Chapter 22 (11)

Developing Countries:

Growth, Crisis, and Reform

◼ Chapter Organization

Income, Wealth, and Growth in the World Economy

The Gap between Rich and Poor

Has the World Income Gap Narrowed Over Time?

Structural Features of Developing Countries

Developing-Country Borrowing and Debt

The Economics of Financial Inflows to Developing Countries

The Problem of Default

Alternative Forms of Financial Inflow

The Problem of “Original Sin”

The Debt Crisis of the 1980s

Reforms, Capital Inflows, and the Return of Crisis

East Asia: Success and Crisis

The East Asian Economic Miracle

Box: Why Have Developing Countries Accumulated Such High Levels of International Reserves?

Asian Weaknesses

Box: What Did East Asia Do Right?

The Asian Financial Crisis

Lessons of Developing-Country Crises

Reforming the World’s Financial “Architecture”

Capital Mobility and the Trilemma of the Exchange Rate Regime

“Prophylactic” Measures

Coping with Crisis

Case Study: China’s Pegged Currency

Understanding Global Capital Flows and the Global Distribution of Income: Is Geography Destiny?

Box: Capital Paradoxes

Summary

142 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Tenth Edition

◼ Chapter Overview

This chapter provides the theoretical and historical background students need to understand the

macroeconomic characteristics of developing countries, the problems these countries face, and some

proposed solutions to these problems. Students should be aware of the general events of the East Asian

financial crisis. The chapter covers the East Asian growth miracle and subsequent financial crisis in depth.

First, though, it introduces general characteristics of developing countries and the economics of their

extensive borrowing on world markets, as well as the inflation experiences, debt crisis, and subsequent

reform in Latin America.

The chapter begins by discussing how the economies of developing countries differ from industrial

economies. The wide differences in per capita income and life expectancy across different classes of all

countries are striking. Some economic theories predict growth convergence, and there is evidence of such

a pattern among industrialized nations, but no clear pattern emerges among developing countries. Some

have grown rapidly, while others have struggled.

There are important structural differences between developing economies and industrial economies.

Governments in developing countries have a pervasive role in the economy, setting many prices and

limiting transactions in a wide variety of markets; this can contribute to higher levels of corruption.

These governments often finance their budget deficits through seigniorage, leading to high and persistent

inflation. The economies of developing countries are typically not well diversified, with a small number

of commodities providing the bulk of exports. These commodities, which may be natural resources or

agricultural products, have extremely variable prices. Finally, economies of developing countries typically

lack developed financial markets and often rely on fixed exchange rates and capital controls.

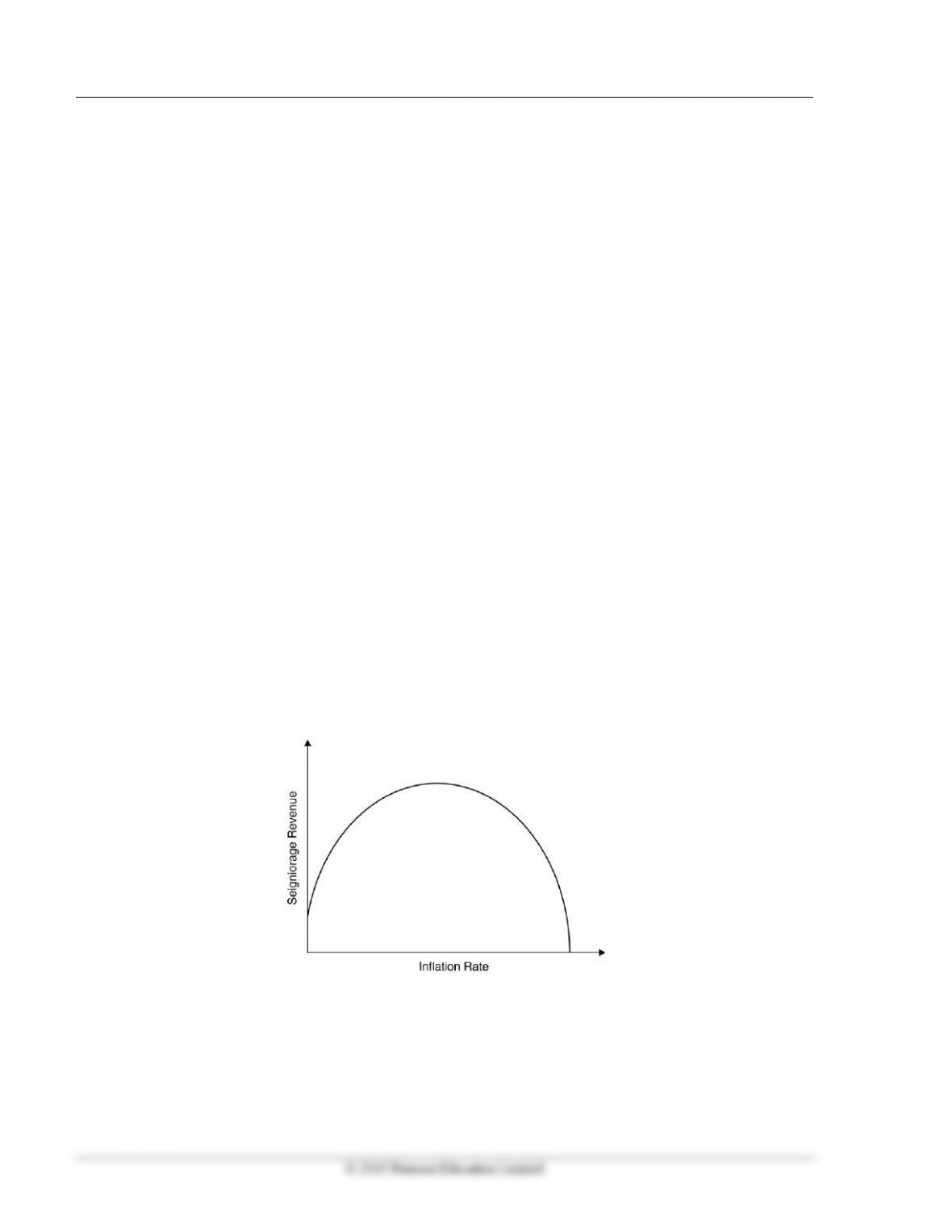

There is a discussion of the use of seigniorage in developing countries in the text. You may want to use the

discussion of seigniorage in the text as a springboard for a more in-depth discussion of this topic. In

particular, you could present a model of where seigniorage revenue is a function of the inflation rate

chosen. The function is concave, at first increasing but eventually decreasing as high inflation leads people

to hold less money (see Figure 22[11]-1 below). It is much like the Laffer curve for taxation. This helps

explain how similar seigniorage revenues may come from widely different inflation levels.

Figure 22(11)-1

In principle, developing countries (and the banks lending to them) should enjoy large gains from

intertemporal trade. Developing countries, with their rich investment opportunities relative to domestic

saving, can build up their capital stocks through borrowing. They can then repay interest and principal

out of the future output the capital generates. Developing-country borrowing can take the form of equity

finance, direct foreign investment, or debt finance, including bond finance, bank loans, and official lending.

These gains from intertemporal trade are threatened by the possibility of default by developing countries.

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform 143

Developing countries have defaulted in many situations over time, from 19th-century American states to

most developing countries in the Depression to the debt crisis in the 1980s. If lenders lose confidence,

they may refuse further lending, forcing developing countries to bring their current account into balance.

These crises are driven by similar self-fulfilling mechanisms as exchange rate crises or bank runs (and are

often referred to as “sudden stops” when financial flows stop running to developing countries seemingly

without warning), and the discussion of debt default provides an opportunity to revisit the ideas of

currency crises and bank runs before a full-fledged discussion of the East Asian crisis.

It is important to recognize the different types of financing available to countries. Bond funding, bank

borrowing, or official lending can all provide debt-oriented funding, while foreign direct investment or

portfolio investment in firms can provide equity financing. In addition, countries can borrow in their own

currency or in another currency. The chapter discusses the problem of “original sin” where many countries

are unable to borrow in their own currency due to both problems in global capital markets and countries’

own histories of poor economic policies.

The next section of the chapter focuses on the experiences of Latin America. In the 1970s, inflation became

a widespread problem in Latin America, and many countries tried using a tablita, or crawling peg. The

strategy, though, did not stop inflation, and large real appreciations were the result. Government-guaranteed

loans were widespread, leading to moral hazard. By the early 1980s, collapsing commodity prices, a rising

dollar, and high U.S. interest rates precipitated default in Mexico followed by other developing countries.

After the debt crisis stretched through most of the decade and slowed developing country growth in many

regions, debt renegotiations finally loosened burdens on many countries by the early 1990s.

After the debt crisis appeared to be ending, capital began to flow back into many developing countries.

These countries were finally undertaking serious economic reform to stabilize their economy. The chapter

details these efforts in Argentina, Brazil, Chile, and Mexico and also discusses how crisis unfortunately

returned to some of these countries.

A case study box on international reserves and China addresses two connected issues that are often

controversial politically: the mass accumulation of international reserves (largely in the form of U.S.

Treasury Bills) by developing countries and the attempt by China to limit the appreciation of its currency.

The box points out that much of the reserves accumulation is connected to insuring against shifts in financial

flows (such as sudden stops of external financing) more than trying to insure against excess needs based

on trade flows (as was the case when financial flows were quite small). In addition to self-insurance, though,

some of the reserves accumulation is a by-product of sterilized intervention. The clearest example of this is

China. China has tried to limit appreciation of its currency to encourage export-led growth. This is done in

part with capital controls, but also through purchasing dollars and selling yuan to prop up the value of the

dollar. As we know from the II–XX model in Chapter 19 (8), at some point, China will likely need to

appreciate or experience inflation. Since 2005, China’s currency has gradually appreciated, gaining about

13 percent in value by January 2008. China repegged its currency in the midst of the 2008 financial crisis,

but then announced in June 2010 (partially in response to foreign pressure) that it would adopt a “managed

float” for its currency. Since that announcement, the yuan has appreciated by another 10 percent. The

experiences outlined in this chapter emphasize the policy trilemma discussed in Chapter 19 (8) and led to

calls for reform of the world’s financial architecture. The chapter next considers some of these, from

144 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Tenth Edition

preventative measures to reduce the risk of crises to measures that improve the way crises are handled (such

as reforming the IMF).

Finally, the chapter concludes with a section on current debates in the growth literature, chiefly a discussion

of the relative importance of geography and institutions in driving income growth and levels. These factors

are crucial to understanding the “Lucas puzzle” of why capital does not appear to be flowing to developing

countries despite their low levels of capital, suggesting a high return in these countries. Rather, it appears

that capital is flowing from the developing world to rich countries! Possible explanations for this puzzle

include lower levels of human capital in developing countries as well as weaker institutions.

◼ Answers to Textbook Problems

1. The amount of seigniorage governments collect does not grow monotonically with the rate of monetary

expansion. The real revenue from seigniorage equals the money growth rate times the real balances

held by the public. But higher monetary growth leads to higher expected future inflation and (through

the Fisher effect) to higher nominal interest rates. To the extent that higher monetary growth raises

the nominal interest rate and reduces the real balances people are willing to hold, it leads to a fall in

2. As discussed in the answer to Problem 1, the real revenue from seigniorage equals the money growth

rate times the real balances held by the public. Higher monetary growth leads to higher expected

future inflation, higher nominal interest rates, and a reduction in the real balances people are willing

to hold. In a year in which inflation is 100 percent and rising, the amount of real balances people are

3. Although Brazil’s inflation rate averaged 147 percent between 1980 and 1985, its seigniorage revenues,

as a percentage of output, were less than half the seigniorage revenues of Sierra Leone, which had an

average inflation rate of 43 percent. Because seigniorage is the product of inflation and real balances

held by the public, the difference in seigniorage revenues reflects lower holdings of real balances in

Brazil than in Sierra Leone. In the face of higher inflation, Brazilians find it more advantageous than

4. If the foreign funding—to reduce the CAD—is stopped, then the government adjusts its savings and

investments to bring the current account balance to zero. The economy either has to increase the

5. Capital flight exacerbates debt problems because the government is left holding a greater external

debt itself but may be unable to identify and tax the people who bought the central bank reserves that

Chapter 22 (11) Developing Countries: Growth, Crisis, and Reform 145

6. An increase in inflation erodes the real value of debt. If the inflation increases in Argentina, then its

real pay towards its loan is less. In other words, the real burden on Argentina is low with high

other words, a high inflation in Argentina would increase the burden of repayment to its debt.

7. When the demand for foreign currency increases this puts pressure on the domestic currency. High

pressure on domestic currency depreciates its real value against the international currency. To protect

8. Cutting investment today will lead to a loss of output tomorrow, so this may be a very shortsighted

strategy. Political expediency, however, makes it easier to cut investment than consumption.

9. If Argentina dollarizes its economy, it will buy dollars from the United States with goods, services, and

assets. This is, in essence, giving the U.S. Federal Reserve assets for green paper to use as domestic

currency. Because Argentina already operates a currency board holding U.S. bonds as its assets,

dollarization would not be as radical as it would be for a country whose central banks hold domestic

assets. Argentina can trade the U.S. bonds it holds for dollars to use as currency. When money

demand increases, the currency board cannot simply print pesos and exchange them for goods and

services; it must sell pesos and buy U.S. government bonds. So, in switching to dollarization, the

government has not surrendered its power to tax its own people through seigniorage; it already does

not have that power.

10. No. Looking simply at countries that are currently industrialized and finding convergence is not a

valid way to test convergence. Countries that are currently well off may have started from a variety

of circumstances, but by only choosing countries that are currently wealthy, we are forcing a finding

11. The moral hazard comes from the fact that borrowers may borrow in a foreign currency, assuming the

government will keep its promise to hold the exchange rate constant. Rather than hedging against the

risk of exchange rate volatility, these borrowers assume the government will prevent the risk from

146 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Tenth Edition

13. The production function in both countries is given by Y = AKαL1-α. We can convert this into a per

worker production function by dividing both sides by L. Y/L = AKαL–α = A(K/L)α. For ease of notation,

let lowercase letters denote per worker values so that y = Akα.

Given these numbers, what value for A (multifactor productivity) would set the two countries

marginal products of capital equal to one another? We can find this by looking at the MPK function:

MPK = αAKα – 1L1 – α = αAkα – 1

We can show that k = (y/A)1/α. Plugging into the expression above gives yInd/yUS =

[(yInd/AInd)/(yUS/AUS)]1/α. Solving for AInd/AUS yields: