Time 4 onward:

Price level continues to grow at the rate of the money supply, and real money

demand remains unchanged at 4,608 billions. See the previous table.

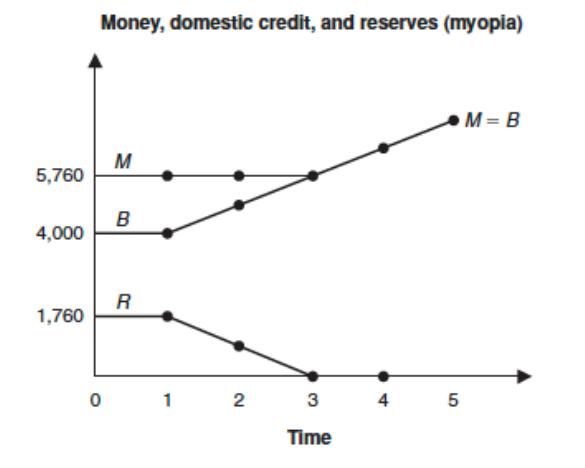

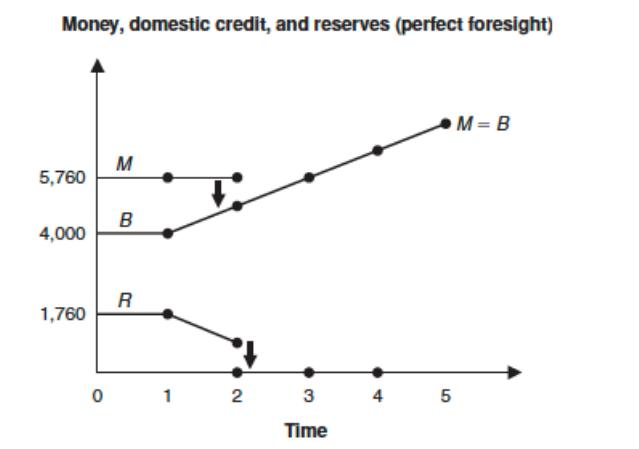

e. Illustrate the behavior of the following variables between t = 1 and t = 5: domestic

credit, reserves, and the money supply.

Answer: See the following diagram.

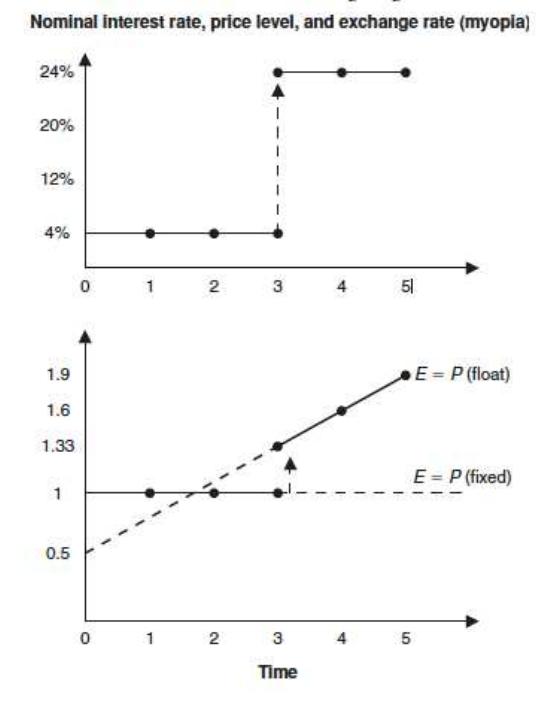

f. Illustrate the behavior of the following variables between t = 1 and t = 5: the

nominal interest rate, the price level, and the exchange rate.

Answer: See the following diagrams.

8. Consider the previous question. In this case, we assume investors are forward-looking

and hear news that the government deficit will grow at 20% each year.

a. How will investors respond to the announcement of the budget deficit? What

happens to reserves as a result?

Answer: Investors will respond to the announcement by selling domestic

b. Calculate the level of critical reserves at which the speculative attack occurs. Is

this central bank holding sufficient reserves to prevent a speculative attack?

According to your calculation, when should the speculative attack occur?

Answer: The critical level of reserves is given by

c. Illustrate the behavior of the following variables between t = 1 and t = 5: domestic

credit, reserves, and the money supply.

Answer: See the following diagrams. Speculative attack occurs at time t = 2

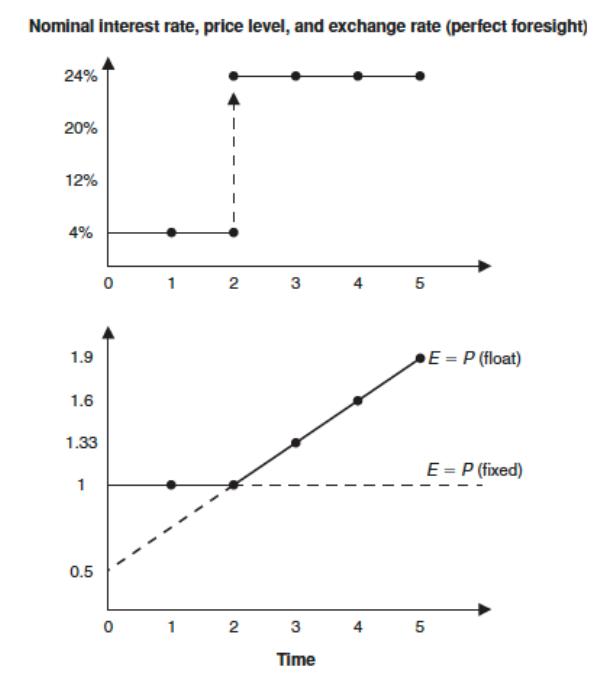

d. Illustrate the behavior of the following variables between t = 1 and t = 5: the

nominal interest rate, the price level, and the exchange rate.

e. Why does the price level “jump” when the country switches from fixed to float in

the myopic case? Why is this not possible in the forward-looking case?

Answer: The price level jump is caused by the unanticipated change in the

9. The textbook examines what happens when governments run persistent budget

deficits in a first-generation model. Suppose that a country begins running large

budget surpluses. In this case, will the country be forced to float? In the forward–

looking model, is a speculative attack possible in this case? Explain.

Answer: No, because budget surpluses contract domestic credit, expanding the

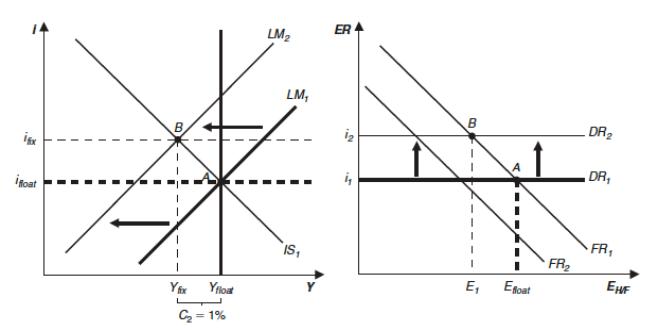

10. Consider a second-generation model of crises. Assume that the benefit of maintaining

an exchange rate peg is equal to 4% (measured in output gap terms). Examine each of

the following cases, assuming the economy experiences a recession. For each case,

illustrate the IS‒LM‒FX model and determine whether the country will (1) peg, (2)

float, or (3) peg or float, depending on the peg’s credibility. On your diagrams,

indicate relevant shifts in the curves.

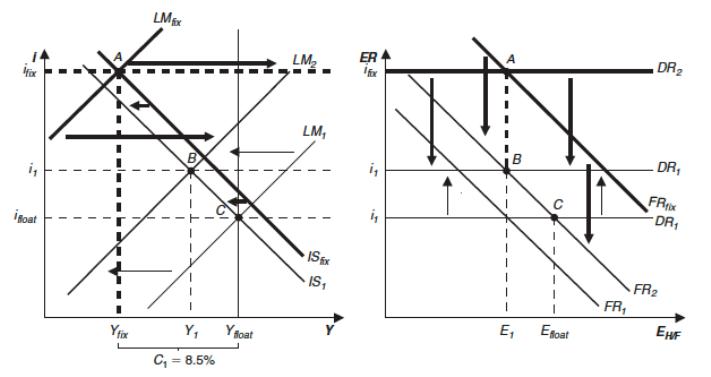

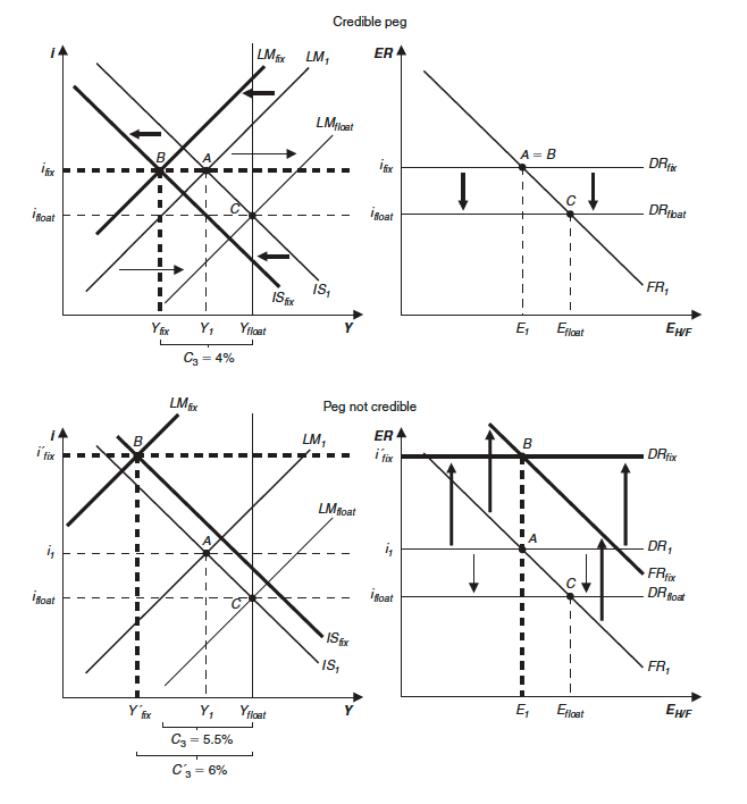

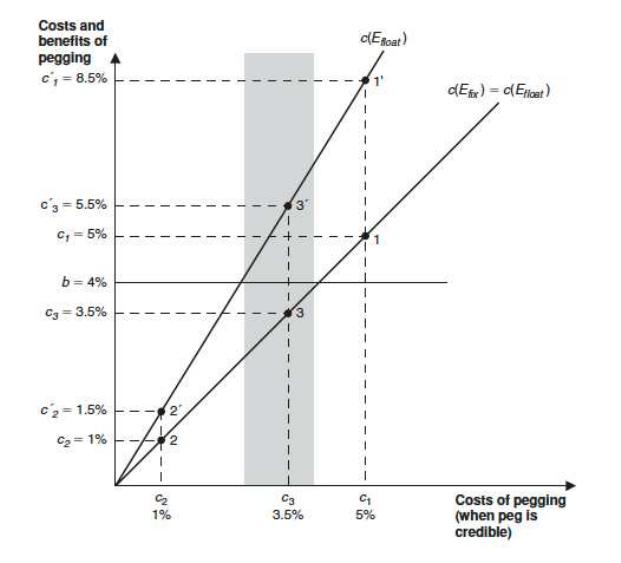

a. Case 1. If the country defends the exchange rate peg, the output gap is equal to

5%. If the peg is not credible, the output gap is equal to 8.5%. Will investors view

the peg as credible in this case? Explain.

Answer: See the following diagrams. No, the peg is not credible. Therefore, there

is a unique equilibrium. Because the cost of defending the peg exceeds the

b. Case 2. If the country defends the exchange rate peg, the output gap is equal to

1%. If the peg is not credible, the output gap is equal to 1.5%. Will investors view

the peg as credible in this case? Explain.

Answer: See the following diagrams. Yes, the peg is credible and there is a

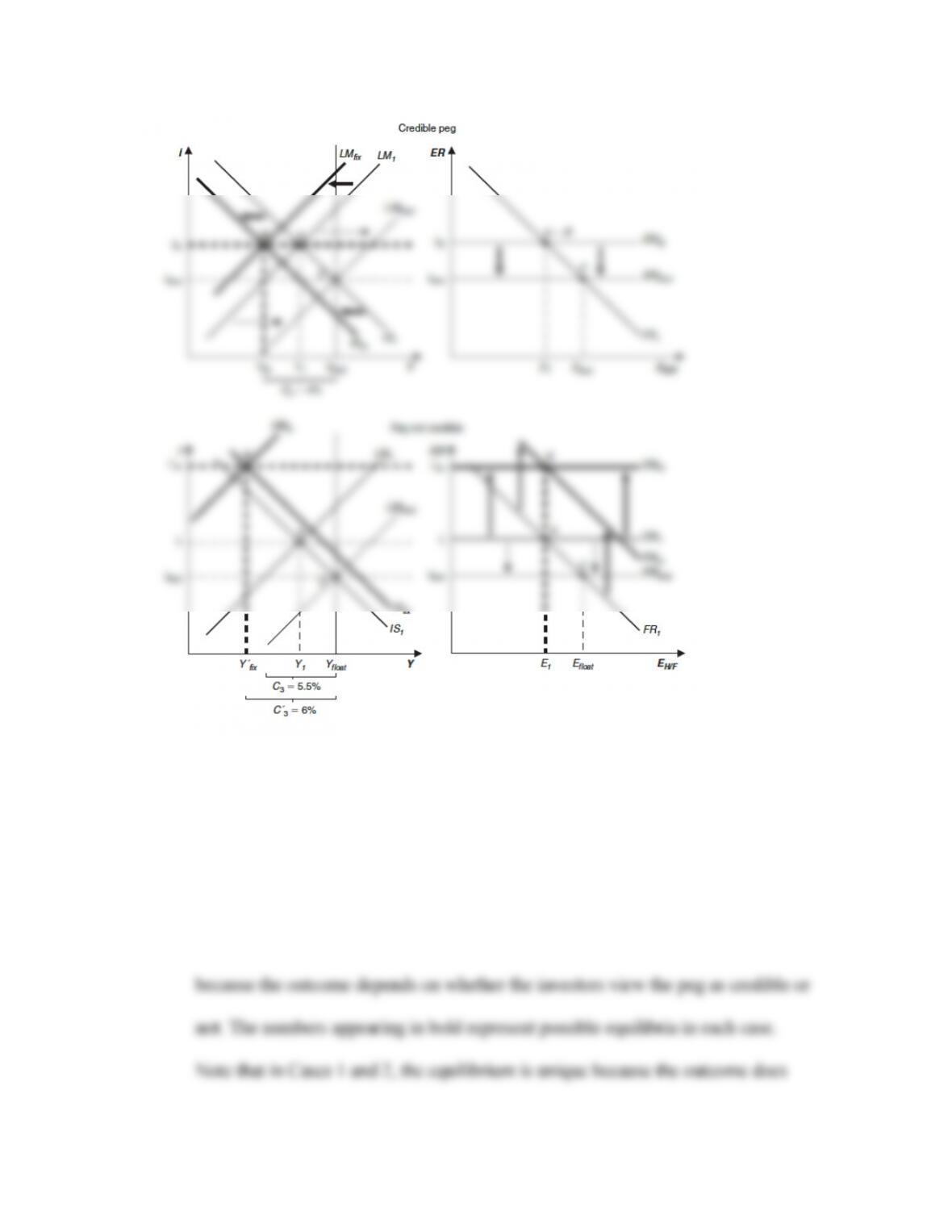

c. Case 3. If the country defends the exchange rate peg, the output gap is equal to

3.5%. If the peg is not credible, the output gap is equal to 5.5%. Will investors

view the peg as credible in this case? Explain.

Answer: See the following diagrams. We are unable to determine whether the

peg is credible or not, giving rise to multiple equilibria. If the peg is credible, the

d. Illustrate the previous three cases using a diagram similar to Figure 20-17 in the

text. In which case do multiple equilibria arise, and why? Why don’t investor

expectations affect outcomes in the other two cases?

Answer: See the following diagram. In Case 3, there are two possible equilibria

11. During the East Asian currency crisis, some countries opted to float their currencies

relative to the U.S. dollar, whereas others did not. Consider two countries: South

Korea and Malaysia. South Korea floated its currency (the won) against the dollar in

the autumn of 1997. Malaysia did not, and still maintains a fixed exchange rate

relative to the U.S. dollar. For simplicity, suppose that these two countries faced

exactly the same costs and benefits of maintaining a credible exchange rate peg. In

this case, is it possible that they both made an optimal decision? Explain.

Answer: Yes, it is possible that they both made an optimal decision. According to the

12. Throughout the chapter, there are applications citing the dramatic accumulation of

reserves among selected emerging markets and developing countries.

a. What are the causes of this reserve accumulation?

Answer: Countries use sterilization bonds to prevent positive money demand

shocks from expanding the money supply. This means a positive money demand

b. What are the costs of reserve accumulation? Why might a country decide to

accumulate reserves, even in the face of relatively large interest rate spreads

between domestic and foreign bonds?

Answer: Sterilization bonds must pay higher interest than the interest received on

c. Explain how reserve accumulation could affect outcomes in a first-generation

model of crises.

Answer: In the first-generation model, countries experience exchange rate crises

because of inconsistent fiscal policies, specifically because of fiscal deficits. The

d. Explain how reserve accumulation could affect outcomes in a second-generation

model of crises.

Answer: In the second-generation model, the costs of maintaining an exchange

rate peg depend on whether or not a peg is credible, giving rise to multiple

equilibria. The actual outcome depends on investors’ expectations about whether