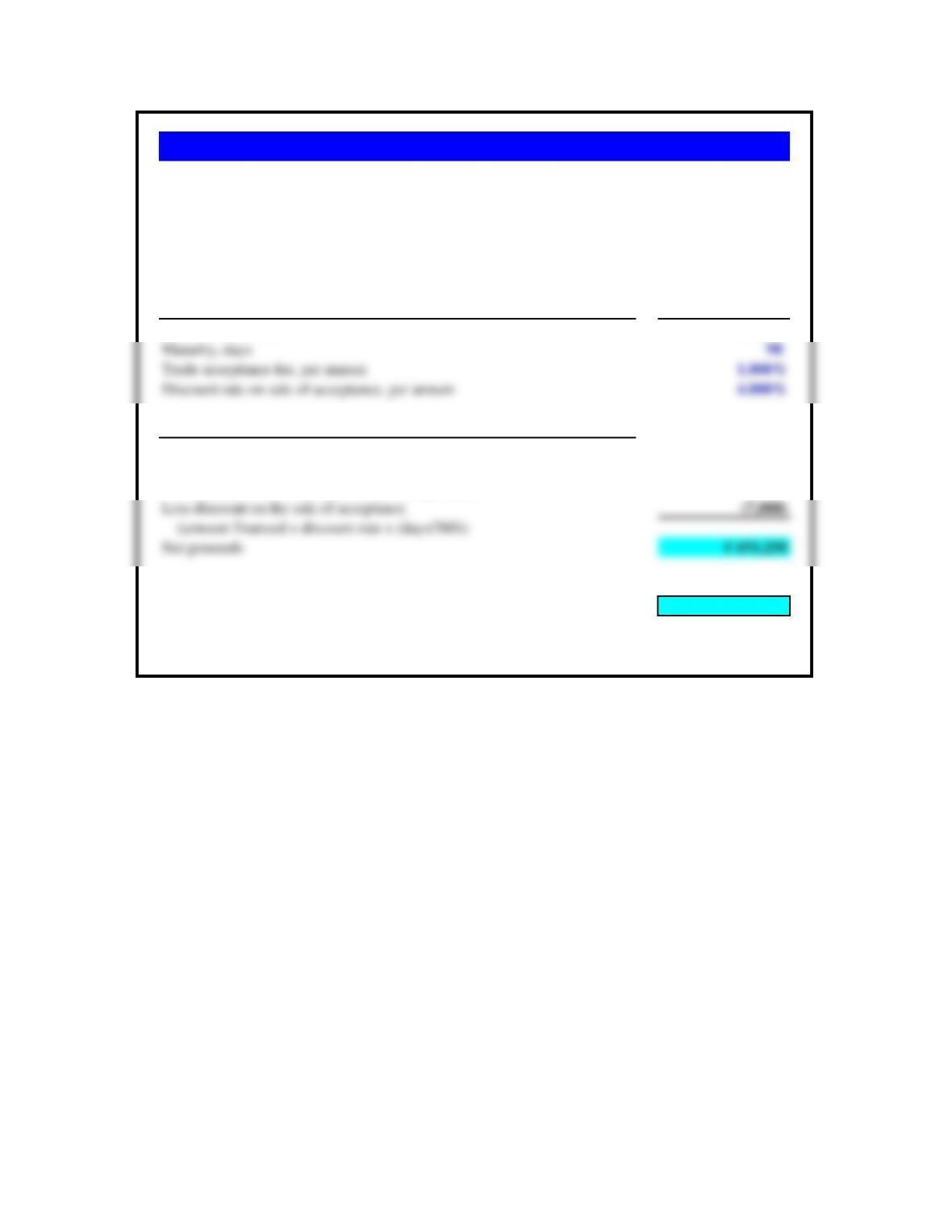

Assumptions Values

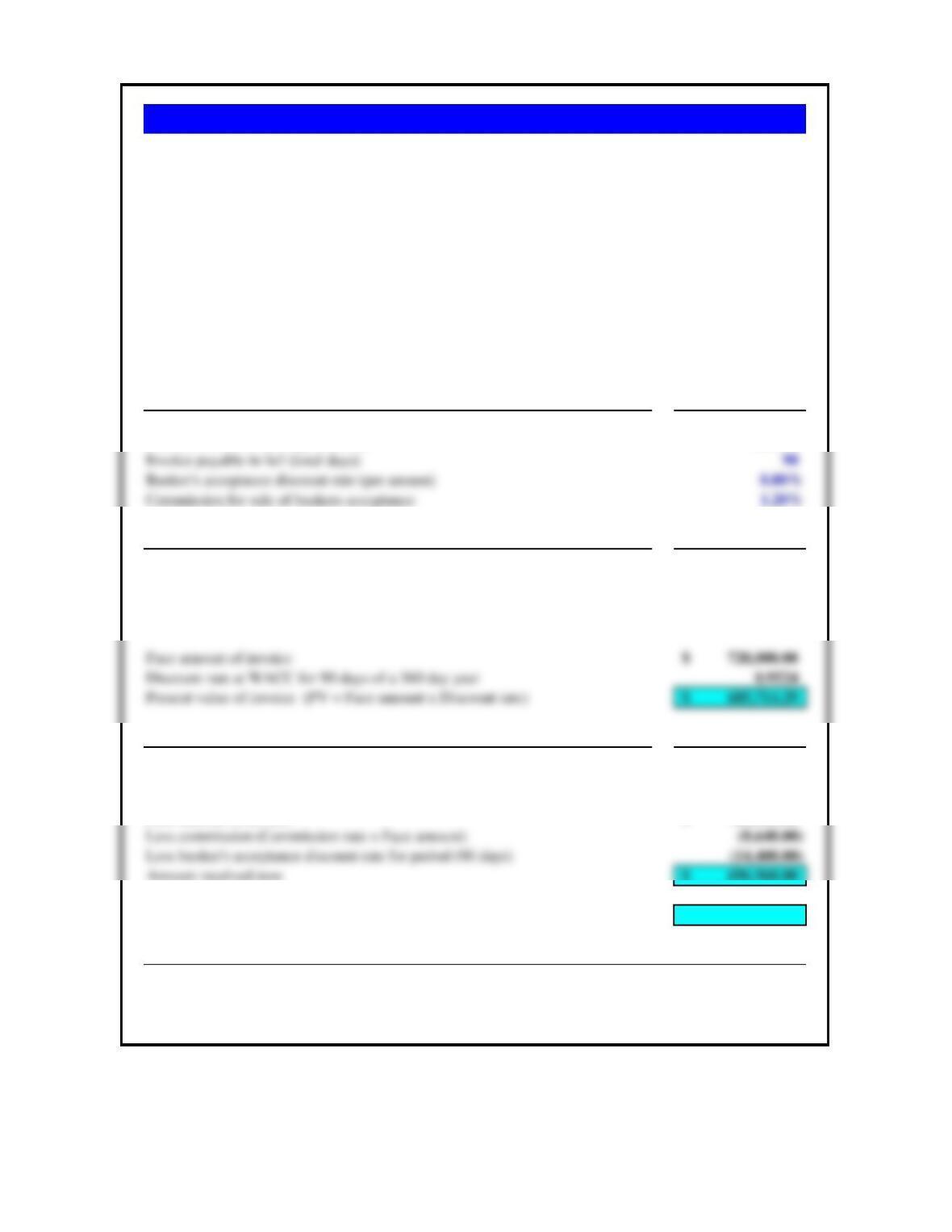

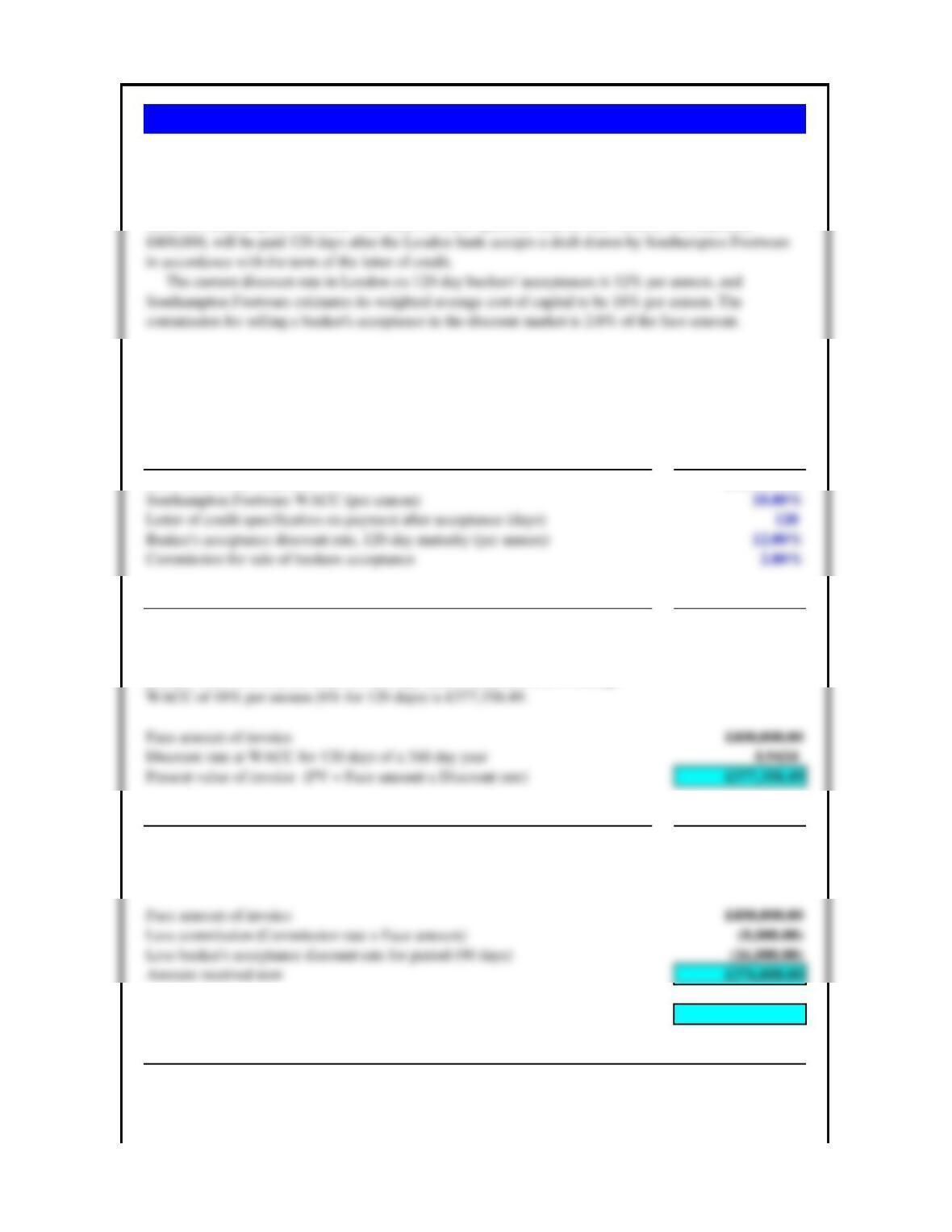

Face amount of sale € 700,000

All-in-Cost of Trade Acceptance

Face amount of the receivable € 700,000

Less trade acceptance fee (1,750)

(amount financed x acceptance fee x (days/360) )

Annualized percentage all-in-cost (AIC) 5.063%

(acceptance fee + discount) / (amount received) x (360/180)

Problem 16.1 Nikken Microsystems (A)

Assume Nikken Microsystems has sold Internet servers to Telecom España for €700,000. Payment

is due in 3 months and will be made with a trade acceptance from Telecom España Acceptance. The

acceptance fee is 1.0% per annum of the face amount of the note. This acceptance will be sold at a

4% per annum discount. What is the annualized percentage all-in-cost in euros of this method of

trade financing?

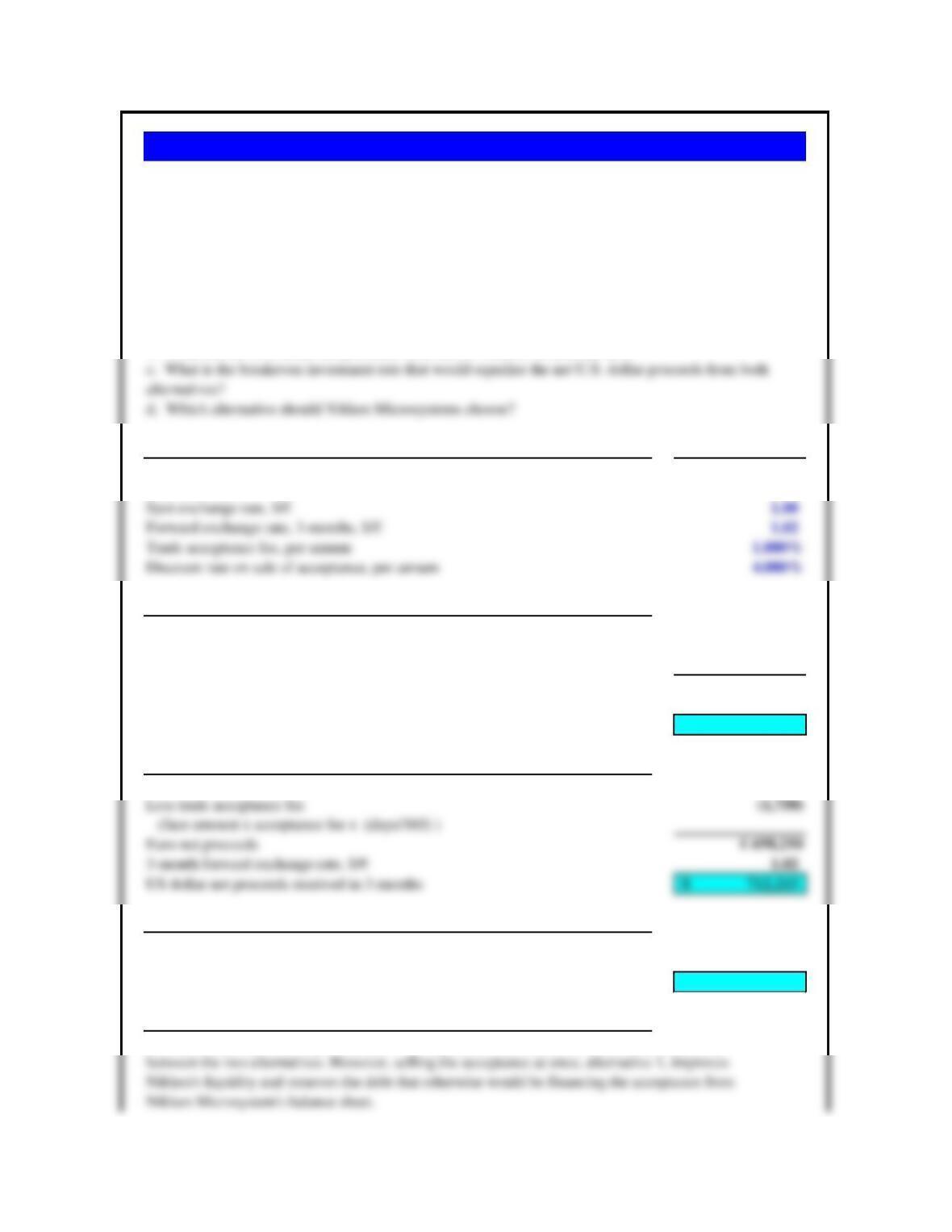

Assumptions Values

Face amount of sale € 700,000

Maturity, days 90

Spot exchange rate, $/€1.00

Forward exchange rate, 3-months, $/€1.02

a. What are the US dollar proceeds received at once?

Face amount of the receivable € 700,000

Less trade acceptance fee (1,750)

(face amount x acceptance fee x (days/360) )

Euro proceeds € 698,250

Spot exchange rate, $/€1.00

US dollar proceeds, now 698,250$

b. What are the dollar proceeds received in 3 months under alternative 2?

Face amount of the receivable € 700,000

3-month forward exchange rate, $/€1.02

c. Breakeven reinvestment rate

US dollars received now, part a) 698,250$

US dollars received at end of 90 days, part b) 712,215$

Breakeven reinvestment rate of $ now to equal $ in 3 months (per annum) 8.000%

d. Which alternative should Nikken Microsystems choose?

If Nikken Microsystems’ opportunity cost of capital is 8%, it should be indifferent financially

Problem 16.2 Nikken Microsystems (B)

Assume that Nikken Microsystems prefers to receive U.S. dollars rather than euros for the trade

transaction described in problem 1. It is considering two alternatives:1) It can sell the acceptance for

euros at once and convert the euros immediately to U.S. dollars at the spot rate of exchange of $1.00/€; or

2) It can hold the euro acceptance until maturity but at the start sell the expected euro proceeds forward

for dollars at the 3-month forward rate of $1.02/€.

d. Which alternative should Nikken Microsystems choose?

a. What are the U.S. dollar net proceeds received at once from the discounted trade acceptance in

alternative 1?

b. What are the U.S. dollar net proceeds received in 3 months in alternative 2?

Assumptions Values

All-in-cost of Bankers’ Acceptance

Face amount of bankers’ acceptance 3,000,000.00$

Less acceptance fee for 6-month maturity (26,250.00)

( face amount x acceptance fee x (term/360))

Amount received by Indian 2,973,750.00$

Problem 16.3 Motoguzzie (A)

Motoguzzie exports large-engine motorcycles (greater than 700cc) to Australia and invoices its

customers in U.S. dollars. Sydney Wholesale Imports has purchased $3,000,000 of merchandise

from Motoguzzie, with payment due in 6 months. The payment will be made with a bankers’

acceptance issued by Charter Bank of Sydney at a fee of 1.75% per annum. Motoguzzie has a

weighted average cost of capital of 10%. If Motoguzzie holds this acceptance to maturity, what is its

annualized percentage all-in cost?

Assumptions Values

Value of shipment 3,000,000$

Credit terms, days 180

All-in-Cost of Bankers’ Acceptance

Face amount of bankers’ acceptance 3,000,000.00$

Less acceptance fee for 6-month maturity (26,250.00)

Problem 16.4 Motoguzzie (B)

Assuming the facts in problem 3, Bank of America is now willing to buy Motoguzzie’s bankers’

acceptance for a discount of 6% per annum. What would be Motoguzzie’s annualized percentage all-

in-cost of financing its $3,000,000 Australian receivable?

Assumptions Values

Face amount of sale (first payment of 5) 200,000$

All-in-Cost of Trade Acceptance

Face amount of sale 200,000.00$

Less cash down-payment (40,000.00)

Amount for financing 160,000.00$

a. Annualized percentage all-in-cost (AIC) 5.128%

(acceptance fee + discount) / (amount received) x (360/180)

a. What is the annualized percentage all-in-cost to Nakatomi Toyota?

b. What are Nakatomi’s net cash proceeds, including the cash down payment?

Problem 16.5 Nakatomi Toyota

NakatomiToyota buys its cars from Toyota Motors-USA, and sells them to U.S. customers. One of

its customers is EcoHire, a car rental firm which buys cars from Nakatomi Toyota at a wholesale

price. Final payment is due to Nakatomi Toyota in 6 months. EcoHire has bought $200,000 worth of

cars from Nakatomi, with a cash down payment of $40,000 and the balance due in 6 months without

any interest charged as a sales incentive. Nakatomi Toyota will have the EcoHire receivable

accepted by Alliance Acceptance for a 2% fee, and then sell it at a 3% per annum discount to Wells

Fargo Bank.

Assumptions Values

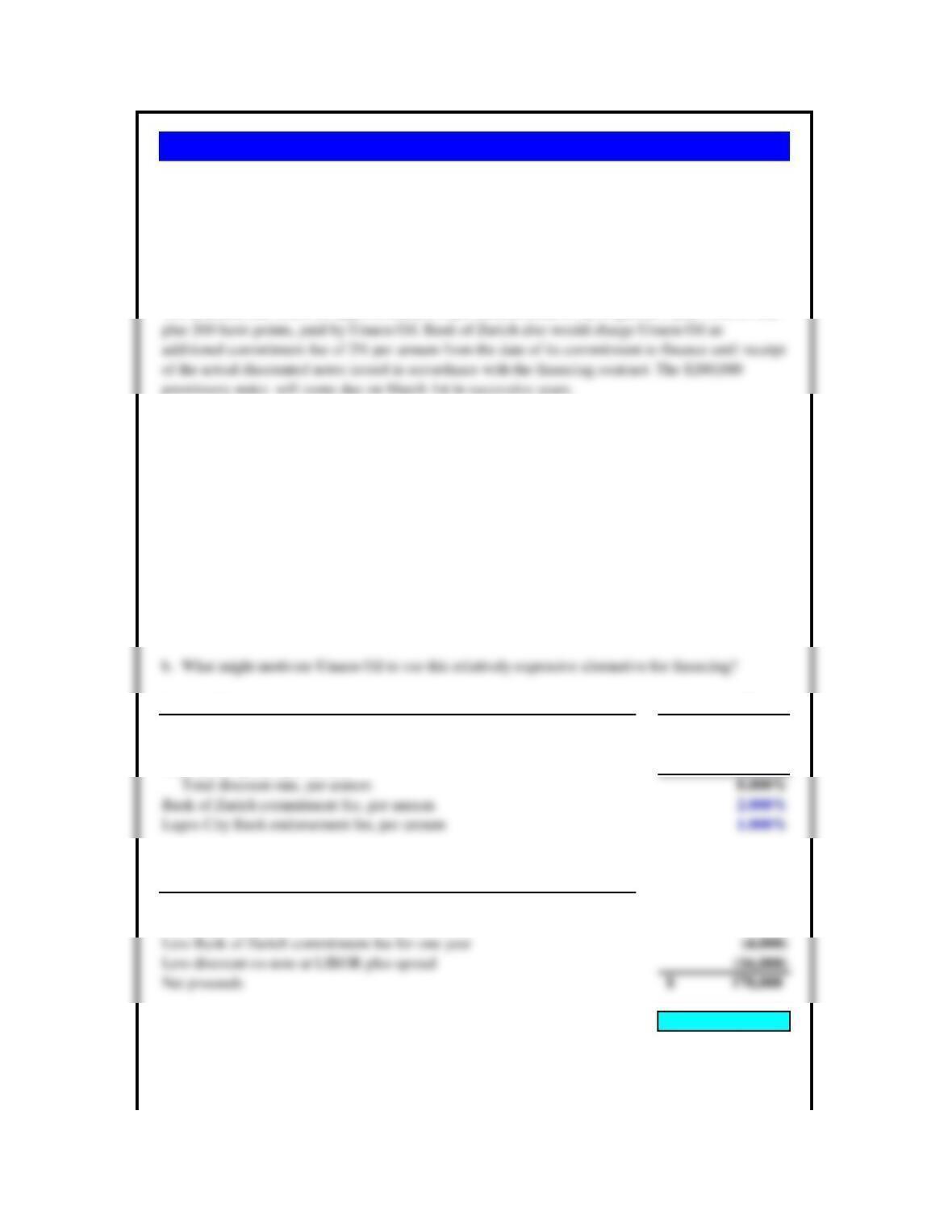

Face amount of the note due March 1, 2011 issued by Kaduna 200,000$

3-year LIBOR rate, per annum 6.000%

Basis point spread, per annum 2.000%

What is the all-in-cost of forfaiting?

Face amount of note 200,000$

Less Lagos City bank endorsement fee (2,000)

Annualized all-in-cost of factoring 11.000%

( total interest and fee costs / face amount of note )

Umaru Oil would probably be motivated to use a forfaiter because its credit worth is too

low to qualify for more normal financing. Note that the 11% annual costs are paid by

b. What might motivate Umaru Oil to use this relatively expensive alternative for financing?

The promissory notes issued by Umaru Oil will be endorsed by their bank, Lagos City Bank, for

a 1% fee and delivered to Gunslinger Drilling. At this point Gunslinger Drilling will endorse the

notes without recourse and discount them with the forfaiter, Bank of Zurich, receiving the full

$200,000 principal amount. Bank of Zurich will sell the notes by re-discounting them to investors in

the international money market without recourse. At maturity the investors holding the notes will

present them for collection at Lagos City Bank. If Lagos City Bank defaults on payment, the

investors will collect on the notes from Bank of Zurich.

a. What is the annualized percentage all-in-cost to Umaru Oil of financing the first $200,000 note

due March 1, 2011?

Problem 16.6 Forfaiting at Umaru Oil (Nigeria)

Umaru Oil of Nigeria has purchased $1,000,000 of oil drilling equipment from Gunslinger Drilling

of Houston, Texas. Umaru Oil must pay for this purchase over the next 5 years at a rate of $200,000

per year due on March 1st of each year.

Bank of Zurich, a Swiss forfaiter, has agreed to buy the 5 notes of $200,000 each at a discount.

promissory notes will come due on March 1st in successive years.

Problem 16.7 Sunny Coast Enterprises (A)

a. What are the annualized percentage all-in-costs of each alternative?

Assumptions Values

Face amount of receivable 100,000$

Maturity, days 180

Alternative 1: Bank Credit Line

Face amount of receivable 100,000$

Less bank interest expense on receivable (3,250)

Annualized all-in-cost of alternative 1 8.469%

Alternative 2: Bank Credit Line + Export Credit Insurance

Face amount of receivable 100,000$

Less credit insurance fee (1,000)

Annualized all-in-cost of alternative 2 9.150%

Note: The reason the compensating balance is deducted from net proceeds is that

Sunny Coast Enterprises does not get that cash and does not earn interest on it.

Sunny Coast Enterprises has sold a combination of films and DVDs to Hong Kong Media

Incorporated for US$100,000, with payment due in 6 months. Sunny Coast Enterprises has the

following alternatives for financing this receivable: 1) Use its bank credit line. Interest would be at

the prime rate of 5% plus 150 basis points per annum. Sunny Coast Enterprises would need to

maintain a compensating balance of 20% of the loan’s face amount. No interest will be paid on the

compensating balance by the bank; or 2) Use its bank credit line but purchase export credit

insurance for a 1% fee. Because of the reduced risk, the bank interest rate would be reduced to 5%

per annum without any points.

Assumptions Values

Face amount of receivable 100,000$

a. What is the annualized all-in-cost of factoring?

Face amount of receivable 100,000$

Less cost of factoring, discount rate (8,000)

Less non-recourse clause (2,000)

Net proceeds from factoring 90,000$

Annualized all-in-cost of factoring 22.222%

b. What are the advantages and disadvantages of the factoring alternative compared to the

alternatives in Sunny Coast Enterprises (A)?

Problem 16.8 Sunny Coast Enterprises (B)

Sunny Coast Enterprises has been approached by a factor that offers to purchase the Hong Kong

Media Imports receivable at a 16% per annum discount plus a 2% charge for a non-recourse clause.

a. What is the annualized percentage all-in-cost of this factoring alternative?

Assumptions Values

Principal of note 100,000$

Maturity of note, days 180

Acceptance fee to be paid by Whatchamacallit 500$

All-in-cost to Whatchamacallit:

Face amount of note 100,000$

Less acceptance fee (500)

Annualized all-in-cost of factoring 3.046%

( total interest and fee costs / net proceeds ) x (360/maturity)

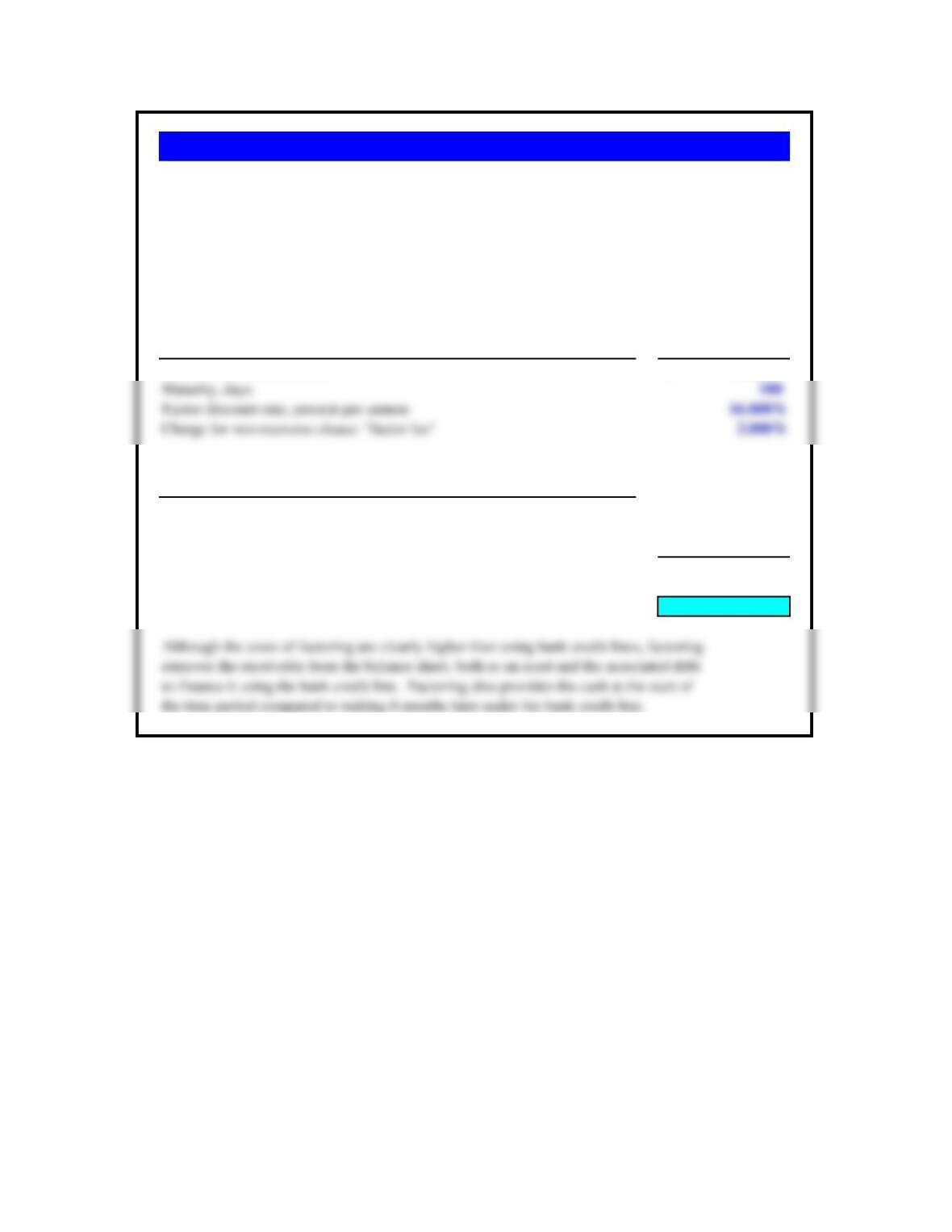

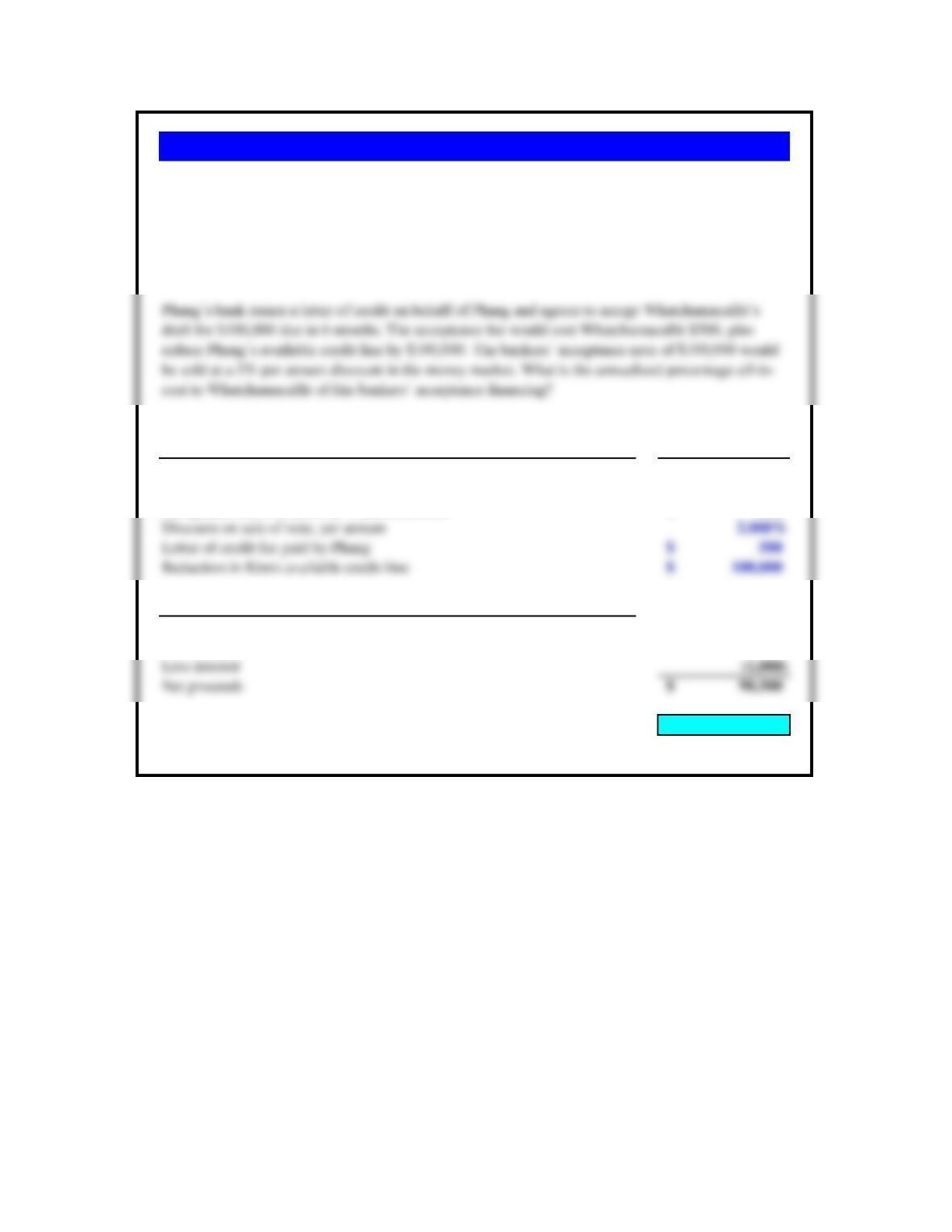

Problem 16.9 Whatchamacallit Sports (A)

Whatchamacallit Sports (Whatchamacallit) is considering bidding to sell $100,000 of ski equipment

to Phang Family Enterprises of Seoul, Korea. Payment would be due in 6 months. Since

Whatchamacallit cannot find good credit information on Phang, Whatchamacallit wants to protect its

credit risk. It is considering the following financing solution.

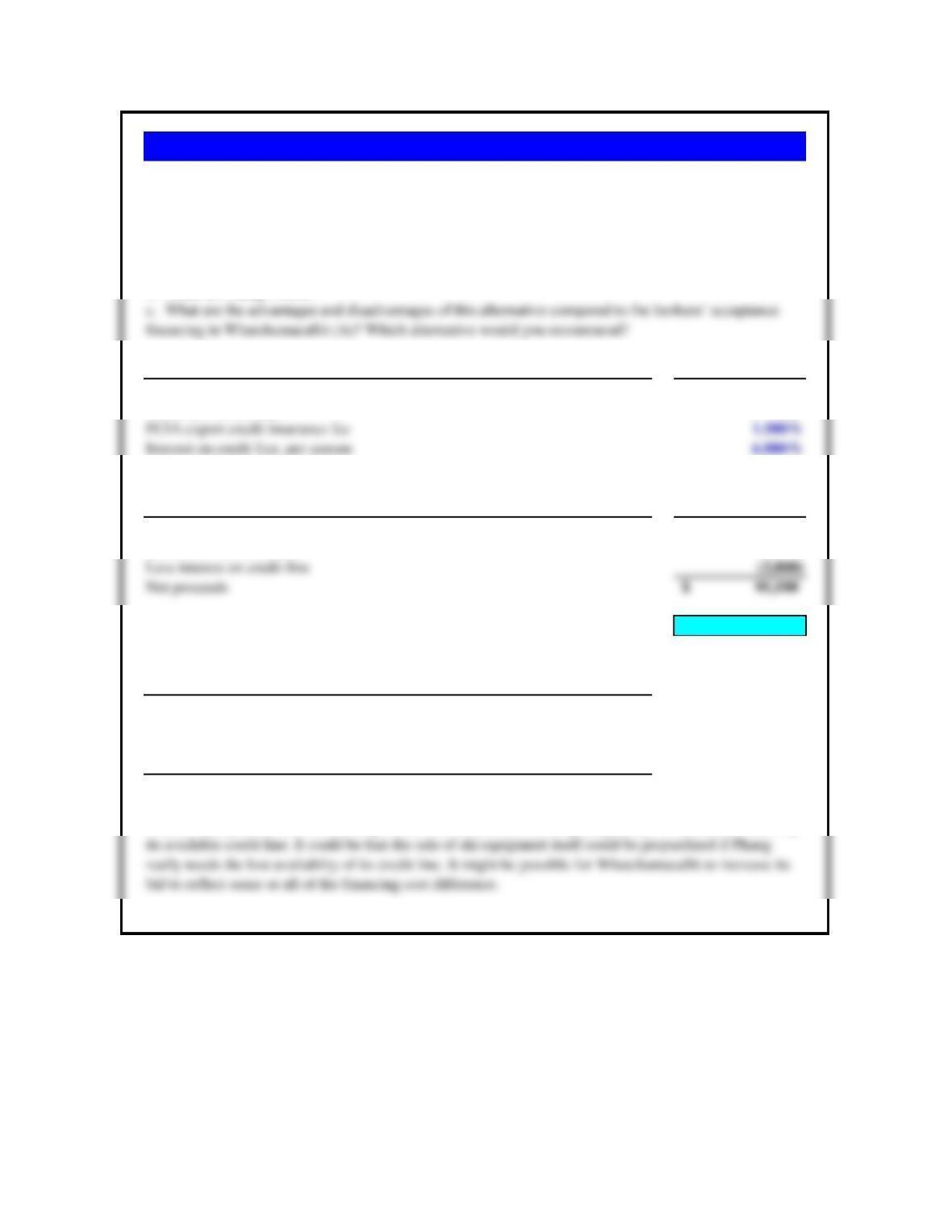

Problem 16.10 Whatchamacallit Sports (B)

a. What is Whatchamacallit’s annualized percentage all-in-cost of financing?

b. What are Phang’s costs?

Assumptions Values

Principal of note 100,000$

Maturity of note, days 180

a. All-in-cost to Whatchamacallit: Values

Face amount 100,000$

Less credit insurance fee (1,500)

Annualized all-in-cost of factoring 9.424%

( total interest and fee costs / net proceeds ) x (360/term of note)

b. What is the cost ot Phang?

Phang has no costs under this alternative, and it preserves its credit line.

c. What are the advanatges and disadvantages of this alternative?

Whatchamacallit could also buy export credit insurance from FCIA for a 1.5% premium. It finances the

$100,000 receivable from Phang from its credit line at 6% per annum interest. No compensating bank

balance would be required.

The cost of using its credit line would cost Whatchamacallit 9.42% compared to only 3.05% with the

bankers’ acceptance. However, Phang would avoid the $500 cost of getting a letter of credit and reducing

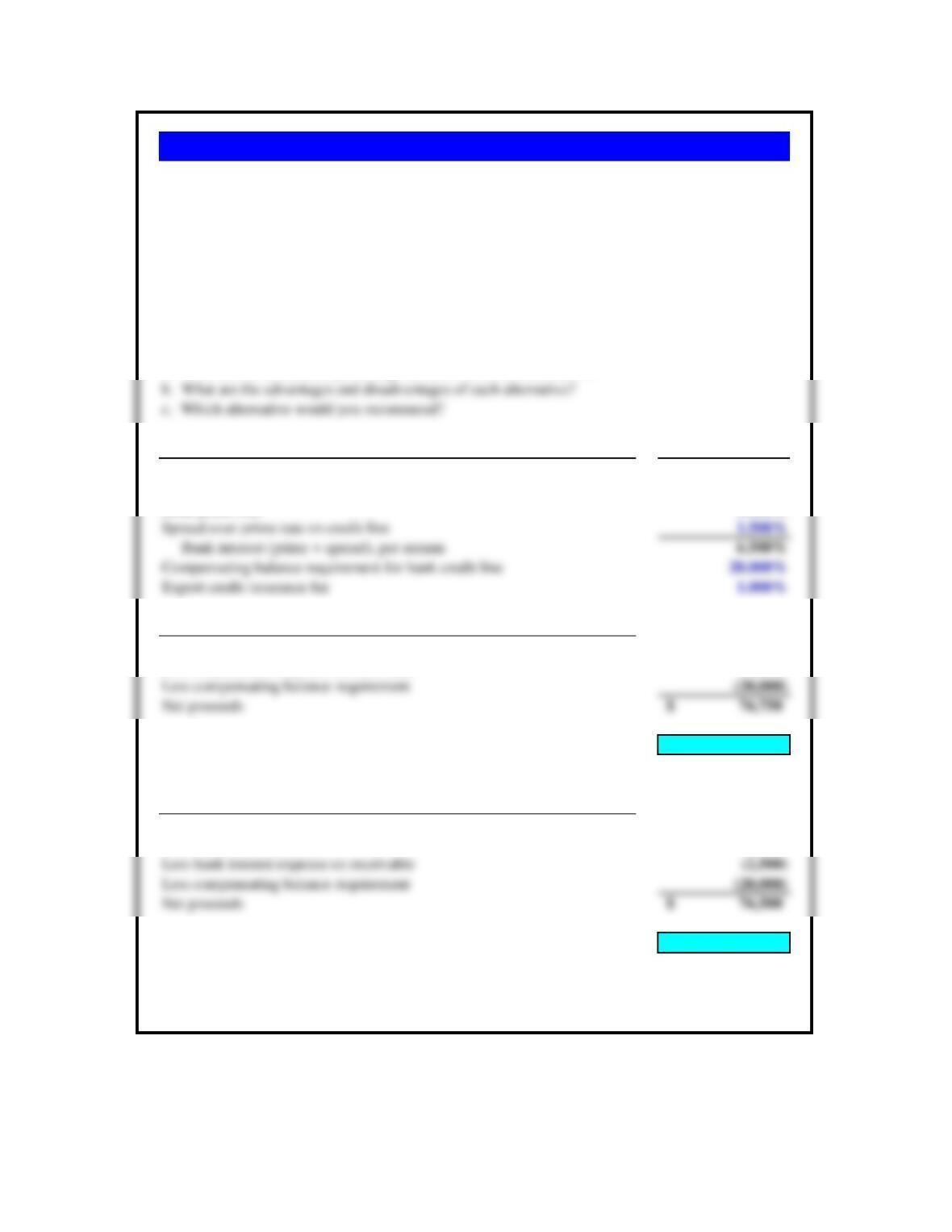

financing in Whatchamacallit (A)? Which alternative would you recommend?

Problem 16.11 Inca Breweries of Peru

Assumptions Values

Invoice 720,000$

Inca Breweries WACC (per annum) 20.00%

Alternative 1 Values

Alternative 2 Values

Inca Breweries can sell the banker’s acceptance in today’s money market at an 8% per annum discount:

Face amount of invoice 720,000.00$

Amount received now 696,960.00$

Difference between alternatives (11,245.71)$

Analysis

If Inca Breweries holds the draft for 90 days after the bank accepts it, Inca

Breweries will receive the face amount of $720,000. The present value of

$720,000 received 90 days hence, discounted at Inca’s WACC of 20% per

The current discount rate on three-month banker’s acceptances is 8% per annum, and Inca Breweries

estimates its weighted average cost of capital to be 20% per annum. The commission for selling a

banker’s acceptance in the discount market is 1.2% of the face amount.

The amount of cash received today (i.e., $696,960) is greater than the present value of the full $720,000

(i.e., $685,714.29) discounted at Inca’s WACC. Inca should sell the acceptance in today’s banker’s

acceptance market and take the cash at once.

Inca Breweries of Lima, Peru, has received an order for 10,000 cartons of beer from Alicante Importers

of Alicante, Spain. The beer will be exported to Spain under the terms of a letter of credit issued by a

Madrid bank on behalf of Alicante Importers. The letter of credit specifies that the face value of the

shipment, $720,000, will be paid 90 days later after the Madrid bank accepts a draft drawn by Inca

Breweries in accordance with the terms of the letter of credit.

How much cash will Inca Breweries receive from the sale if it holds the acceptance until maturity? Do

you recommend that Inca Breweries hold the acceptance until maturity or discount it at once in the U.S.

banker’s acceptance market?

Problem 16.12 Swishing Shoe Company

b. Does Swishing Shoe Company incur any other risks in this transaction?

Assumptions Values

Face value of the shipment £400,000.00

Alternative 1 Values

WACC of 18% per annum (6% for 120 days) is £377,358.49.

Alternative 2 Values

Difference between alternatives £1,358.49

Analysis

Point 1. Swishing’s gain should be calculated in present value terms. Swishing will receive £376,000

today by discounting the banker’s acceptance. The present value of the £400,000 to be received in 120

days, discounted at Swishing’s WACC of 18%, is £377,358.49. The difference is £1,358.49. Swishing

would gain, in terms of present value cash, £1,358.49 by waiting 120 days to receive the face amount of

Swishing Shoe Company of Durham, North Carolina, has received an order for 50,000 cartons of athletic

shoes from Southampton Footware, Ltd., of England, payment to be in British pounds sterling. The shoes

will be shipped to Southampton Footware under the terms of a letter of credit issued by a London bank on

behalf of Southampton Footware. The letter of credit specifies that the face value of the shipment,

£400,000, will be paid 120 days after the London bank accepts a draft drawn by Southampton Footware

in accordance with the term of the letter of credit.

The current discount rate in London on 120-day bankers’ acceptances is 12% per annum, and

Southampton Footware estimates its weighted average cost of capital to be 18% per annum. The

commission for selling a banker’s acceptance in the discount market is 2.0% of the face amount.

If Southampton Footware holds the draft for 120 days after the bank has

accepted it, Swishing Footware will received the face amount of £400,000. The

present value of £400,000 received 120 days hence, discounted at Swishing‘s

Swishing Shoes can sell the banker’s acceptance in today’s London money

market at a 12% per annum discount:

a. Would Swishing Shoe Company gain by holding the acceptance to maturity, as compared to

discounting the bankers’ acceptance at once?

Point 1. Swishing’s gain should be calculated in present value terms. Swishing will receive £376,000

today by discounting the banker’s acceptance. The present value of the £400,000 to be received in 120

days, discounted at Swishing’s WACC of 18%, is £377,358.49. The difference is £1,358.49. Swishing

would gain, in terms of present value cash, £1,358.49 by waiting 120 days to receive the face amount of

Point 2. In this transaction Swishing has assumed the foreign exchange transaction risk; that is, the risk

that the pounds sterling to be received from the export will be worth fewer dollars when received. In part

rate then in effect. If Swishing waits 120 days to receive the pounds sterling, Swisher assumes the added

risk that the exchange rate will deteriorate between the time of sale and the time of collection. (Of course,

Swishing might gain if the pound would buy more, rather than less, dollars in 120 days.)

Problem 16.13 Going Abroad

If Swishing decides to open a plant and manufacture in Ireland, the following factors must be considered:

1. Corporate income tax rates in Ireland and the United States.

Assume that Great Britain charges a duty of 10% on shoes imported into the United Kingdom. Swishing Shoe

Company, in Problem 12, discovers that it can manufacture shoes in Ireland and import them into Britain free of

any import duty. What factors should Swishing consider in deciding to continue to export shoes from North

Carolina versus manufacture them in Ireland?

If Swishing shifts manufacturing to Ireland from North Carolina, it avoids the 10% import duty and the discount

on such banker’s acceptances as it now might be incurring. Alternatively, Swishing would avoid waiting 120 days

for its cash and undertaking the associated translation risk. Note that the solution to problem 2, above, in which

Swishing found it advantageous to wait 120 days for the cash is unique to that moment in time. A week or a

month later discount rates might change and the alternative would then be preferable.

7. The possibility that valuable technology of a proprietary nature would be stolen. (This might seem unlikely in

the Irish British context, but for other countries it could be a significant factor.)

Such a list as above cannot possibly identify all the subjective factors that might go into a decision to invest

rather than export, but it provides a starting point for consideration of the global strategy of a firm.

2. Present and possible future changes in shipping costs. (If Swishing had been using air freight before the

terrorist attack on the Twin Towers in New York and the Pentagon, it might encounter a sharp rise in air freight

rates afterward. Terrorists attacks and their aftermath can not be easily predicted, but success of a foreign

manufacturing venture versus exporting must consider the possibility of any kind of unpredictable structural

3. Expected production volume in Ireland relative to the designed manufacturing capacity of the new factory

there. The cost of manufacturing shoes in Ireland will depend both on the volume for which that plant is designed

and the percent of capacity expected to be used in the near future.

potential workers.

5. The existence, or nonexistence, of excess capacity in the North Carolina factory, both at present and in terms

of expected future growth.

6. The political risk of investing in Ireland for the British market, should the type of political terrorism and anti-

British feelings currently in Northern Ireland spread to the Republic of Ireland itself.

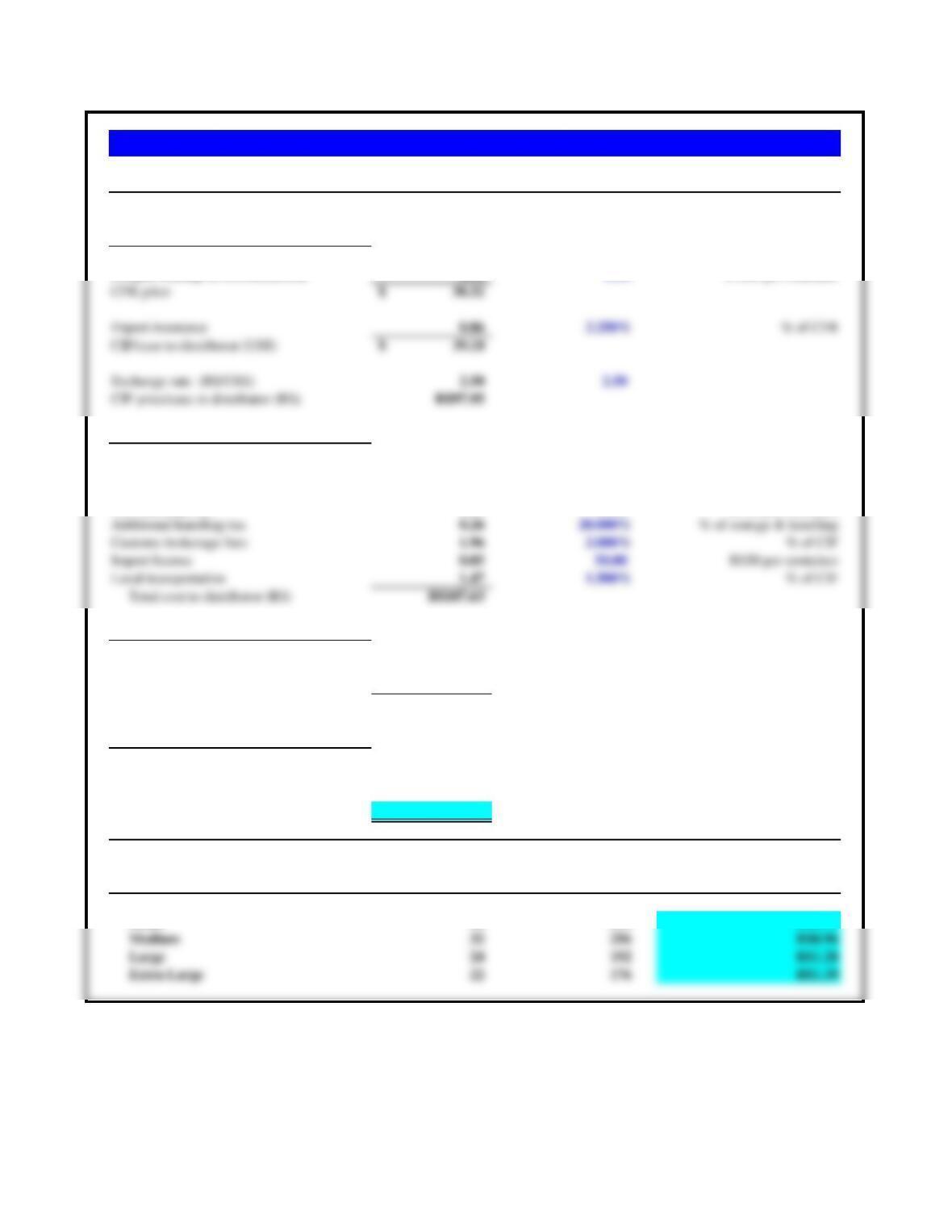

Price / case Rate Calculation

Cases per container 968

Export to Brazil Costs & Pricing

FOB price per case (US$) 34.00$

Brazilian Importation Costs

Import duties (ID) 1.96 2.000% % of CIF

Merchant marine renovation fee (MMRF) 2.70 25.00% % of freight

Port storage 1.27 1.300% % of CIF

Port handling fees 0.01 14.00 R$12 per container

Distributor’s Costs & Pricing

Storage cost 1.47 1.500% % of CIF * months

Cost of financing diaper inventory 6.86 7.000% % of CIF * months

Distributor’s margin 23.19 20.000% % of Price + storage + cc

Price to retailer (R$) 139.15

Brazilian Retailer Costs & Pricing

Industrial product tax (IPT-2) 20.87 15.000% % of price to retailer

Tax on merc circulation services (ICMS-2) 28.80 18.000% % of price + IPT2

Retailer costs and markup 56.65 30.000% % of price + IPT2 + ICMS2

Price per case to consumer (R$)

245.48

DIAPER PRICES Bags of 8 Diapers per Price to Consumer

per case case (R$/diaper)

Mini-Case: Crosswell International’s Precious Ultra-Thin Diapers