Assumptions Values

Singapore dollars to be exchanged SGD 1,000.00

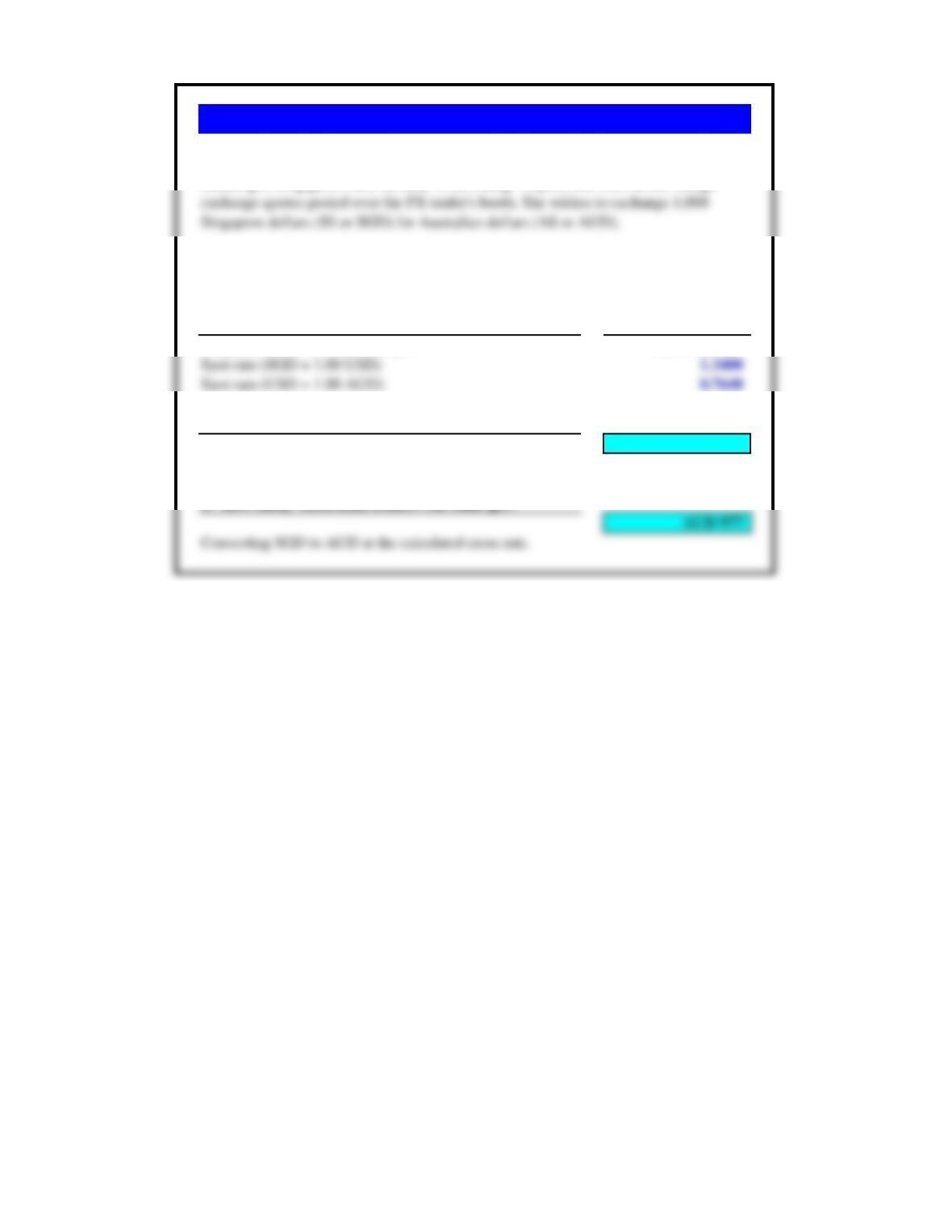

a. What is the SGD per AUD cross rate? 1.0238

SGD per AUD = SGD/USD x USD/SGD

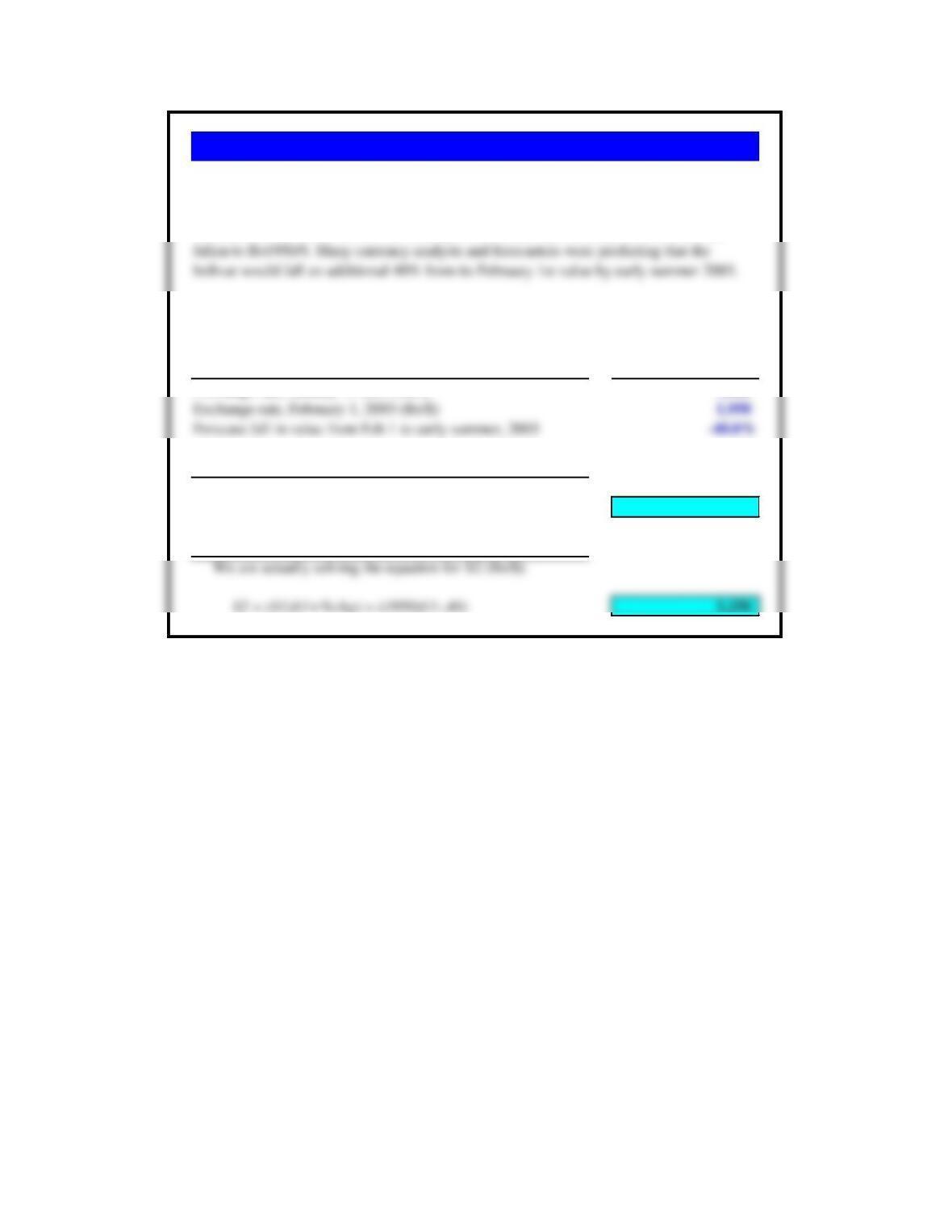

Problem 5.1 Anne Dietz in Changi #3 (Singapore)

Anne Dietz lives in Singapore, but is making her first business trip to Sydney, Australia.

a. What is the Singapore dollar to Australian dollar cross rate?

b. How many Australian dollars will Anne get for her Singapore dollars?

Days

Period Forward

¥/euro US$/euro

spot 0.0083 1.1079

1 month 30 0.0084 1.1100

Days Forward Premium

¥ Proceeds of Difference

Period Forward

¥/euro on the ¥/euro € 2,500,000.00 Over Spot

spot 120.4800 301,200,000.00 –

1 month 30 119.0500 -14.243% 297,625,000.00 -¥3,575,000.00

Days Forward Premium US$ Proceeds of Difference

Period Forward US$/euro on the US$/euro € 2,500,000.00 Over Spot

spot 1.1079 $2,769,750.00 –

1 month 30 1.1100 2.275% $2,775,000.00 $5,250.00

Period

C$/€US$/€

spot 1.3830 1.4389

1 month 1.3840 1.4440

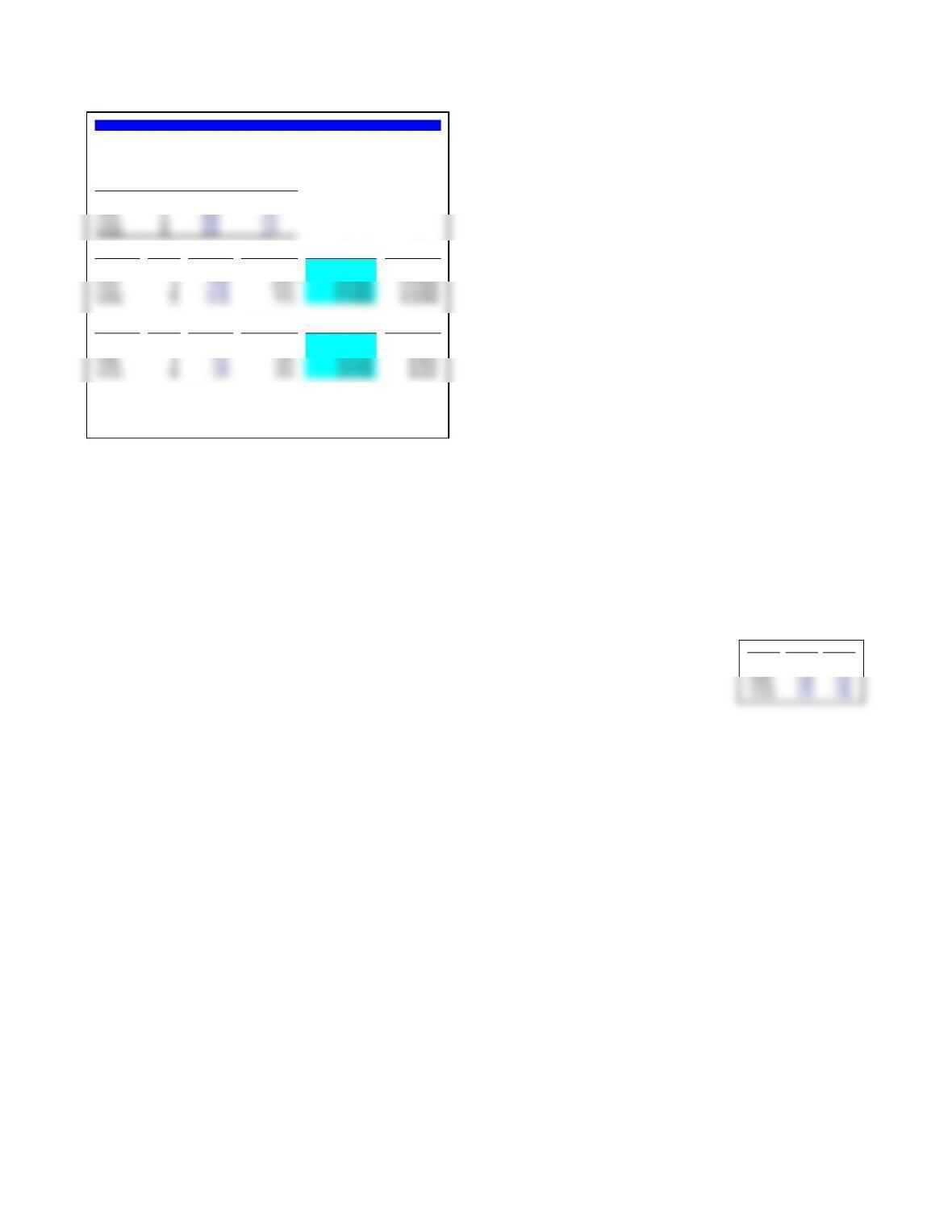

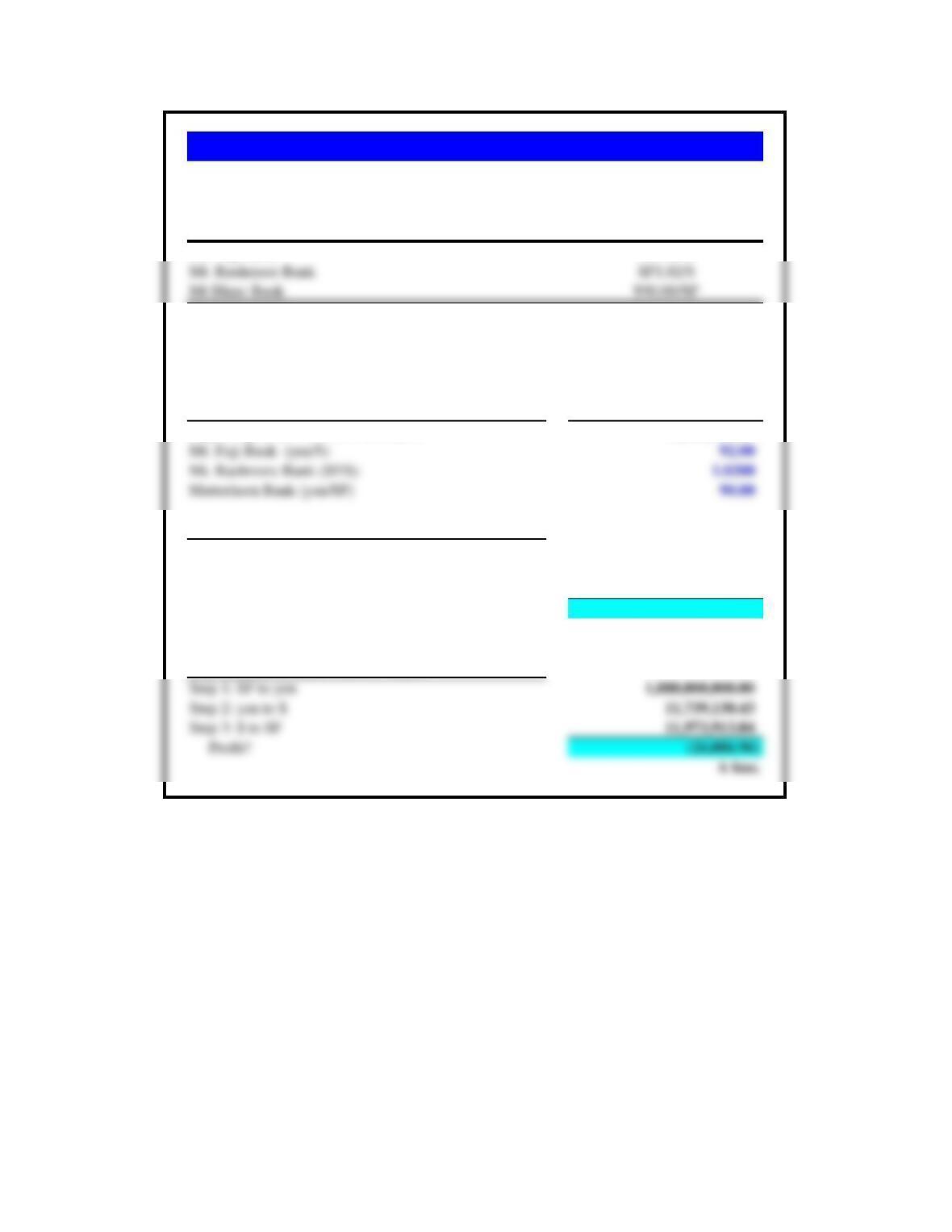

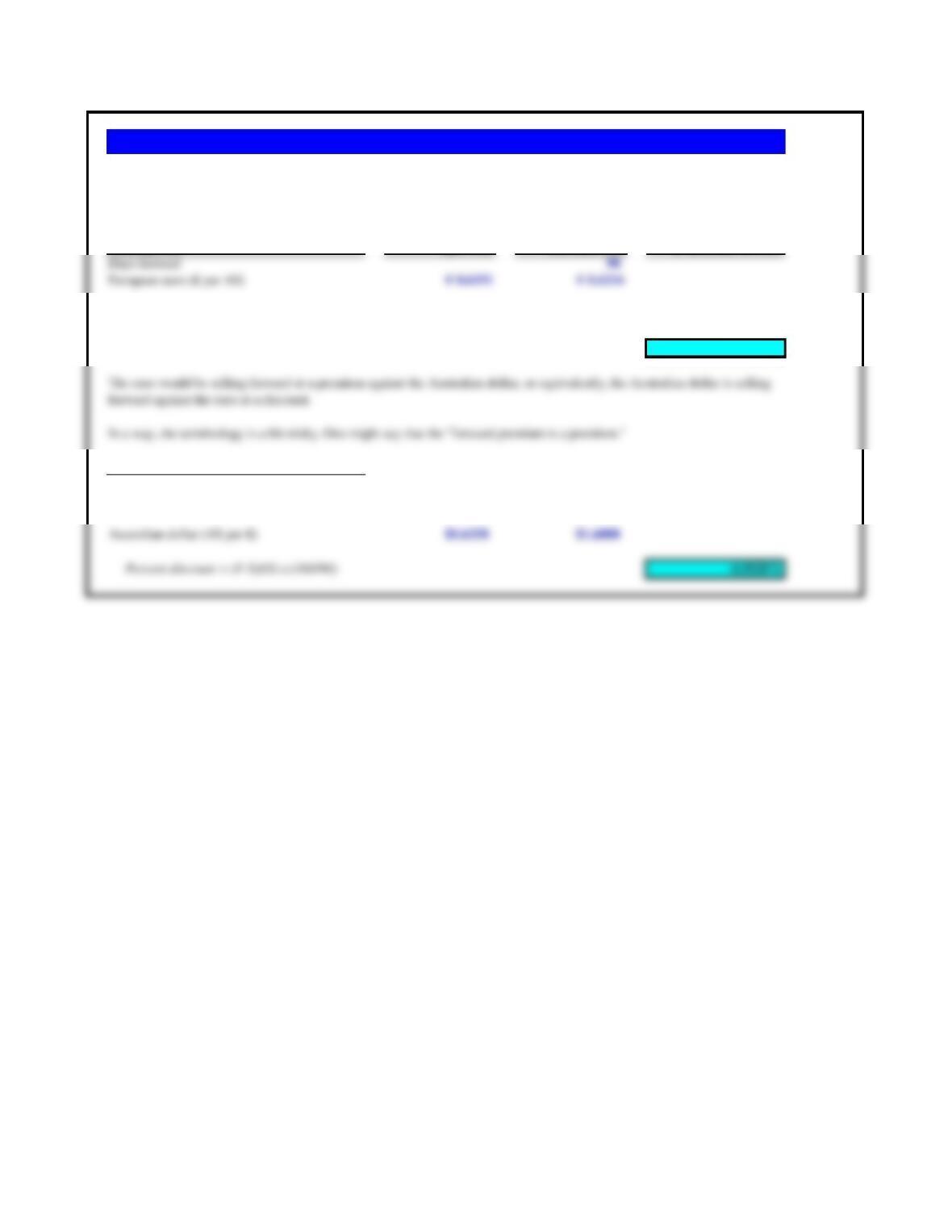

Problem 5.2 Konbanwa Sushi (Japan)

The Japanese exporter will be receiving six payments of 2,500,000 euros, ranging from now to 12 months in the future. Since the company keeps

cash balances in both Japanese yen and US dollars, it can choose which currency to change the euros to at the end of the various periods. And

since the company wishes to lock in the forward rate for each and every payment, it would appear that the company should lock in forward rates

in US$ for all payments. Since the euro is selling forward at discount against the Japanese yen and the euro is selling forward at a premium against

U.S. dollar, the resulting dollar proceeds are higher.

The Japanese sushi franchise, Konbanwa Sushi, will be receiving six payments of €2,500,000 from now to 12 months in the future. Since the

company keeps cash balances in both Japanese yen and U.S. dollars, it can choose which currency to exchange the euros for at the end of the

various periods. Which currency appears to offer the better rates in the forward market?

Period

¥/$

Bid Rate ¥/$

Ask Rate

spot 85.41 85.46

1 month 85.02 85.05

2 months 84.86 84.90

a. What is the mid-rate for each maturity?

b. What is the annual forward premium for all maturities?

c. Which maturities have the smallest and largest forward premiums?

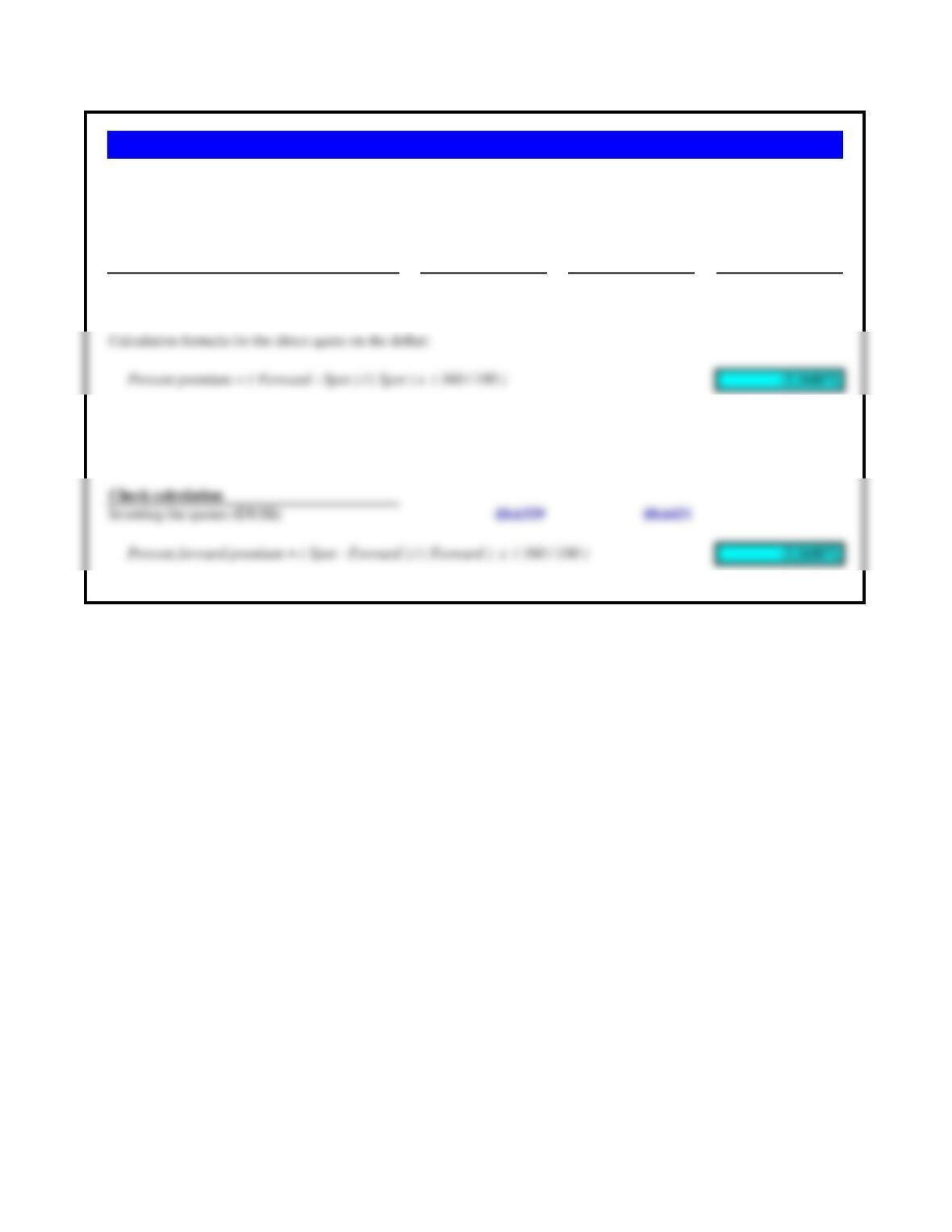

Since the exchange rate quotes are indirect quotes on the dollar (¥/$), the proper forward premium calculation is:

Forward premium = ( Spot – Forward ) / (Forward) x (360 / days)

a. b.

¥/$ ¥/$ Calculated Forward

Period Days Forward Bid Rate Ask Rate Mid-Rate Premium

spot 85.41 85.46 85.43500

1 month 30 85.02 85.05 85.03500 5.6447%

2 months 60 84.86 84.90 84.88000 3.9232%

3 months 90 84.37 84.42 84.39500 4.9292%

The 24 month forward rate has the smallest premium, while the 1 month forward possesses the largest premium.

The forward rates progressively require fewer and fewer Japanese yen per dollar than the current spot rate. Therefore the yen is

selling forward at a premium and the dollar is selling forward at a discount.

¥/$ ¥/$

Period Bid Rate Ask Rate

spot 114.23 114.27

1 month 113.82 113.87

2 months 113.49 113.52

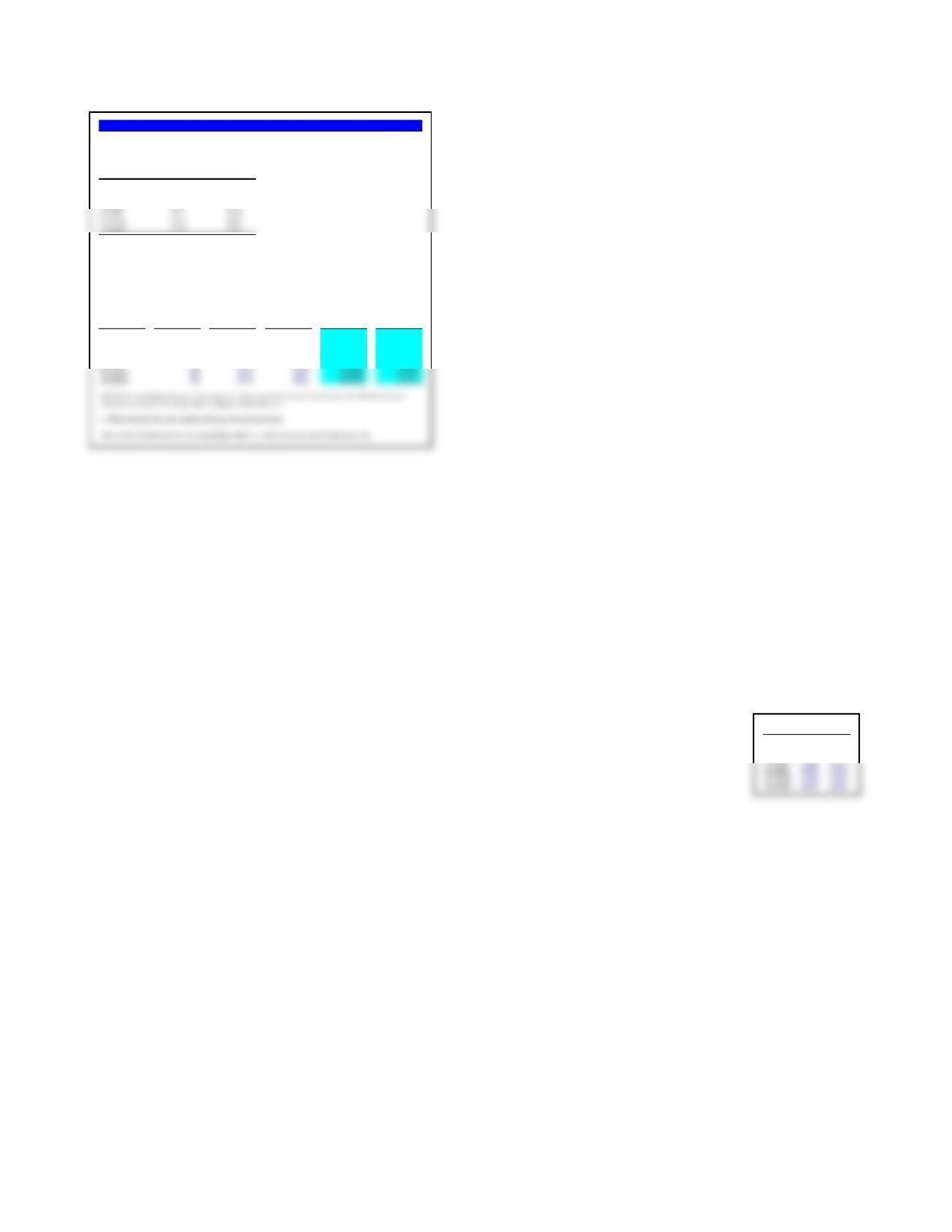

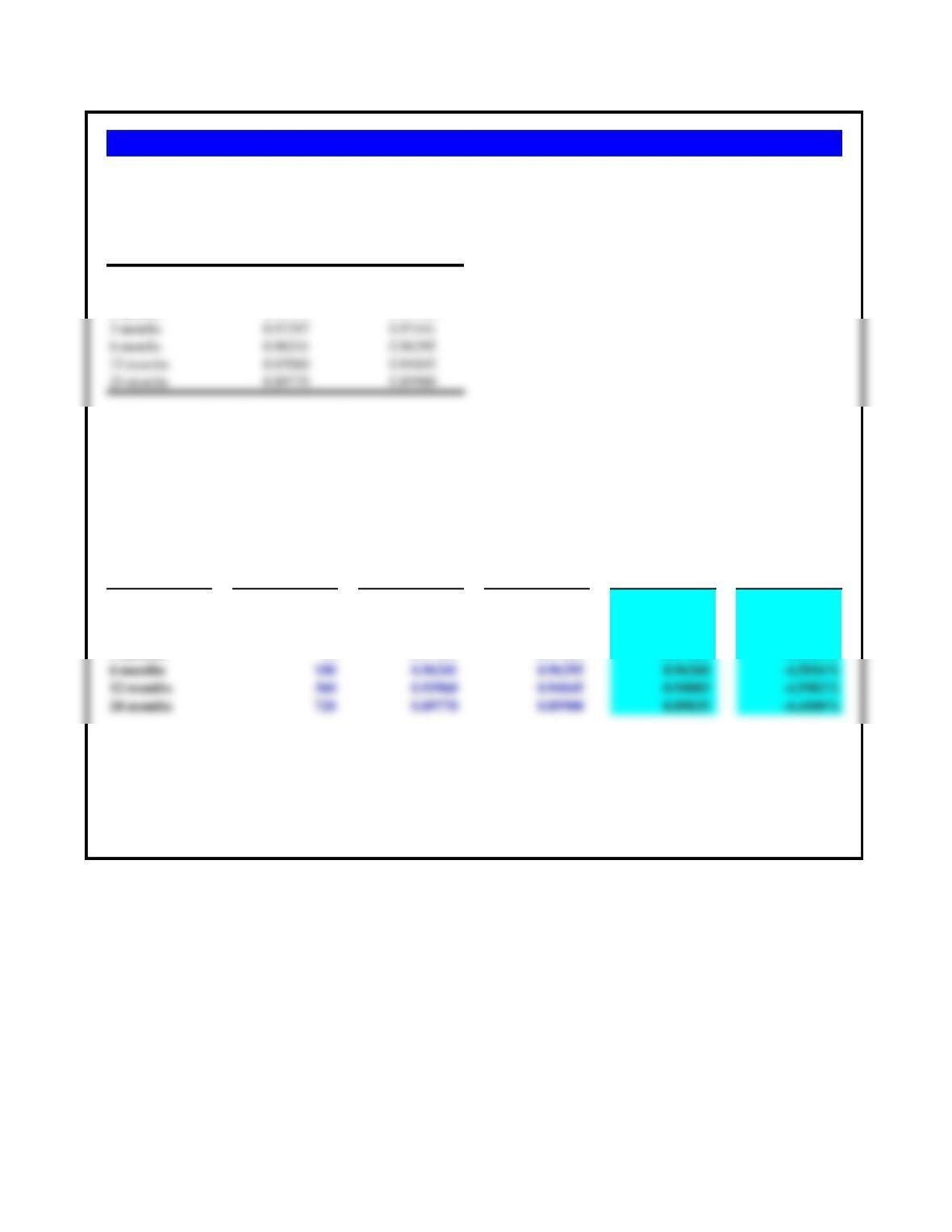

Problem 5.3 Japanese Yen Forward

Use the following spot and forward bid-ask rates for the Japanese yen/U.S. dollar (¥/$) exchange rate from September 16, 2010, to

answer the following questions:

Spot exchange rate:

Bid rate SF 1.2575/$

a. Calculate outright quotes for bid and ask, and the number of points spread between each.

b. What do you notice about the spread as quotes evolve from spot toward six months?

c. What is the 6-month Swiss bill rate?

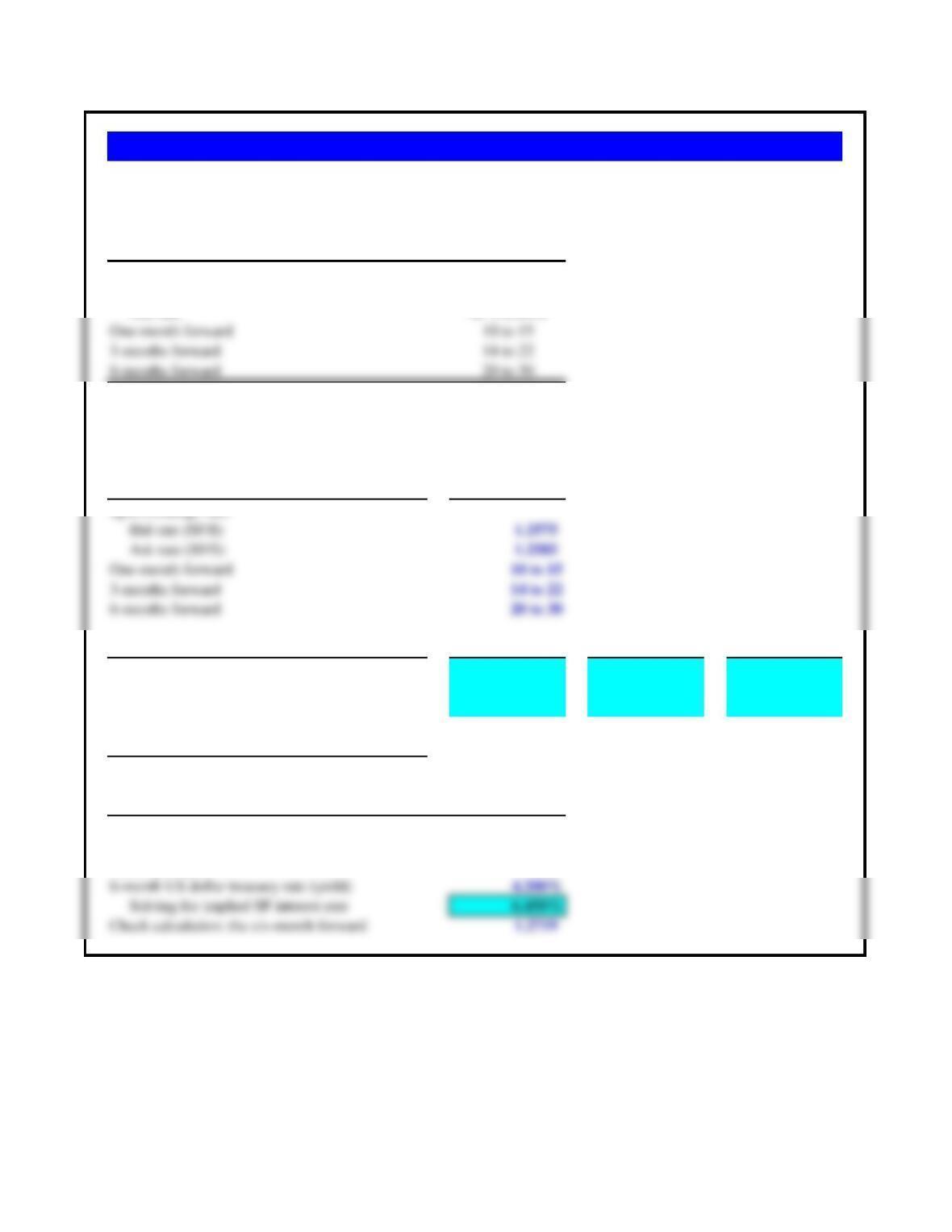

Assumptions Values

a. Calculate outright quotes Bid Ask Spread

One-month forward 1.2585 1.2600 0.0015

3-months forward 1.2589 1.2607 0.0018

6-months forward 1.2595 1.2615 0.0020

b. What do you notice about the spread?

It widens, most likely a result of thinner and thinner trading volume.

c. Added/optional question: What is the 6-month Swiss bill rate?

Spot rate, midrate (SF/$) 1.2580

Six-month forward rate, midrate (SF/$) 1.2605

Maturity (days) 180

Problem 5.4 Andreas Broszio (Geneva)

Andreas Broszio just started as an analyst for Credit Suisse in Geneva, Switzerland. He receives the following quotes

for Swiss francs against the dollar for spot, one-month forward, 3-months forward, and 6-months forward.

Assumptions Values

Beginning your trip with euros 15,000.00

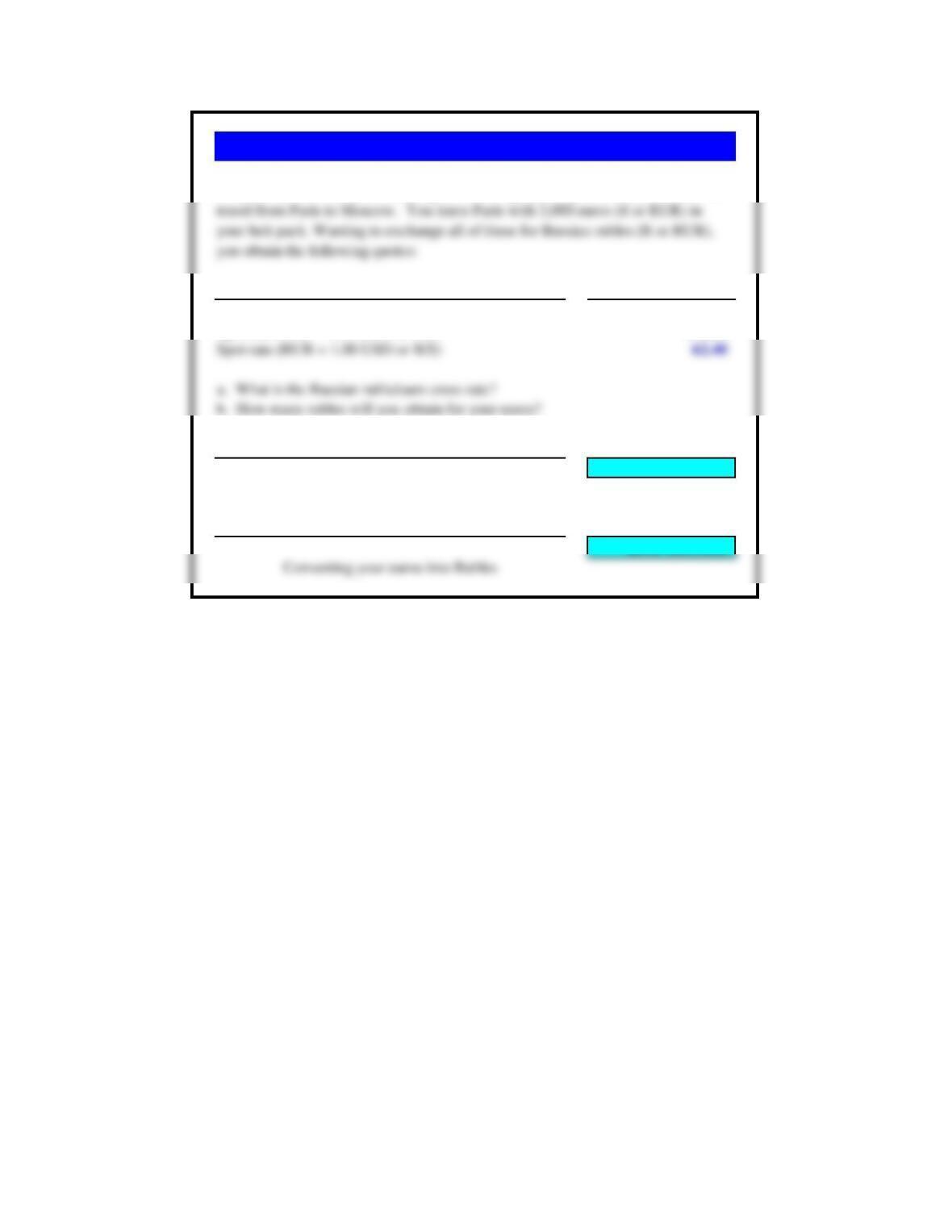

Spot rate (USD = 1.00 EUR or $/€)1.1280

a) What is the Russian ruble/euro cross rate? 70.39

R/ € = R/$ x $/ €

b) How many rubles will you obtain for your euros? RUB 1,055,808

Problem 5.5 Study Abroad: Paris to Moscow

On your summer study abroad program in Europe you stay an extra two weeks to

Assumptions Values

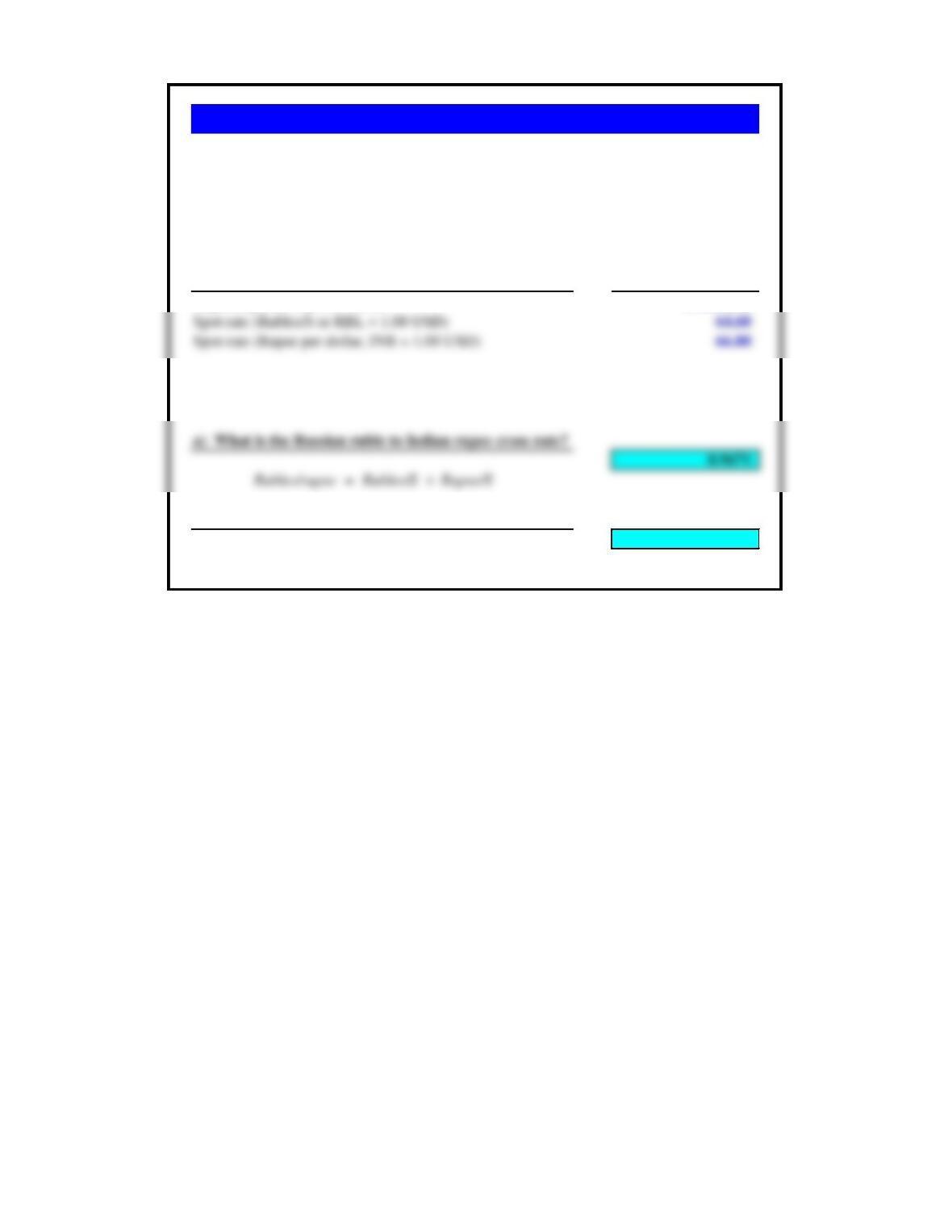

Beginning your trip with rubles 450,000.00

b) How many Indian rupee will you obtain for your rubles? INR 465,325

Converting your Rubles into rupee

Problem 5.6 Summer Abroad: Moscow to Mumbai

a. What is the Russian ruble to Indian rupee cross rate?

b. How many Indian rupee will you obtain for your rubles?

After spending a week in Moscow you get an email from your friend in India. He can get

you a really good deal on a plane ticket and wants you to meet him in Mumbai next week

to continue your global studies. You have 450,000 rubles left in your money pouch. In

preparation for the trip you want to exchange your Russian rubles for Indian rupee at the

Moscow airport:

Part a.

July 1997 November 1997 Percentage

Country Currency (per US$) (per US$ Change vs dollar

China yuan 8.40 8.40 0.0%

Hong Kong dollar 7.75 7.73 0.3%

Indonesia rupiah 2,400 3,600 -33.3%

Korea won 900 1,100 -18.2%

Part b.

Problem 5.7 Asian Pacific Crisis (1997)

The Chinese yuan’s value against the US dollar, as a result of the Chinese government maintaining its

peg to the dollar, did not change at all during the crisis. The Thai baht, however, fell 37.5% in only five

months, with the Indonesian rupiah a close second with a loss of 33.3%.

The Asian financial crisis which began in July 1997 wreaked havoc throughout the currency markets of

East Asia.

a. Which of the following currencies had the largest depreciations or devaluations during the July to

November period?

b. Which seemingly survived the first five months of the crisis with the least impact on their currencies?

Use the table from Bloomberg below to calculate each of the following:

Currency USD EUR JPY GBP CHF CAD AUD HKD

HKD 7.8402 8.6854 0.0721 10.0497 7.8773 5.9987 5.3455

AUD 1.4669 1.6251 0.0135 1.88 1.4736 1.1222 0.1871

CAD 1.307 1.4479 0.012 1.6753 1.3132 0.8911 0.1667

Quote Calculated

a. Japanese yen per US dollar? 108.75

b. U.S. dollars per Japanese yen? 0.0092 0.0092

c. U.S. dollars per euro? 1.1078

d. Euros per U.S. dollar? 0.9027 0.9027

e. Japanese yen per euro? 120.4732

f. Euros per Japanese yen? 0.0083 0.0083

g. Canadian dollars per U.S. dollar? 1.307

Problem 5.8 Bloomberg Cross Rates

CHF/€CHF/€

Period Bid Rate Ask Rate

spot 1.1027 1.1033

1 month 1.1030 1.1035

Since the exchange rate quotes are direct quotes on the dollar (CHF/€), the proper forward premium calculation is:

Forward premium = ( Forward – Spot ) / (Spot) x (360 / days)

a) b)

CHF/€CHF/€Calculated Forward

Period Days Forward Bid Rate Ask Rate Mid-Rate Premium

spot 1.1027 1.1033 1.10300

1 month 30 1.1030 1.1035 1.10325 0.2720%

2 months 60 1.1033 1.1071 1.10520 1.1967%

$/€$/€

Period Bid Rate Ask Rate

spot 1.4389 1.4403

1 month 1.4440 1.4410

2 months 1.4400 1.4415

The 1 month forward rate as the smallest premium, while the 2 month forward possesses the largest premium.

Problem 5.9 Bid/Ask on Swiss Franc/Euro Forwards

Use the following spot and forward bid-ask rates for the Swiss franc/euro (CHF/€) from October 28, 2019, to answer the

following questions:

The forward rates progressively require more and more Swiss francs per euro than the current spot rate. Therefore the Swiss franc

is selling forward at a discount and the euro is selling forward at a premium.

c) Which maturities have the smallest and largest forward premiums?

Mt. Fuji Bank ¥92.00/$

Assumptions Values

Beginning funds in Swiss francs (SF) 12,000,000.00

Try Number 1: Start with SF to $

Step 1: SF to $ 11,764,705.88

Step 2: $ to yen 1,082,352,941.18

Step 3: yen to SF 12,026,143.79

Profit? 26,143.79 A profit.

Try Number 2: Start with SF to yen

Problem 5.10 Swissie Triangular Arbitrage

The following exchange rates are available to you. (You can buy or sell at the stated rates.)

Assume you have an initial SF12,000,000. Can you make a profit via triangular arbitrage?

If so, show the steps and calculate the amount of profit in Swiss francs (Swissies).

US$/A$ US$/A$

Period Bid Rate Ask Rate

spot 0.98510 0.98540

1 month 0.98131 0.98165

a. What is the mid-rate for each maturity?

b. What is the annual forward premium for all maturities?

c. Which maturities have the smallest and largest forward premiums?

Since the exchange rate quotes are direct quotes on the dollar (US$/A$), the proper forward premium calculation is:

Forward premium = ( Forward – Spot ) / (Spot) x (360 / days) a. b.

US$/A$ US$/A$ Calculated Forward

Period Days Forward Bid Rate Ask Rate Mid-Rate Premium

spot 0.98510 0.98540 0.98525

1 month 30 0.98131 0.98165 0.98148 -4.5917%

2 months 60 0.97745 0.97786 0.97766 -4.6252%

The 24 month forward rate has the largest premium, while the 2 month forward possesses the smallest premium.

Problem 5.11 Bid/Ask on Aussie Dollar Forward

Use the following spot and forward bid-ask rates for the U.S. dollar/Australian dollar (US$=A$1.00) exchange rate from

December 10, 2010, to answer the following questions

The forward rates progressively require fewer and fewer US dollars per Australian dollar than the current spot rate. Therefore

the US dollar is selling forward at a premium and the Australian dollar is selling forward at a discount.

c. Which maturities have the smallest and largest forward premiums?

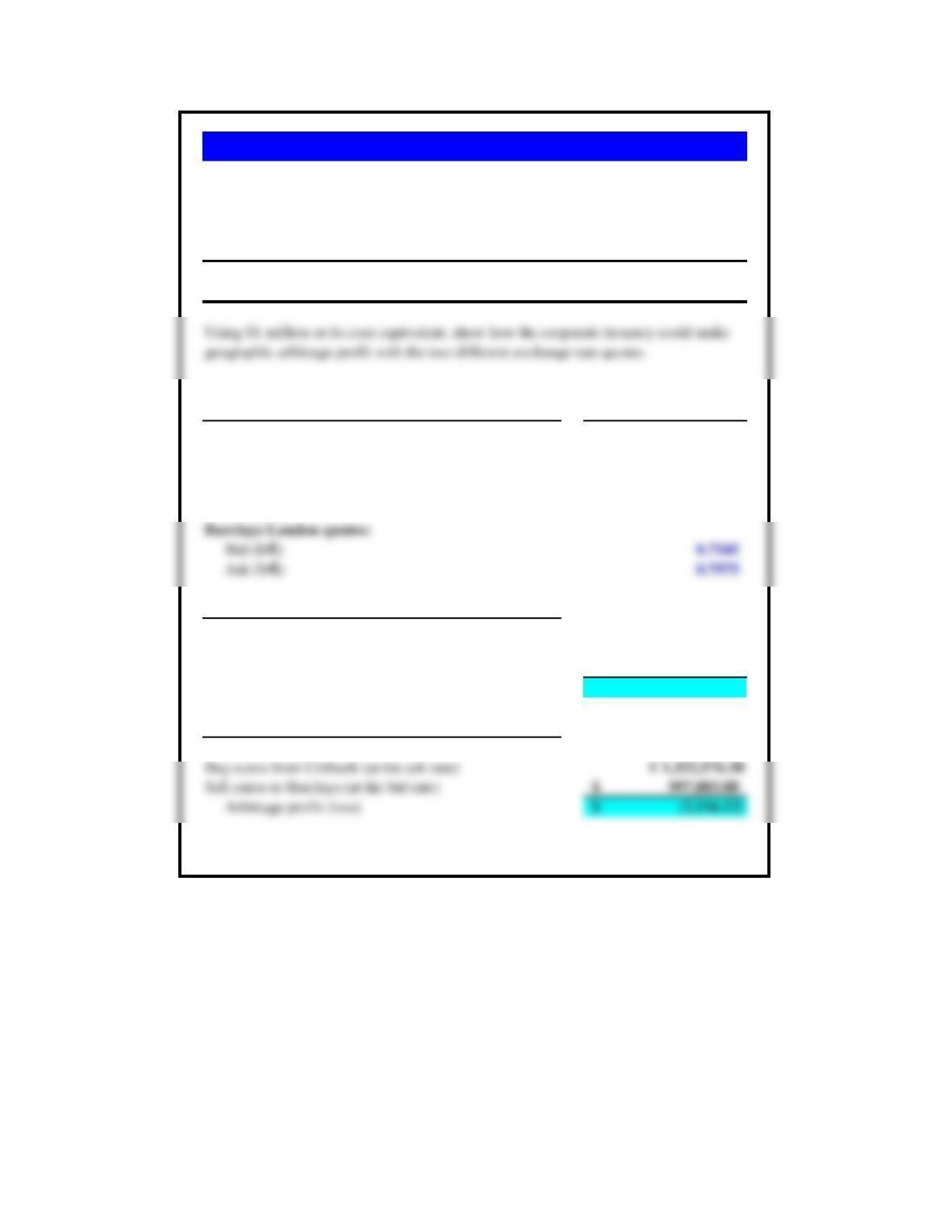

Assumptions Values

Beginning funds 1,000,000.00$

Citibank NYC quotes:

Bid ($/€)0.7551

Ask ($/€)0.7561

Bid ($/€)0.7545

Ask ($/€)0.7575

Arbitrage Strategy #1

Initial investment 1,000,000.00$

Buy euros from Barclays (at the ask rate) € 1,320,132.01

Sell euros to Citibank (at the bid rate) 996,831.68$

Arbitrage profit (loss) (3,168.32)$

Arbitrage Strategy #2

Initial investment 1,000,000.00$

The arbitrager cannot make a profit using these quotes.

Problem 5.12 Vienna Corporate Treasury

Citibank NYC Barclays London

$0.7551-61/€ $0.7545-75/€

A corporate treasury working out of Vienna with operations in New York

simultaneously calls Citibank in New York City and Barclays in London. The two

banks give the following quotes at the same time on the euro:

a. Is this a devaluation or depreciation?

b. By what percentage did its value change?

a. Is this a devaluation or depreciation? Devaluation

then

Depreciation

b. By what percentage did its value change?

Percentage devaluation is: -24.10%

Problem 5.13 Venezuelan Bolivar (A)

The Venezuelan government officially floated the Venezuelan bolivar (Bs) in February of 2002.

Within weeks, its value had moved from the pre-float fix of BS778/$ to Bs1025/$.

This is a case in which a government has changed its currency from a

governmentally determined fixed rate, to a regime in which the currency

market. As a result of the move, the currency‘s value in this case was a

“depreciation” against the U.S. dollar.

a. What was the percentage change in January?

b. Forecast value for June 2003?

Assumptions Values

a) What was the percentage change in January?

% chg = (S1 – S2)/(S2) -28.21%

b) Forecast value for June 2003?

Problem 5.14 Venezuelan Bolivar (B)

The Venezuelan political and economic crisis deepened in late 2002 and early 2003. On

January 1st, 2003, the bolivar was trading at Bs1400/$. By February 1st, its value had

Quoted 90-day Percent premium

European euro (€ per A$) € 0.6151 € 0.6216

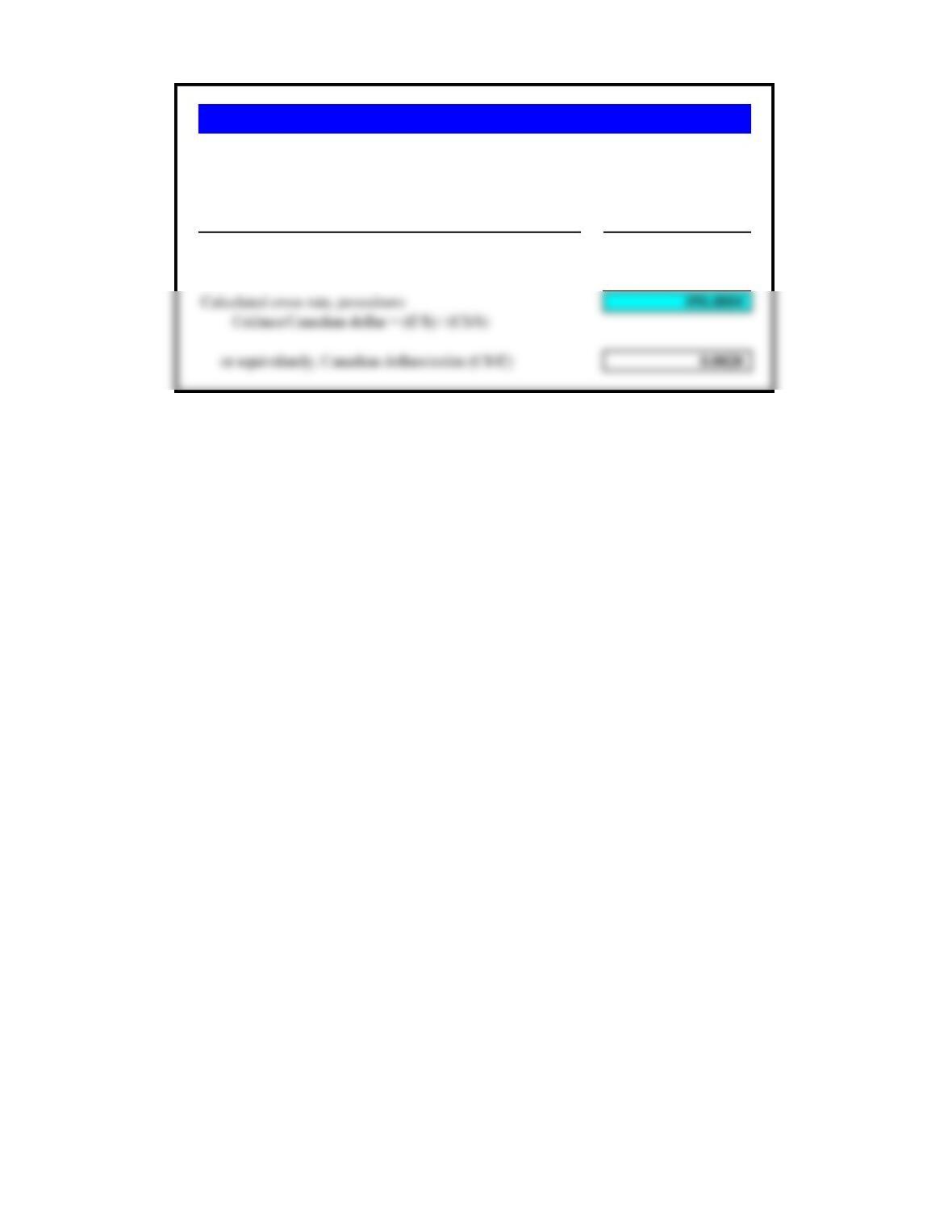

Calculation formula for the indirect quote on the dollar:

Percent premium = (S-F)/(F) x (360/90)

-4.1828%

Check calculation

One way to check percentage change calculations is to invert each of the currency

quotes (1/(€/A$)), and recalculate the quote using the direct quotation formula.

-4.1828%

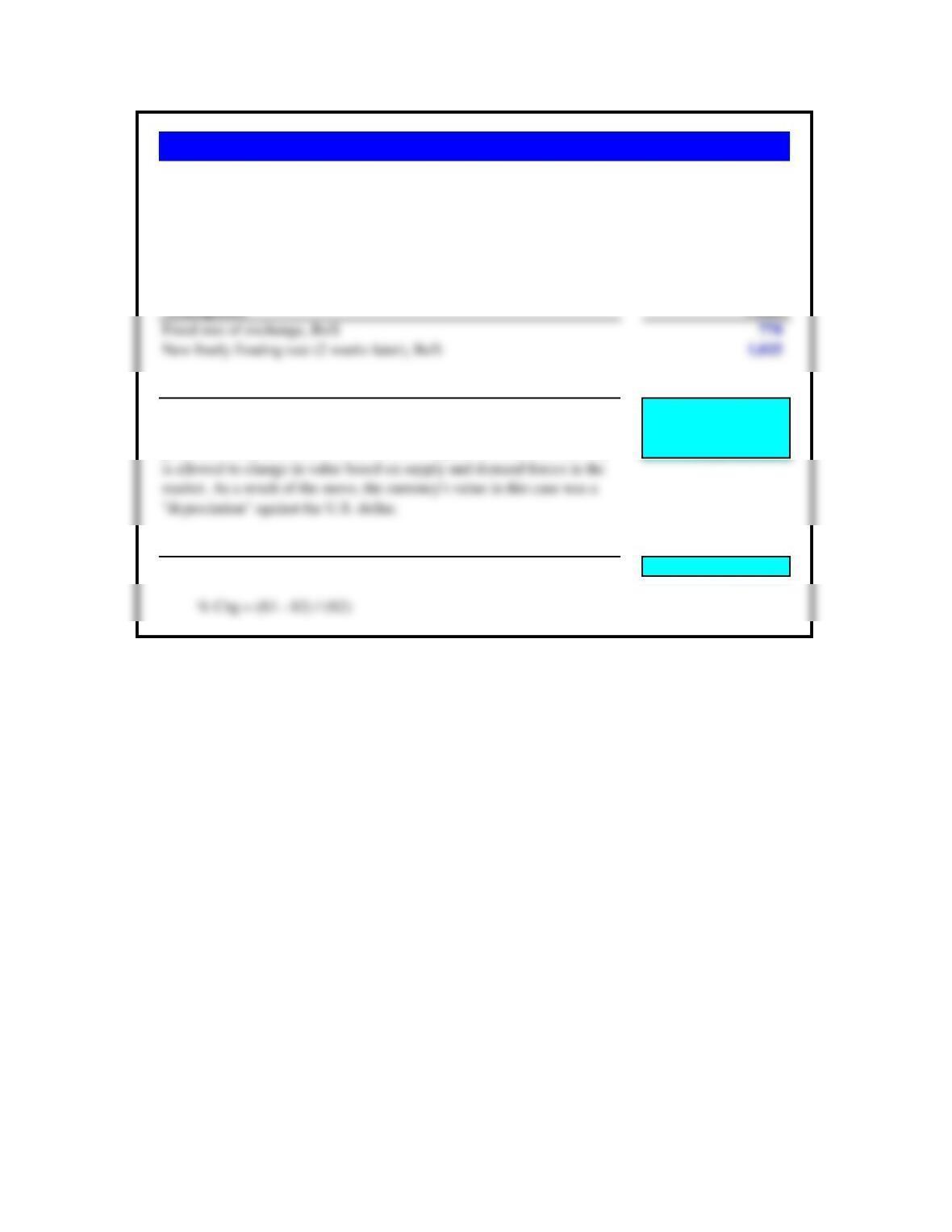

Problem 5.15 Indirect Forward Premium on the Australian dollar

Calculate the forward premium on the Australian dollar (the Australian dollar is the home currency) if the spot rate is

€0.6151/A$ and the 3-month forward rate is €0.6216/A$.

Quoted 180-day Percent premium

Assumptions Spot rate Forward rate or discount

Days forward 180

Exchange rate, US$/£1.5800$ 1.5550$

Inverting the quotes (£/US$) £0.6329 £0.6431

Problem 5.16 Direct Forward Discount on the Dollar

Calculate the forward discount on the dollar (the dollar is the home currency) if the spot rate is spot rate is $1.5800/£ and

the 6-month forward rate is $1.5550/£

The forward rate requires fewer US dollars in exchange for pounds than the current spot rate. The dollar is therefore

selling forward at a premium against the pound (and the pound is simultaneously selling forward at a discount versus the

US dollar).

Assumptions Exchange rate

Mexican peso, pesos/dollar (Ps/$) 12.45

Problem 5.17 Mexican Peso – European Euro Cross Rate

Calculate the cross rate between the Mexican peso (Ps) and the euro (€ ) from the

following two spot rates: Ps12.45/$ and € 0.7550/$.

Assumptions Exchange rate

Costa Rican colón, colónes/dollar (₡/$) 500.29

Canadian dollar, Canadian dollars/dollar (C$/$) 1.0200

Problem 5.18 Pura Vida

Calculate the cross rate between the Costa Rican colón (₡) and the Canadian dollar (C$

) from the following two spot rates: ₡500.29/$ and C$1.02/$.

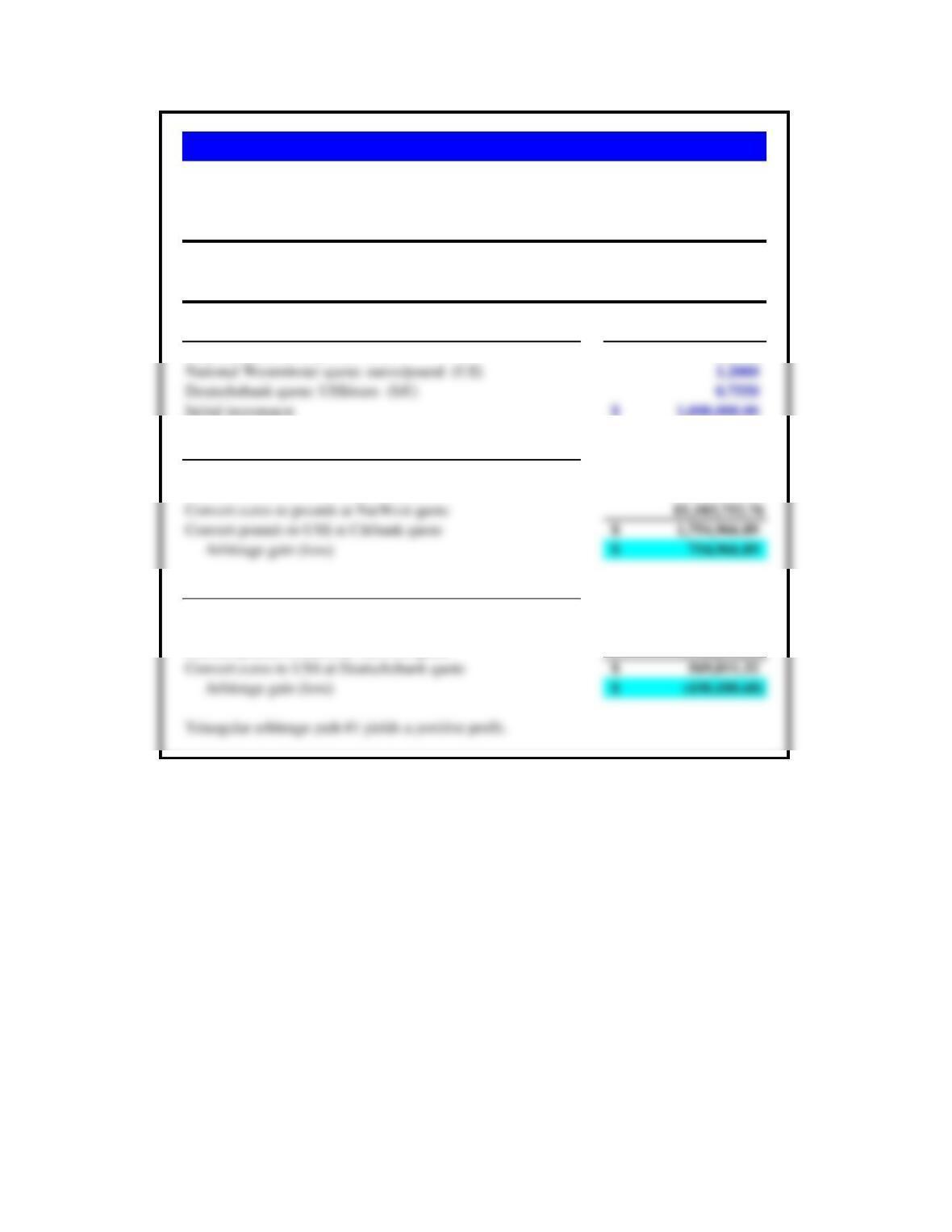

Citibank quotes U.S. dollar per pound: $1.5900/£

National Westminster quotes euros per pound: €1.2000/£

Deutschebank quotes U.S. dollar per euro: $0.7550/€

Assumptions Exchange rate

Citibank quote: US$/pound ($/£) 1.5900

Initial investment 1,000,000.00$

Path #1: US$ to euros to pounds to US$

Start with US$ 1,000,000.00$

Convert to euros at Deutschebank quote € 1,324,503.31

Path #2: US$ to pounds to euros to US$

Start with US$ 1,000,000.00$

Convert to pounds at Citibank quote £628,930.82

Problem 5.19 Around the Horn

Around the horn. Assuming the following quotes, calculate how a market trader at Citibank

with $1,000,000 can make an intermarket arbitrage profit.:

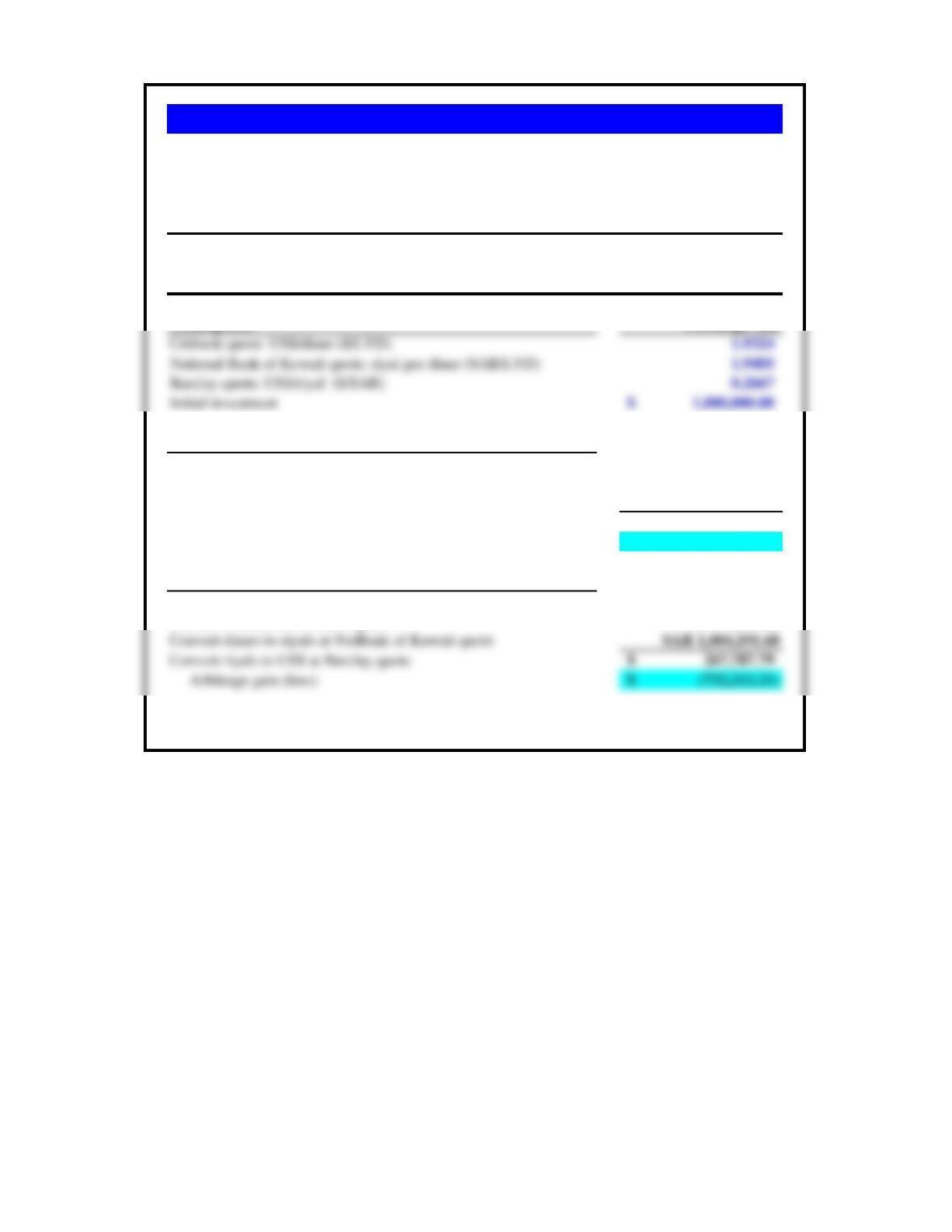

Citibank quotes U.S. dollar per Libyan dinar: USD1.9324 = LYD1.00

National Bank of Kuwait quotes Saudi riyal per Libyan dinar: SAR 1.9405 = LYD1.00

Barclay quotes U.S. dollar per Saudi riyal: USD0.2667 = SAR1.00

Path #1: US$ to riyals to dinars to US$

Start with US$ 1,000,000.00$

Convert to riyals at Barclay quote SAR 3,749,953.13

Convert riyals to dinars at NatBank of Kuwait quote LYD 1,932,467.47

Convert dinars to US$ at Citibank quote 3,734,300.14$

Arbitrage gain (loss) 2,734,300.14$

Path #2: US$ to dinars to riyals to US$

Start with US$ 1,000,000.00$

Convert to dinars at Citibank quote LYD 517,491.20

Triangular arbitrage path #1 yields a positive profit.

Problem 5.20 Great Pyramids

Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he

can make an intermarket arbitrage profit using Libyan dinars and Saudi riyals. He has $1,000,000

to work with so he gathers the following quotes: