Chapter 15

International Capital Budgeting

QUESTIONS

1. Can an investment project of a foreign subsidiary that has a positive net present value when

evaluated as a stand-alone firm ever be rejected by the parent corporation? Assume that the

parent accepts all projects with positive adjusted net present values.

2. How do licensing agreements, royalties, and overhead allocation fees affect the value of a

foreign project?

3. Why does an adjusted net present value analysis treat the present value of financial side effects

as a separate item? Isn’t interest expense a legitimate cost of doing business?

Answer: The adjusted net present value approach to capital budgeting starts by valuing the free cash

flows to the all-equity cash firm. It then adds other sources of value associated with how the firm is

financed. As in the weighted average cost of capital (WACC) approach in Chapter 16, the numerator

©2017 Cambridge University Press

4. What is meant by the net present value of the financial side effects of a project?

5. Why is it costly to issue securities?

6. What is an interest tax shield? How do you calculate its value?

( ) ( ) ( )

23

DDD

1 + r 1 + r 1 + r

7. What is an interest subsidy? How do you calculate its value?

Answer: Interest subsidies arise when governments are willing to lend to corporations at below

market interest rates. Such subsidies add value to a project. The appropriate discount rate for an

interest subsidy is the market’s required rate of return on the debt of the corporation because the

©2017 Cambridge University Press

8. What are growth options? Provide an example of one in an international context.

9. What is the difference between EBIT and NOPLAT?

10. Why is it important to understand and manage net working capital?

11. What does CAPX mean, and why is it a firm’s engine of growth?

12. Why is it sometimes assumed that CAPX equals depreciation in the later stages of a project?

How does expected inflation affect this assumption?

©2017 Cambridge University Press

17. What risks are present in the IWPI-Spain project? How do they affect the value of the project?

Answer: The primary source of risk is the business risk of selling wooden furniture in Europe. The

PROBLEMS

1. What percentage of the adjusted net present value of the IWPI-Spain project arises from the

dividends that will occur more than 10 years in the future?

2. How sensitive is the value of IWPI-Spain to the assumed discount rate of 11.10%? What

happens to the value of the project if the rate is 12.1% instead?

Answer: When the project was discounted with 11.1%, upon adding together all the costs and benefits

of the project, we found

ANPV of IWPI-Spain = – €178.66 million in initial costs

Chapter 15: International Capital Budgeting

6

3. What would be the terminal values of the dividends from IWPI-Spain if they were expected to

grow in real terms at 1% rather than 0%?

4. How much does the value of IWPI-Spain, viewed as a stand-alone firm, change if the royalty fee

is increased by 1% and the overhead allocation fee is reduced by 1%? What is the change in

value to IWPI-U.S.? What is the source of this change in value?

5. Valuing Metallwerke’s Contract with Safe Air, Inc.

Consider the discounted expected value of the 10-year contract that Metallwerke may sign with

Safe Air in Chapter 9. In the initial year of the deal, Metallwerke sells an air tank to Safe Air

for $400. It costs

€

238 to produce an air tank. The current exchange rate is $1.40/

€

. Assume

that 15,000 air tanks will be sold the first year. Make the following other assumptions in your

valuation:

a. The demand for air tanks is expected to grow at 5% for the second year, 4% for the third

and fourth years, and 3% for the remaining life of the contract.

b. Euro-denominated costs are expected to increase at the euro rate of inflation of 2%.

c. The base dollar price of the air tank will be increased at the U.S. rate of inflation plus one-

half of any real depreciation of the dollar relative to the euro, but the base dollar price will

be reduced by one-half of any appreciation of the dollar relative to the euro. The U.S. rate

of inflation is expected to be 4%.

d. The dollar is currently not expected to strengthen or weaken in real terms relative to the

euro.

e. The German corporate income tax rate is 30%.

f. The appropriate euro discount rate for the project is 12%.

Chapter 15: International Capital Budgeting

7

g. Metallwerke typically establishes an account receivable for its customers. At any given time,

the stock of the account receivable is expected to equal 10% of a given year’s revenue.

h. Accepting the Safe Air project will not require any major capital expenditures by

Metallwerke.

Can you determine the value of the contract to Metallwerke?

Answer: The value of the project can be determined by discounting the expected incremental free

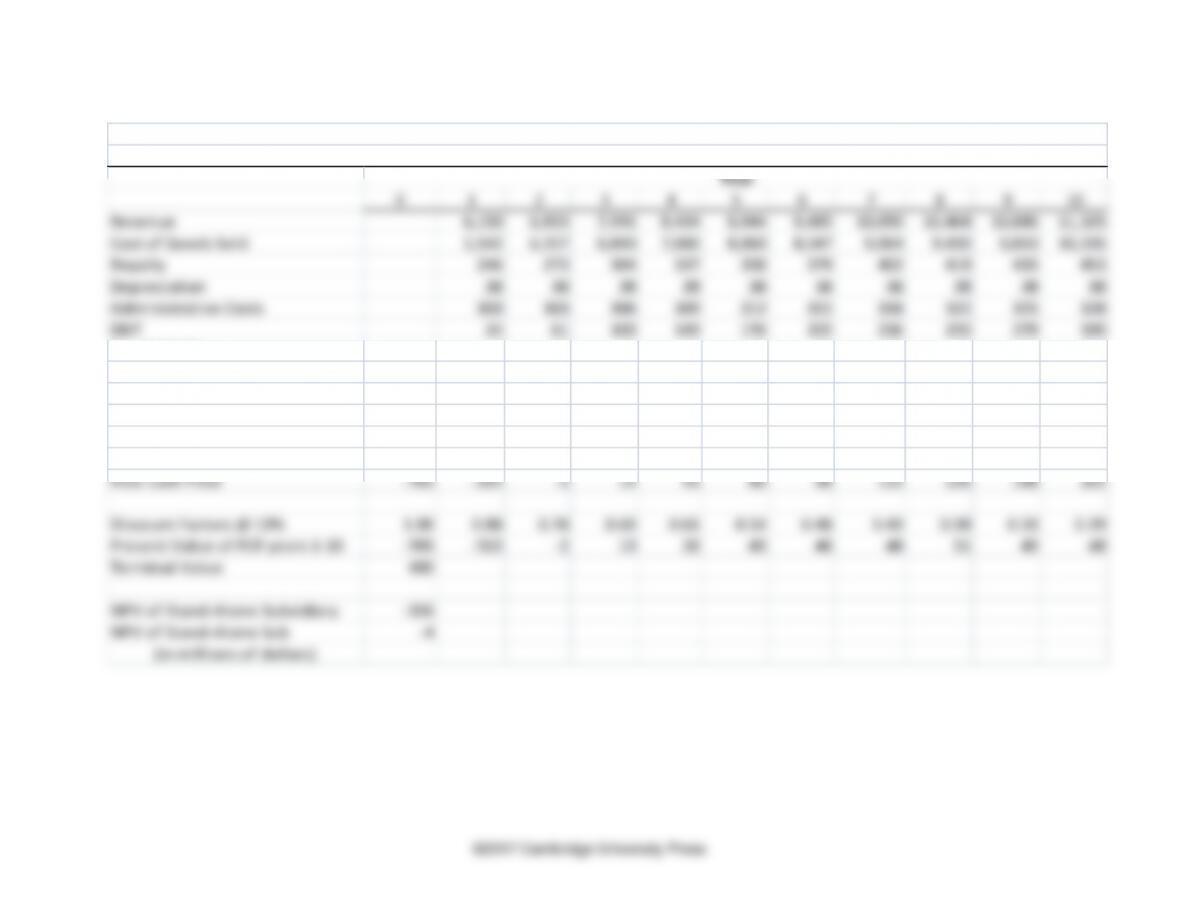

Valuing Metallwerke’s 10-year Contract with Safe Air

Year

01 2 3 4 5 6 7 8 9 10

US Inflation 4% 4% 4% 4% 4% 4% 4% 4% 4% 4%

Euro Inflation 2% 2% 2% 2% 2% 2% 2% 2% 2% 2%

Dollars per euro 1.4000 1.4275 1.4554 1.4840 1.5131 1.5427 1.5730 1.6038 1.6353 1.6673 1.7000

Retail Price per tank (dollars) 400 416 433 450 468 487 506 526 547 569

Cost per tank (euros) 238 243 248 253 258 263 268 273 279 284

Growth in demand 5% 4% 4% 3% 3% 3% 3% 3% 3%

tanks sold 15,000 15,750 16,380 17,035 17,546 18,073 18,615 19,173 19,748 20,341

All cash flows below are in euros

Revenue 4,203,297 4,501,731 4,775,436 5,065,783 5,322,111 5,591,410 5,874,335 6,171,577 6,483,858 6,811,942

Cost of goods sold 3,570,000 3,823,470 4,055,937 4,302,538 4,520,246 4,748,971 4,989,269 5,241,726 5,506,957 5,785,609

EBIT 633,297 678,261 719,499 763,245 801,865 842,439 885,067 929,851 976,901 1,026,333

NOPLAT @ 30% tax 443,308 474,783 503,649 534,271 561,305 589,707 619,547 650,896 683,831 718,433

Working Capital 420,330 450,173 477,544 506,578 532,211 559,141 587,434 617,158 648,386 681,194

Change in Working Capital 420,330 29,843 27,371 29,035 25,633 26,930 28,293 29,724 31,228 32,808

The first lines establish the background data. U.S. inflation is forecast to be 4% and German

inflation is forecast to be 2%. The real exchange rate is forecast to be constant, so the nominal

dollar/euro exchange rate is forecast to satisfy relative PPP. The first year nominal exchange rate

The first year retail price is set at $400, and it is assumed to grow at the U.S. rate of inflation

because there are no forecasts of real appreciation or real depreciation of the dollar. The first year

6. Deli-Delights Inc.

Deli-Delights Inc. is a U.S. company that is considering expanding its operations into Japan.

The company supplies processed foods to storefront delicatessens in large cities. This requires

Deli-Delights to have a centralized production and warehousing facility in each of these cities.

Deli-Delights has located a possible site for a Japanese subsidiary in Tokyo. The cost to

purchase and equip the facility is ¥765,000,000. Perform an ANPV analysis to determine

whether this is a good investment, under the following assumptions:

a. The average per-unit sales price will initially be ¥410.

b. First-year sales will be 15 million units, and physical sales will then grow at 10%

per annum for the next 3 years, 5% per annum for the 3 years after that, and

then stabilize at 3% per annum for the indefinite future.

c. First-year variable costs of production will be ¥225 per unit of labor and $1.75

per unit of imported semi-finished goods. Administrative costs will be ¥300

million.

d. Depreciation will be taken on a straight-line basis over 20 years.

e. Retail prices, labor costs, and administrative expenses are expected to rise at the

Japanese yen rate of inflation, which is forecast to be 1%. Dollar prices of semi–

finished goods are expected to rise at the U.S. dollar rate of inflation, which is

expected to be 4%.

f. The yen/dollar exchange rate is currently ¥85/$, and the yen is expected to

appreciate at a rate justified by the expected inflation differential between the

yen and dollar rates of inflation.

Chapter 15: International Capital Budgeting

10

g. There will be a 4% royalty paid by the Japanese subsidiary to its U.S. parent.

h. The Japanese corporate income tax rate is 37.5%, and there is a 10%

withholding tax on dividends and royalty payments.

i. The yen-denominated equity discount rate for the project is 13%.

j. Net working capital will average 6% of total sales revenue.

k. Capital expenditures will offset depreciation.

l. All of the Japanese subsidiary’s free cash flow will be paid to the parent as

dividends.

m. The corporate income tax rate for the United States is 34%.

n. Deli-Delights Inc. has sufficient other foreign income that will allow it to fully

utilize any excess foreign tax credits generated by its Japanese subsidiary.

o. Deli-Delights Inc. does not plan to issue any debt associated with this project.

Answer: The solution is presented in the following spread sheet pages. The first lays out the facts.

Inflation is expected to be 4% in the United States and 1% in Japan. The current exchange rate is

¥85/$ and is expected to satisfy relative purchasing power parity in which case the yen is expected to

Chapter 15: International Capital Budgeting

11

0 1 2 3 4 5 6 7 8 9 10

USD Inflation 4% 4% 4% 4% 4% 4% 4% 4% 4% 4%

JPY Inflation 1% 1% 1% 1% 1% 1% 1% 1% 1% 1%

Yen per Dollar 85.00 82.55 80.17 77.85 75.61 73.43 71.31 69.25 67.25 65.31 63.43

Retail Price (yen) 410 414 418 422 427 431 435 440 444 448

Growth in Unit Sales 10% 10% 10% 5% 5% 5% 3% 3% 3%

Unit Sales (millions) 15.00 16.50 18.15 19.97 20.96 22.01 23.11 23.81 24.52 25.26

Labor Cost per unit (yen) 225 227 230 232 234 236 239 241 244 246

Total Labor Costs (millions of yen) 3,375 3,750 4,166 4,628 4,908 5,205 5,520 5,743 5,974 6,215

Import Part Cost (dollars) 1.75 1.82 1.89 1.97 2.05 2.13 2.21 2.30 2.39 2.49

Import Part Cost (yen) 144.46 145.90 147.36 148.84 150.32 151.83 153.35 154.88 156.43 157.99

Total Part Cost (millions of yen) 2,167 2,407 2,675 2,972 3,151 3,342 3,544 3,687 3,836 3,990

Valuing Deli-Delights Japanese Subsidiary as a Stand-Alone Firm: Basic Data

Year

Chapter 15: International Capital Budgeting

13

0 1 2 3 4 5 6 7 8 9 10

Revenue 6,150 6,833 7,591 8,434 8,944 9,485 10,059 10,464 10,886 11,325

Cost of Goods Sold 5,542 6,157 6,840 7,600 8,060 8,547 9,064 9,430 9,810 10,205

Royalty 246 273 304 337 358 379 402 419 435 453

Depreciation 38 38 38 38 38 38 38 38 38 38

Administrative Costs 300 303 306 309 312 315 318 322 325 328

EBIT 24 61 103 149 176 205 236 256 278 300

Tax @ 37.5% 9 23 39 56 66 77 88 96 104 113

NOPLAT 15 38 64 93 110 128 147 160 174 188

Working Capital 369 410 455 506 537 569 604 628 653 679

Change in Working Capital 369 41 46 51 31 32 34 24 25 26

NPV of Stand-Alone Subsidiary –356

NPV of Stand-Alone Sub -4

(in millions of dollars)

Valuing Deli–Delights Japanese Subsidiary as a Stand-Alone Firm: The Cash Flows

(all cash flows are in millions of yen)

Year

Chapter 15: International Capital Budgeting

14

0 1 2 3 4 5 6 7 8 9 10

Required Investments –765 –354 -3 0 0 0 0 0 0 0 0

Dividends Declared 0 0 0 19 43 80 96 113 136 148 161

Withholding Tax @ 10% 0 0 0 2 4 8 10 11 14 15 16

Dividends Received Net of Tax 0 0 0 17 38 72 86 102 122 134 145

Deemed Paid Tax Credit 11 26 48 57 68 81 89 97

Foreign Tax Credit 0 0 0 13 30 56 67 79 95 104 113

Grossed-Up Dividend 0 0 0 30 68 127 153 180 217 237 258

Potential U.S. Tax @ 34% 0 0 0 10 23 43 52 61 74 81 88

Actual U.S. Tax 0 0 0 0 0 0 0 0 0 0 0

After-Tax Dividends 0 0 0 17 38 72 86 102 122 134 145

Discount Factors @ 13% 1.00 0.88 0.78 0.69 0.61 0.54 0.48 0.43 0.38 0.33 0.29

PV of Dividends and Investments –765 –313 -2 12 24 39 41 43 46 44 43

Terminal Value of Dividends 106

Sum of PV Divs and CAPX –683

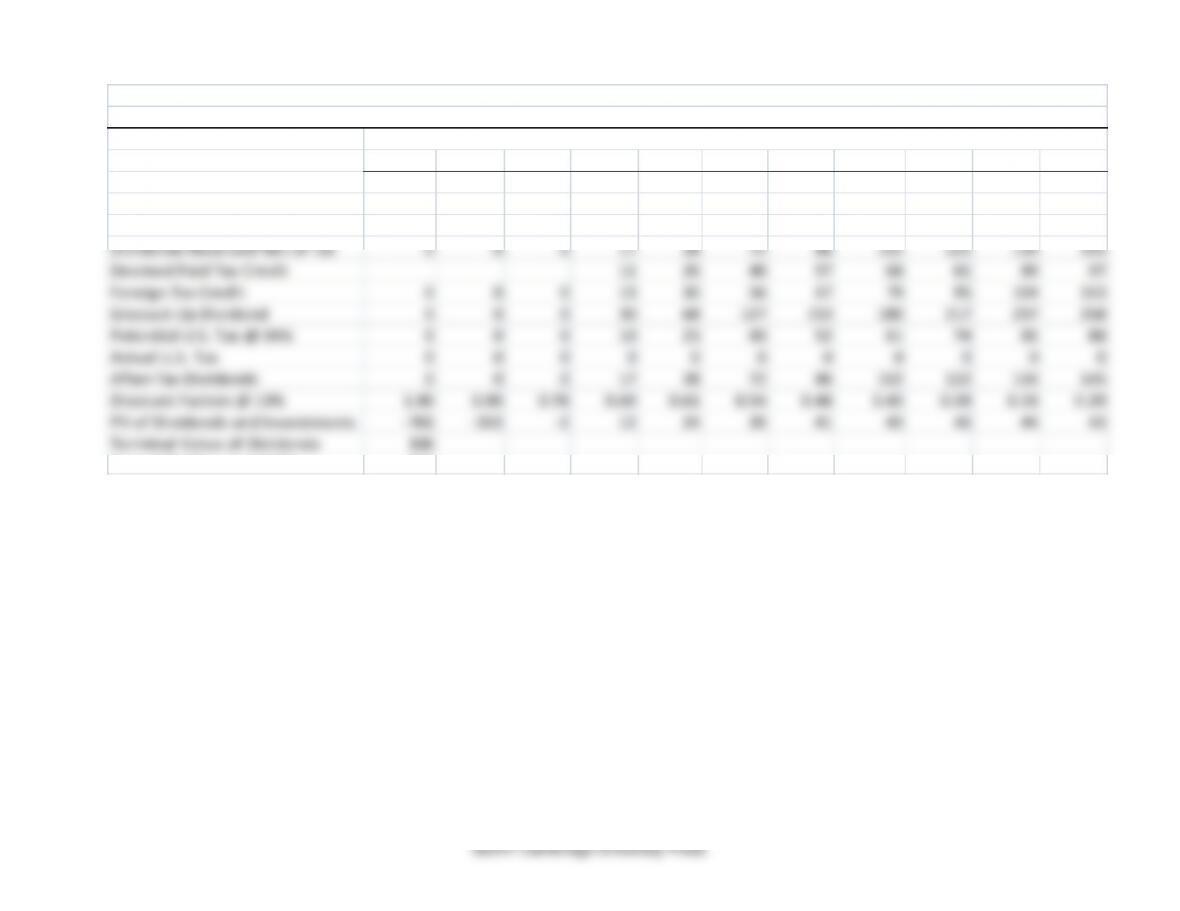

Valuing Deli–Delights Japanese Subsidiary: The Parent Perspective

(all cash flows are in millions of yen)

Year

Chapter 15: International Capital Budgeting

15

0 1 2 3 4 5 6 7 8 9 10

Royalty Cash Flow 246 273 304 337 358 379 402 419 435 453

Withholding Tax @ 10% 25 27 30 34 36 38 40 42 44 45

Net of Tax Royalty Received 221 246 273 304 322 341 362 377 392 408

Foreign Tax Credit 25 27 30 34 36 38 40 42 44 45

Grossed-Up Royalty 246 273 304 337 358 379 402 419 435 453

Potential U.S. Tax @ 34% 84 93 103 115 122 129 137 142 148 154

Unused Foreign Tax Credit 0 0 3 7 12 15 18 21 23 25

Actual U.S. Tax 59 66 70 74 73 76 79 79 81 84

After-Tax Royalty 162 180 203 229 249 265 283 297 311 324

Discount Factors @ 13% 0.88 0.78 0.69 0.61 0.54 0.48 0.43 0.38 0.33 0.29

PV of Royalty Years 1-10 144 141 141 141 135 127 120 112 103 95

Terminal Value of Royalty 804

NPV Divs, CAPX, Royalty 121

NPV of Subsidiary to Parent 1

(in millions of dollars)

Valuing Deli–Delights Japanese Subsidiary: The Parent Perspective

(all cash flows are in millions of yen)

Year

7. Go to https://abc.xyz/investor/index.html and find Alphabet’s latest annual income

statement. Determine its free cash flow. If you discount its free cash flow as a perpetuity

growing at rate, g, and you discount at 12%, what perpetual growth rate justifies Alphabet’s

current market price?