Country Risk Analysis ❖ 12

22. Integrating Country Risk and Capital Budgeting. Tovar Co. is a U.S. firm that has been asked to

provide consulting services to help Grecia Company (in Greece) improve its performance. Tovar

would need to spend $300,000 today on expenses related to this project. In one year, Tovar will

receive payment from Grecia, which will be tied to Grecia’s performance during the year. There is

uncertainty about Grecia’s performance and about Grecia’s tendency for corruption.

Tovar expects that it will receive 400,000 euros if Grecia achieves strong performance following the

consulting job. However, there are two forms of country risk that are a concern to Tovar Co. First,

there is an 80 percent chance that Grecia will achieve strong performance. In other words, there is a

20 percent chance that Grecia will perform poorly, in which case Tovar will receive a payment of

only 200,000 euros.

Second, while there is a 90 percent chance that Grecia will make its payment to Tovar, there is a 10

percent chance that Grecia will become corrupt. In this case, Grecia will not submit any payment to

Tovar.

Assume that the outcome of Grecia’s performance is independent of whether Grecia becomes corrupt.

The prevailing spot rate of the euro is $1.30, but Tovar expects that the euro will depreciate by 10

percent in one year, regardless of Grecia’s performance or whether it is corrupt.

Tovar’s cost of capital is 26 percent. Determine the expected value of the project’s net present value.

Determine the probability that the project’s NPV will be negative.

ANSWER:

Here are the results of each of four scenarios:

1. If the Greek firm performs well and there is no corruption, the net present value of the project is:

2. If Grecia performs well and there is corruption, there will not be a payment to Tovar, so the net

3. If the Grecia performs poorly and there is no corruption, the net present value of the project is:

4. If Grecia performs poorly and there is corruption, there will be no payment to Tovar, so the net

present value of the project is –$300,000.

Summary of Scenarios:

Scenario

Regarding

Performance

Probability

Regarding

Performance

Scenario

Regarding

Corruption

Probability

Regarding

Corruption

NPV

Strong

80%

Not corrupt

90%

$71,428

Strong

80%

Corrupt

10%

–$300,000

Weak

20%

Not corrupt

90%

–$114,286

Weak

20%

Corrupt

10%

–$300,000

Country Risk Analysis ❖ 13

Scenario

Joint probability

NPV

Strong/Not corrupt

80% × 90% = 72%

$71,428

Strong/Corrupt

80% × 10% = 8%

–$300,000

Weak/Not corrupt

20% × 90% = 18%

–$114,286

Weak/Corrupt

20% × 10% = 2%

–$300,000

Expected Value of NPV = (72% × $71,428) + (8% × –$300,000) + 18% (–$114,286)

+ 2% (–$300,000) = ($51,428) + (–$24,000) + (–$20,571) + (–$6,000) = –$857.

There is a 28% chance that the project’s NPV will be negative.

23. Capital Budgeting and Country Risk. Wyoming Co. is a non-profit educational institution that

wants to import educational software products from Hong Kong and sell them in the U.S. It wants to

assess the net present value of this project since any profits it earns will be used for its foundation. It

expects to pay HK$5 million for the imports. Assume the existing exchange rate is HK$1 =$.12. It

would also incur selling expenses of $1 million to sell the products in the U.S. The company would

be able to sell the products in the U.S. for $1.7 million. However, it is concerned about two forms of

country risk. First, there is a 60% chance that the Hong Kong dollar will be revalued to be worth

HK$1 = $.16 by the Hong Kong government. Second, there is a 70% chance that the Hong Kong

government imposes a special tax of 10% on the amount that U.S. importers must pay for Hong Kong

exports. These two forms of country risk are independent, meaning that the probability that the Hong

Kong dollar will be revalued is independent of the probability that the Hong Kong government will

impose a special tax. Wyoming’s required rate of return on this project is 22%. What is the expected

value of the project’s net present value? What is the probability that the project’s NPV will be

negative?

ANSWER:

Scenario 1:

No tax or

exchange rate

adjustment

Scenario 2:

10% tax

Scenario 3:

exchange rate

adjustment

Scenario 4:

10% tax and

exchange rate

adjustment

Revenue

$1,700,000

$1,700,000

$1,700,000

$1,700,000

Import Cost (in HKD)

5,000,000

5,500,000

5,000,000

5,500,000

Exchange Rate

$0.12

$0.12

$0.16

$0.16

Import Cost in $

$600,000

$660,000

$800,000

$880,000

Gross Profit

$1,100,000

$1,040,000

$900,000

$820,000

Selling expense

$1,000,000

$1,000,000

$1,000,000

$1,000,000

Cash flow

$100,000

$40,000

-$100,000

-$180,000

NPV

$81,967

$32,787

-$81,967

-$147,541

24. Accounting for Country Risk of a Project. Kansas Co. wants to invest in a project in China, The

proposed project would require an initial investment of 5,000,000 yuan, but is expected to generate

Country Risk Analysis ❖ 14

cash flows of 7,000,000 yuan at the end of one year. The spot rate of the yuan is $.12, and Kansas

thinks this exchange rate is the best forecast of the future. However, there are 2 forms of country risk.

First, there is a 30% chance that the Chinese government will require that the yuan cash flows earned

by Kansas at the end of one year be reinvested in China for one year before it can be remitted (so that

cash would not be remitted until 2 years from today). In this case, Kansas would earn 4% after taxes

on a bank deposit in China during that second year.

Second, there is a 40% chance that the Chinese government will impose a special remittance tax of

400,000 yuan at the time that Kansas Co. remits cash flows earned in China back to the U.S.

The two forms of country risk are independent. The required rate of return on this project is 26%.

There is no salvage value. What is the expected value of the project’s net present value?

ANSWER:

30%

40%

Scenario 1

Scenario 2

Scenario 3

Scenario 4

No country

risk

Remittance

must be

invested for

1 year

400,000

Yuan

remittance

Tax

Both

country

risks

Yuan remitted by subsidiary

7,000,000

7,000,000

7,000,000

7,000,000

Withholding Tax

NA

NA

400,000

400,000

Interest Rate

NA

0.04

NA

0.04

Yuan after Interest Earned

NA

7280000

NA

7280000

Yuan remitted after taxes

NA

NA

6,600,000

6,880,000

Exchange Rate of yuan

$0.12

$0.12

$0.12

$0.12

Cash flow to parent

$840,000.00

$873,600.00

$792,000.00

$825,600.00

PV of parent cash flow (26%)

$666,666.67

$550,264.55

$628,571.43

$520,030.23

Initial Investment in US$

-$600,000.00

-$600,000.00

-$600,000.00

-$600,000.00

NPV

$66,666.67

-$49,735.45

$28,571.43

-$79,969.77

NPV

Probability

Probability

NPV x

Probability

Scenario 1

$66,666.67

70% * 60%

0.42

$28,000.00

Scenario 2

-$49,735.45

30% * 60%

0.18

-$8,952.38

Scenario 3

$28,571.43

70% * 40%

0.28

$8,000.00

Scenario 4

-$79,969.77

30% * 40%

0.12

-$9,596.37

NPV=$17,451

25. Accounting for Country Risk of Projects. Slidell Co. (a U.S. firm) considers a foreign project in

which it expects to receive 10 million euros at the end of this year. It plans to hedge receivables of 10

million euros with a forward contract. Today, the spot rate of the euro is $1.20, the one-year forward

rate of the euro is presently $1.24, and the expected spot rate of the euro in one year is $1.19. The

initial outlay is $7 million. Slidell has a required return of 18%.

Country Risk Analysis ❖ 15

There is a 20% chance that political problems will cause a reduction in foreign business, such that

Slidell would only receive only 4 million euros at the end of one year. Determine the expected value

of the net present value of this project.

ANSWER:

Normal conditions

26. Political Risk and Currency Derivative Values. Assume that interest rate parity exists. At 10:30

a.m., the media reported news that the Mexican government political problems had been solved,

which reduced the expected volatility of the Mexican peso against the dollar over the next month.

However, this news had no effect on the prevailing one-month interest rates of the U.S. dollar or

Mexican peso, and also had no effect on the expected exchange rate of the Mexican peso in one

month. The spot rate of the Mexican peso was $.13 as of 10 a.m. and remained at that level all

morning.

a. At 10 a.m., Piazza Co. purchased a call option at the money on 1 million Mexican pesos with a

December expiration date. At 11:00 a.m., Corradetti Co. purchased a call option at the money on

1 million pesos with a December expiration date. Did Corradetti Co. pay more than, less than, or

the same as Piazza Co. for the options? Briefly explain.

b. Teke Co. purchased futures contracts on 1 million Mexican pesos with a December settlement

date at 10 a.m. Malone Co. purchased futures contracts on 1 million Mexican pesos with a

December settlement date at 11 a.m. Did Teke Co. pay more than, less than, or the same as

Malone Co. for the futures contracts. Briefly explain.

ANSWER:

27. Political Risk and Project NPV. Drysdale Co. (a U.S. firm) is considering a new project that

would result in cash flows of 5 million Argentine pesos in one year under the most likely economic

and political conditions. The spot rate of the Argentina peso in one year is expected to be $.40 based

on these conditions. However, Drysdale also wants to also account for the 10% probability of a

political crisis in Argentina, which would change the expected cash flows to 4 million Argentine

pesos in one year. In addition, it wants to account for the 20% probability that the exchange rate may

Country Risk Analysis ❖ 16

be only $.36 at the end of one year. These two forms of country risk are independent. Drysdale’s

required rate of return is 25% and its initial outlay for this project is $1.4 million. Show the

distribution of possible outcomes for the project’s net present value (NPV).

ANSWER:

Scenario

Probability

NPV of Cash flows

Most likely conditions

68%

(5 million x $.40)/1.25 – $1.4 million = $200,000

Political crisis

10%

(4 million x $.40)/1.25 – $1.4 million = -$12,000

Weak exchange rate

20%

(5 million x $.36)/1.25 – $1.4 million = $40,000

Political crisis and

weak exchange rate

2%

(4 million x $.36)/1.25 – $1.4 million = -$248.000

28. Country Risk and Project NPV. Atro Co. (a U.S. firm) considers a foreign project in which it

expects to receive 10 million euros at the end of one year. While it realizes that its receivables are

uncertain, it decides to hedge receivables of 10 million euros with a forward contract today. As of

today, the spot rate of the euro is $1.20, while the one-year forward rate of the euro is presently $1.24,

and the expected spot rate of the euro in one year is $1.19. The initial outlay of this project is $7

million. Atro has a required return of 18%.

a. Estimate the NPV of this project based on the expectation of 10 million euros in receivables.

b. Now estimate the NPV based on the possibility that country risk could cause a reduction in

foreign business, such that Atro Co. only receives only 4 million euros instead of 10 million euros

at the end of one year. Estimate the net present value of the project if this form of country risk

occurs.

ANSWER:

a. Using forward rate after 1 year: euros 10,000,000 x $1.24 = $12,400,000

29. Accounting for Political Risk and the Hedging Decision.

a. Duv Co. (a U.S. firm) is planning to invest $2.5 million in a project in Portugal that will exist for

one year. Its required rate of return on this project is 18%. It expects to receive cash flows of 2

million euros in one year from this project. The spot rate of the euro in one year is expected to be

$1.50, and the one-year forward rate of the euro is presently $1.40. Duv Co. also wants to account

also for the 20% probability of a crisis in Portugal. If this crisis occurs, Duv’s expected cash

flows would decrease to 1 million euros in one year. Duv does not plan to hedge its expected cash

flows. Show the distribution of possible outcomes for the project’s estimated net present value

(NPV), including the probability of each possible outcome.

ANSWER:

Country Risk Analysis ❖ 17

Scenario

Probability

NPV of Cash flows

No Crisis: Cash flows

of 2 million euros

80%

(2 million euros x $1.50)/1.18 – $2,500,000 =

$42,373

Crisis: Cash flows of 1

million euros

20%

(1 million euros x $1.50)/1.18 – $2,500,000 =

-$1,228,813

b. Now assume that Duv plans to hedge the cash flows that it believes it will receive if a crisis in

Portugal occurs. However, it decides not to hedge additional cash flows that it would receive if

the crisis does not occur. Estimate what the net present value (NPV) of the project will be based

on the hedging strategy described here, and assuming that a crisis in Portugal does not occur.

ANSWER:

Cash flows (hedged): 1,000,000 euros × $1.40 = $1,400,000.

CRITICAL THINKING

Recognizing Exposure to Country Risk Select a U.S.-based MNC (such as ExxonMobil or

Coca-Cola) that does considerable business in Russia. Write a short essay describing the

MNC’s business in Russia and how its cash flows are exposed to country risk due to the

tensions between the United States and Russia.

ANSWER

The question is intended to allow students to learn about a practical example of how country risk has to be

assessed over a long-term period, is difficult to predict far in advance, and can reduce cash flows. A

review of the MNC’s situation will likely reveal that the revenue and therefore cash inflows due to sales

by MNCs in Russia may been reduced when tensions are high between countries.

Solution to Continuing Case Problem: Blades, Inc.

1. Based on the information provided in the case, do you think the political risk associated with Thailand

is higher or lower for a manufacturer of leisure products such as Blades as opposed to, say, a food

producer? That is, conduct a micro-assessment of political risk for Blades, Inc.

2. Do you think the financial risk associated with Thailand is higher or lower for a manufacturer of

leisure products such as Blades as opposed to, say, a food producer? That is, conduct a micro-

assessment of financial risk for Blades, Inc. Do you think a leisure product manufacturer such as

Blades will be more affected by political or financial risk factors?

Country Risk Analysis ❖ 18

ANSWER: The level of financial risk in Thailand is higher for a manufacturer of leisure products

such as Blades, Inc. This is because consumers will first eliminate purchases of these types of

3. Without using a numerical analysis, do you think establishing a subsidiary in Thailand or acquiring

Skates’n’Stuff will result in a higher assessment of political risk? Of financial risk? Substantiate your

answer.

ANSWER: Establishing a subsidiary in Thailand will probably result in a higher level of political risk

than acquiring Skates’n’Stuff. Asian consumers prefer to purchase from Asian producers. If Blades

4. Using a spreadsheet, conduct a quantitative country risk analysis for Blades, Inc., based on the

information that Ben Holt has provided for you. Use your judgment to assign weights and ratings to

each political and financial risk factor and determine an overall country risk rating for Thailand.

Conduct two separate analyses for (a) the establishment of a subsidiary in Thailand and (b) the

acquisition of Skates’n’Stuff.

ANSWER: (See spreadsheet below.) There is no one correct answer to this question. The estimates

provided in the attached spreadsheet are somewhat arbitrary, but students should at least use the

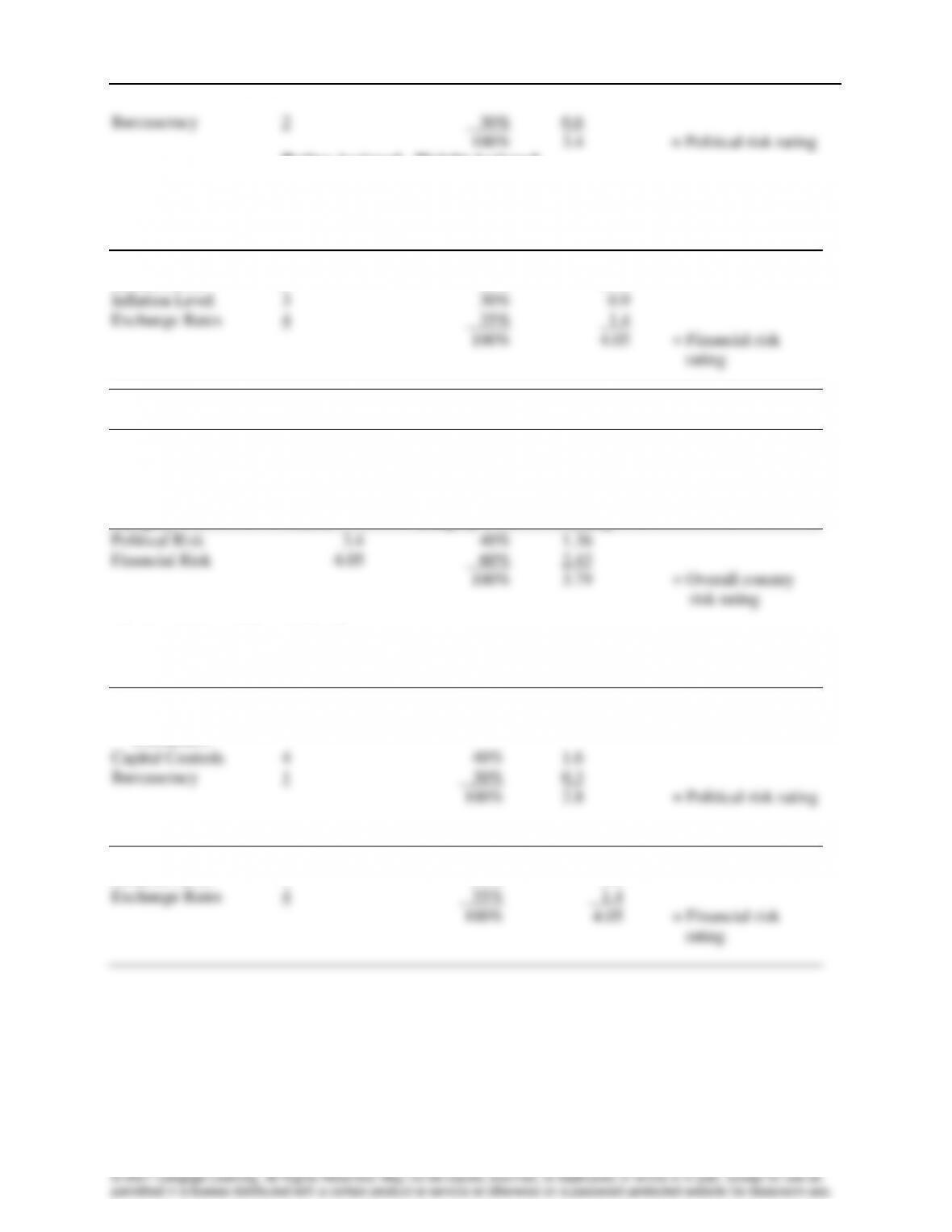

(1) Establishment of a Subsidiary in Thailand

(1)

(2)

(3)

(4) = (2) × (3)

Rating Assigned

Weight Assigned

by Blades to

by Blades to

Weighted

Factor (within a

Factor According

Value

Political Risk Factor

range of 1-5)

to Importance

of Factor

Attitude of Thai

Consumers

4

30%

1.2

Capital Controls

4

40%

1.6

Country Risk Analysis ❖ 19

Bureaucracy

2

30%

0.6

100%

3.4

= Political risk rating

Rating Assigned

Weight Assigned

by Blades to

by Blades to

Weighted

Factor (within a

Factor According

Value

Political Risk Factor

range of 1-5)

to Importance

of Factor

Financial Risk Factor

Interest Rates

5

35%

1.75

Inflation Level

3

30%

0.9

Exchange Rates

4

35%

1.4

100%

4.05

= Financial risk

rating

(1)

(2)

(3)

(4) = (2) × (3)

Weight Assigned

Rating as

by Blades to

Category

Determined

Above

Each Risk

Category

Weighted

Rating

Political Risk

3.4

40%

1.36

Financial Risk

4.05

60%

2.43

100%

3.79

= Overall country

risk rating

(2) Acquisition of Skates’n’Stuff

(1)

(2)

(3)

(4) = (2) × (3)

Attitude of Thai

Consumers

3

30%

0.9

Capital Controls

4

40%

1.6

Bureaucracy

1

30%

0.3

100%

2.8

= Political risk rating

Financial Risk Factor

Interest Rates

5

35%

1.75

Inflation Level

3

30%

0.9

Exchange Rates

4

35%

1.4

100%

4.05

= Financial risk

rating