4 (15) Exchange Rates II: The Asset Approach in the Short Run

Discovering Data In this question we will be testing an assumption of our model of

exchange rate determination. In particular, you will be showing that the PPP assumption

often fails in the short run, emphasizing the importance of the unifying approach

discussed in this chapter. Go to the website of the Federal Reserve Bank of St. Louis

(FRED) at https://research.stlouisfed.org/fred2/ and download annual data for Consumer

Price Indices for the United States, Japan, and Canada as well as the U.S. dollar exchange

rate with the Canadian dollar and Japanese Yen going back to 1971. Put each data series

into a separate column in a new spreadsheet.

a. We will want to check our assumption for relative PPP (that the difference in

inflation each of these countries and the United States should equal the change in the

exchange rate). To do this you must first calculate the percent change in the spot

exchange rate for each year. Do this for both countries with respect to the United States.

In both cases, when did the largest appreciation occur? The largest depreciation?

b. Now check relative PPP as stated in Equation 3-2(14-2) in the last chapter.

Compute the difference in annual rate of inflation in these two pairs of countries (Canada

and the United States, and Japan and the United States) and see if it is equal to the annual

change in the exchange rate for the pair. Create a new column showing the magnitude of

the deviation from relative PPP. Next, compute the mean and standard deviation for each

country pair over the sample period. Are the means what you would expect it to be if PPP

holds in the long run? What is the largest deviation from our PPP assumption?

Answer: Subtracting the change in exchange rates from the difference in inflation

between the country pairs, we find the following values:

US/Japan

• Mean(%E$/¥ – (US – JAP)) = 0.0126

US/Canada

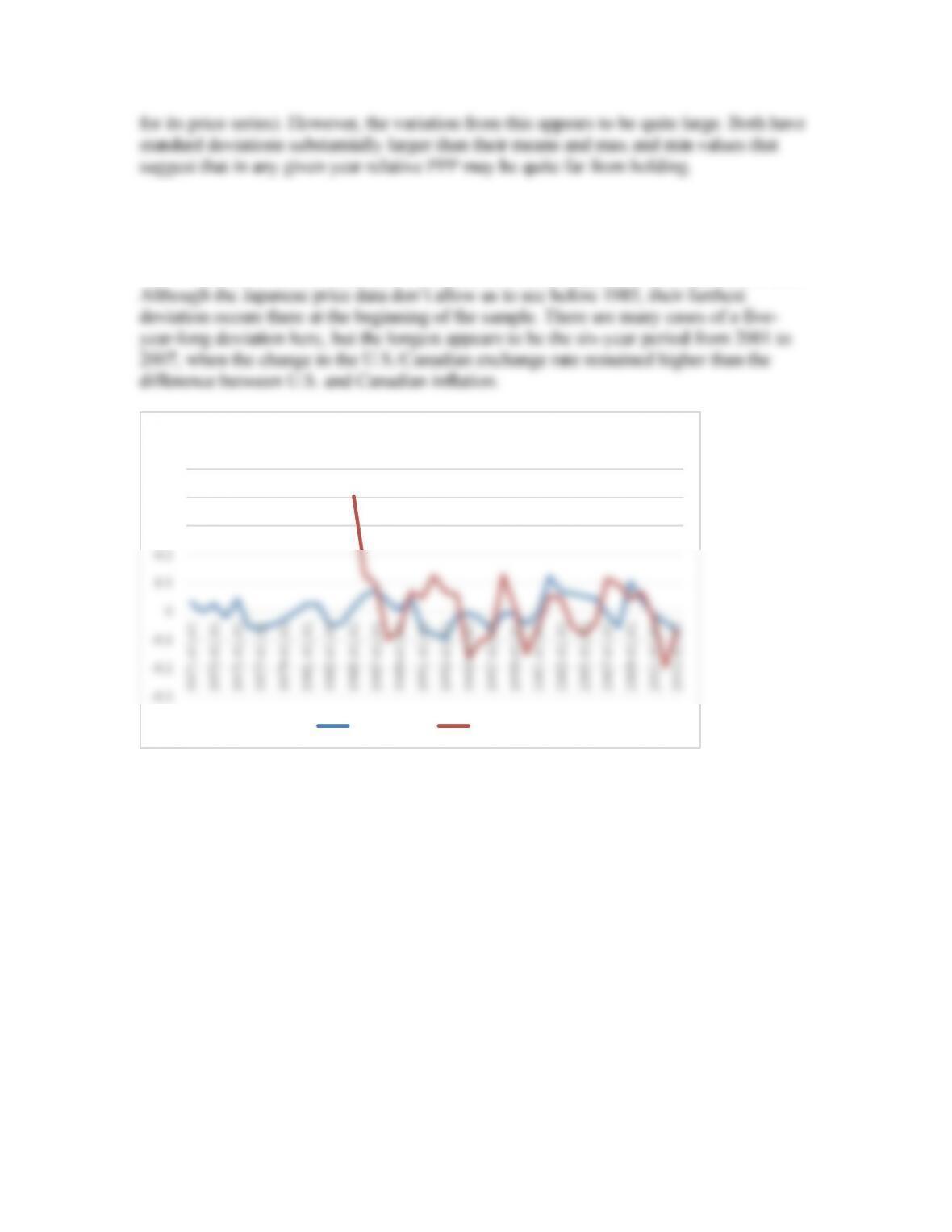

c. Create a line graph showing the deviations from relative PPP plotted against

time in each case. Does it appear that these deviations are trending toward zero over

time? What appears to be the longest time before a deviation from PPP returns to zero?

Answer: See the chart below. Both of these series appear to oscillate around zero.

-0.2

-0.1

0

0.1

0.2

0.3

0.4

0.5

Deviations from Relative PPP

b. Using your diagram from (a), state how each of the following variables changes in

the short run (increase/decrease/no change): U.S. interest rate, British interest rate, E$/£,

Ee$/£, and the U.S. price level P.

c. Using your diagram from (a), state how each of the following variables changes in

the long run (increase/decrease/no change relative to their initial values at point A): U.S.

interest rate, British interest rate, E$/£, Ee$/£, and U.S. price level P.

2. Use the money market and FX diagrams to answer the following questions. This

question considers the relationship between the Indian rupees (Rs) and the U.S. dollar ($).

The exchange rate is in rupees per dollar, ERs/$. On all graphs, label the initial equilibrium

point A.

a. Illustrate how a permanent decrease in India’s money supply affects the money and

FX markets. Label your short-run equilibrium point B and your long-run equilibrium

point C.

b. By plotting them on a chart with time on the horizontal axis, illustrate how each

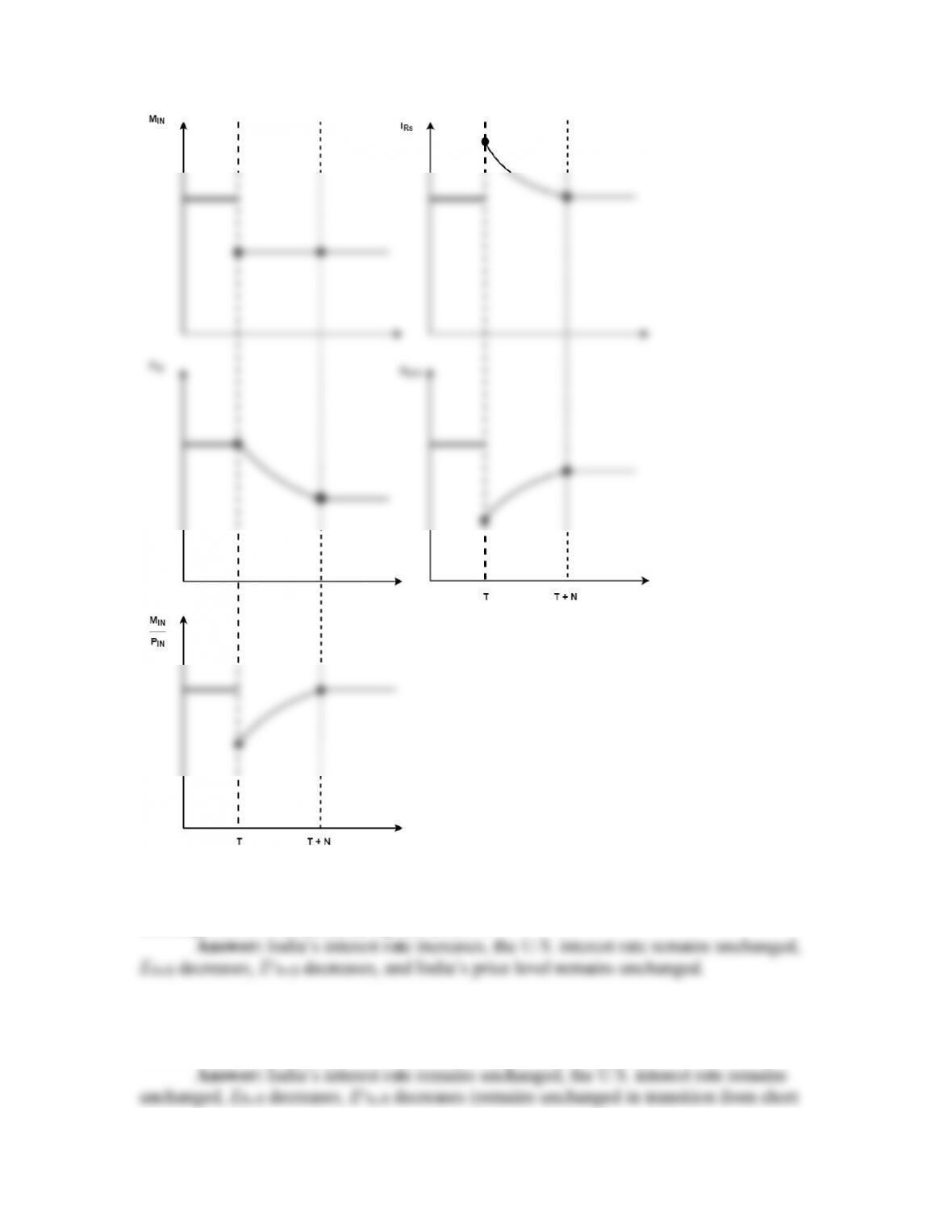

of the following variables changes over time (for India): nominal money supply MIN,

price level PIN, real money supply MIN/PIN, India’s interest rate iRs, and the exchange rate

ERs/$.

c. Using your previous analysis, state how each of the following variables changes

in the short run (increase/decrease/no change): India’s interest rate iRs, ERs/$, expected

exchange rate EeRs/$, and India’s price level PIN.

d. Using your previous analysis, state how each of the following variables changes

in the long run (increase/decrease/no change relative to their initial values at point A):

India’s interest rate iRs, ERs/$, EeRs/$, and India’s price level PIN.

to long run), and India’s price level decreases.

e. Explain how overshooting (in theory and in practice) applies to this situation.

Answer: The short-run exchange rate overshoots its long-run value, EE as in the

3. Is overshooting (in theory and in practice) consistent with purchasing power parity?

Consider the reasons for the usefulness of PPP in the short run versus the long run and

the assumption we’ve used in the asset approach (in the short run versus the long run).

How does overshooting help to resolve the empirical behavior of exchange rates in the

short run versus the long run?

Answer: Yes, overshooting is consistent with PPP. Investors forecast the expected

4. Use the money market and FX diagrams to answer the following questions. This

question considers the relationship between the euro (€) and the U.S. dollar ($). The

exchange rate is in U.S. dollars per euro, E$/€. Suppose that with financial innovation in

the United States, real money demand in the United States decreases. On all graphs, label

the initial equilibrium point A.

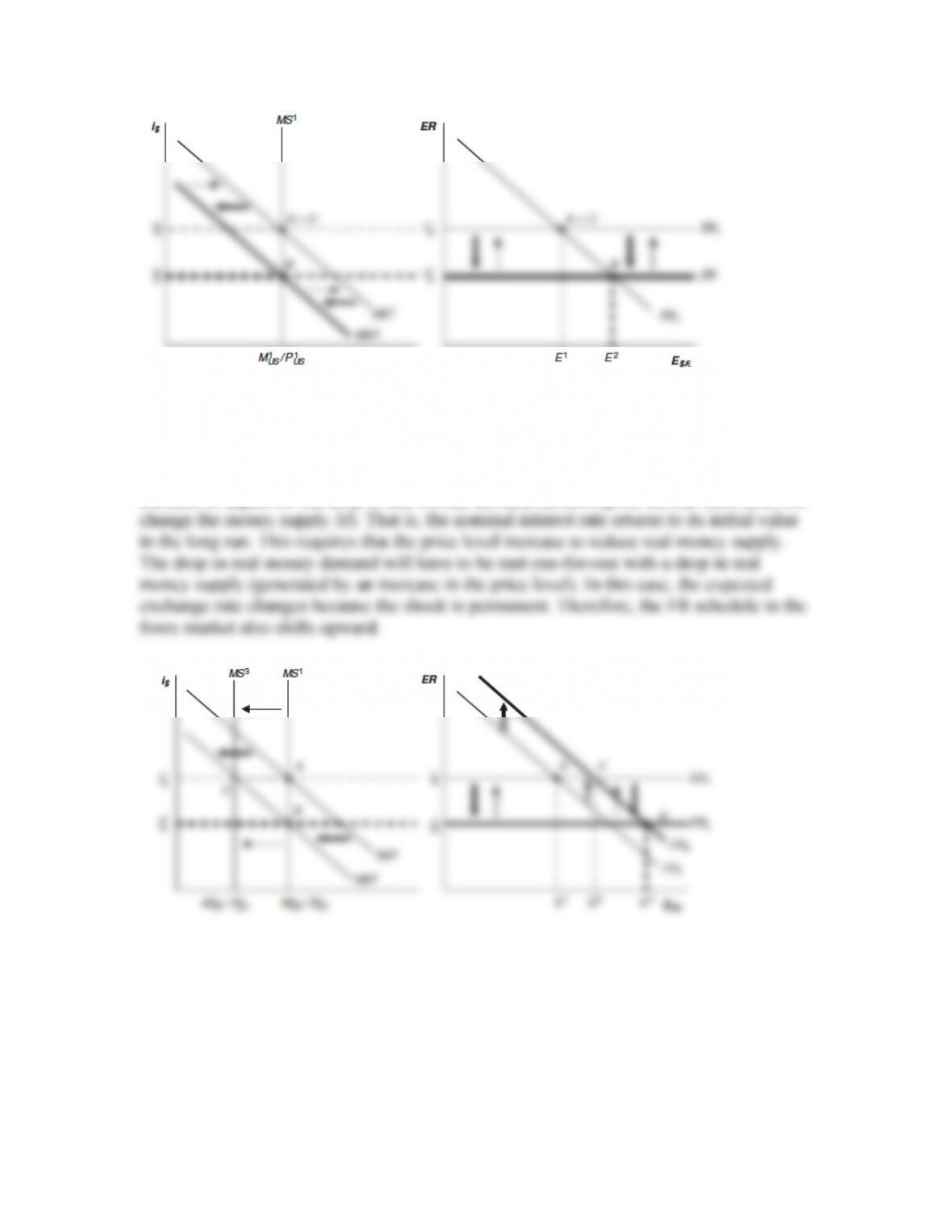

a. Assume this change in U.S. real money demand is temporary. Using the

FX/money market diagrams, illustrate how this change affects the money and FX

markets. Label your short-run equilibrium point B and your long-run equilibrium point C.

Answer: See the following diagram. The long-run values are the same as the

b. Assume this change in U.S. real money demand is permanent. Using a new

diagram, illustrate how this change affects the money and FX markets. Label your short-

run equilibrium point B and your long-run equilibrium point C.

Answer: See the following diagram. In the long run, the price level will have to

increase to adjust for the drop in real money demand (assuming the central bank does not

c. Illustrate how each of the following variables changes over time in response to a

permanent reduction in real money demand: nominal money supply MUS, price level PUS,

real money supply MUS/PUS, U.S. interest rate i$, and the exchange rate E$/€.

Answer: See the following diagrams.

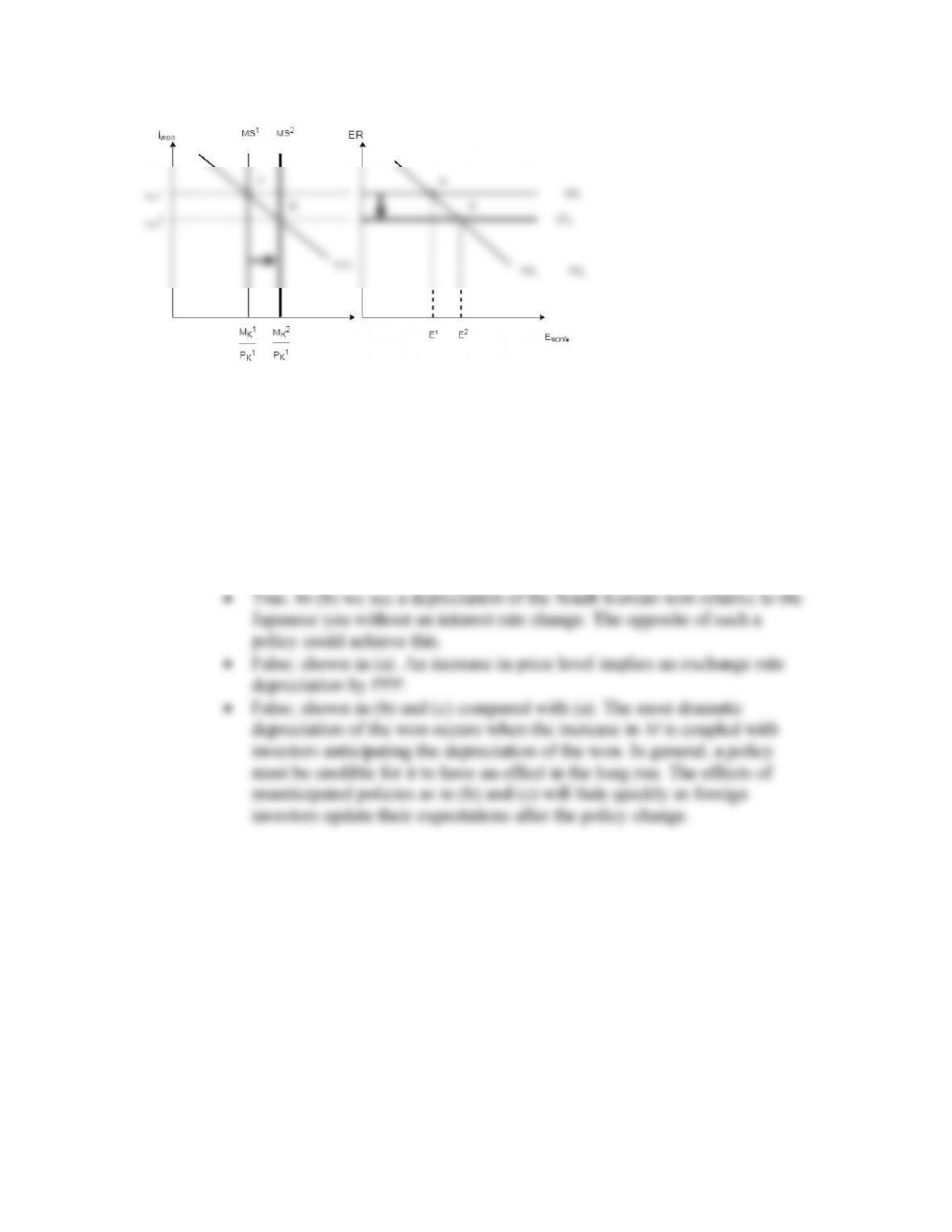

5. This question considers how the FX market will respond to changes in monetary

policy. For these questions, define the exchange rate as South Korean won per Japanese

yen, Ewon/¥. Use the FX and money market diagrams to answer the following questions.

On all graphs, label the initial equilibrium point A.

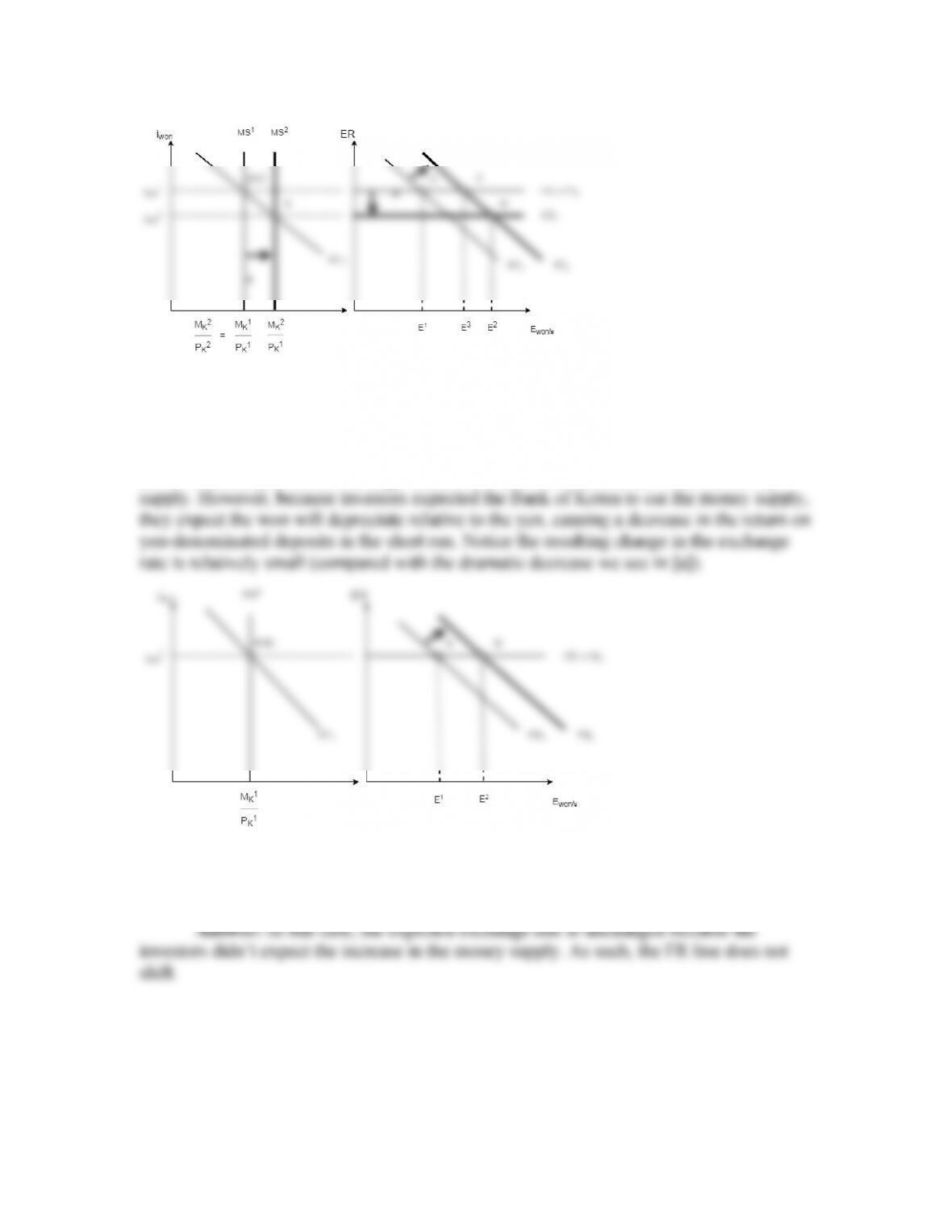

a. Suppose the Bank of Korea permanently increases its money supply. Illustrate the

short-run (label the equilibrium point B) and long-run effects (label the equilibrium point

C) of this policy.

Answer: See the following diagram. In the short run, prices are fixed. Therefore,

b. Now, suppose the Bank of Korea announces it plans to permanently increase its

money supply but doesn’t actually implement this policy. How will this affect the FX

market in the short run if investors believe the Bank of Korea’s announcement?

Answer: See the following diagram. In this case, interest rates on won-

denominated deposits don’t change because the Bank of Korea doesn’t cut the money

c. Finally, suppose the Bank of Korea permanently increases its money supply, but

this change is not anticipated. When the Bank of Korea implements this policy, how will

this affect the FX market in the short run?

d. Using your previous answers, evaluate the following statements:

• If a country wants to decrease the value of its currency, it can do so

(temporarily) without raising domestic interest rates.

• The central bank can increase both the domestic price level and the value

of its currency in the long run.

• The most effective way to decrease the value of a currency is through

surprising investors.

Answer: Though it is theoretically possible, as shown in (b), it is not a good

policy because it is bad for the policy makers’ reputation in the long run.

6. In the late 1990s, several East Asian countries used limited flexibility or currency

pegs in managing their exchange rates relative to the U.S. dollar. This question considers

how different countries responded to the East Asian currency crisis (1997–1998). For the

following questions, treat the East Asian country as the home country and the United

States as the foreign country. Also, for the diagrams, you may assume these countries

maintained a currency peg (fixed rate) relative to the U.S. dollar. Also, for the following

questions, you need consider only the short-run effects.

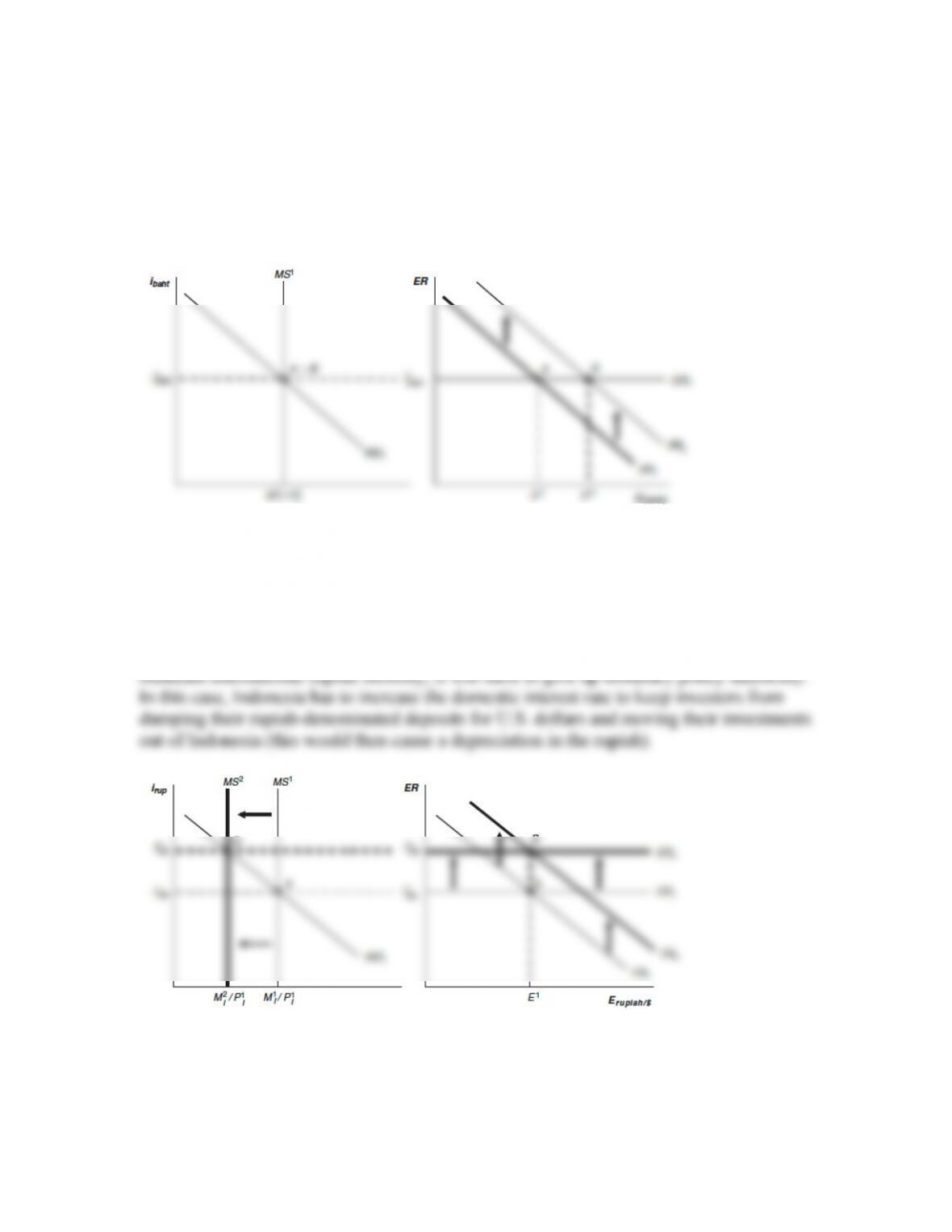

a. In July 1997, investors expected that the Thai baht would depreciate. That is, they

expected that Thailand’s central bank would be unable to maintain the currency peg with

the U.S. dollar. Illustrate how this change in investors’ expectations affects the Thai

money market and the FX market, with the exchange rate defined as baht (B) per U.S.

dollar, denoted EB/$. Assume the Thai central bank wants to maintain capital mobility and

preserve the level of its interest rate, and abandons the currency peg in favor of a floating

exchange rate regime.

Answer: If Thailand is willing to let its currency float against the dollar, then

Thailand’s central bank can maintain monetary policy autonomy and international capital

mobility. See the following diagram:

b. Indonesia faced the same constraints as Thailand—investors feared Indonesia

would be forced to abandon its currency peg. Illustrate how this change in investors’

expectations affects the Indonesian money market and FX market, with the exchange rate

defined as rupiahs (Rp) per U.S. dollar, denoted ERp/$. Assume that the Indonesian central

bank wants to maintain capital mobility and the currency peg.

Answer: If Indonesia wants to maintain the currency peg against the dollar and

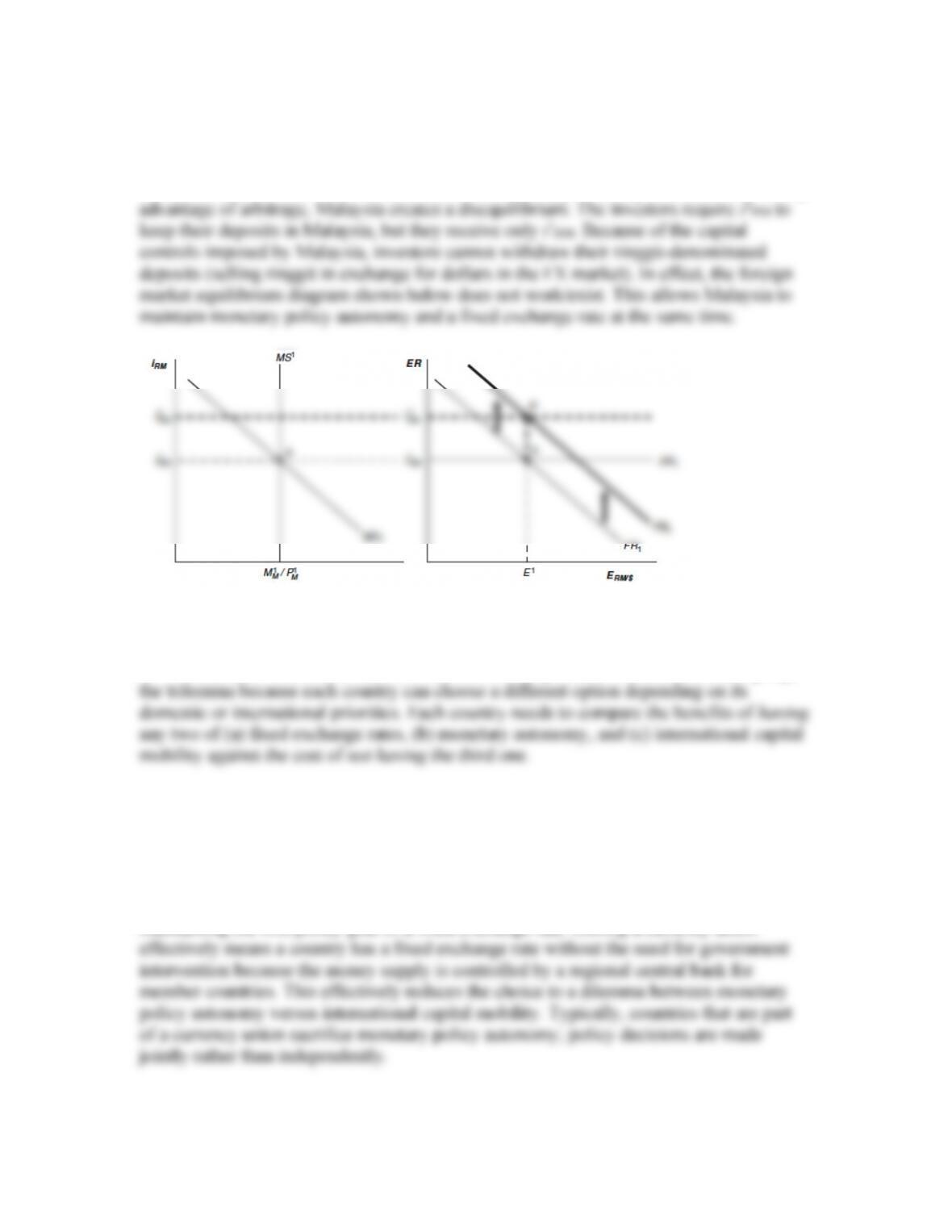

c. Malaysia had a similar experience, except that it used capital controls to maintain

its currency peg and preserve the level of its interest rate. Illustrate how this change in

investors’ expectations affects the Malaysian money market and FX market, with the

exchange rate defined as ringgit (RM) per U.S. dollar, denoted ERM/$. You need show

only the short-run effects of this change in investors’ expectations.

Answer: See the following diagram. In the absence of capital controls, the

Malaysian interest rate would have to rise. However, by preventing investors from taking

d. Compare and contrast the three approaches just outlined. As a policy maker,

which would you favor? Explain.

Answer: There is no “correct” answer to this question. The cases above highlight

7. Several countries have opted to join currency unions. Examples include those in the

euro area, the CFA franc union in West Africa, and the Caribbean currency union. This

involves sacrificing the domestic currency in favor of using a single currency unit in

multiple countries. Assuming that once a country joins a currency union, it will not leave,

do these countries face the policy trilemma discussed in the text? Explain.

Answer: These countries do face the trilemma because they are committed to

maintaining the first policy goal of a fixed exchange rate. Joining a currency union

8. During the Great Depression, the United States remained on the international gold

standard longer than other countries. This effectively meant that the United States was

committed to maintaining a fixed exchange rate at the onset of the Great Depression. The

U.S. dollar was pegged to the value of gold along with other major currencies, including

the British pound, the French franc, and so on. Many researchers have blamed the

severity of the Great Depression on the Federal Reserve and its failure to react to

economic conditions in 1929 and 1930. Discuss how the policy trilemma applies to this

situation.

Answer: The United States was committed to the fixed exchange rate with gold;

9. On June 20, 2007, John Authers, investment editor of the Financial Times, wrote the

following in his column “The Short View”:

The Bank of England published minutes showing that only the narrowest

possible margin, 5–4, voted down [an interest] rate hike last month.

Nobody foresaw this. . . . The news took sterling back above $1.99, and to

a 15-year high against the yen.

Can you explain the logic of this statement? Interest rates in the United Kingdom had

remained unchanged in the weeks since the vote and were still unchanged after the

minutes were released. What news was contained in the minutes that caused traders to

react? Explain using the asset approach.

10. We can use the asset approach to both make predictions about how the market will

react to current events and understand how important these events are to investors.

Consider the behavior of the Union/Confederate exchange rate during the Civil War.

How would each of the following events affect the exchange rate, defined as Confederate

dollars per Union dollar, EC$/$?

a. The Confederacy increases the money supply by 2,900% between July and

December 1861.

b. The Union Army suffers a defeat in Battle of Chickamauga in September 1863.

Answer: Appreciation in the Confederate dollar is expected because a military

c. The Confederate Army suffers a major defeat with Sherman’s March in the

autumn of 1864.