Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

9 (20) Exchange Rate Crises: How Pegs Work and How They Break

1. Discovering Data From Figure 2-4(13-4) in Chapter 2(13), identify three countries

with fixed exchange rates. Now use the Internet to search for and visit the websites of

each of these countries’ central banks and download the latest balance sheet

information. For each of the three central banks, answer the following questions.

Answer: Answers will depend on the countries chosen as well as the years. Here we use

a. What is the size of the central bank’s balance sheet in local currency (i.e., total

assets or total liabilities)?

Country

Size of Balance Sheet

Denmark

DKr 2,252,579

Venezuela

VEF 15,169,233

Hong Kong

HK$20,654,286

b. On the liability side, what is the base money supply in local currency issued by

the central bank (call it Mbase)?

Country

M

base

Denmark

DKr 1,730,023

Venezuela

VEF 12,316,553

Hong Kong

HK$2,213,970

c. On the asset side, what is the quantity of foreign exchange reserves in local

currency held by the central bank (call it R)?

Country

R

Denmark

DKr 454,565

Venezuela

VEF 106,336 ($1 = VEF 10.2)

Hong Kong

HK$2,908,876 ($1 = HK$7.69)

d. What is the central bank’s backing ratio (R/Mbase)?

Finally, given the balance sheet positions and backing ratios of these central banks,

discuss their ability to defend their pegs.

Answer: The backing ratios are listed below. It is clear that Hong Kong, which runs a

currency board, has sufficient foreign reserves to back its currency in nearly any

Country

R/M

base

Denmark

26.28%

Venezuela

8.63%

Hong Kong

132%

2. The economic costs of currency crises appear to be larger in emerging markets and

developing countries, than they are in advanced countries. Discuss why this is the

case, making reference to the interaction between the currency crisis and the financial

sector. In what ways do currency crises lead to banking crises in these countries? In

what ways do banking crises spark currency crises?

Answer: Developing countries and emerging markets are less likely to have sound

institutions of macroeconomic policy and financial markets. Also, these countries are

more likely to adopt a fixed exchange rate regime because the benefits are relatively

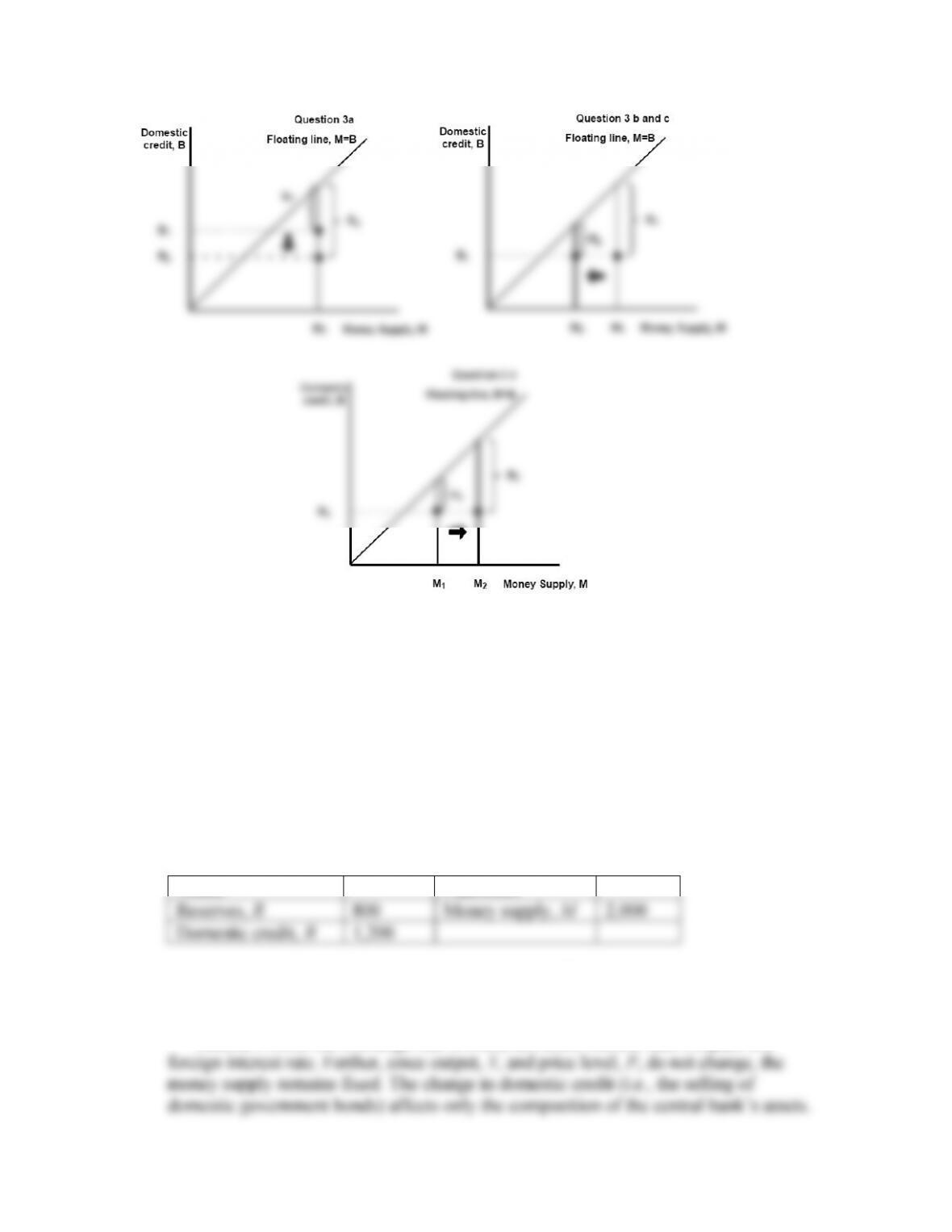

3. Using the central bank balance sheet diagrams, evaluate how each of the following

shocks affects a country’s ability to defend a fixed exchange rate.

In the following answers, we assume the central bank keeps domestic credit

unchanged whenever possible. See the following graphs.

b. Currency traders expect a depreciation in the home currency in the future.

c. An economic contraction leads to a change in home money demand.

Answer: The decrease in money demand will lead to a decrease in interest rates

d. The foreign interest rate falls.

Answer: This increases domestic money demand, so the central bank must

4. Consider the central bank balance sheet for the country of Riqueza. Riqueza currently

has 2,000 million escudos in its money supply, 1,200 million escudos of which is

backed by domestic government bonds; the rest is backed by foreign exchange

reserves. Assume that Riqueza maintains a fixed exchange rate of one escudo per

dollar, the foreign interest rate remains unchanged, and money demand takes the

usual form, M/P = L(i)Y. Assume prices are sticky.

a. Show Riqueza’s central bank balance sheet, assuming there are no private banks.

What is the backing ratio?

Answer: The central bank balance sheet follows. The backing ratio is R/M =

800/2,000 = 40%.

Assets

Liabilities

Reserves, R

800

Money supply, M

2,000

Domestic credit, B

1,200

b. Suppose that Riqueza’s central bank sells 400 million escudos in government

bonds. Show how this affects the central bank balance sheet. Does this change affect

Riqueza’s money supply? Explain why or why not. What is the backing ratio now?

Answer: Since the exchange rate is fixed, domestic interest rate, i, equals the

Reserves increase by the amount of the decrease in domestic credit. The new backing

ratio is 60% (1,200/2,000).

Assets

Liabilities

Reserves, R

1,200

Money supply, M

2,000

Domestic credit, B

800

c. Now, starting from this new position, suppose that there is an economic downturn

in Riqueza, so that real income contracts by 10%. How will this affect money demand

in Riqueza? How will forex traders respond to this change? Explain the responses in

the money market and the forex market.

Answer: Real money demand will decrease by 10%, putting pressure on the

currency to depreciate (decrease in interest rates). Forex traders will respond by

d. Using a new balance sheet, show how the change described in part (c) affects

Riqueza’s central bank. What happens to domestic credit? What happens to Riqueza’s

foreign exchange reserves? Explain the responses in the money market and the forex

market.

Assets

Liabilities

Reserves, R

1,000

Money supply, M

1,800

Domestic credit, B

800

e. How will the change above affect the central bank’s ability to defend the fixed

exchange rate? What is the backing ratio now? Describe how this situation differs

from one in which the central bank buys government bonds, as in part (b).

Answer: The backing ratio is now 55.5% (= 1,000/1,800). The central bank loses

5. What is a currency board? Describe the strict rules about the composition of reserves

and domestic credit that apply to this type of monetary arrangement.

Answer: A currency board forces the central bank to maintain a backing ratio of

100%. The country’s money supply is entirely backed by foreign currency reserves,

6. What is a lender of last resort and what does it do? If a central bank acts as a lender of

last resort under a fixed exchange rate regime, why are reserves at risk?

Answer: A lender of last resort provides credit to banks that are either insolvent or

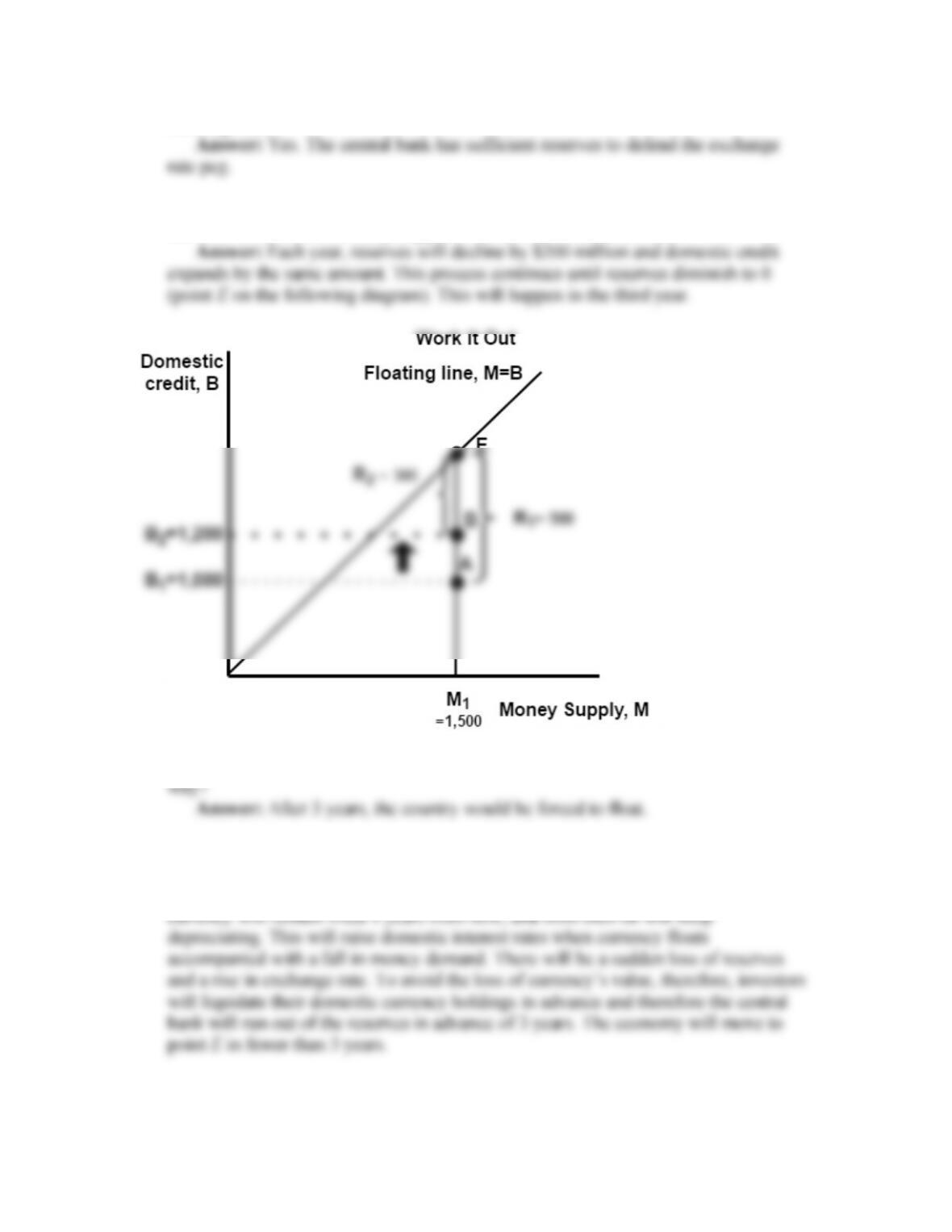

Work It Out

Suppose that a country has a local currency known as the dollar, its money supply is

$1,500 million, and its domestic credit is equal to $1,000 million in the year 2015.

The country maintains a fixed exchange rate, the central bank monetizes any

government budget deficit, and prices are sticky.

a. Compute total reserves for the year 2015 in dollars. Illustrate this situation on a

central bank balance sheet diagram.

b. Now, suppose the government unexpectedly runs a $200 million deficit in the

year 2016 and the money supply is unchanged. Illustrate this change on your diagram.

What is the new level of reserves?

c. If the deficit is unexpected, will the central bank be able to defend the fixed

exchange rate?

d. Suppose the government runs a deficit of $200 million each year from this point

forward. What will eventually happen to the central bank’s reserves?

e. In what year will the central bank be forced to abandon its exchange rate peg and

f. What if the future deficits are anticipated? How does your answer to part (e)

change? Explain briefly.

Answer: If the future deficits are anticipated, then investors know that the

7. Consider two countries with fixed exchange rate regimes. In one country, government

authorities exert fiscal dominance. In the other, they do not. Describe how this affects

the central bank’s ability to defend the exchange rate peg. How might this difference

in fiscal dominance affect the central bank’s credibility?

Answer: If a country has fiscal dominance, the central bank is forced to finance

budget deficits through buying government bonds. This expands domestic credit,

8. The government of the Republic of Andea is currently pegging the Andean peso to

the dollar at E = 1 peso per dollar. Assume the following:

In year 1 the money supply M is 2,700 pesos, reserves R are 1,500 pesos, and

domestic credit B is 1,200 pesos. To finance spending, B is growing at 50% per year.

Inflation is currently zero, prices are flexible, PPP holds at all times, and initially, P =

1. Assume also that the foreign price level is P* = 1, so PPP holds. The government

will float the peso if and only if it runs out of reserves. The U.S. nominal interest rate

is 5%. Real output is fixed at Y = 2,700 at all times. Real money balances are M/P =

2,700 = L(i)Y, and L is initially equal to 1.

a. Assume that Andean investors are myopic and do not foresee the reserves running

out. Calculate domestic credit in years 1, 2, 3, 4, and 5. At each date, also compute

reserves, money supply, and the growth rate of money supply since the previous

period (in percent).

Answer: See the following table.

Time, t

M

B

R

P

Growth Rate of

Money Supply

1

2,700

1,200

1,500

1

0

2

2,700

1,800

900

1

0

3

2,700

2,700

0

1

0

4

4,050

4,050

0

1.5

50%

5

6,075

6,075

0

2.25

50%

b. Continue to assume myopia. When do reserves run out? Call this time T. Assume

inflation is constant after time T. What will that new inflation rate be? What will the

rate of depreciation be? What will the new domestic interest rate be? (Hint: use PPP

and the Fisher effect.)

Answer: Reserves run out at time T = 3. Once this time is reached, the price level

c. Continue to assume myopia. Suppose that at time T, when the home interest rate i

increases, then L(i) drops from 1 to 2/3. Recall that Y remains fixed. What is M/P

before time T? What will be the new level of M/P after time T once reserves have run

out and inflation has started?

Answer: Real money balances before T = 3, M/P = 2,700/1 = 2,700. If money

d. Continue to assume myopia. At time T, what is the price level going to be right

before reserves run out? Right after? What is the percentage increase in the price

level? In the exchange rate? (Hint: Use the answer to part (c) and PPP.)

Answer: Right before reserves run out, P = 1. Then the price level jumps to P =

e. Suppose investors know the rate at which domestic credit is growing. Is the path

described above consistent with rational behavior? What would rational investors

want to do instead?

Answer: This path is not consistent with rational behavior. If investors have

f. Given the data presented in the question so far, when do you think a speculative

attack would occur? At what level of reserves will such an attack occur? Explain your

answer.

Answer: The attack will occur when investors expect currency to float, that is, at

time T = 2. This is exactly when the real money demand is going to drop from 2,700

9. A peg is not credible when investors fear depreciation in the future, despite official

announcements. Why is the home interest rate always higher under a noncredible peg

than under a credible peg? Why does that make it more costly to maintain a

noncredible peg than a credible peg? Explain why nothing more than a shift in

investor beliefs can cause a peg to break.

Answer: The home interest rate is always higher under a noncredible peg because

there is a positive probability that the currency may depreciate, giving rise to an

10. You are the economic advisor to Sir Bufton Tufton, the prime minister of Perfidia.

The Bank of Perfidia is pegging the exchange rate of the local currency, the Perfidian

albion. The albion is pegged to the wotan, which is the currency of the neighboring

country of Wagneria. Until this week both countries have been at full employment.

This morning, new data showed that Perfidia was in a mild recession, 1% below

desired output. Tufton believes a downturn of 1% or less is economically and

politically acceptable but a larger downturn is not. He must face the press in 15

minutes and is considering making one of three statements:

a. “We will abandon the peg to the wotan immediately.”

b. “Our policies will not change unless economic conditions deteriorate further.”

c. “We shall never surrender our peg to the wotan.”

What would you say to Tufton concerning the merits of each statement?

a. By abandoning the peg, the central bank is free to conduct monetary policy to

push the economy closer to full employment, through the expansion of domestic

b. This statement is designed to reassure investors that the peg is credible because

the cost of the output gap is smaller than the benefit of pegging. The benefit of this

c. This statement has a similar effect to the previous one, but it too has pros and

cons. First, this statement is a stronger commitment to the peg, possibly staving off a

11. What steps have been proposed to prevent exchange rate crises? Discuss their pros

and cons.

Answer: The propositions are as follows:

• Impose capital controls to stop the outflow (or restrict the inflow) of foreign

capital to prevent speculative attack. However, capital flows are hard to control, and