Chapter 5

Currency Derivatives

Lecture Outline

Forward Market

How MNCs Use Forward Contracts

Bank Quotations on Forward Rates

Premium or Discount on Forward Rate

Movements in the Forward Rate Over Time

Currency Futures Market

Contract Specifications

Trading Currency Futures

Credit Risk of Currency Futures Contracts

Comparing Currency Futures Contracts to Forward Contracts

How MNCs Use Currency Futures Contracts

Speculation with Currency Futures

Currency Options Market

Currency Options Exchanges

Conditional Currency Options

European Currency Options

Currency Derivatives ❖ 2

Chapter Theme

This chapter provides an overview of currency derivatives, which are sometimes referred to as

“speculative.” Yet, firms are increasing their use of these instruments for hedging purposes. The chapter

Topics to Stimulate Class Discussion

1. What advantage do currency options offer that are not available with futures or forward contracts?

2. What are some disadvantages of currency option contracts?

3. Why do currency futures prices change over time?

POINT/COUNTER-POINT:

Should Speculators Use Currency Futures or Options?

POINT: Speculators should use currency futures because they can avoid a substantial premium. To the

extent that they are willing to speculate, they must have confidence in their expectations. If they have

sufficient confidence in their expectations, they should bet on their expectations without having to pay a

large premium to cover themselves if they are wrong. If they do not have confidence in their expectations,

they should not speculate at all.

COUNTER-POINT: Speculators should use currency options to fit the degree of their confidence. For

example, if they are very confident that a currency will appreciate substantially, but want to limit their

investment, they can buy deep out-of-the-money options. These options, which have a high exercise price

but a low premium, require a relatively small investment. Alternatively, speculators can buy options that

have a lower exercise price (higher premium), which will likely generate a greater return if the currency

appreciates. Speculation involves risk. Speculators must recognize that their expectations may be wrong.

While options require a premium, the premium is worthwhile as a means to limit the potential downside

risk. Options enable speculators to select the degree of downside risk that they are willing to tolerate.

WHO IS CORRECT? Use the Internet to learn more about this issue. Which argument do you support?

Offer your own opinion on this issue.

ANSWER: By comparing futures with options, students should recognize the tradeoff that is formed by

the two opposing arguments. The choice of options versus futures may depend on the probability

Currency Derivatives ❖ 3

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

but want to cover against possible depreciation may be willing to buy call options so that their downside

risk is limited to what they pay for the call option.

Answers to End of Chapter Questions

1. Forward versus Futures Contracts. Compare and contrast forward and futures contracts.

2. Using Currency Futures.

a. How can corporations use currency futures?

ANSWER: U.S. corporations that desire to lock in a price at which they can sell a foreign currency

b. How can speculators use currency futures?

3. Currency Options. Differentiate between a currency call option and a currency put option.

4. Forward Premium. Compute the forward discount or premium for the Mexican peso whose 90-day

forward rate is $.102 and spot rate is $.10. State whether your answer is a discount or premium.

5. Effects of a Forward Contract. How can a forward contract backfire?

6. Hedging with Currency Options. When would a U.S. firm consider purchasing a call option on

euros for hedging? When would a U.S. firm consider purchasing a put option on euros for hedging?

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

7. Speculating with Currency Options. When should a speculator purchase a call option on Australian

dollars? When should a speculator purchase a put option on Australian dollars?

8. Currency Call Option Premiums. List the factors that affect currency call option premiums and

briefly explain the relationship that exists for each. Do you think an at-the-money call option in euros

has a higher or lower premium than an at-the-money call option in Mexican pesos (assuming the

expiration date and the total dollar value represented by each option are the same for both options)?

ANSWER: These factors are listed below:

• The higher the existing spot rate relative to the strike price, the greater is the call option value,

9. Currency Put Option Premiums. List the factors that affect currency put options and briefly explain

the relationship that exists for each.

ANSWER: These factors are listed below:

10. Speculating with Currency Call Options. Randy Rudecki purchased a call option on British pounds

for $.02 per unit. The strike price was $1.45 and the spot rate at the time the option was exercised

was $1.46. Assume there are 31,250 units in a British pound option. What was Randy’s net profit on

this option?

ANSWER:

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

15. Speculating with Currency Futures. Assume that the euro’s spot rate has moved in cycles over

time. How might you try to use futures contracts on euros to capitalize on this tendency? How could

you determine whether such a strategy would have been profitable in previous periods?

ANSWER: Use recent movements in the euro to forecast future movements. A cycle implies that a

16. Hedging with Currency Derivatives. Assume that the transactions listed in the first column of the

following table are anticipated by U.S. firms that have no other foreign transactions. Place an “X” in

the table wherever you see possible ways to hedge each of the transactions.

a. Georgetown Co. plans to purchase Japanese goods denominated in yen.

b. Harvard, Inc., sold goods to Japan, denominated in yen.

c. Yale Corp. has a subsidiary in Australia that will be remitting funds to the U.S. parent.

d. Brown, Inc., needs to pay off existing loans that are denominated in Canadian dollars.

e. Princeton Co. may purchase a company in Japan in the near future (but the deal may not go through).

ANSWER:

Forward Contract Futures Contract Options Contract

Forward Forward Buy Sell Purchase Purchase

Purchase Sale Futures Futures Calls Puts

17. Price Movements of Currency Futures. Assume that on November 1, the spot rate of the British

pound was $1.58 and the price on a December futures contract was $1.59. Assume that the pound

depreciated during November so that by November 30 it was worth $1.51.

a. What do you think happened to the futures price over the month of November? Why?

Currency Derivatives ❖ 7

b. If you had known that this would occur, would you have purchased or sold a December futures

contract in pounds on November 1? Explain.

ANSWER: You would have sold futures at the existing futures price of $1.59. Then as the spot rate

18. Speculating with Currency Futures. Assume that a March futures contract on Mexican pesos was

available in January for $.09 per unit. Also assume that forward contracts were available for the same

settlement date at a price of $.092 per peso. How could speculators capitalize on this situation,

assuming zero transaction costs? How would such speculative activity affect the difference between

the forward contract price and the futures price?

ANSWER: Speculators could purchase peso futures for $.09 per unit, and simultaneously sell pesos

19. Speculating with Currency Call Options. LSU Corp. purchased Canadian dollar call options for

speculative purposes. If these options are exercised, LSU will immediately sell the Canadian dollars

in the spot market. Each option was purchased for a premium of $.03 per unit, with an exercise price

of $.75. LSU plans to wait until the expiration date before deciding whether to exercise the options.

Of course, LSU will exercise the options at that time only if it is feasible to do so. In the following

table, fill in the net profit (or loss) per unit to LSU Corp. based on the listed possible spot rates of the

Canadian dollar on the expiration date.

ANSWER:

Possible Spot Rate Net Profit (Loss) per

of Canadian Dollar Unit to LSU Corporation

on Expiration Date if Spot Rate Occurs

20. Speculating with Currency Put Options. Auburn Co. has purchased Canadian dollar put options for

speculative purposes. Each option was purchased for a premium of $.02 per unit, with an exercise

price of $.86 per unit. Auburn Co. will purchase the Canadian dollars just before it exercises the

options (if it is feasible to exercise the options). It plans to wait until the expiration date before

deciding whether to exercise the options. In the following table, fill in the net profit (or loss) per unit

to Auburn Co. based on the listed possible spot rates of the Canadian dollar on the expiration date.

Currency Derivatives ❖ 8

ANSWER:

Possible Spot Rate Net Profit (Loss) per Unit

of Canadian Dollar to Auburn Corporation

on Expiration Date if Spot Rate Occurs

21. Speculating with Currency Call Options. Bama Corp. has sold British pound call options for

speculative purposes. The option premium was $.06 per unit, and the exercise price was $1.58.

Bama will purchase the pounds on the day the options are exercised (if the options are exercised) in

order to fulfill its obligation. In the following table, fill in the net profit (or loss) to Bama Corp. if the

listed spot rate exists at the time the purchaser of the call options considers exercising them.

ANSWER:

Possible Spot Rate at the Net Profit (Loss) per

Time Purchaser of Call Option Unit to Bama Corporation

Considers Exercising Them if Spot Rate Occurs

$1.53 $.06

1.57 .06

1.62 .02

22. Speculating with Currency Put Options. Bulldog, Inc., has sold Australian dollar put options at a

premium of $.01 per unit, and an exercise price of $.76 per unit. It has forecasted the Australian

dollar’s lowest level over the period of concern as shown in the following table. Determine the net

profit (or loss) per unit to Bulldog, Inc., if each level occurs and the put options are exercised at that

time.

ANSWER:

Possible Value Net Profit (Loss) to

of Australian Dollar Bulldog, Inc. if Value Occurs

$.72 –$.03

23. Hedging with Currency Derivatives. A U.S. professional football team plans to play an exhibition

game in the United Kingdom next year. Assume that all expenses will be paid by the British

government, and that the team will receive a check for 1 million pounds. The team anticipates that the

pound will depreciate substantially by the scheduled date of the game. In addition, the National Foot-

Currency Derivatives ❖ 9

ball League must approve the deal, and approval (or disapproval) will not occur for three months.

How can the team hedge its position? What is there to lose by waiting three months to see if the

exhibition game is approved before hedging?

ANSWER: The team could purchase put options on pounds in order to lock in the amount at which it

could convert the 1 million pounds to dollars. The expiration date of the put option should

Advanced Questions

24. Risk of Currency Futures. Currency futures markets are commonly used as a means of capitalizing

on shifts in currency values, because the value of a futures contract tends to move in line with the

change in the corresponding currency value. Recently, many currencies have appreciated against the

dollar. Most speculators anticipated that these currencies would continue to strengthen and took large

buy positions in currency futures. However, the Fed intervened in the foreign exchange market by

immediately selling foreign currencies in exchange for dollars, causing an abrupt decline in the values

of foreign currencies (as the dollar strengthened). Participants that had purchased currency futures

contracts incurred large losses. One prominent trader responded to the effects of the Fed’s

intervention by immediately selling 300 futures contracts on British pounds (with a value of about

$30 million). Such actions caused even more panic in the futures market.

a. Explain why the central bank’s intervention caused such panic among currency futures traders

with buy positions.

ANSWER: Futures prices on pounds rose in tandem with the value of the pound. However, when

central banks intervened to support the dollar, the value of the pound declined, and so did values of

futures contracts on pounds. So traders with long (buy) positions in these contracts experienced

losses because the contract values declined.

b. Explain why the prominent trader’s willingness to sell 300 pound futures contracts at the going

market rate aroused such concern. What might this action signal to other traders?

c. Explain why speculators with short (sell) positions could benefit as a result of the central bank’s

intervention.

Currency Derivatives ❖ 10

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

purchasing the same contracts that they had sold earlier. Since the prices of futures contracts

declined, they would purchase the contracts for a lower price than the price at which they initially

sold the contracts.

d. Some traders with buy positions may have responded immediately to the central bank’s

intervention by selling futures contracts. Why would some speculators with buy positions leave

their positions unchanged or even increase their positions by purchasing more futures contracts in

response to the central bank’s intervention?

25. Estimating Profits from Currency Futures and Options. One year ago, you sold a put option

on 100,000 euros with an expiration date of one year. You received a premium on the put option of

$.04 per unit; the exercise price was $1.22. Assume that one year ago, the spot rate of the euro was

$1.20, the one-year forward rate exhibited a discount of 2%, and the one-year futures price was the

same as the one-year forward rate. From one year ago to today, the euro depreciated against the

dollar by 4 percent. Today the put option will be exercised (if it is feasible for the buyer to do so).

a. Determine the total dollar amount of your profit or loss from your position in the put option.

b. Now assume that instead of taking a position in the put option one year ago, you sold a futures

contract on 100,000 euros with a settlement date of one year. Determine the total dollar amount of

your profit or loss.

ANSWER:

a. The spot rate depreciated from $1.20 to $1.152.

26. Impact of Information on Currency Futures and Options Prices. Myrtle Beach Co. purchases

imports that have a price of 400,000 Singapore dollars and it has to pay for the imports in 90 days. It

can purchase a 90-day forward contract on Singapore dollars at $.50 or purchase a call option contract

on Singapore dollars with an exercise price of $.50 to cover its payables. This morning, the spot rate

of the Singapore dollar was $.50. At noon, the central bank of Singapore raised interest rates, while

there was no change in interest rates in the U.S. These actions immediately increased the degree of

uncertainty surrounding the future value of the Singapore dollar over the next three months. The

Singapore dollar’s spot rate remained at $.50 throughout the day.

a. Myrtle Beach Co. is convinced that the Singapore dollar will definitely appreciate substantially

over the next 90 days. Would a call option hedge or forward hedge be more appropriate given its

opinion?

b. Assume that Myrtle Beach uses a currency options contract to hedge rather than a forward

contract. If the company purchased a currency call option contract at the money on Singapore

dollars this afternoon, would its total U.S. dollar cash outflows be more than, less than, or the

Currency Derivatives ❖ 11

same as the total U.S. dollar cash outflows if it had purchased a currency call option contract at

the money this morning? Explain.

ANSWER:

a. A forward hedge would be more appropriate, because it can lock in payment at $.50 per unit with

27. Currency Straddles. Reska, Inc., has constructed a long euro straddle. A call option on euros with an

exercise price of $1.10 has a premium of $.025 per unit. A euro put option has a premium of $.017

per unit. Some possible euro values at option expiration are shown in the following table. (See

Appendix B in this chapter.)

Value of Euro at Option Expiration

$.90

$1.05

$1.50

$2.00

Call

Put

Net

a. Complete the worksheet and determine the net profit per unit to Reska Inc. for each possible

future spot rate.

b. Determine the break-even point(s) of the long straddle. What are the break-even points of a short

straddle using these options?

ANSWER:

a.

Value of Euro at Option Expiration

$.90

$1.05

$1.50

$2.00

Call

–$.025

–$.025

+$.375

+$.875

Put

+$.183

+$.033

–$.017

–$.017

Net

+$.158

+$.008

+$.358

+$.858

b. The break-even points for a long straddle can be found by subtracting and adding both premiums

28. Currency Straddles. Refer to the previous question but assume that the call and put option premiums

are $.02 per unit and $.015 per unit, respectively. (See Appendix B in this chapter.)

a. Construct a contingency graph for a long euro straddle.

b. Construct a contingency graph for a short euro straddle.

ANSWER:

Currency Derivatives ❖ 12

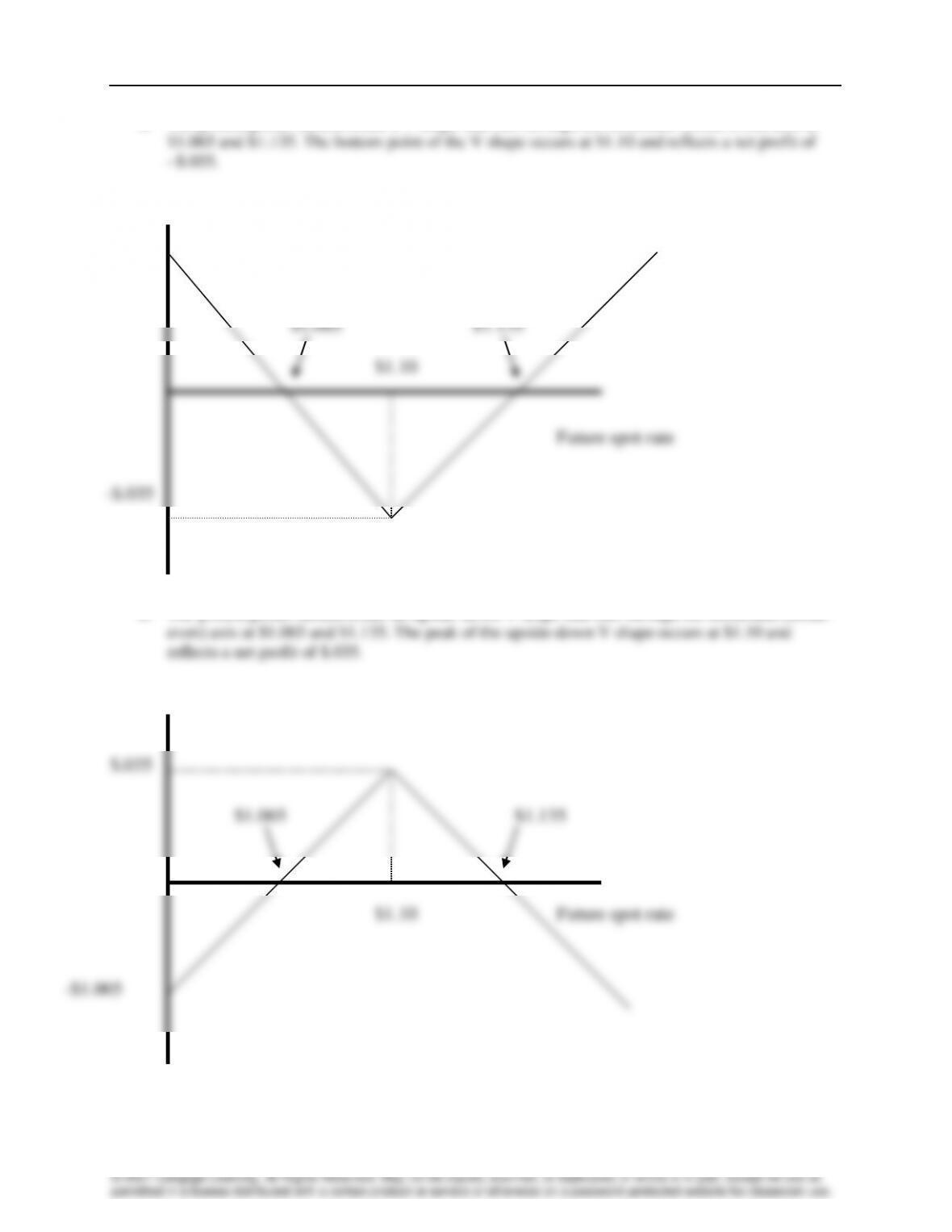

a. The plotted points should create a V shape that cuts through the horizontal (break-even) axis at

Net profit per unit

b. The plotted points should create an upside-down V shape that cuts through the horizontal (break-

Net profit per unit

Future spot rate

$1.065

$1.135

$1.10

Future spot rate

$1.065

$1.135

$1.10

-$.035

$1.065

-$1.065

$.035

Currency Derivatives ❖ 13

29. Currency Option Contingency Graphs. (See Appendix B in this chapter.) The current spot rate of

the Singapore dollar (S$) is $.50. The following option information is available:

• Call option premium on Singapore dollar (S$) = $.015

• Put option premium on Singapore dollar (S$) = $.009

• Call and put option strike price = $.55

• One option contract represents S$70,000

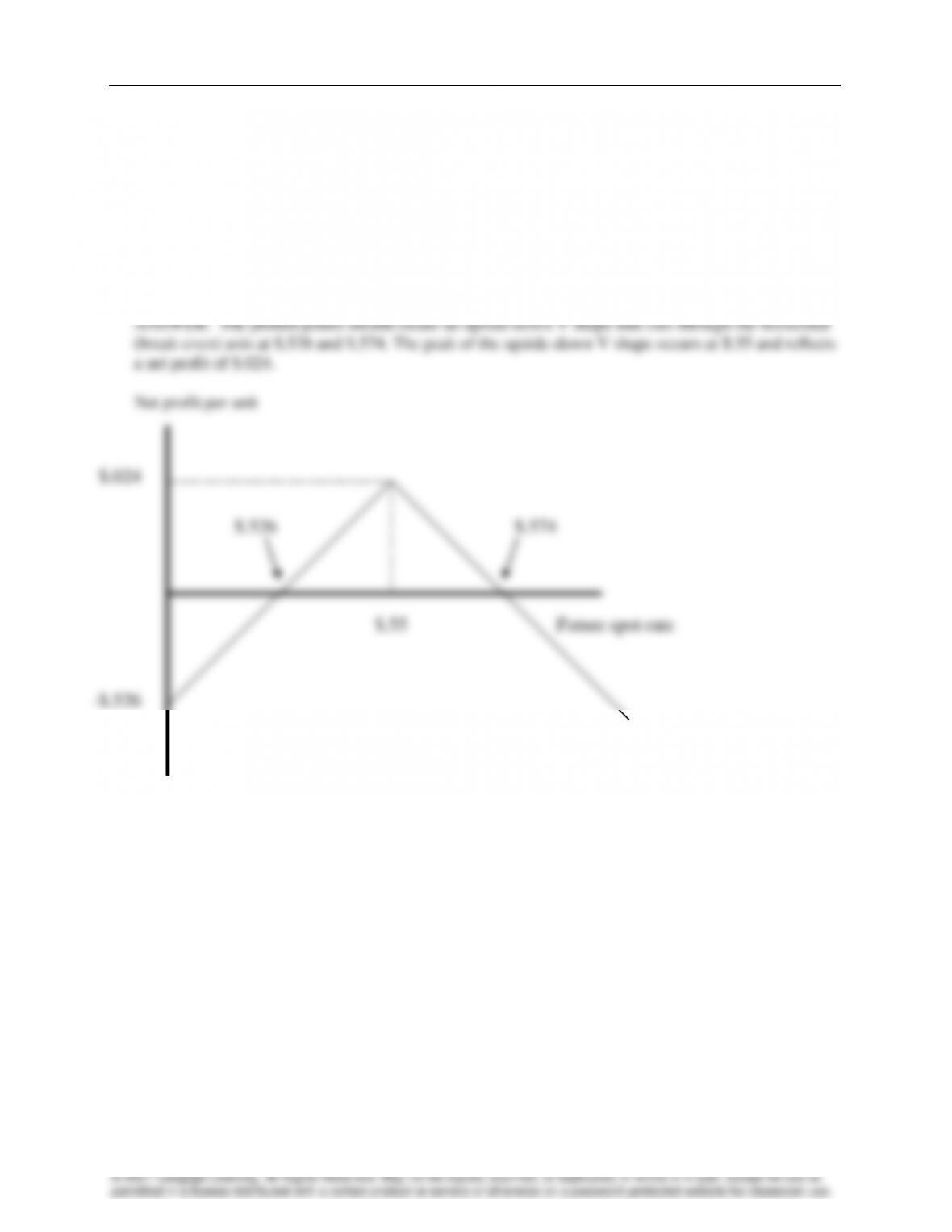

Construct a contingency graph for a short straddle using these options.

30. Speculating with Currency Straddles. Maggie Hawthorne is a currency speculator. She has noticed

recently that the euro has appreciated substantially against the U.S. dollar. The current exchange rate

of the euro is $1.15. After reading a variety of articles on the subject, Maggie believes that the euro

will continue to fluctuate substantially in the months to come. Although most forecasters expect that

the euro will depreciate against the dollar in the near future, Maggie thinks that there is also a good

possibility of further appreciation. Currently, a call option on euros is available with an exercise price

of $1.17 and a premium of $.04. A euro put option with an exercise price of $1.17 and a premium of

$.03 is also available. (See Appendix B in this chapter.)

a. Describe how Maggie could use straddles to speculate on the euro’s value.

b. At option expiration, the value of the euro is $1.30. What is Maggie’s total profit or loss from a

long straddle position?

Future spot rate

$.526

$.574

$.55

-$.526

$.024

Currency Derivatives ❖ 14

c. What is Maggie’s total profit or loss from a long straddle position if the value of the euro is $1.05

at option expiration?

d. What is Maggie’s total profit or loss from a long straddle position if the value of the euro at

option expiration is still $1.15?

e. Given your answers to the questions (b) through (d), when is it advantageous for a speculator to

engage in a long straddle? When is it advantageous to engage in a short straddle?

ANSWER:

b.

Per Unit

Per Contract

Selling Price of €

$1.30

$81,250 ($1.30 × 62,500 units)

– Purchase price of €

–1.17

–73,125 ($1.17 × 62,500 units)

– Premium paid for call option

–.04

–2,500 ($.04 × 62,500 units)

– Premium paid for put option

–.03

–1,875 ($.03 × 62,500 units)

= Net profit

$.06

$3,750 ($.06 × 62,500 units)

c.

Per Unit

Per Contract

Selling Price of €

$1.17

$73,125 ($1.17 × 62,500 units)

– Purchase price of €

–1.05

–65,625 ($1.05 × 62,500 units)

– Premium paid for call option

–.04

–2,500 ($.04 × 62,500 units)

– Premium paid for put option

–.03

–1,875 ($.03 × 62,500 units)

= Net profit

$.05

$3,125 ($.05 × 62,500 units)

d.

Per Unit

Per Contract

Selling Price of €

$1.17

$73,125 ($1.17 × 62,500 units)

– Purchase price of €

–1.15

–71,875 ($1.15 × 62,500 units)

– Premium paid for call option

–.04

–2,500 ($.04 × 62,500 units)

– Premium paid for put option

–.03

–1,875 ($.03 × 62,500 units)

= Net profit

–$.05

–$3,125 ($.05 × 62,500 units)

e. It is advantageous for a speculator to engage in a long straddle if the underlying currency is