Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 6 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN

EXCHANGE RATES

ANSWERS & SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

QUESTIONS

1. Give a full definition of arbitrage.

2. Discuss the implications of the interest rate parity for the exchange rate determination.

Answer: Assuming that the forward exchange rate is roughly an unbiased predictor of the future

spot rate, IRP can be written as:

3. Explain the conditions under which the forward exchange rate will be an unbiased predictor

of the future spot exchange rate.

4. Explain the purchasing power parity, both the absolute and relative versions. What causes

the deviations from the purchasing power parity?

Answer: The absolute version of purchasing power parity (PPP):

5. Discuss the implications of the deviations from the purchasing power parity for countries’

competitive positions in the world market.

6. Explain and derive the international Fisher effect.

Answer: The international Fisher effect can be obtained by combining the Fisher effect and the

7. Researchers found that it is very difficult to forecast the future exchange rates more

accurately than the forward exchange rate or the current spot exchange rate. How would you

interpret this finding?

8. Explain the random walk model for exchange rate forecasting. Can it be consistent with the

technical analysis?

*9. Derive and explain the monetary approach to exchange rate determination.

Answer: The monetary approach is associated with the Chicago School of Economics. It is

10. Explain the following three concepts of purchasing power parity (PPP):

a. The law of one price.

b. Absolute PPP.

c. Relative PPP.

Answer:

a. The law of one price (LOP) refers to the international arbitrage condition for the standard

11. Evaluate the usefulness of relative PPP in predicting movements in foreign exchange rates

on:

a. Short-term basis (for example, three months)

b. Long-term basis (for example, six years)

Answer.

PROBLEMS

1. Suppose that the treasurer of IBM has an extra cash reserve of $100,000,000 to invest for

six months. The six-month interest rate is 8 percent per annum in the United States and 7

percent per annum in Germany. Currently, the spot exchange rate is €1.01 per dollar and the

six-month forward exchange rate is €0.99 per dollar. The treasurer of IBM does not wish to bear

any exchange risk. Where should he/she invest to maximize the return?

Solution: The market conditions are summarized as follows:

2. While you were visiting London, you purchased a Jaguar for £35,000, payable in three

months. You have enough cash at your bank in New York City, which pays 0.35% interest per

month, compounding monthly, to pay for the car. Currently, the spot exchange rate is $1.45/£

and the three-month forward exchange rate is $1.40/£. In London, the money market interest

rate is 2.0% for a three-month investment. There are two alternative ways of paying for your

Jaguar.

(a) Keep the funds at your bank in the U.S. and buy £35,000 forward.

(b) Buy a certain pound amount spot today and invest the amount in the U.K. for three months

so that the maturity value becomes equal to £35,000.

Evaluate each payment method. Which method would you prefer? Why?

Solution: The problem situation is summarized as follows:

Option a:

3. Currently, the spot exchange rate is $1.50/£ and the three-month forward exchange rate is

$1.52/£. The three-month interest rate is 8.0% per annum in the U.S. and 5.8% per annum in

the U.K. Assume that you can borrow as much as $1,500,000 or £1,000,000.

a. Determine whether the interest rate parity is currently holding.

b. If the IRP is not holding, how would you carry out covered interest arbitrage? Show all the

steps and determine the arbitrage profit.

c. Explain how the IRP will be restored as a result of covered arbitrage activities.

Solution: Let’s summarize the given data first:

c. Following the arbitrage transactions described above,

4. Currently, the spot exchange rate is $0.85/A$ and the one-year forward exchange rate

is $0.81/A$. One-year interest is 3.5% in the United States and 4.2% in Australia.

You may borrow up to $1,000,000 or A$1,176,471, which is equivalent to $1,000,000

at the current spot rate.

a. Determine if IRP is holding between Australia and the United States.

b. If IRP is not holding, explain in detail how you would realize certain profit in U.S. dollar

terms.

c. Explain how IRP will be restored as a result of arbitrage transactions you carry out above.

Solution:

a. (1+i$) = 1.035

b. (1) Borrow A$1,176,471 and repay A$1,225,883 in one year.

5. Suppose that the current spot exchange rate is €0.80/$ and the three-month forward

exchange rate is €0.7813/$. The three-month interest rate is 5.60 percent per annum in the

United States and 5.40 percent per annum in France. Assume that you can borrow up to

$1,000,000 or €800,000.

a. Show how to realize a certain profit via covered interest arbitrage, assuming that you want to

realize profit in terms of U.S. dollars. Also determine the size of your arbitrage profit.

b. Assume that you want to realize profit in terms of euros. Show the covered arbitrage process

and determine the arbitrage profit in euros.

Solution:

a. (1+ i$) = 1.014 < (F/S) (1+ i €) = 1.0378. Thus, one has to borrow dollars and invest in euros

to make arbitrage profit.

6. In the October 23, 1999 issue, the Economist reports that the interest rate per annum is

5.93% in the United States and 70.0% in Turkey. Why do you think the interest rate is so high in

Turkey? Based on the reported interest rates, how would you predict the change of the

exchange rate between the U.S. dollar and the Turkish lira?

Solution: A high Turkish interest rate must reflect a high expected inflation in Turkey. According

to international Fisher effect (IFE), we have

7. As of November 1, 1999, the exchange rate between the Brazilian real and U.S. dollar is

R$1.95/$. The consensus forecast for the U.S. and Brazil inflation rates for the next 1-year

period is 2.6% and 20.0%, respectively. What would you forecast the exchange rate to be at

around November 1, 2000?

Solution: Since the inflation rate is quite high in Brazil, we may use the purchasing power parity

to forecast the exchange rate.

8. (CFA question) Omni Advisors, an international pension fund manager, uses the concepts of

purchasing power parity (PPP) and the International Fisher Effect (IFE) to forecast spot

exchange rates. Omni gathers the financial information as follows:

Base price level 100

Current U.S. price level 105

Current South African price level 111

Base rand spot exchange rate $0.175

Current rand spot exchange rate $0.158

Expected annual U.S. inflation 7%

Expected annual South African inflation 5%

Expected U.S. one-year interest rate 10%

Expected South African one-year interest rate 8%

Calculate the following exchange rates (ZAR and USD refer to the South African rand and U.S.

dollar, respectively).

a. The current ZAR spot rate in USD that would have been forecast by PPP.

b. Using the IFE, the expected ZAR spot rate in USD one year from now.

c. Using PPP, the expected ZAR spot rate in USD four years from now.

Solution:

9. Suppose that the current spot exchange rate is €1.50/₤ and the one-year forward exchange

rate is €1.60/₤. The one-year interest rate is 5.4% in euros and 5.2% in pounds. You can borrow

at most €1,000,000 or the equivalent pound amount, i.e., ₤666,667, at the current spot

exchange rate.

a. Show how you can realize a guaranteed profit from covered interest arbitrage. Assume that

you are a euro-based investor. Also determine the size of the arbitrage profit.

b. Discuss how the interest rate parity may be restored as a result of the above

transactions.

c. Suppose you are a pound-based investor. Show the covered arbitrage process and

determine the pound profit amount.

Solution:

a. First, note that (1+i €) = 1.054 is less than (F/S)(1+i €) = (1.60/1.50)(1.052) = 1.1221.

b. As a result of the above arbitrage transactions, the euro interest rate will rise, the pound

10. Due to the integrated nature of their capital markets, investors in both the U.S. and U.K.

require the same real interest rate, 2.5%, on their lending. There is a consensus in capital

markets that the annual inflation rate is likely to be 3.5% in the U.S. and 1.5% in the U.K. for the

next three years. The spot exchange rate is currently $1.50/£.

a. Compute the nominal interest rate per annum in both the U.S. and U.K., assuming that the

Fisher effect holds.

b. What is your expected future spot dollar-pound exchange rate in three years from now?

c. Can you infer the forward dollar-pound exchange rate for one-year maturity?

Solution.

11. After studying Iris Hamson’s credit analysis, George Davies is considering whether he can

increase the holding period return on Yucatan Resort’s excess cash holdings (which are held in

pesos) by investing those cash holdings in the Mexican bond market. Although Davies would be

investing in a peso-denominated bond, the investment goal is to achieve the highest holding

period return, measured in U.S. dollars, on the investment.

Davies finds the higher yield on the Mexican one-year bond, which is considered to be

free of credit risk, to be attractive but he is concerned that depreciation of the peso will reduce

the holding period return, measured in U.S. dollars. Hamson has prepared selected economic

and financial data, given in Exhibit 3-1, to help Davies make the decision.

Selected Economic and Financial Data for U.S. and Mexico

Expected U.S. Inflation Rate 2.0% per year

Expected Mexican Inflation Rate 6.0% per year

U.S. One-year Treasury Bond Yield 2.5%

Mexican One-year Bond Yield 6.5%

Nominal Exchange Rates

Spot 9.5000 Pesos = U.S. $ 1.00

One-year Forward 9.8707 Pesos = U.S. $ 1.00

Hamson recommends buying the Mexican one-year bond and hedging the foreign currency

exposure using the one-year forward exchange rate. She concludes: “This transaction will result

in a U.S. dollar holding period return that is equal to the holding period return of the U.S. one-

year bond.”

a. Calculate the U.S. dollar holding period return that would result from the transaction

recommended by Hamson. Show your calculations. State whether Hamson’s conclusion

about the U.S. dollar holding period return resulting from the transaction is correct or

incorrect. After conducting his own analysis of the U.S. and Mexican economies, Davies

expects that both the U.S. inflation rate and the real exchange rate will remain constant over

the coming year. Because of favorable political developments in Mexico, however, he

expects that the Mexican inflation rate (in annual terms) will fall from 6.0 percent to 3.0

percent before the end of the year. As a result, Davies decides to invest Yucatan Resorts’

cash holdings in the Mexican one-year bond but not to hedge the currency exposure.

b. Calculate the expected exchange rate (pesos per dollar) one year from now. Show your

calculations. Note: Your calculations should assume that Davies is correct in his

expectations about the real exchange rate and the Mexican and U.S. inflation rates.

c. Calculate the expected U.S. dollar holding period return on the Mexican one-year bond.

Show your calculations. Note: Your calculations should assume that Davies is correct in his

expectations about the real exchange rate and the Mexican and U.S. inflation rates.

Solution:

a. The U.S. dollar holding period return that would result from the transaction recommended by

Hamson is 2.5%. The investor can buy “x” amount of pesos at the (indirect) spot exchange

rate, invest these “x” pesos in the Mexican bond market and have “x × (1 + YMEX)” pesos in

one year, and convert these pesos back into dollars using the (indirect) forward exchange

Solving for YUS:

b. The expected exchange rate one year from now is 9.5931. The rate can be calculated by

using the formula:

c. The expected U.S. dollar holding period return on the Mexican one-year bond is 5.47%. The

12. James Clark is a foreign exchange trader with Citibank. He notices the following quotes.

Spot exchange rate SFr1.2051/$

Six-month forward exchange rate SFr1.1922/$

Six-month $ interest rate 2.5% per year

Six-month SFr interest rate 2.0% per year

a. Is the interest rate parity holding? You may ignore transaction costs.

b. Is there an arbitrage opportunity? If yes, show what steps need to be taken to make

arbitrage profit. Assuming that James Clark is authorized to work with $1,000,000, compute

the arbitrage profit in dollars.

Solution:

a. For six months, iSFr = 1.0% and i$ = 1.25%. the spot exchange rate is $0.8298/SFr and the

b. Because IRP is not holding, there is an arbitrage possibility: Because 1.0125 < 1.02095, we

can say that the SFr interest rate quote is more than what it should be as per the quotes for

the other three variables. Equivalently, we can also say that the $ interest rate quote is less

than what it should be as per the quotes for the other three variables. Therefore, the

arbitrage strategy should be based on borrowing in the $ market and lending in the SFr

market. The steps would be as follows:

13. Suppose you conduct currency carry trade by borrowing $1 million at the start of each year

and investing in New Zealand dollar for one year. One-year interest rates and the exchange rate

between the U.S. dollar ($) and New Zealand dollar (NZ$) are provided below for the period

2000 – 2009. Note that interest rates are one-year interbank rates on January 1st each year, and

that the exchange rate is the amount of New Zealand dollar per U.S. dollar on December 31

each year. The exchange rate was NZ$1.9088/$ on January 1, 2000. Fill out the columns (4) –

(7) and compute the total dollar profits from this carry trade over the ten-year period. Also,

assess the validity of uncovered interest rate parity based on your solution of this problem. You

are encouraged to use Excel program to tackle this problem.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

Year

iNZ$

i$

SNZ$/$

iNZ$ - i$

eNZ$/$

(4)-(5)

$ Profit

2000

6.53

6.50

2.2599

2001

6.70

6.00

2.4015

2002

4.91

2.44

1.9117

2003

5.94

1.45

1.5230

2004

5.88

1.46

1.3845

2005

6.67

3.10

1.4682

2006

7.28

4.84

1.4182

2007

8.03

5.33

1.2994

2008

9.10

4.22

1.7112

2009

5.10

2.00

1.3742

Data source: Datastream.

Solution:

(1)

(2)

(3)

(4)

(5)

(6)

(7)

Year

iNZ$

i$

SNZ$/$

iNZ$ - i$

eNZ$/$

(4)-(5)

$ Profit

2000

6.53

6.50

2.2599

0.03

18.40

-18.37

-183655

2001

6.70

6.00

2.4015

0.7

6.27

-5.57

-55680

2002

4.91

2.44

1.9117

2.47

-20.40

22.87

228676

Notes:

1. Interest rates are interbank 1-year rates on January 1st of each year and measured in percent

terms.

Veritas Emerging Market Fund specializes in investing in emerging stock markets of the world.

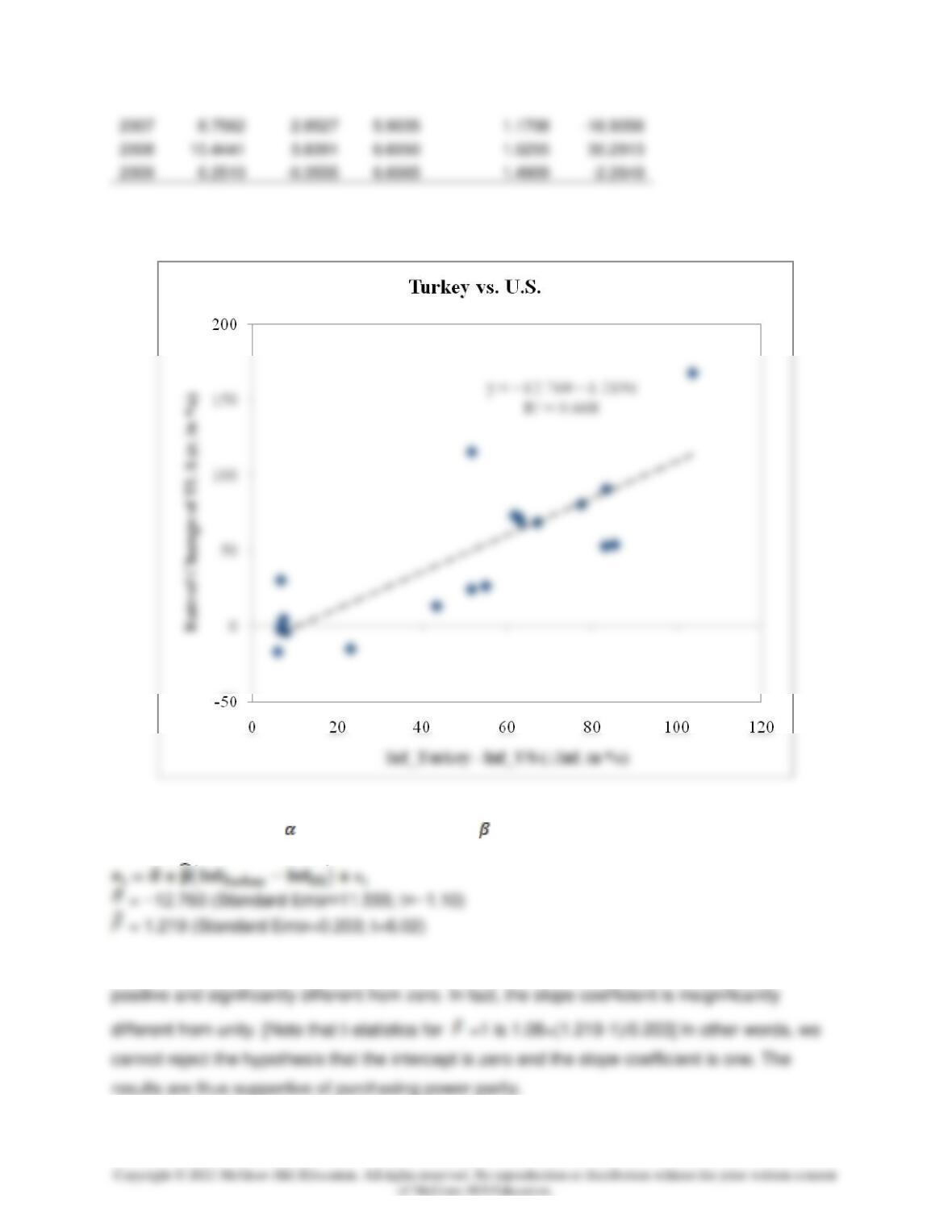

Mr. Henry Mobaus, an experienced hand in international investment and your boss, is currently

interested in Turkish stock markets. He thinks that Turkey will eventually be invited to negotiate

its membership in the European Union. If this happens, it will boost the stock prices in Turkey.

But, at the same time, he is quite concerned with the volatile exchange rates of the Turkish

currency. He would like to understand what drives the Turkish exchange rates. Since the

inflation rate is much higher in Turkey than in the U.S., he thinks that the purchasing power

parity may be holding at least to some extent. As a research assistant for him, you were

assigned to check this out. In other words, you have to study and prepare a report on the

following question: Does the purchasing power parity hold for the Turkish lira-U.S. dollar

exchange rate? Among other things, Mr. Mobaus would like you to do the following:

1. Plot past annual exchange rate changes against the differential inflation rates between

Turkey and the U.S. for the last 20 years.

2. Regress the annual rate of exchange rate changes on the annual inflation rate differential to

estimate the intercept and the slope coefficient, and interpret the regression results.

Solution:

Inf_TK (%)

(1)

Inf_US (%)

(2)

∆Inf

(1)-(2)

S(TL/$)

End-of-year rate

∆St/St-1 (%)

:= et

1989

0.0023

1990

60.3127

5.3980

54.9147

0.0029

26.6406

1996

80.3469

2.9312

77.4157

0.1078

80.6790

1998

84.6413

1.5523

83.0890

0.3145

52.9457

2000

54.9154

3.3769

51.5385

0.6734

24.3785

2002

44.9641

1.5860

43.3781

1.6437

13.3485

2004

10.5842

2.6772

7.9070

1.3395

-4.0912

2006

10.5110

3.2259

7.2851

1.4090

4.7545

Solution:

1. In the current solution, we use the annual data from 1990 to 2009.

2. We regress the rate of exchange rate changes (e) on the inflation rate differential and

estimate the intercept ( ) and slope coefficient ( ):

The estimated intercept is insignificantly different from zero, whereas the slope coefficient is