7 (18) Balance of Payments II: Output, Exchange Rates, and Macroeconomic

Policies in the Short Run

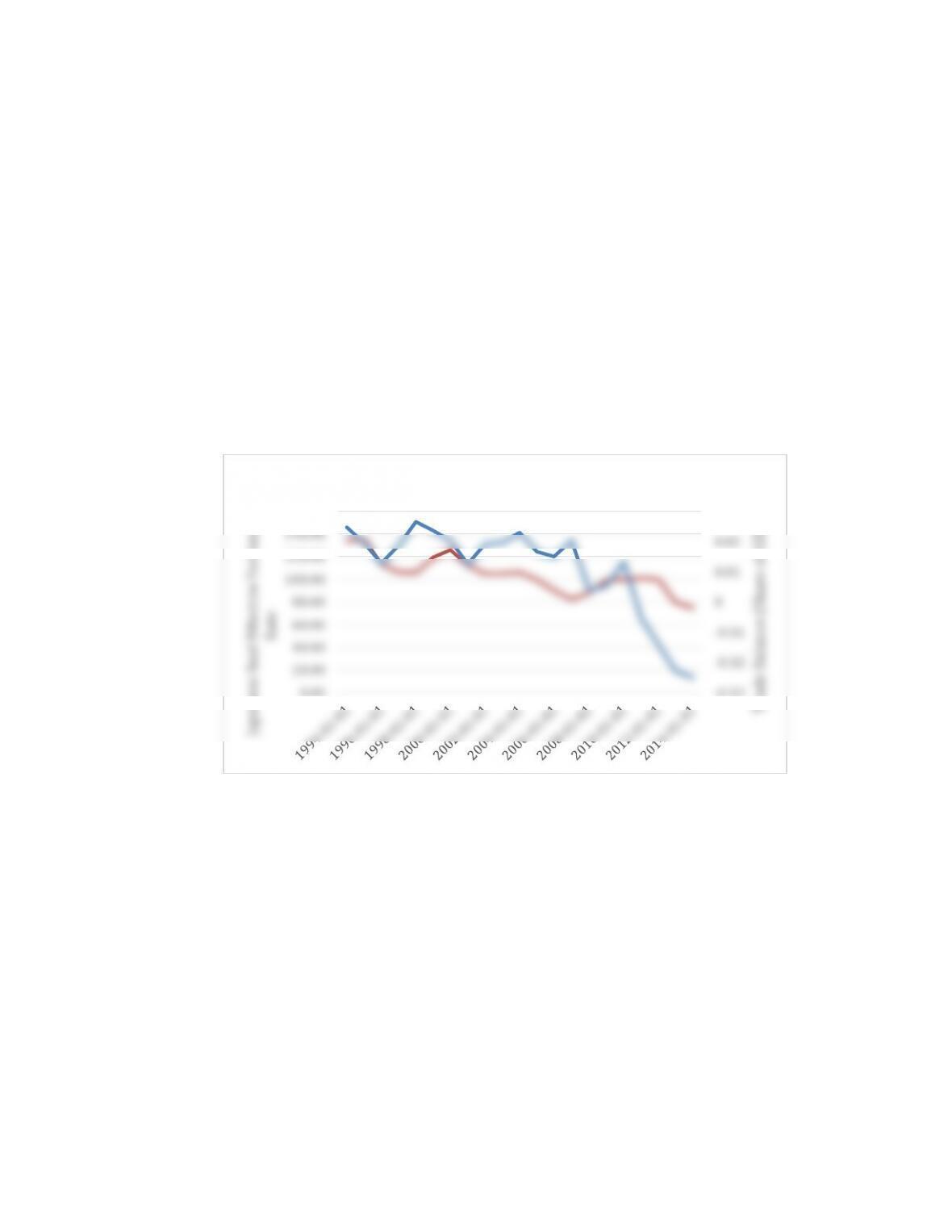

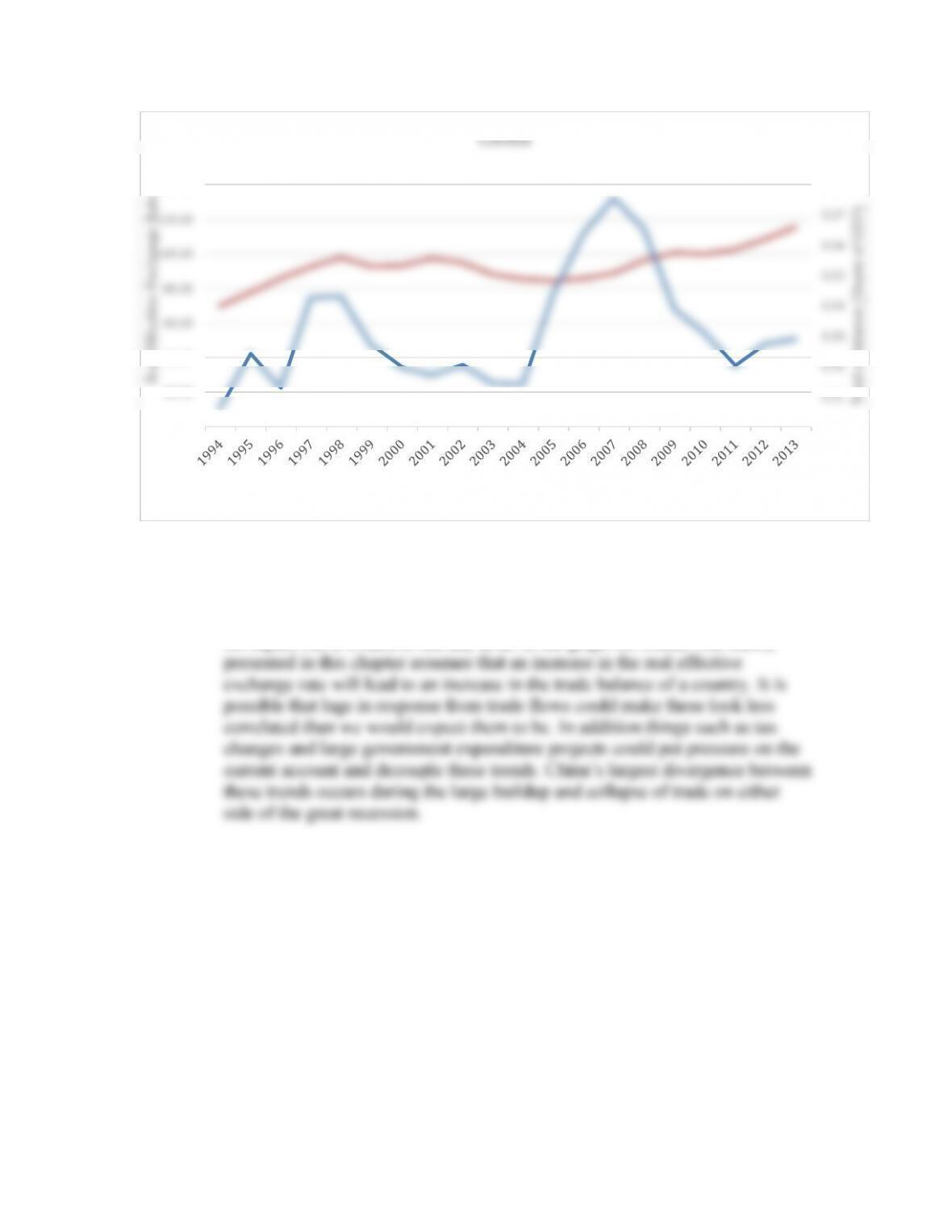

1. Discovering Data In this chapter we discussed the weak link between the real

exchange rate and the trade balance. We looked at a time series diagram showing

these two variables for the United States in Figure 18-4, but what about other

countries? Go to the online FRED database (https://fred.stlouisfed.org) and download

the data for the real effective exchange rate, the trade balance (in local currency)

and GDP (in local currency) for China and Japan from 1995 to the present.

a. For each country make a chart, like Figure 18-4, that shows the real exchange

rate and the trade balance as a share of GDP on the same line graph. Use the

left vertical axis for the real exchange rate and the right vertical axis for the

trade balance as a percent of GDP.

ANSWER: See the charts below.

-0.03

-0.02

-0.01

0

0.01

0.02

0.03

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

Trade Balance (Share of GDP)

Japanese Real Effective Exchange

Rate

Japan

b. For each country, do you find that these variables have a strong relationship?

Is it what you would expect from this chapter? Explain why this relationship

might fail or even go in the opposite direction of what we would expect.

Answer: There does appear to be a weak relationship between these variables

for Japan, but it is hard to see any at all in the graph for China. Our theory

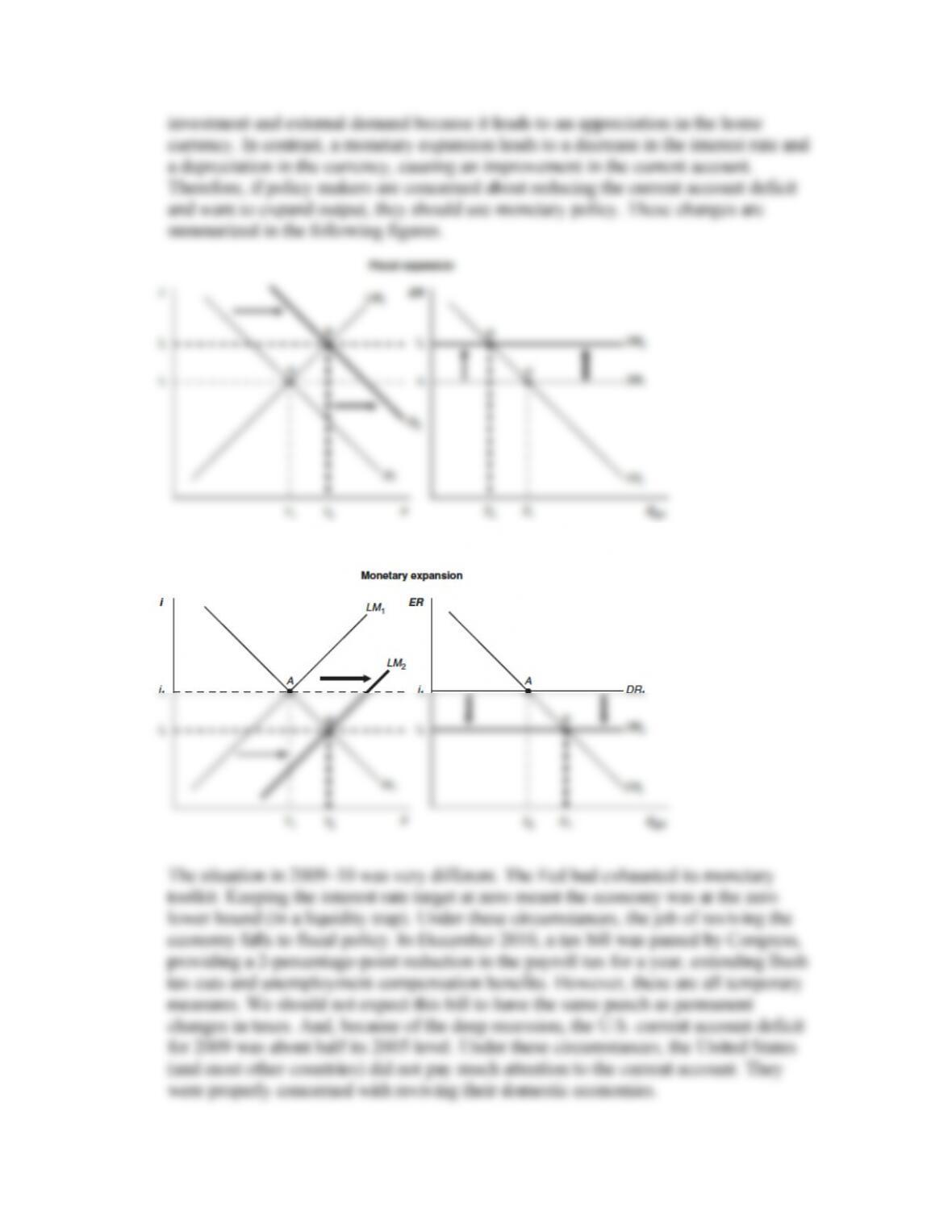

2. In 2001, President George W. Bush and Federal Reserve Chairman Alan Greenspan

were both concerned about a sluggish U.S. economy. They also were concerned about

the large U.S. current account deficit. To help stimulate the economy, President Bush

proposed a tax cut, while the Fed had been increasing U.S. money supply. Compare

the effects of these two policies in terms of their implications for the current account.

If policy makers are concerned about the current account deficit, discuss whether

stimulatory fiscal policy or monetary policy makes more sense in this case. Then,

reconsider similar issues for 2009–10, when the economy was in a deep slump, the

Fed had taken interest rates to zero, and the Obama administration was arguing for

larger fiscal stimulus. Why might many believe that the Fed should keep interest rates

at near zero levels in 2016 and beyond as growth remains stagnant?

Answer: From the model, we know that fiscal expansion leads to crowding out of

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Trad e Balance (Share of GDP)

Real Effective Exchange Rate

China

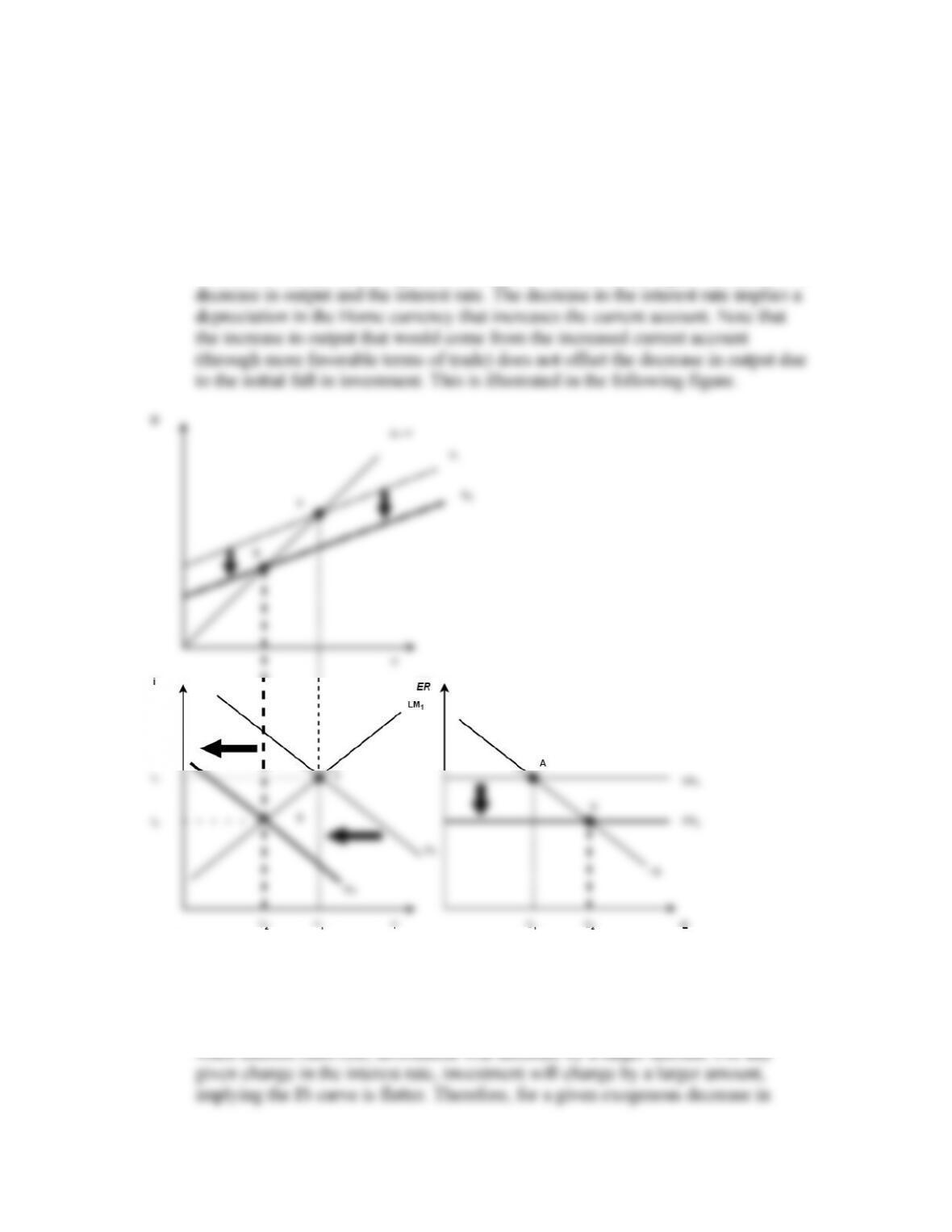

3. Suppose that American firms become more pessimistic and decide to reduce

investment expenditure today in new factories and office space.

a. How will this increase in investment affect output, interest rates, and the current

account?

Answer: This is an exogenous decrease in investment demand. This leads to an

increase in the demand for goods, shifting the IS curve to the right. This leads to a

b. Now repeat part (a), assuming that domestic investment is very responsive to the

interest rate so that U.S. firms will cancel most of their changes in investment

plans if the interest rate falls. How will this affect the answer you gave

previously?

Answer: If investment is very responsive to the interest rate, then this implies that

when interest rates rise, investment will decrease by a larger amount. For any

Work It Out

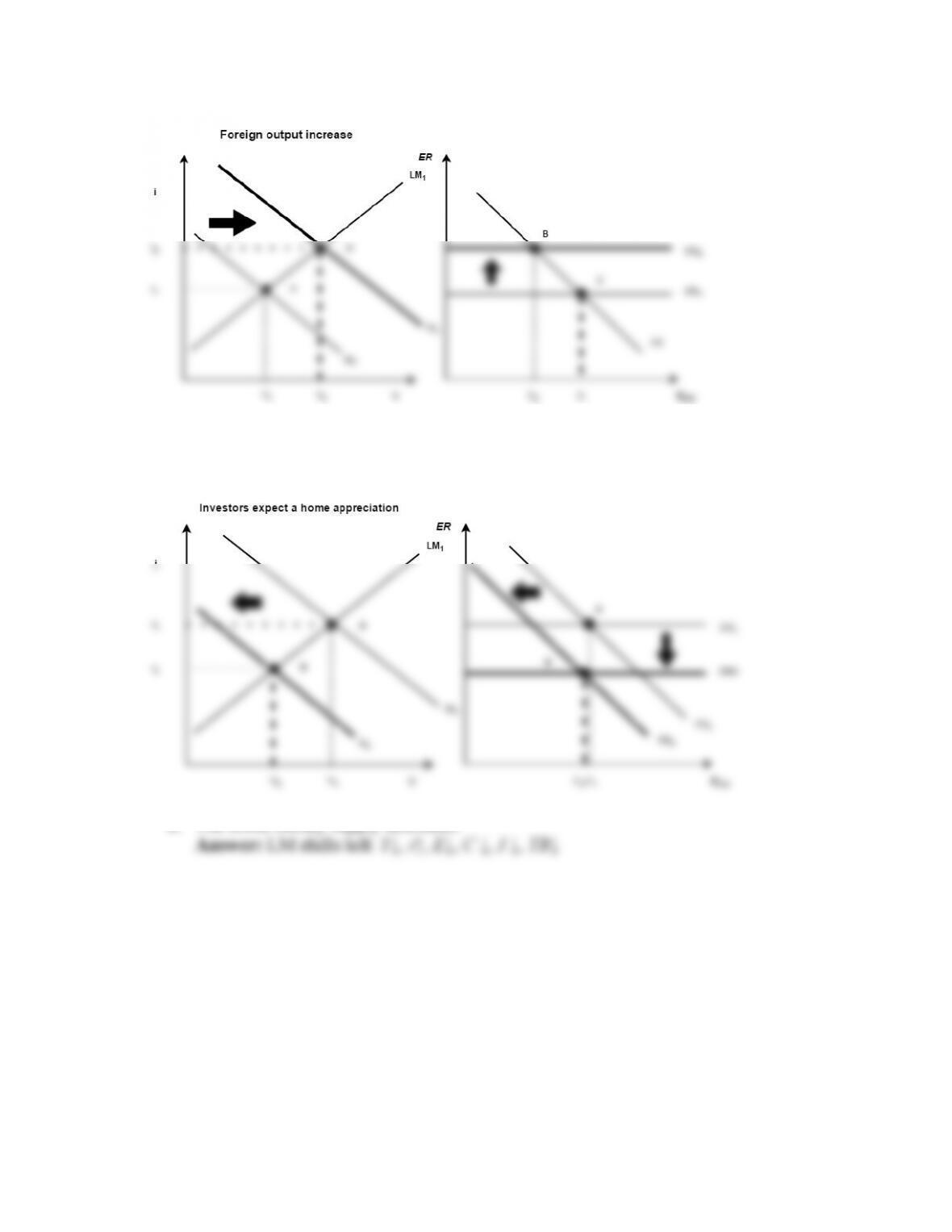

For each of the following situations, use the IS–LM–FX model to illustrate the effects of

the shock. For each case, state the effect of the shock on the following variables

(increase, decrease, no change, or ambiguous): Y, i, E, C, I, and TB. Note: In this

question, assume the government allows the exchange rate to float and makes no

policy response.

Hint: In each case, make use of the goods market equilibrium condition to understand

what happens to consumption, investment, and the trade balance in the shift from the

old to the new equilibrium.

a. Foreign output increases.

b. Investors expect an appreciation of the home currency in the future.

Answer: FR shifts left, IS shifts left, DR shifts down: Y ↓, i↓ , E↓ , C↓ , I ↑, TB↓

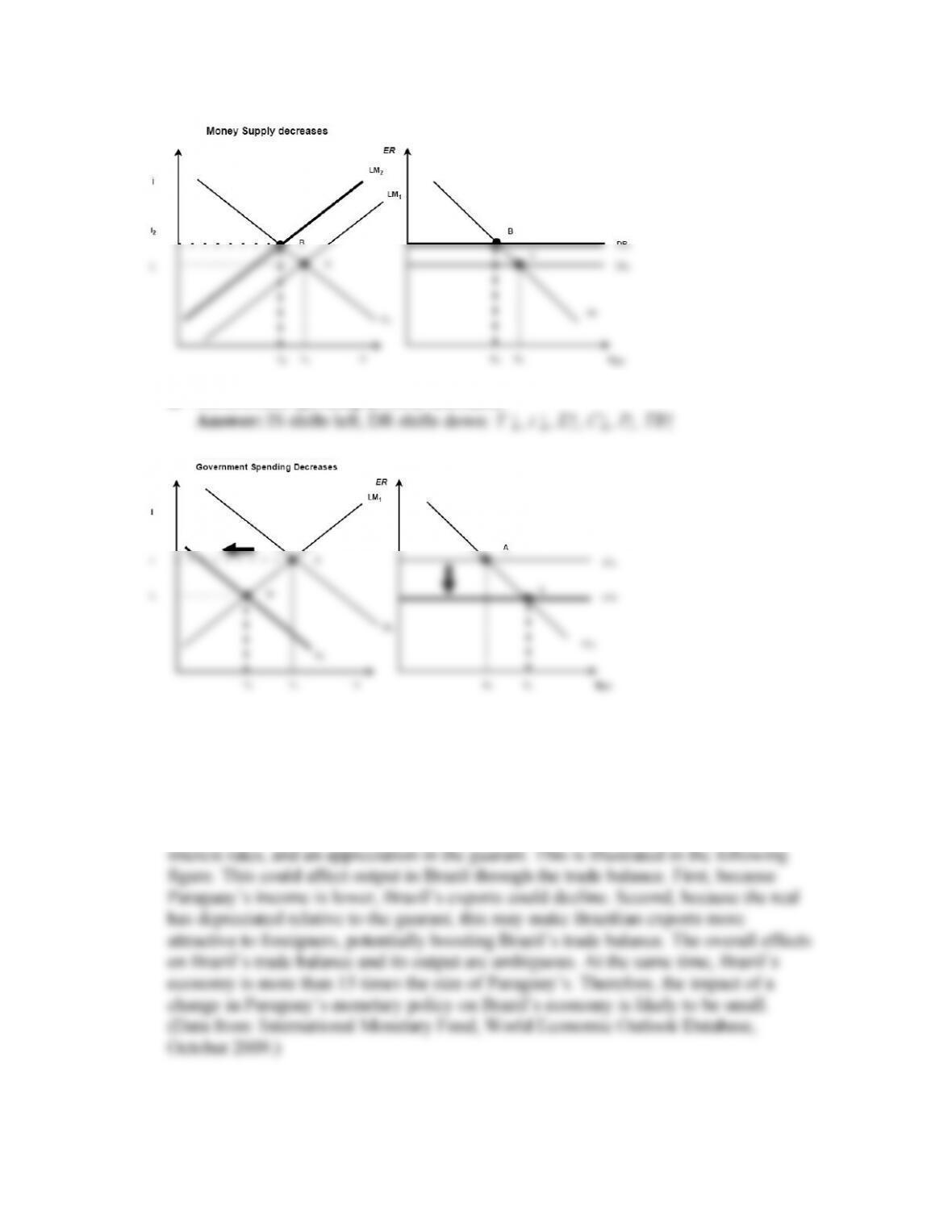

c. The home money supply decreases.

d. Government spending at home decreases.

4. How would a decrease in the money supply of Paraguay (currency unit: the guaraní)

affect its own output and its exchange rate with Brazil (currency unit: the real). Do

you think this policy in Paraguay might also affect output across the border in Brazil?

Explain.

Answer: A decrease in the real money supply leads to a leftward shift in the LM

curve. This leads to a decrease in Paraguay’s output, an increase in Paraguay’s

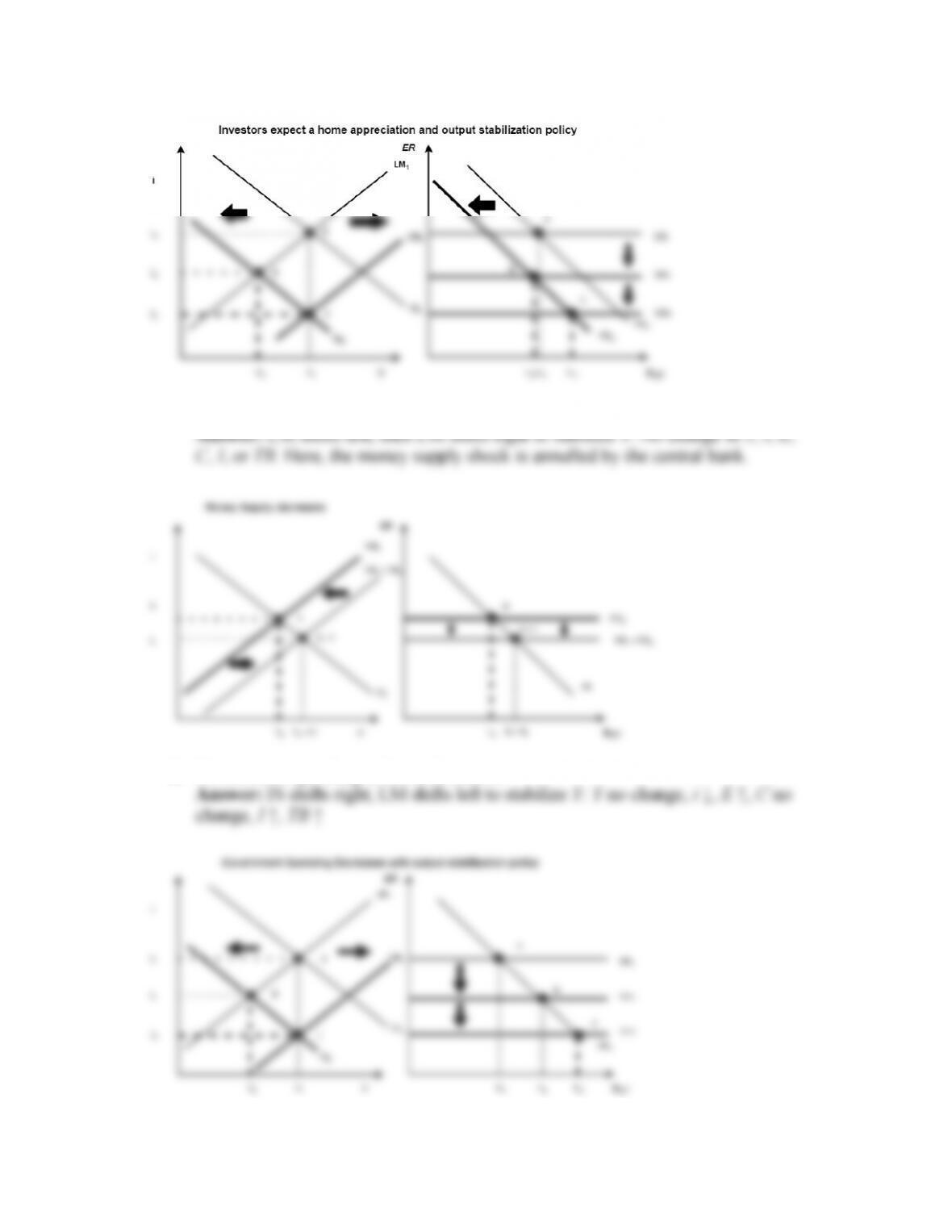

5. For each of the following situations, use the IS–LM–FX model to illustrate the effects

of the shock and the policy response. For each case, state the effect of the shock on

the following variables (increase, decrease, no change, or ambiguous): Y, i, E, C, I,

and TB. Note: In this question (unlike in the Work It Out question) assume that the

government allows the exchange rate to float but also responds by using monetary

policy to stabilize output.

Hint: In each case, make use of the goods market equilibrium condition to understand

what happens to consumption, investment, and the trade balance in the shift from the old

to the new equilibrium.

a. Foreign output increases.

Answer: IS shifts right, LM shifts left to stabilize Y: Y no change, i↑, E↓ , C no

b. Investors expect an appreciation of the home currency in the future.

c. The home money supply decreases.

d. Government spending at home decreases.

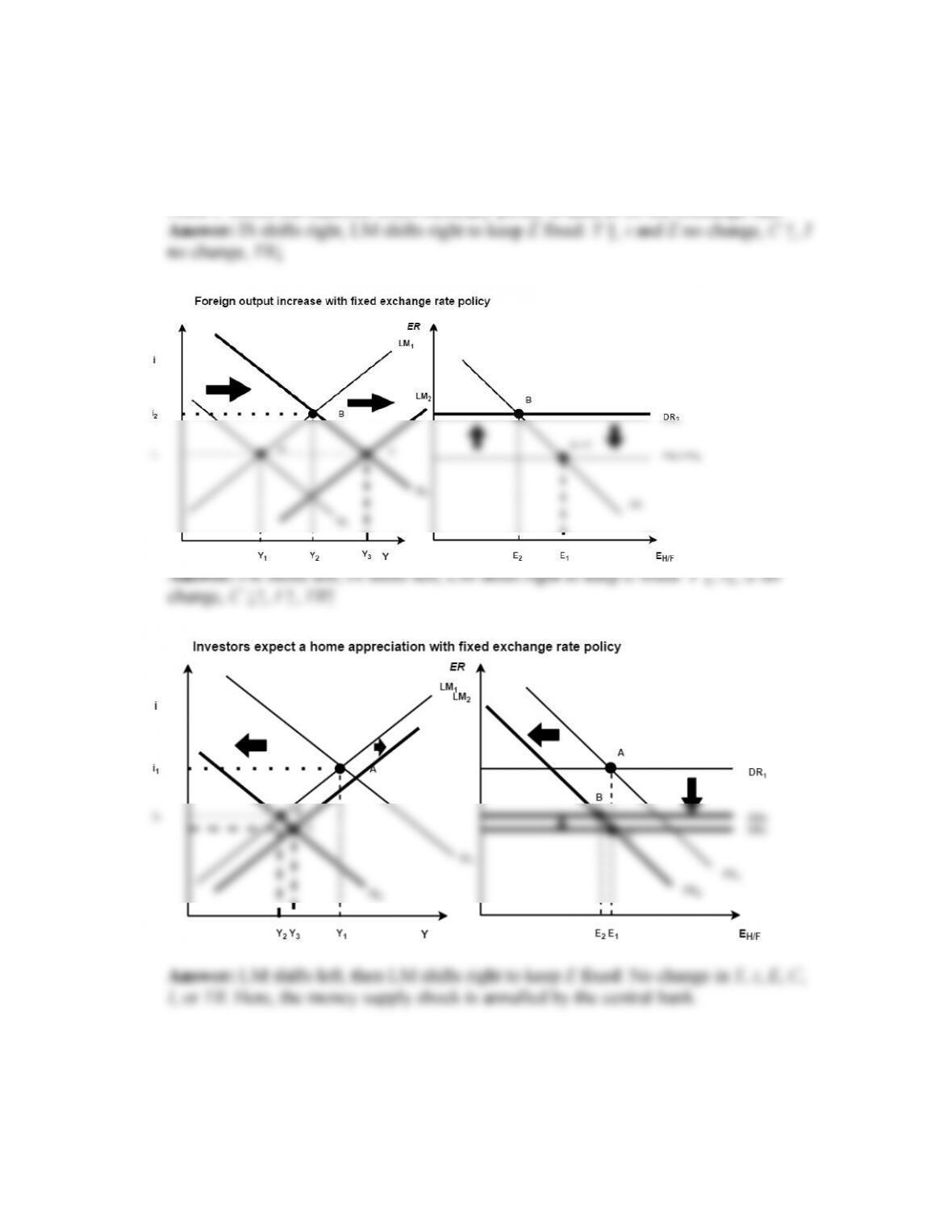

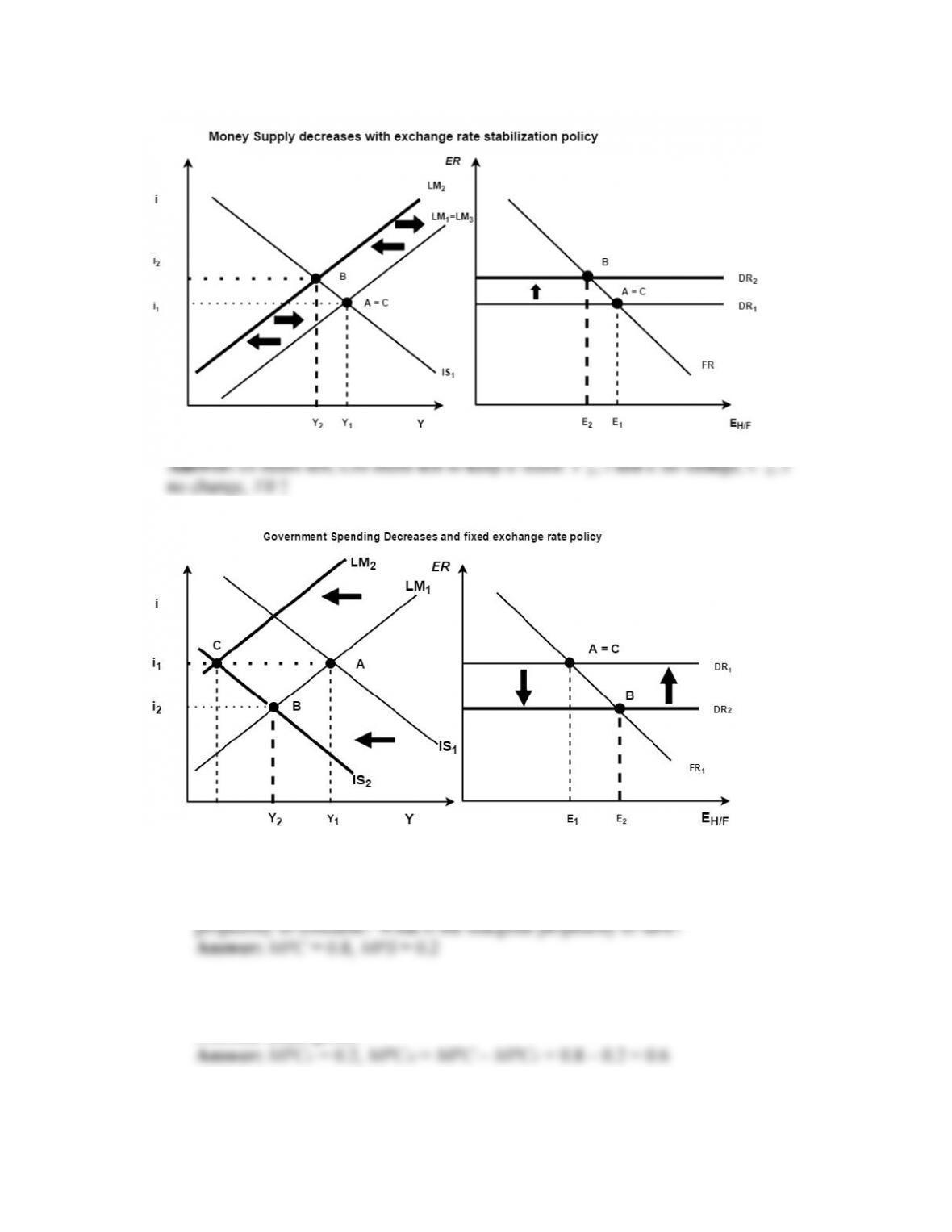

6. Repeat the previous question, assuming the central bank responds in order to maintain

a fixed exchange rate. In which case or cases will the government response be the

same as in the previous question?

See the following diagrams. Point B is identical to the outcomes shown in Question 3.

Point C shows the outcome when monetary policy is used to fix the exchange rate.

7. This question explores IS and FX equilibria in a numerical example.

a. The consumption function is C = 1.5 + 0.8(Y – T). What is the marginal

b. The trade balance is TB = 5(1 – [1/E]) – 0.2(Y – 8). What is the marginal

propensity to consume foreign goods? What is the marginal propensity to

consume home goods?

c. The investment function is I = 3 – 10i. What is investment when the interest rate i

is equal to 0.10 = 10%?

d. Assume government spending is G. Add up the four components of demand and

write down the expression for D.

Answer: D = C + I + G + TB

e. Assume forex market equilibrium is given by i = ([1/E] – 1) + 0.15, where the two

foreign return terms on the right are expected depreciation and the foreign interest

rate. What is the foreign interest rate? What is the expected future exchange rate?

8. [More difficult] Continuing the last question, solve for the IS curve: obtain an

expression for Y in terms of i, G, and T (eliminate E).

Answer: Solve the UIP condition for E:

9. Assume that initially the IS curve is given by

IS1: Y = 22 – 1.5T – 30i + 2G

and that the price level P is 1, and the LM curve is given by

LM1: M = Y(1 – i)

The home central bank uses the interest rate as its policy instrument. Initially, the

home interest rate equals the foreign interest rate of 10% or 0.1. Taxes and

government spending both equal 2. Call this case 1.

a. According to the IS1 curve, what is the level of output Y? Assume this is the

desired full employment level of output.

b. According to the LM1 curve, at this level of output, what is the level of the home

money supply?

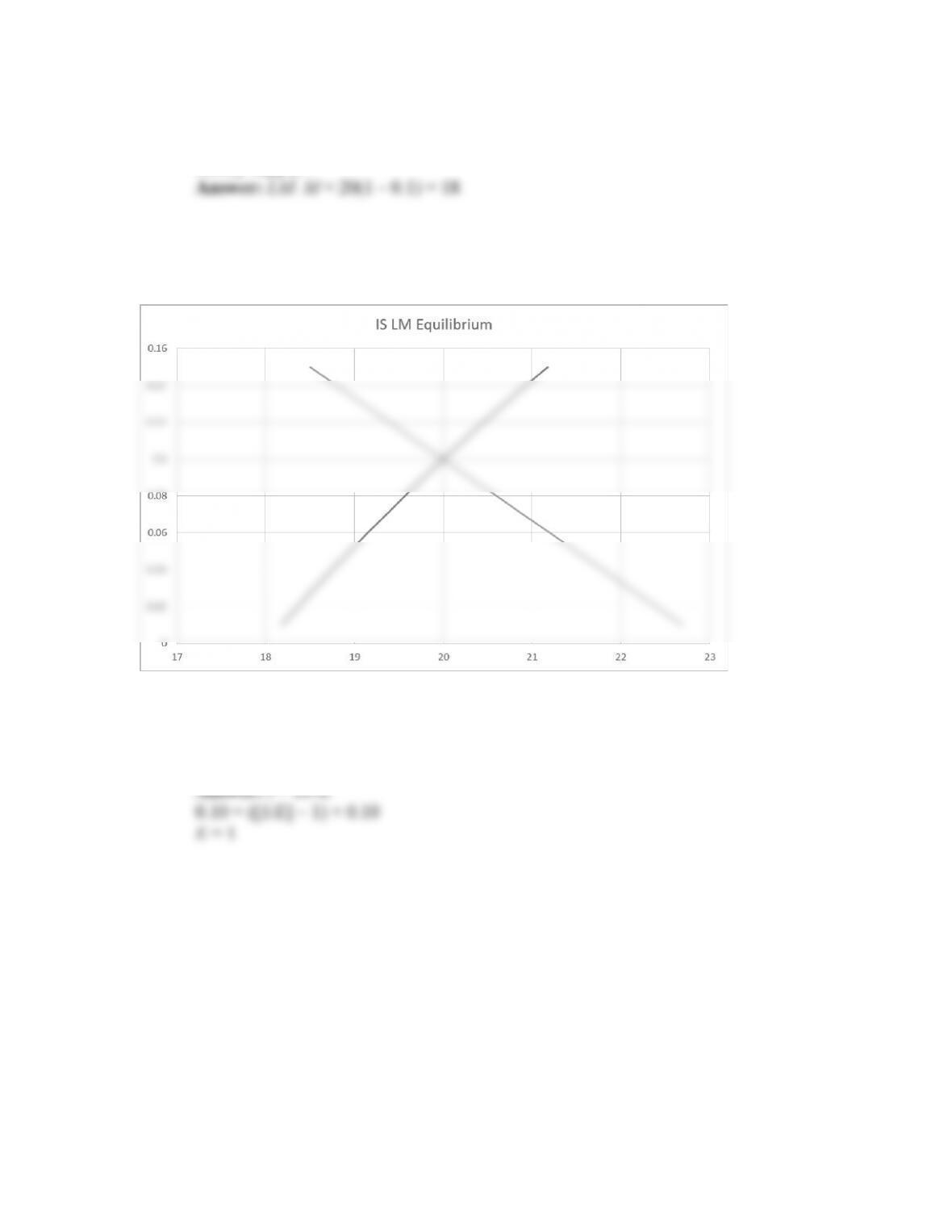

c. Plot the IS1 and LM1 curves for case 1 on a chart. Label the axes, and the

equilibrium values.

Answer: See the following diagram.

d. Assume that forex market equilibrium is given by i = ([1/E] – 1) + 0.10, where the

two foreign return terms on the right are expected depreciation and the foreign

interest rate. The expected future exchange rate is 1. What is today’s spot

exchange rate?

e. There is now a foreign demand shock, such that the IS curve shifts left by 1.5

units at all levels of the interest rate, and the new IS curve is given by

IS2: Y = 20.5 – 1.5T – 30i + 2G

The government asks the central bank to stabilize the economy at full

employment. To stabilize and return output back to the desired level, according to

this new IS curve, by how much must the interest rate be lowered from its initial

level of 0.1? (Assume taxes and government spending remain at 2.) Call this case

2.

Answer: Plug the desired value of output (Y = 20) into the new IS curve to find

the implied interest rate, i2:

f. At the new lower interest rate and at full employment, on the new LM curve

(LM2), what is the new level of the money supply?

Answer: Plug the output and interest rate from (e) into the LM curve to find M:

g. According to the forex market equilibrium, what is the new level of the spot

exchange rate? How large is the depreciation of the home currency?

Answer: Plug the new interest rate into the UIP condition:

h. Plot the new IS2 and LM2 curves for case 2 on a chart. Label the axes, and the

equilibrium values.

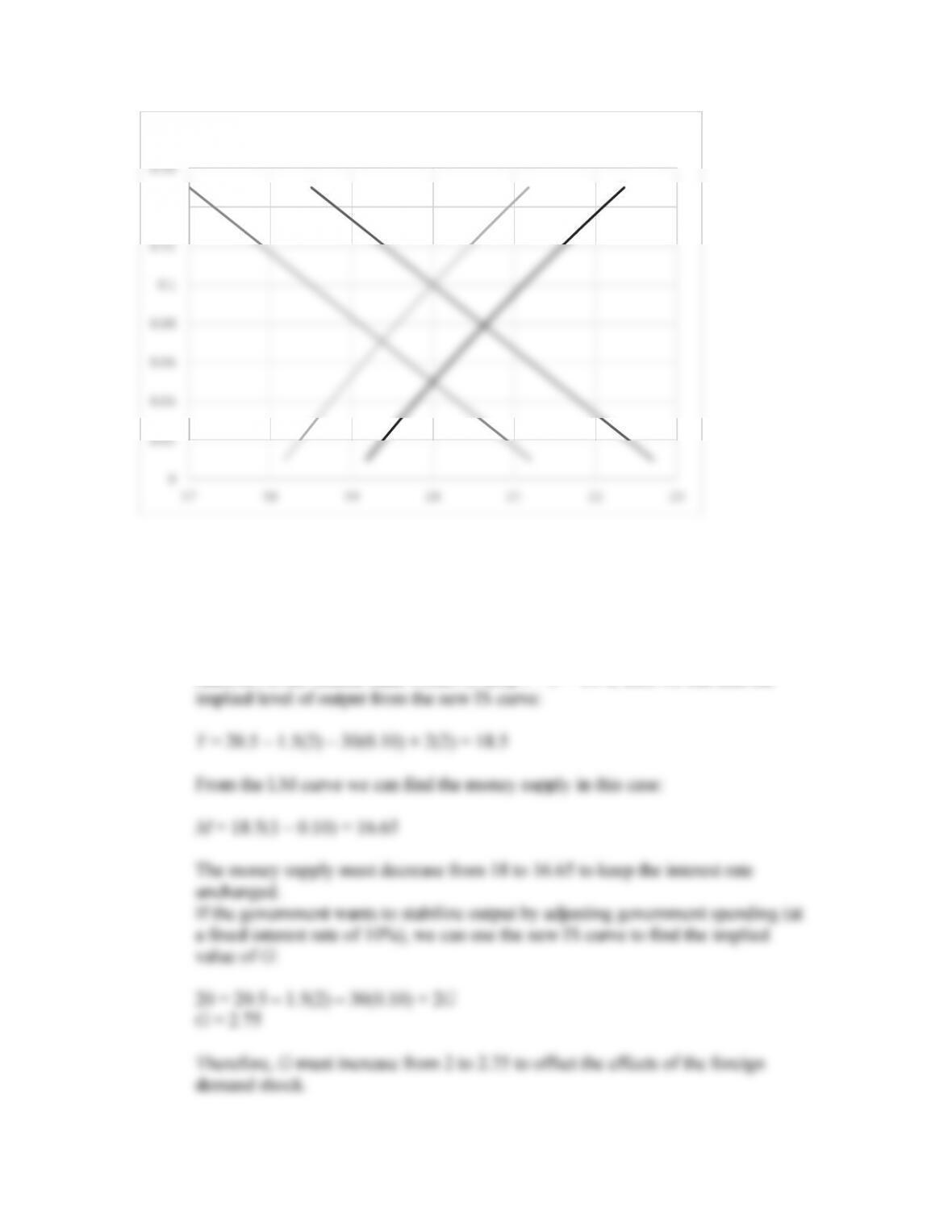

Answer: See the diagram below.

IS–LM Equilibrium

j. Plot the new IS3 and LM3 curves for case 3 on a chart. Label the axes, and the

equilibrium values.

Answer: See the figure below. IS’ and LM’ indicate the IS and LM curves when

IS curve has the same shock as in part (e) and the central bank still keeps the

10. In this chapter, we’ve studied how policy responses affect economic variables in an

open economy. Consider each of the problems in policy design and implementation

discussed in this chapter. Compare and contrast each problem as it applies to

monetary policy stabilization versus fiscal policy stabilization.

Answer: Consider the following limitations:

• Policy constraints. Depending on the exchange rate regime, these are more likely

to restrict monetary policy. Because monetary policy typically uses a nominal