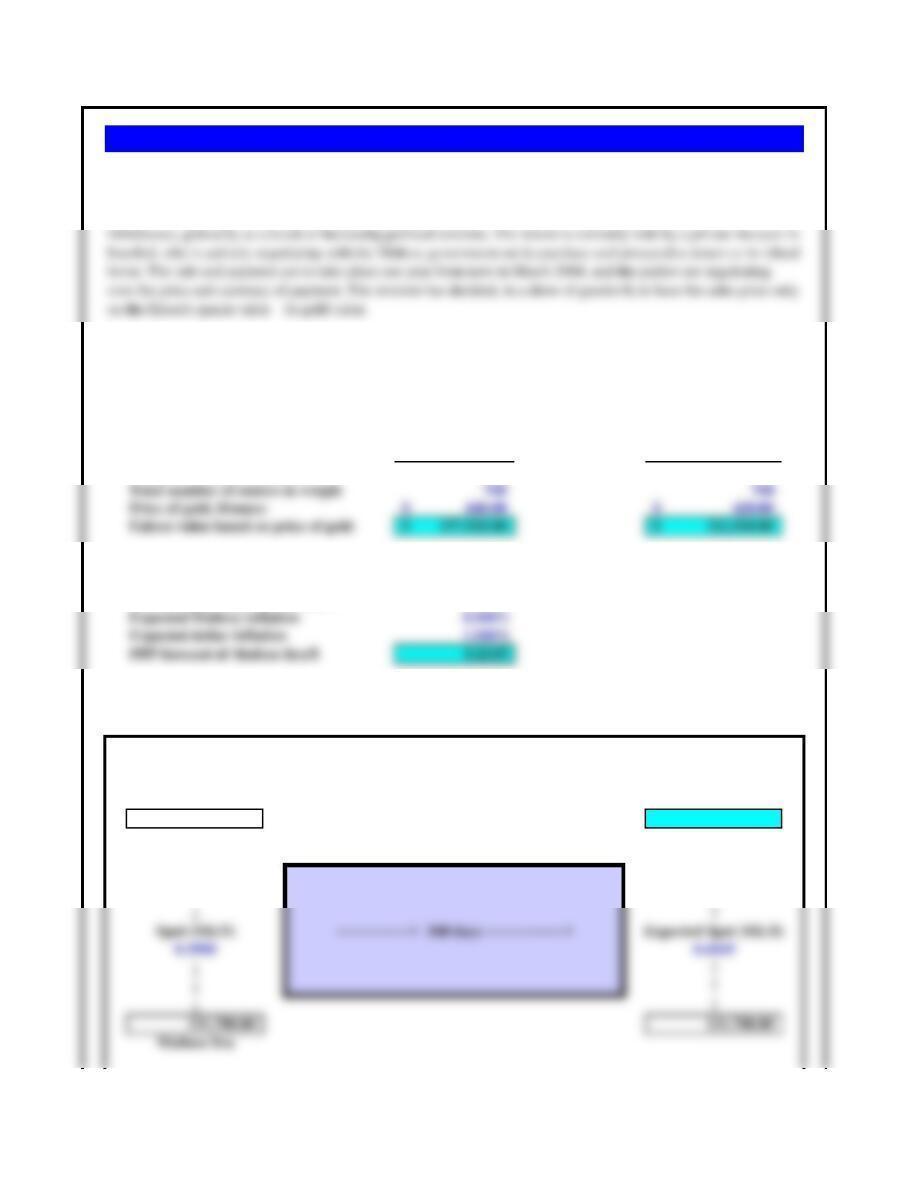

Problem 6.14 Casper Landsten — Thirty Days Later

Assumptions

This tells Casper Landsten he should borrow U.S. dollars and invest in the lower yielding currency, the Swiss franc,

and then sell the Swiss franc principal and interest forward three months locking in a CIA profit.

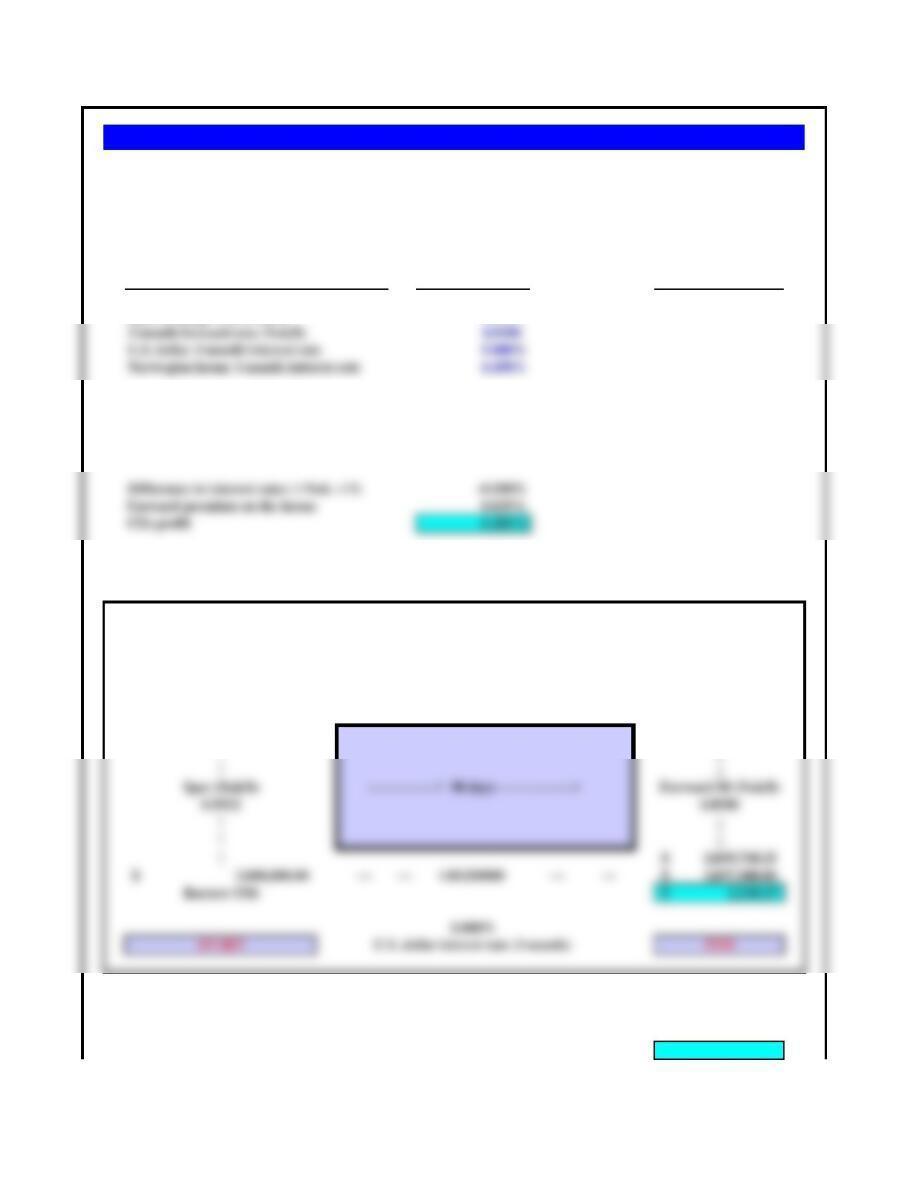

One month after the events described in the previous two questions, Casper Landsten once again has $1 million (or

its Swiss franc equivalent) to invest for three months. He now faces the following rates. Should he again ener into a

covered interest arbitrage (CIA) investment?

Arbitrage Rule of Thumb: If the difference in interest rates is greater than the forward premium/discount, or

expected change in the spot rate for UIA, invest in the higher interest yielding currency. If the difference in interest

rates is less than the forward premium (or expected change in the spot rate), invest in the lower yielding currency.

Value Krone Equivalent

Arbitrage funds available $3,000,000 18,093,600

Norwegian krone interest rate (3-month)

4.450%

18,093,600.00 → → 1.0111250 → → 18,294,891.30

↑ ↓

↑ ↓

↑ ↓

↑ ↓

Annualized rate of return: 0.2947%

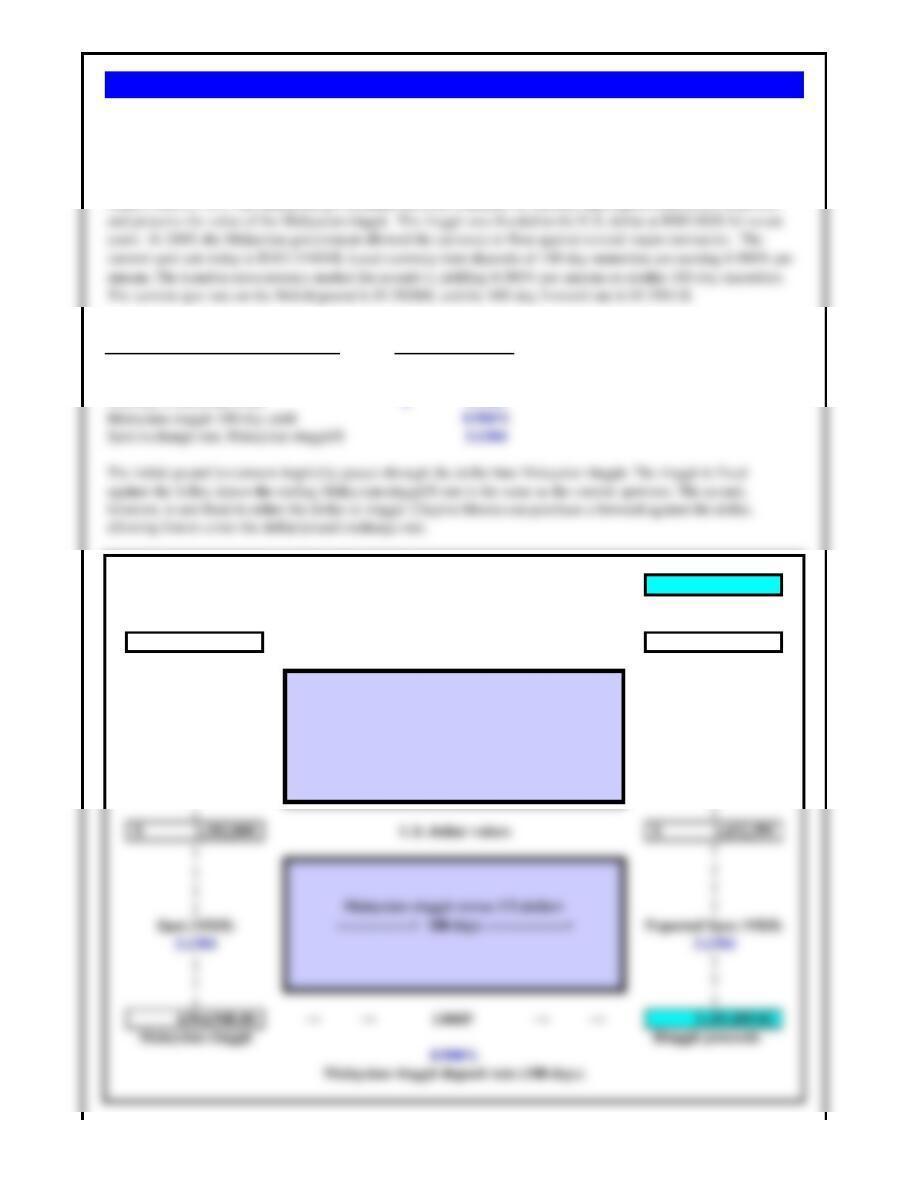

This tells Ari Karlsen he should borrow U.S. dollars and invest in the lower yielding currency, the Norwegian krone, selling

the dollars forward 90 days, and therefore earn covered interest arbitrage (CIA) profits.

Ari Karlsen can make $2,210.25 for Statoil on each $3 million he invests in this covered interest arbitrage (CIA)

transaction. Note that this is a very slim rate of return on an investment of such a large amount.

Problem 6.15 Statoil’s Arbitrage

Assumptions

Statoil, the national oil company of Norway, is a large, sophisticated, and active participant in both the currency and

petrochemical markets. Although it is a Norwegian company, because it operates within the global oil market, it considers

the U.S. dollar as its functional currency, not the Norwegian krone. Ari Karlsen is a currency trader for Statoil, and has

immediate use of either $3 million (or the Norwegian krone equivalent). He is faced with the following market rates, and

wonders whether he can make some arbitrage profits in the coming 90 days.

Arbitrage Rule of Thumb: If the difference in interest rates is greater than the forward premium/discount, or expected

change in the spot rate for UIA, invest in the higher interest yielding currency. If the difference in interest rates is less than

the forward premium (or expected change in the spot rate), invest in the lower yielding currency.

Assumptions London New York

a. What do the financial markets suggest for inflation in Europe next year?

According to the Fisher effect, real interest rates should be the same in both Europe and the US.

Since the nominal rate = [ (1+real) x (1+expected inflation) ] – 1:

The expected rate of inflation in Europe is then: 0.669%

b. Estimate today‘s one-year forward exchange rate between the dollar and the euro.

Spot exchange rate ($/€) 1.3264

Problem 6.16 Trans-Atlantic Quotes

The separation of over 3,000 nautical miles and five time zones, money and foreign exchange markets in

both London and New York are very efficient. The following information has been collected from the

respective areas:

Assumptions Value

Spot exchange rate ($/€) $1.3620

Expected US inflation for coming year 2.500%

Expected French inflation for coming year 3.500%

Current chateau nominal weekly rent (€) € 9,800.00

Forecasting the future rent amount and exchange rate: Value

Purchasing power parity exchange rate forecast ($/€) 1.3488

Spot (one year) = Spot x ( 1 + US$ inflation ) / ( 1 + French inflation )

Nominal monthly rent, in euros, one year from now 10,143.00

Rent now x ( 1 + inflation France )

Problem 6.17 Chamonix Rentals

You are planning a ski vacation to Mt. Blanc in Chamonix, France, one year from now. You are

negotiating over the rental of a chateau. The chateau’s owner wishes to preserve his real income

against both inflation and exchange rate changes, and so the present weekly rent of €9,800

(Christmas season) will be adjusted upwards or downwards for any change in the French cost of

living between now and then. You are basing your budgeting on purchasing power parity (PPP).

Value

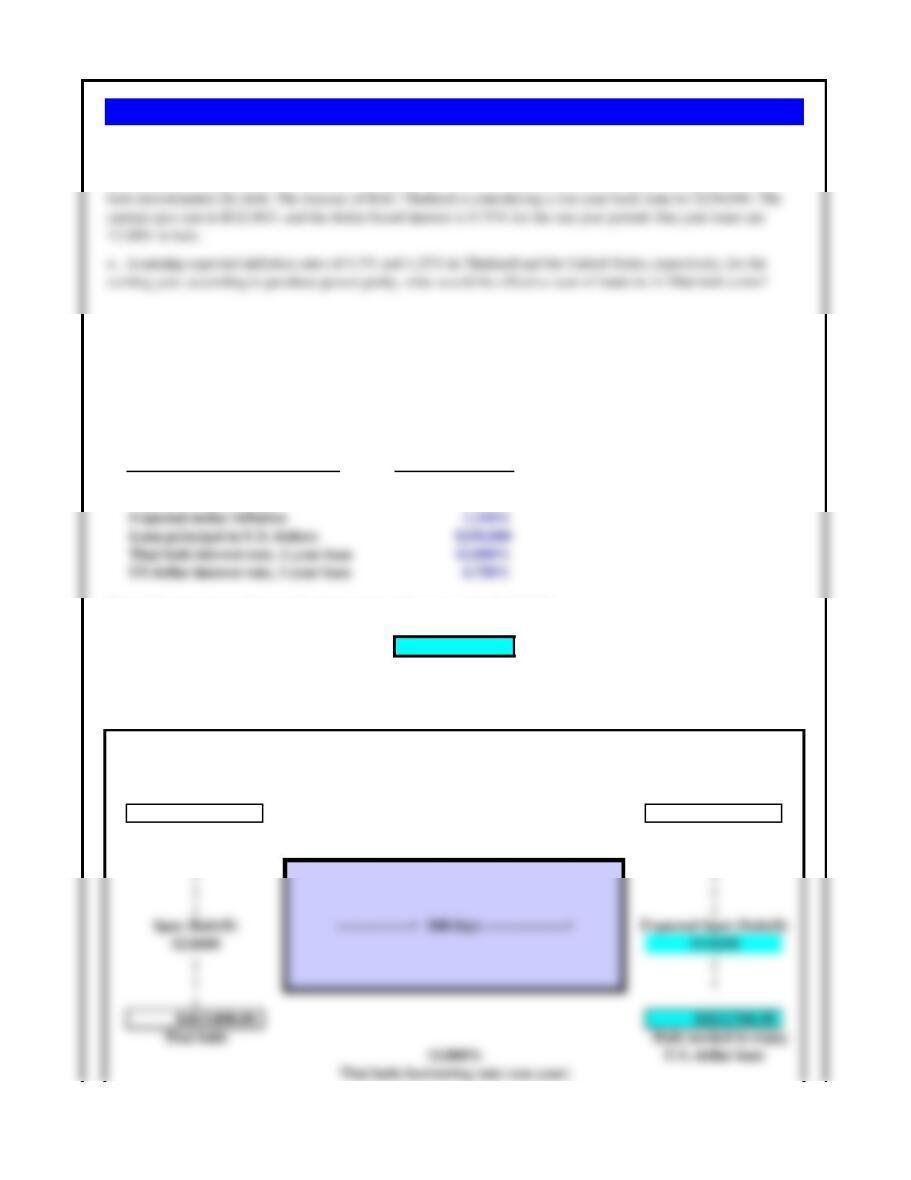

Current spot rate, Thai baht/$ 32.06

Expected Thai inflation 4.300%

Expected dollar inflation 1.250%

Loan principal in U.S. dollars $250,000

Thai baht interest rate, 1-year loan 12.000%

US dollar interest rate, 1-year loan 6.750%

First, it is necessary to forecast the future spot exchange rate for the baht/$.

PPP forecast of Thai baht/$ 33.0258

Different expectations of the future spot exchange rate, either PPP for part a), or an expected devaluation for

part b), allow the isolation of exactly how many Thai baht would be required to repay the dollar loan.

U.S. dollar borrowing rate (one year)

6.750%

250,000$ → → 1.06750 → → 266,875$

↓ ↓

↓ ↓

↓ ↓

↓ ↓

↓ ↓

↓ ↓

Problem 6.18 East Asiatic–Thailand

Assumptions

The East Asiatic Company (EAC), a Danish company with subsidiaries all over Asia, has been funding its Bangkok

subsidiary primarily with U.S. dollar debt because of the cost and availability of dollar capital as opposed to Thai

b. If EAC’s foreign exchange advisers believe strongly that the Thai government wants to push the value of the

baht down against the dollar by 5% over the coming year (to promote its export competitiveness in dollar

markets), what might the effective cost of funds end up being in baht terms?

c. If EAC could borrow Thai baht at 13% per annum, would this be cheaper than either part (a) or part (b)

above?

Implied cost = (Repaid/Initial proceeds) – 1 9.966%

b) Assuming a future spot rate for the baht which is 5% weaker than the current spot rate (B32.06/$ ÷ ( 1 – .05), or

B33.7474/$), the implied cost is 12.369%. (This is found by plugging in this new forecast spot rate in the expected

spot rate cell on the right-hand-side of the box.)

a) Assuming a purchasing power parity forecast of the future spot rate, B33.0258/$, it will take 8,813,760 baht to

repay the U.S. dollar loan. The implied cost of funds, in baht terms, is 9.966%.

Now In One Year

Weight of falcon, in pounds 48 48

Total number of ounces in weight 768 768

Price of gold, $/ounce 440.00$ 420.00$

Falcon value based on price of gold 337,920.00$ 322,560.00$

The purchasing power parity forecast of the Maltese lira/dollar exchange rate:

Current spot rate, Maltese lira/$ 0.3900

Expected dollar inflation 1.500%

PPP forecast of Maltese lira/$ 0.4169

Investor Receives

in March 2004

Current Value Assuming PPP

337,920$ 316,116$

↓ ↑

↓ ↑

↓ ↑

↓ ↑

↓ ↑

↓ ↑

↓ ↑

Problem 6.19 Maltese Falcon: The Black Bird

Imagine that the mythical solid gold falcon, initially intended as a tribute by the Knights of Malta to the King of

Spain in appreciation for his gift of the island of Malta to the order in 1530, has recently been recovered. The falcon

is 14 inches high and solid gold, weighing approximately 48 pounds. Assume that gold prices have risen to

The current spot exchange rate is 0.39 Maltese lira (ML) per 1.00 U.S. dollar. Maltese inflation is expected to be

about 8.5% for the coming year, while U.S. inflation, on the heels of a double-dip recession, is expected to come in

at only 1.5%. If the investor bases value in the U.S. dollar, would he be better off receiving Maltese lira in one year

(assuming purhcasing power parity), or receiving a guaranteed dollar payment (assuming a gold price of $420 per

ounce)?

If the investor bases his gross sales proceeds in U.S. dollars, the guaranteed dollar payment at $420/ounce yields a

larger amount ($322,560) than accepting Maltese lira assuming PPP ($316,116).

Assumptions Values

Principal investment, British pounds

£1,000,000.00

Spot exchange rate ($/£)

1.5820$

1.5561$

Return = (Proceeds/Initial investment) – 1 6.188%

Initial Investment Investment Proceeds

£1,000,000.00 £1,061,884.84

↓ ↑

↓ ↑

↓ ↑

↓British pounds versus US dollars ↑

Spot ($/£) —————> 180 days —————-> Fwd-180 ($/£)

1.5820 1.5561

↓ ↑

↓ ↑

↓ ↑

↓ ↑

3.1384 3.1384

↓ ↑

↓ ↑

Problem 6.20 Clayton Moore’s Money Fund

Clayton Moore is the manager of an international money market fund managed out of London. Unlike many money

funds that guarantee their investors a near risk-free investment with variable interest earnings, Clayton Moore’s fund

is a very aggressive fund that searches out relatively high interest earnings around the globe, but at some risk. The

fund is pound-denominated. Clayton is currently evaluating a rather interesting opportunity in Malaysia. Since the

If Clayton Moore invests in the Malaysian ringgit deposit, and accepts the uncovered risk associated with the RM/$

exchange rate (managed by the government), and sells the dollar proceeds forward, he should expect a return of

6.188% on his 180-day pound investment. This is better than the 4.200% he can earn in the euro-pound market.

Spot Under or

Local Local In Implied rate overvalued

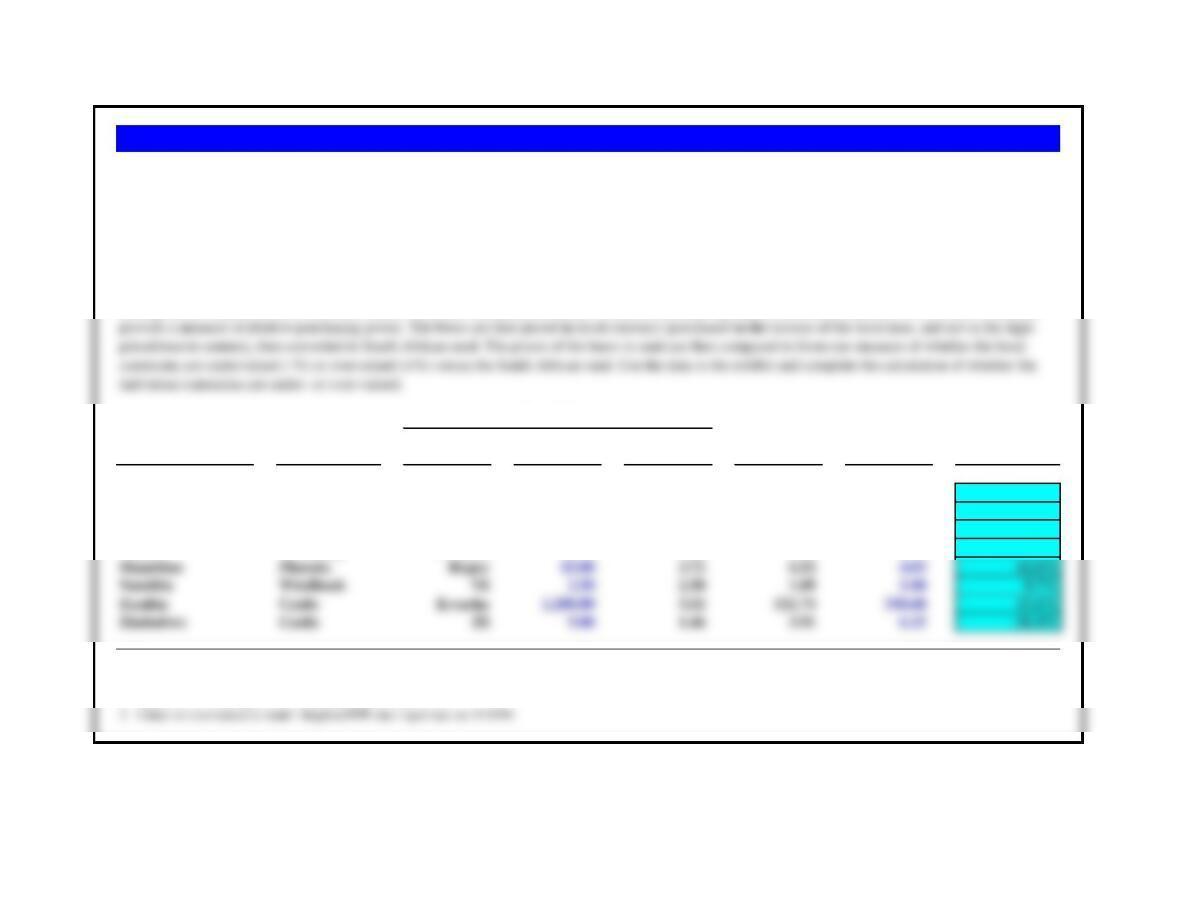

Country Beer currency currency rand PPP rate (3/15/99) to rand (%)

South Africa Castle Rand 2.30 —- —- —- —-

Botswana Castle Pula 2.20 2.94 0.96 0.75 27.9%

Ghana Star Cedi 1,200.00 3.17 521.74 379.10 37.6%

Kenya Tusker Shilling 41.25 4.02 17.93 10.27 74.6%

Malawi Carlsberg Kwacha 18.50 2.66 8.04 6.96 15.6%

Notes:

1. Beer price in South African rand = Price in local currency / spot rate on 3/15/99.

2. Implied PPP exchange rate = Price in local currency / 2.30.

Beer Prices

In 1999 the Economist magazine reported the creation of an index or standard for the evaluation of African currency values using the local prices of beer.

Beer was chosen as the product for comparison because McDonald’s had not peneterated the African continent beyond South Africa, and beer met most of the

same product and market characteristics required for the construction of a proper currency index. Investec, a South African investment banking firm, has

replicated the process of creating a measure of purchasing power parity (PPP) like that of the Big Mac Index of the Economist, for Africa.

The index compares the cost of a 375 milliliter bottle of clear lager beer across sub-Sahara Africa. As a measure of PPP the beer needs to be relatively

homogeneous in quality across countries, needs to possess substantial elements of local manufacturing, inputs, distribution, and service, in order to actually

Problem 6.21 African Beer Standard

Borrowing principal £30,000,000

Current spot rate, pesos/pounds (CLP$/£)930.250

Actual spot rate end of year (CLP$/£)900.15

Actual spot rate end of year (CLP$/£)900.15

U.S. dollar borrowing rate (one year)

1.750%

£30,000,000 → → 1.0175 → → £30,525,000

↓ ↓

↓ ↓

↓ ↓

↓ ↓

↓ ↓

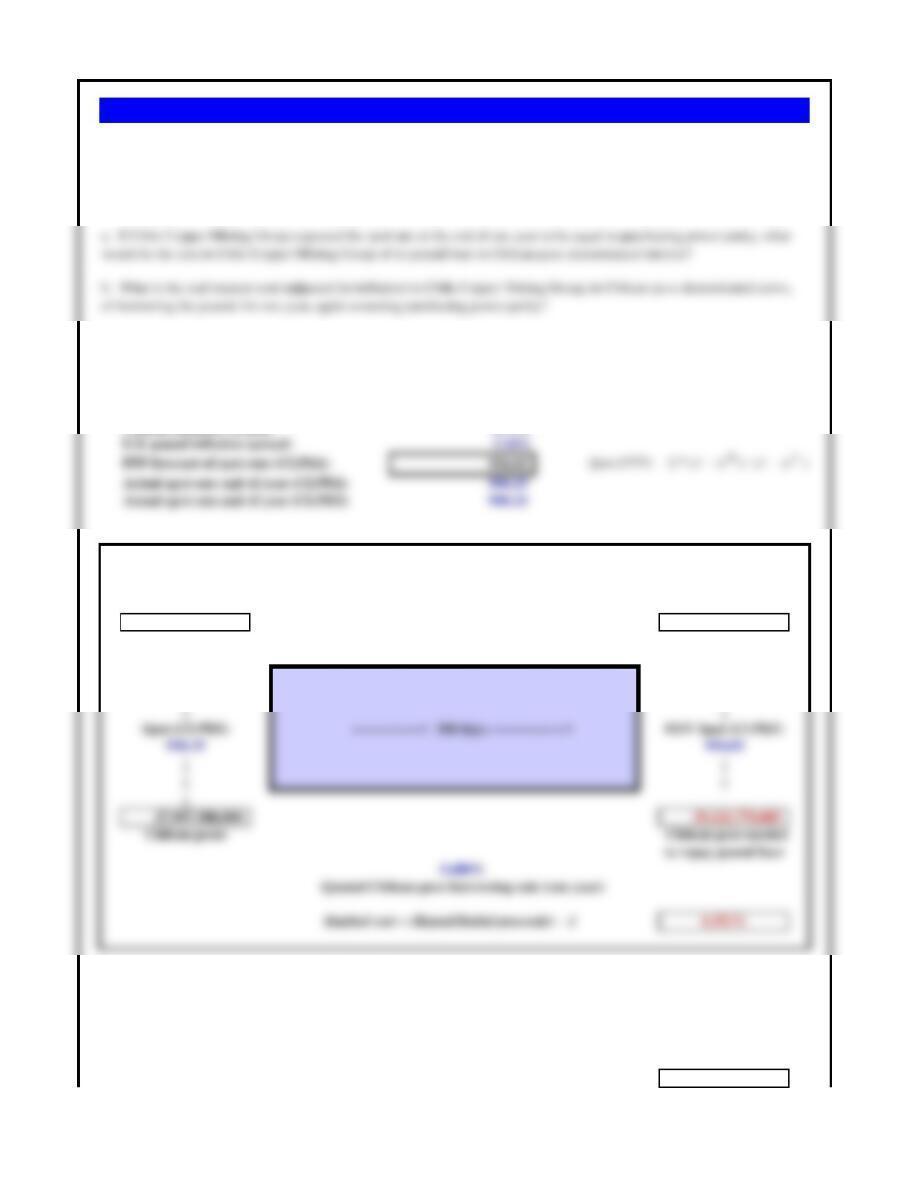

a. If the ending spot rate was CLP$954.03/£ as PPP would predict, the actual peso-based interest cost would be 4.351%.

b. The real peso-denominated interest cost (corrected for inflation) would be:

Nominal interest 4.3511%

Actual inflation 4.7100%

Real peso-interest -0.3428%

Problem 6.22 Chile Copper Mining Group (Chile)

The calculation shown at right is the precise or exact

answer. The approximate form, found simply by

subtracting inflation from nominal interest, would be

Chile Copper Mining Group, headquartered in Santiago, Chile, is one of the largest copper mining firms in the world. On

January 1st, when the spot exchange rate is CLP$930.25/£, the company borrows £30.0 million from a London bank for one

year at 1.75% interest (Chilean banks had quoted 5.68% for an equivalent loan in Chilean pesos). During the year, the U.K.

inflation rate is 2.1% and Chilean inflation rate is 4.71%. At the end of the year, the firm repays the pound loan.

a. If Chile Copper Mining Group expected the spot rate at the end of one year to be equal to purchasing power parity, what

would be the cost to Chile Copper Mining Group of its pound loan in Chilean peso-denominated interest?

b. What is the real interest cost (adjusted for inflation) to Chile Copper Mining Group, in Chilean peso-denominated terms,

of borrowing the pounds for one year, again assuming purchasing power parity?

c. If the actual spot rate at the end of the year turned out to be CLP$900.15/£, what was the actual Chilean peso-denominated

interest cost of the loan?

-0.3589%.

Calendar year 2013 2014 2015 2016 2017 2018

XC90 Price (Swedish krona) 619,900

Swedish inflation (forecast) 0.28% 0.88% 1.64% 3.45% 0.90%

Australian inflation (forecast) 2.51% 1.51% 1.25% 1.97% 1.96%

Exchange rate (kr = A$1.00) 6.65

a. If the domestic price of the XC90 increases with the rate of inflation, what would be its price over the 2013–2018 period?

g. What did the Swedish krona end up doing over the 2013-2018 period?

Calendar year 2013 2014 2015 2016 2017 2018

a. XC90 Price with Swedish inflation (krona) 619,900 621,636 627,106 637,391 659,381 665,315

6.65 6.51 6.46 6.49 6.58 6.52

c. Export price if using PPP ( Australian dollars) 93,218.05$ 95,557.82$ 97,000.74$ 98,213.25$ 100,148.05$ 102,110.95$

d. Export price at fixed exchange rate ( Australian dollars) 93,218.05$ 93,479.06$ 94,301.67$ 95,848.22$ 99,154.98$ 100,047.38$

An added note is to recognize that if this was the case, PPP is definitely not ‘holding’ in the academic sense.

If export price rises at Australian dollar inflation 93,218.05$ 95,557.82$ 97,000.74$ 98,213.25$ 100,148.05$ 102,110.95$

679,038

Problem 6.23 Volvo of Sweden’s XC90 Export Pricing Analysis

b. Assuming the forecasts of Australian and Swedish inflation prove accurate, what would the value of the Swedish krona be over the coming years if its value versus the

Australian dollar followed purchasing power parity?

c.If the export price of the XC90 were set using the purchasing power parity forecast of the Swedish krona-Australian dollar exchange rate, what would the export price be

Volvo Sweden, a leading auto manufacturer in Sweden, was scheduled to launch a new variant of the XC90 SUV in 2013 and was in the midst of generating a complete

pricing analysis of the car for sales in Sweden and export. The new variant of the XC90 would be initially priced at Swedish kronor 619,900 in Sweden, and if exported to

Australia, the price would be A$92,985 in Australian dollars at the current spot rate of kr6.65 = A$1.00. Volvo intends to raise the price domestically with the rate of

Swedish inflation over time, but is worried about how that compares to the export price given Australian dollar inflation and the future exchange rate. Use the following data

table to answer the pricing analysis questions.

If most of the competition in the target Australian markets were Australian dollar-based manufacturers, their costs and prices might be rising with Australian dollar inflation.

high by 2018 (to A$100,047.38), whereas if rate of exchange had remained fixed the export price would be much higher in 2018 (A$102,110.95). Of course pricing

strategies can and should be changed over time with changing market conditions, but the general consensus of analysts would be to expect to increase the at a rate

somewhere inbetween (c) and (d) forecasts.

f. Exporters generally would prefer that their own currency weakens over time versus the currency of the customer — making their product offering increasingly affordable

(cheaper), and hopefully increasing sales volume. Since Volvo’s costs are all in Swedish krona, earning a hard currency like the Australian dollar which would be slowly

weaken against the Australian dollar might decrease profit margins (depending on what happens to costs over time from other factors).

b. Exchange rate (Swedish krona=A$1.00) if purchasing

power parity (PPP) holds

e. Stefan, one of the newly hired pricing strategists, believes that prices of automobiles in both domestic and export markets will increase with the rate of inflation, and that

the Swedish krona/Australian dollar exchange rate will remain fixed. What would this imply or forecast for the future export price of the XC90?

f. If you were Volvo, what would you hope to happen to the Swedish krona’s value versus the Australian dollar over time given your desire to export the XC90? Now if you

combined that “hope” with some assumptions about the competition – other automobile sales prices in Australian dollar markets over time – how might your strategy evolve?