Assumptions Value

Share price, P1 HK$318.00

Share price, P2 HK$324.00

Dividend paid, D2 HK$0.00

b. And if the company paid a HK$2.50 dividend:

Assumptions Value

Share price, P1 HK$318.00

Share price, P2 HK$324.00

Dividend paid, D2 HK$2.50

Dividend yield is D2 / P1 0.786%

Capital gain is (P2 – P1) / (P1) 1.887%

Total shareholder return is the sum of the two 2.673%

Problem 4.1 Tencent Holdings Limited

Tencent Holdings Limited is a Chinese multinational conglomerate holding

company. If its share price rises from HK$318 to HK$324 within one year,

what is the rate of return to a shareholder given each of the following:

a. The company paid no dividends.

Share Exchange Rate

Assumptions Price

(US$/€)

Prices when Spencer purchased his shares € 17.25 1.3600

Prices Spencer sees in the market today € 28.33 1.4170

b. What has been the percentage change in the value of euro versus the dollar over this same period?

Percentage change (US$/€) = ( S2 – S1 ) / (S1) 4.19%

c. What would be the total return Spencer would earn on his shares if he sold them at these rates?

If he sold his shares today, it would yield the following amount in euros: € 2,833.00

These euros would in turn be worth the following in US dollars: $4,014.36

The amount he invested in the beginning can be determined by tracing backwards the cost of 100 shares of

Vaniteux at the original price, and then finding what that amount would have been in U.S. dollars.

The rate of return on Spencer’s investment, proceeds divided by initial investment: 71.12%

(Remember to subtract 1, the value of the initial investment, when calculating return.)

Alternatively, the total return which Spencer could earn if he sold his shares now, can be calculated by finding

compound rate of return of the change in the share price and the change in the value of the euro.

Problem 4.2 Spencer Grant and Vaniteux (A)

Spencer Grant is a New York-based investor. He has been closely following his investment in 100 shares of

Vaniteux, a French firm that went public in February of 2010. When he purchased his 100 shares at €17.25 per

share, the euro was trading at $1.360/€. Currently, the share is trading at €28.33 per share, and the dollar has

fallen to $1.4170/€.

a. If Spencer sells his shares today, what percentage change in the share price would he receive?

Share Exchange Rate

Assumptions Price (US$/Euro)

Prices when Spencer purchased his shares 17.25 1.3600

Prices Spencer sees in the market today 31.14 1.3110

c. What would be the total return Spencer would earn on his shares if he sold them at these rates?

If he sold his shares today, it would yield the following amount in euros: 3,114.00

These euros would in turn be worth the following in U.S. dollars: $4,082.45

Percentage return = ( 1 + percent change in share price) x (1 + percent change in spot rate) – 1

Ironically, although the share price has risen considerably more, the fall in the value of the euro has offset that

gain, resulting in nearly the identical same total return as in the previous problem.

Problem 4.3 Spencer Grant and Vaniteux (B)

The amount he invested in the beginning can be determined by tracing backwards the cost of 100 shares of

Vaniteux at the original price, and then finding what that amount would have been in U.S. dollars.

Alternatively, the total return which Spencer could earn if he sold his shares now, can be calculated by finding

compound rate of return of the change in the share price and the change in the value of the euro.

Spencer Grant chooses not to sell his shares at the time described in problem 3. He waits, expecting the share

price to rise further after the announcement of quarterly earnings. His expectations prove correct; the share

price rises to €31.14 per share after the announcement. He now wishes to recalculate his returns. The current

spot exchange rate is $1.3110/€.

Note that the dollar has now actually appreciated versus the euro from Spencer’s initial purchase date. This

results in a negative percentage change in the value of the euro, and therefore a negative percentage change.

Share Exchange Rate

Assumptions Price (US$/Euro)

Prices when Spencer purchased his shares 17.25 1.3600

Prices Spencer sees in the market today 31.14 1.3110

Using the same prices and exchange rates as in problem 4, Vaniteux (B), what would be the total return on the

Vaniteux investment by Laurent Vuagnoux, a Paris-based investor?

Problem 4.4 Vaniteux’s Returns ( C )

Closing If Shareholder Shareholder

Share Dividend Return Return

Date Price Paid (without Div) (with Div)

1998 (January 2) 131.13$

1999 (January 4) 141.00$ 0.16$ 7.53% 7.65%

2000 (January 3) 116.56$ 0.16$ -17.33% -17.22%

In January 2003, Microsoft announced that it would begin paying a dividend of $0.16 per share. Given the following share prices

for Microsoft stock in the recent past, how would a constant dividend of $0.16 per share per year have changed the company’s

average annual return to its shareholders over this period?

Problem 4.5 Microsoft’s Dividend Yield

Problem 4.6 Carty’s Choices

Assumptions Value

Share price, P1 59.00$

Share price, P2 71.00$

Dividend paid, D2 1.75$

Total shareholder return for the period is 23.31%

Brian Carty, a prominent investor, is evaluating investment alternatives. If

Market Total

Number value Market

Company P/E ratio of shares per share Earnings EPS Value

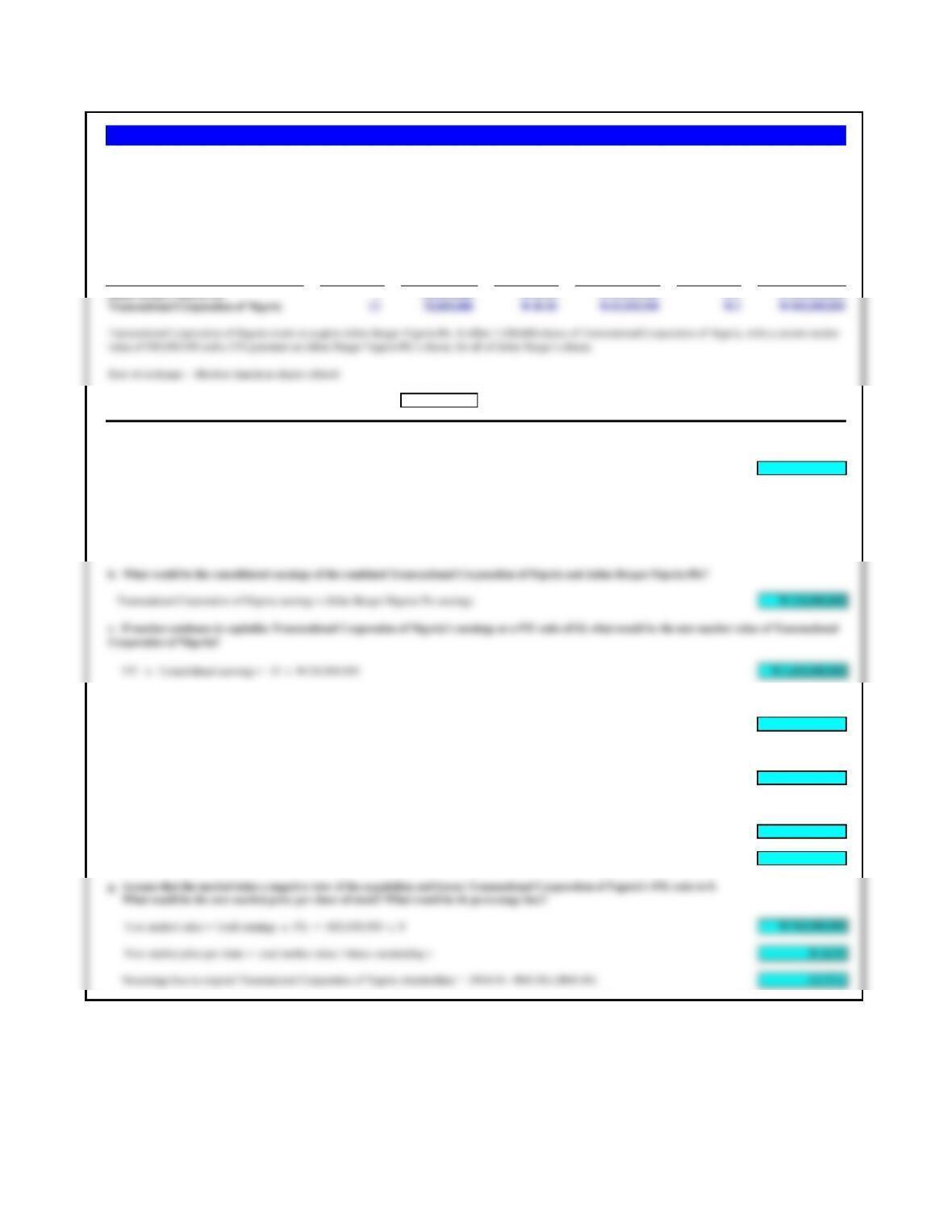

Julius Berger Nigeria Plc 7 20,000,000 ₦ 20.00 ₦ 60,000,000 ₦ 3 ₦ 400,000,000

Transnational Corporation of Nigeria 13 20,000,000 ₦ 40.00 ₦ 60,000,000 ₦ 3 ₦ 800,000,000

Rate of exchange — Modern American shares offered:

Transnational Corporation of Nigeria wants to acquire Julius Berger Nigeria Plc. It offers 7,500,000 shares of Transnational Corporation of Nigeria, with a current market

7,500,000

a. How many shares would Transnational Corporation of Nigeria have outstanding after the acquisition of Julius Berger?

20,000,000 + 7,500,000 27,500,000

So, Transnational Corporation of Nigeria pays: 20 million divided by 2 x (1 + 12% premium)

b. What would be the consolidated earnings of the combined Transnational Corporation of Nigeria and Julius Berger Nigeria Plc?

Transnational Corporation of Nigeria earnings + Julius Berger Nigeria Plc earnings ₦ 120,000,000

P/E x Consolidated earnings = 13 x ₦120,000,000 ₦ 1,600,000,000

d. What would be the new earnings per share of Transnational Corporation of Nigeria?

₦120,000,000 / 27,500,000 shares ₦ 4.36

e. What would be the new market of a share of Transnational Corporation of Nigeria?

New market value / Total shares outstanding = ₦1,600,000,000 / 27,500,000 ₦ 58.18

f. How much would Transnational Corporation of Nigeria’s stock price increase?

Share price rose from ₦4.36 to ₦58.18. ₦ 18.18

Percentage increase 45.45%

g. Assume that the market takes a negative view of the acquisition and lowers Transnational Corporation of Nigeria’s P/E ratio to 8.

What would be the new market price per share of stock? What would be its percentage loss?

New market value = Total earnings x P/E = ₦20,000,000 x 8 ₦ 960,000,000

New market price per share = total market value / shares outstanding = ₦ 34.91

During the 1960s, many conglomerates were created by firms that were enjoying a high price/earnings ratio (P/E). These firms then used their highly valued stock to

acquire other firms that had lower P/E ratios, usually in unrelated domestic industries. Conglomerates went out of fashion during the 1980s when their P/E ratios

significantly declined, thus making it more difficult to find other firms with lower P/E ratios to acquire.

During the 1990s, the same acquisition strategy was possible for firms located in countries where high P/E ratios were common compared to firms in other countries

where low P/E ratios were common. Consider the two hypothetical firms shown in the following table:

Problem 4.7 Transnational Corporation of Nigeria

Because Julius Berger Nigeria Plc shares are worth ₦20 per share, they are only worth one-half the value per share of Transnational Corporation of Nigeria’s ₦40 per

share. So, on a straight exchange, 1 Transnational Corporation of Nigeria share is worth 2 Julius Berger Nigeria Plc shares. But, Transnational Corporation of Nigeria also

needs to pay a premium for gaining control of Julius Berger Nigeria Plc, so it pays an additional 12% over market.

Problem 4.8 Corporate Governance: Overstating Earnings

Market Total

Number value Market

Company P/E ratio of shares per share Earnings EPS Value

Julius Berger Nigeria Plc 7 20,000,000 ₦ 20.00 ₦ 60,000,000 ₦ 3 ₦ 400,000,000

Transnational Corporation of Nigeria 13 20,000,000 ₦ 20.00 ₦ 30,000,000 ₦ 2 ₦ 400,000,000

If earnings were lowered to ₦30 million from the previously reported ₦60 million, could Transnational Corporation of Nigeria still do the deal?

To do the deal, Transnational Corporation of Nigeria’s shareholders need to be paid their market value plus a 12% premium, or

₦ 448,000,000

A number of firms around the world have had to lower their previously reported earnings due to accounting errors or fraud. Assume that Transnational Corporation of

Nigeria (Problem 4.7) had to lower its earnings to ₦30,000,000 from the previously reported ₦60,000,000. What might be its new market value prior to the

acquisition? Could it still do the acquisition?

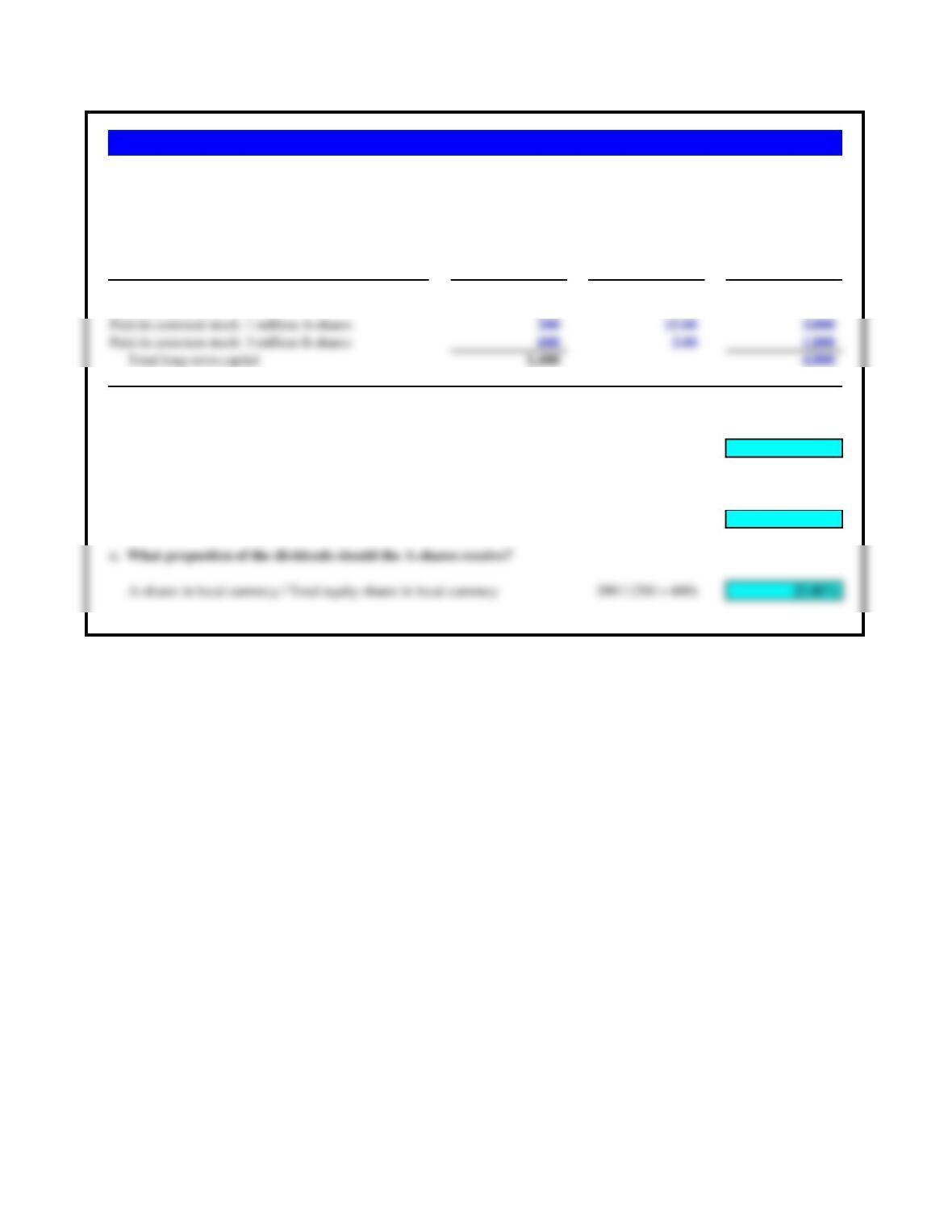

Local Currency

Sasquatch Corporation (millions) Votes per share Total Votes

Long-term debt

250

Retained earnings

350

200 15.00 3,000

600 3.00 1,800

a. What proportion of the total long-term capital has been raised by A-shares?

A-shares / Total long-term capital 200 / 1,400

14.29%

b. What proportion of voting rights is represented by A-shares?

A-share total votes / Total Votes 3,000 / 4,800

62.50%

c. What proportion of the dividends should the A-shares receive?

25.00%

Dual classes of common stock are common in a number of countries. Assume that Sasquatch Corporation has the following

capital structure at book value. The A-shares have 15 votes per share and the B-shares have 3 votes per share.

Problem 4.9 Sasquatch Corporation (A)

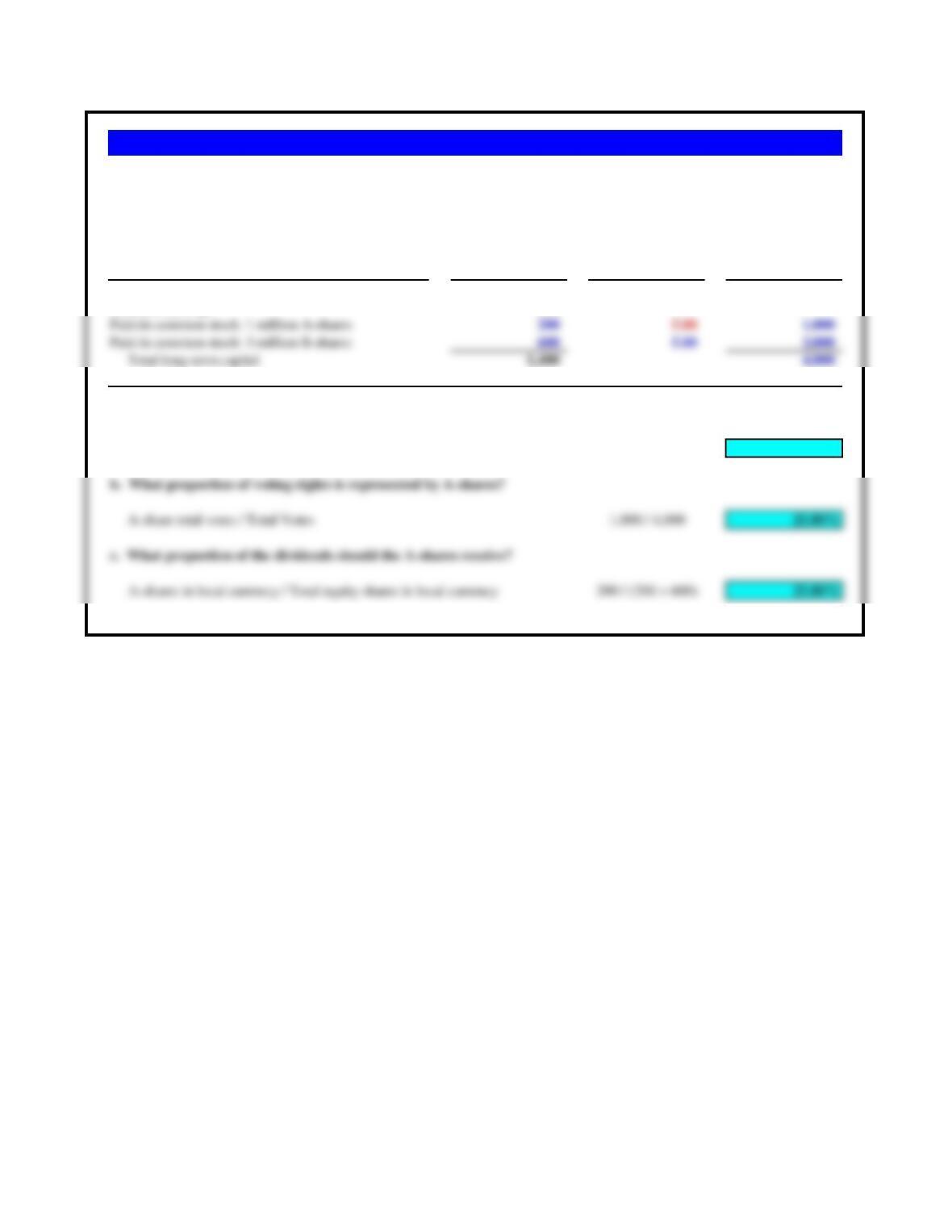

Local Currency

Sasquatch Corporation (millions) Votes per share Total Votes

Long-term debt

250

Retained earnings

350

200 5.00 1,000

600 5.00 3,000

a. What proportion of the total long-term capital has been raised by A-shares?

A-shares / Total long-term capital 200 / 1,400

14.29%

b. What proportion of voting rights is represented by A-shares?

25.00%

c. What proportion of the dividends should the A-shares receive?

25.00%

Assume all the same debt and equity values for Sasquatch Corporation in Problem 4.9, with the sole exception that both A-

shares and B-shares have the same voting rights – 5 votes per share.

Problem 4.10 Sasquatch Corporation (B)

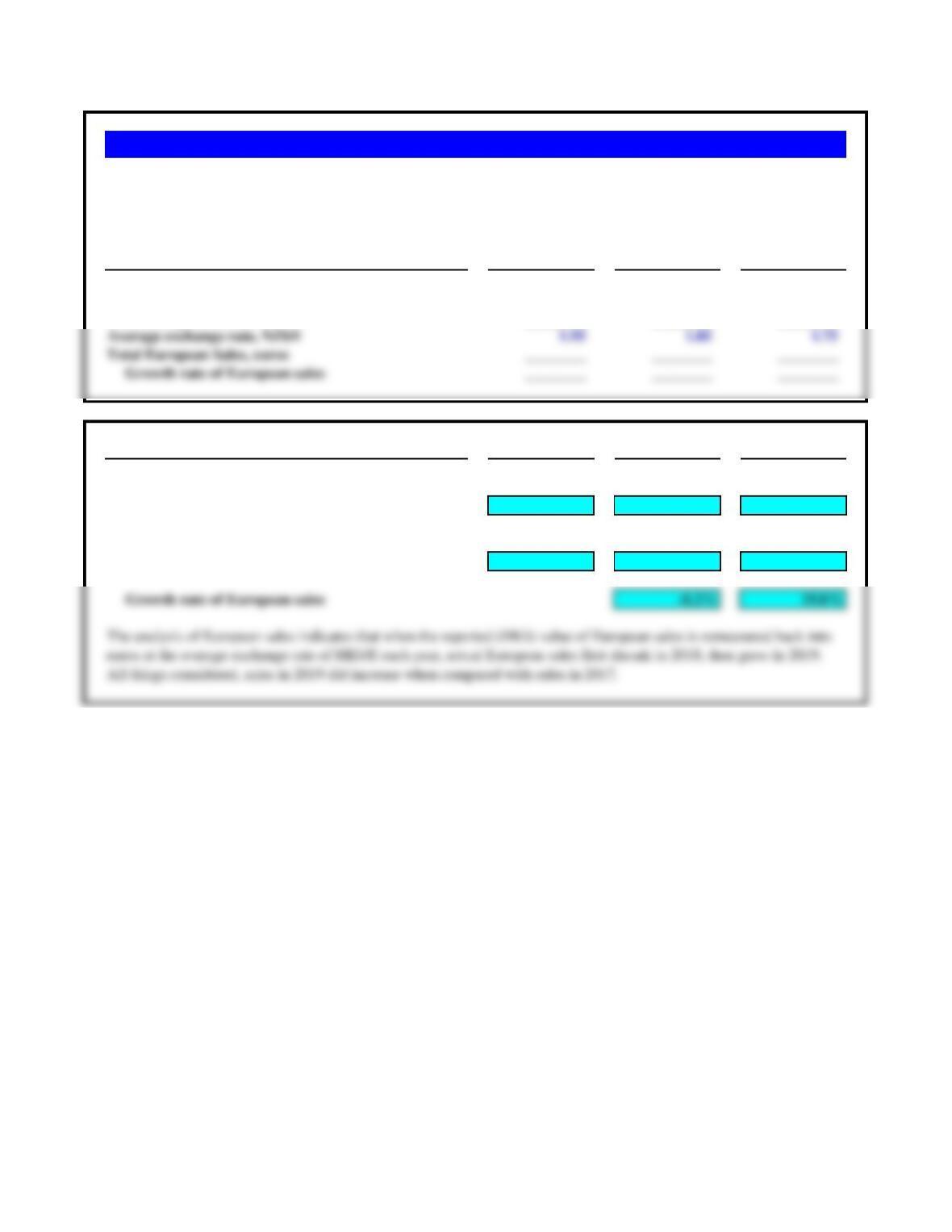

2017 2018 2019

Total net sales, NZ$ 180,900 195,275 250,500

Percent of total sales from Europe 49% 43% 38%

Total European sales, NZ$ ________ ________ ________

Average exchange rate, NZ$/€ 1.95 1.85 1.75

Total European Sales, euros ________ ________ ________

Growth rate of European sales ________ ________ ________

Analysis of European Sales 2017 2018 2019

Total net sales, NZ$ 180,900 195,275 250,500

Percent of total sales from Europe 49% 43% 38%

Total European sales, NZ$ 88,641 83,968 95,190

Average exchange rate, NZ$/€ 1.95 1.85 1.75

Total European Sales, euros (€) € 45,457 € 45,388 € 54,394

Growth rate of European sales -0.2% 19.8%

All things considered, sales in 2019 did increase when compared with sales in 2017.

Problem 4.11 Maori Beer (A): European Sales

Maori Beer is a New Zealand-based brewery and files all of its financial statements in New Zealand dollars (NZ$). The

company’s European sales director Kieran Barrett has been criticized for his performance. He disagrees, arguing that

sales in Europe have grown steadily in recent years. Who is correct?

Analysis of Hong Kong dollar-Denominated Debt 2017 2018 2019

Annual Hong Kong dollar payments on debt agreement (HK$) 90,000,000 90,000,000 90,000,000

Average exchange rate, HK$/NZ$ 5.20 5.10 4.98

Problem 4.12 Maori Beer (B): Hong Kong Dollar Debt

Maori Beer of New Zealand borrowed Hong Kong dollars under a long-term loan agreement several years ago. The company’s

new CFO believes, however, that what was originally thought to have been relatively “cheap debt” is no longer true. What do you

think?

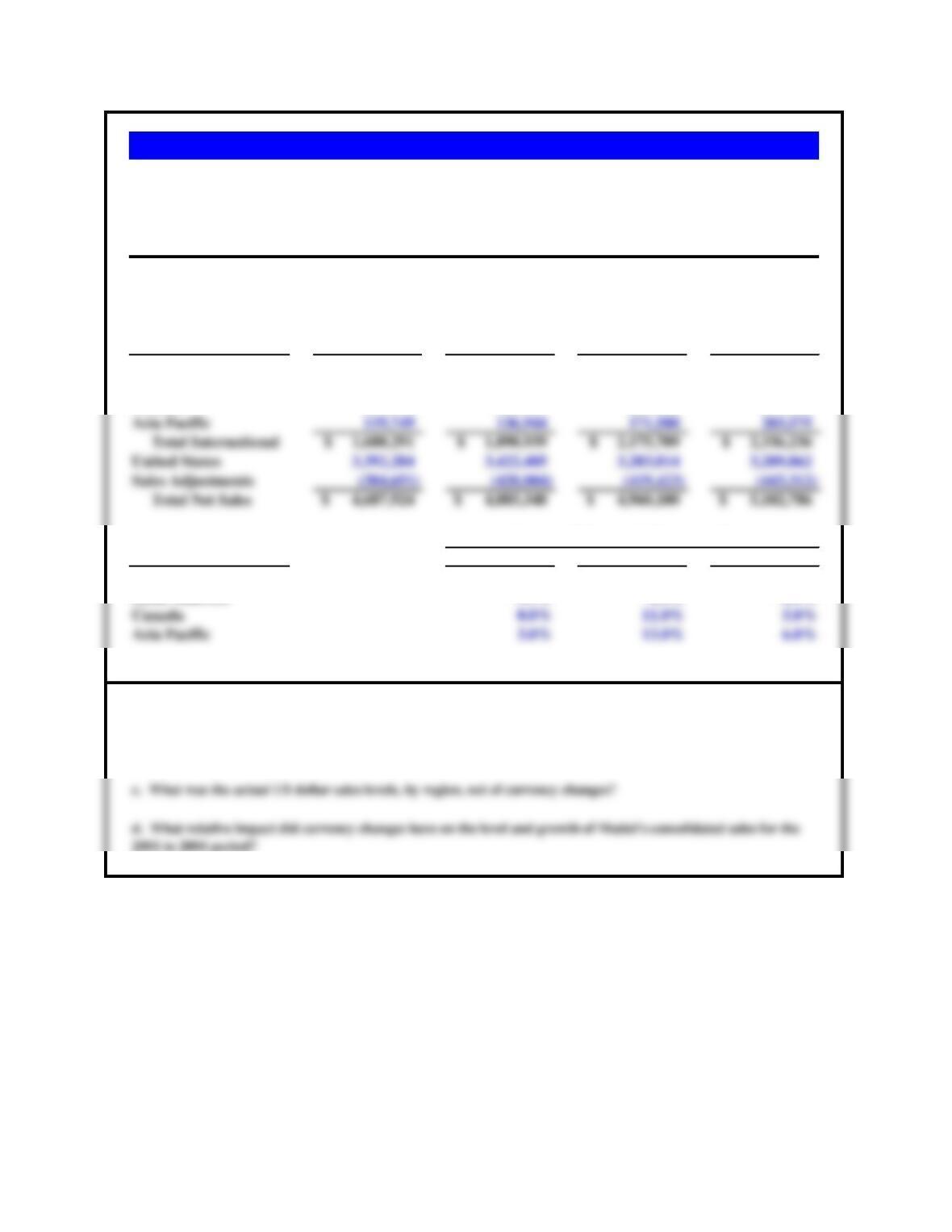

2001 2002 2003 2004

(thousands of US$) Sales ($) Sales ($) Sales ($) Sales ($)

Europe 933,450$ 1,126,177$ 1,356,131$ 1,410,525$

Latin America 471,301 466,349 462,167 524,481

Canada 155,791 161,469 185,831 197,655

Region 2001-2002 2002-2003 2003-2004

Europe 7.0% 15.0% 8.0%

Source: Mattel, Annual Report, 2002, 2003, 2004.

a. What was the percentage change in sales, in US dollars, by region?

b. What was the percentage change in sales by region net of currency change impacts?

Mattel’s Global Sales

Mattel (US) achieved significant sales growth in its major international regions between 2001 and 2004. In its

filings with the United States Security and Exchange Commission (SEC), it reported what percentage change

in regional sales occurred as a result of exchange rate changes.

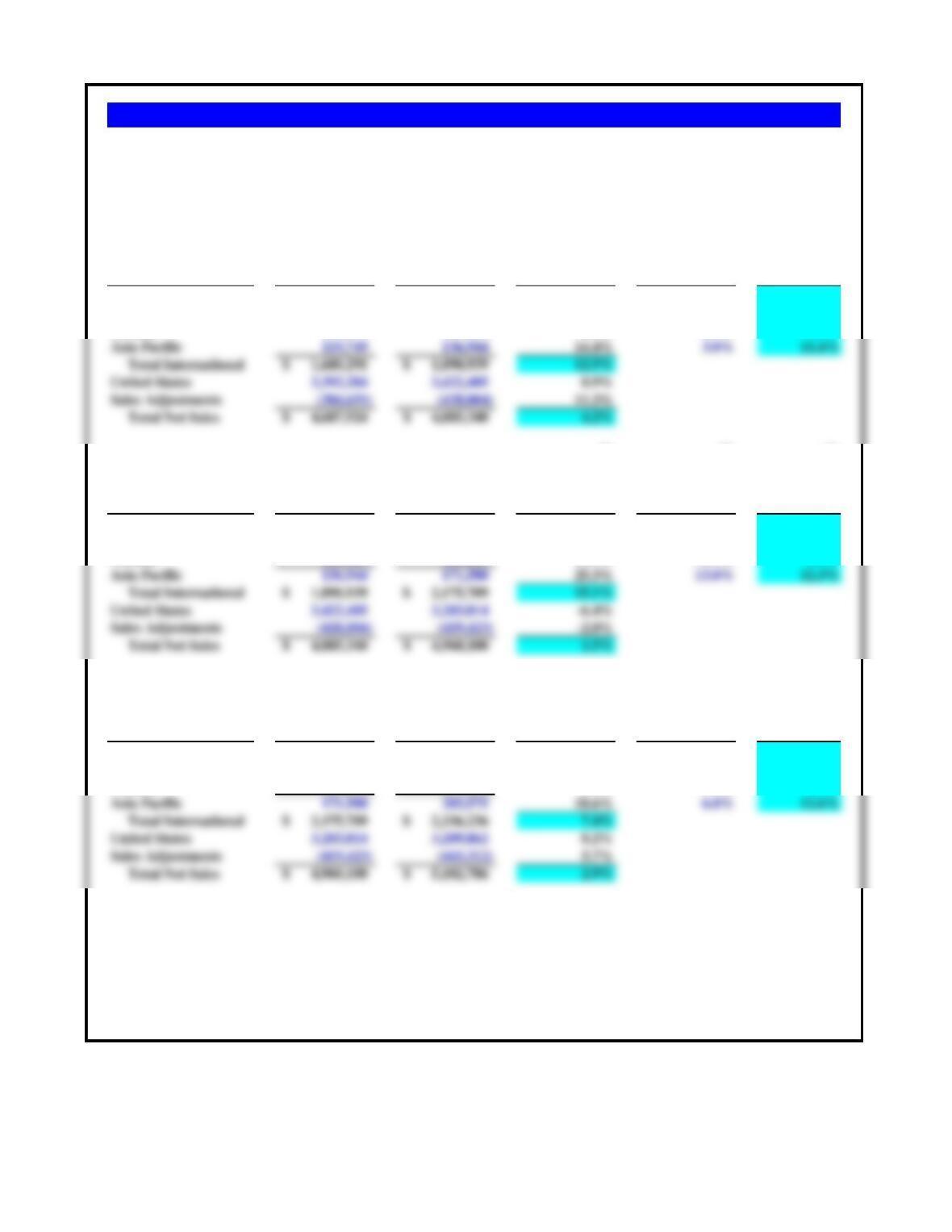

Impact of Change in Currency Rates

Mattel’s Global Sales

Answer to a) Answer to b)

(1) (2) (3)

Percent Impact of Net

2001 2002 Change in Change in Change in

(thousands of US$) Sales ($) Sales ($) Gross Sales Currency Rates Sales

Europe 933,450$ 1,126,177$ 20.6% 7.0% 13.6%

Latin America 471,301 466,349 -1.1% -9.0% 7.9%

Canada 155,791 161,469 3.6% 0.0% 3.6%

(1) (2) (3)

Percent Impact of Net

2002 2003 Change in Change in Change in

(thousands of US$) Sales ($) Sales ($) Gross Sales Currency Rates Sales

Europe 1,126,177$ 1,356,131$ 20.4% 15.0% 5.4%

Latin America 466,349 462,167 -0.9% -6.0% 5.1%

(1) (2) (3)

Percent Impact of Net

2003 2004 Change in Change in Change in

(thousands of US$) Sales ($) Sales ($) Gross Sales Currency Rates Sales

Europe 1,356,131$ 1,410,525$ 4.0% 8.0% -4.0%

Latin America 462,167 524,481 13.5% -2.0% 15.5%

Canada 185,831 197,655 6.4% 5.0% 1.4%

Answer to c)

Mattel (U.S.) achieved significant sales growth in its major international regions between 2001 and 2004. In its filings with the

United States Security and Exchange Commission (SEC), it reported what percentage change in regional sales occurred as a

result of exchange rate changes.

Note: The “net change in sales” by global region is determined by netting the change in currency rates from the calcualted

percent change in gross sales. Column (3) = Column (1) + Column (2).

Over the 2001 to 2004 period, Mattel benefited greatly from the change in exchange rates. Only in the case of Latin America,

where exchange rate changes were actually negative in impact on sales levels for the entire period, did the exchange rate

changes not positively impact regional sales.

Problem 4.13 Mattel’s Global Sales Performance

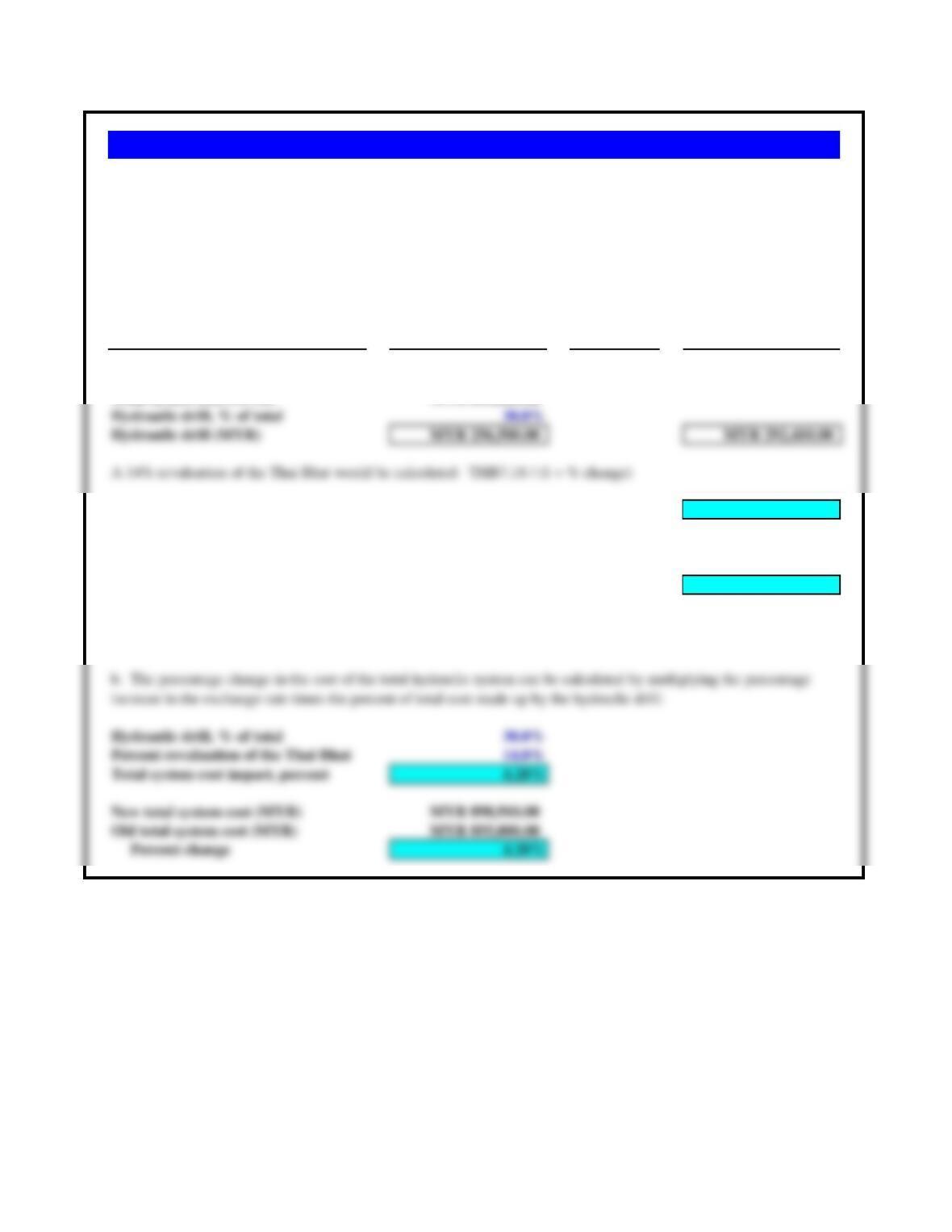

Assumptions Original/Current Revaluation? Future?

Total system cost (MYR) MYR 900,000.00

Cost savings from six sigma/lean 5.0%

Total system cost (MYR) MYR 855,000.00

Hydraulic drill, % of total 30.0%

Hydraulic drill (MYR) MYR 256,500.00 MYR 292,410.00

Exchange rate (THB/MYR) 7.18 14.0% 6.30

Hydraulic tubing (Thai Bhat) 1,841,670.00 1,841,670.00

Cost increase as a result of revaluation MYR 35,910.00

Total system cost after revaluation MYR 890,910.00

Hydraulic drill, % of total 30.0%

Percent revaluation of the Thai Bhat 14.0%

Total system cost impact, percent 4.20%

New total system cost (MYR) MYR 890,910.00

Old total system cost (MYR) MYR 855,000.00

Percent change 4.20%

Idris Hydraulics of Kuala Lumpur, Malaysia, purchases all of its hydraulic drills from manufacturers in Thailand. The

company has recently completed a corporatewide initiative in six sigma/lean manufacturing. Completed oil field

hydraulic system costs were reduced 5% over a one-year period from RM900,000 to RM855,000. The company is

now worried that all of the hydraulic drills that goes into the systems (making up 30% of their total costs) will be hit

by an increasingly stronger Thai baht due to the robust Thai economy. If the current exchange rate is THB7.18/MYR,

how would a 14% revaluation of the Thai baht against the Malaysian ringgit impact total systems costs?

a. The revaluation of the Thai Bhat by 14% would completely nullify all of the cost reduction benefits achieved via

the six sigma/lean manufacturing initiatives recently completed.

Problem 4.14 Idris Hydraulics and the Thai Baht

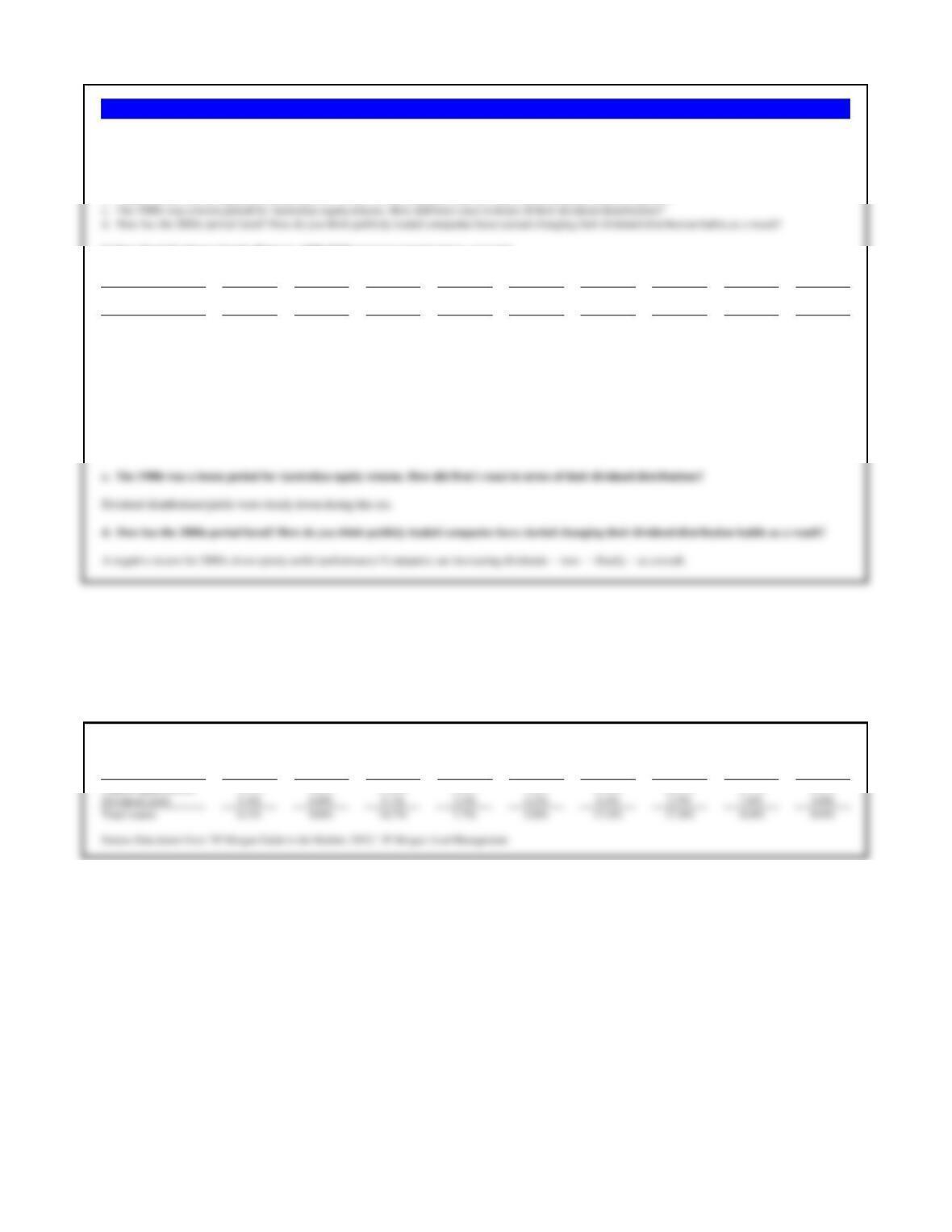

a. Which period shown had the highest total returns? The lowest?

Sydney Stock Exchange Equity Returns, 1930-2019 (average annual return, percent)

1930 to

Period 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s 2019

Capital appreciation -9.2% 8.0% 8.4% 7.2% 5.0% 20.3% 15.3% -5.5% 5.7%

Dividend yield 5.1% 3.0% 2.5% 2.0% 2.2% 2.0% 1.5% 1.7% 3.5%

Total return -4.1% 11.0% 10.9% 9.2% 7.2% 22.3% 16.8% -3.8% 9.2%

a. Which period shown had the highest total returns? The lowest?

The 1980s — had the highest total returns. The lowest were the 1930s.

b. Which decade had the highest dividend returns? When were dividends clearly not a priority for publicly traded companies?

Dividend returns were the highest in the 1930s. Since 1980s dividend yields have clearly been a lower priority.

c. The 1980s was a boom period for Australian equity returns. How did firm‘s react in terms of their dividend distributions?

d. How has the 2000s period fared? How do you think publicly traded companies have started changing their dividend distribution habits as a result?

S&P 500 Equity Returns, 1926-2014 (average annual return, percent)

1926 to

Period 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s 2014

Problem 4.15 Sydney Stock Exchange Equity Returns

The Australian equity market has delivered very different returns over the past 90 years. Use the data from the table below, arranged by decade to answer the

following questions about these Australian equity investment returns.