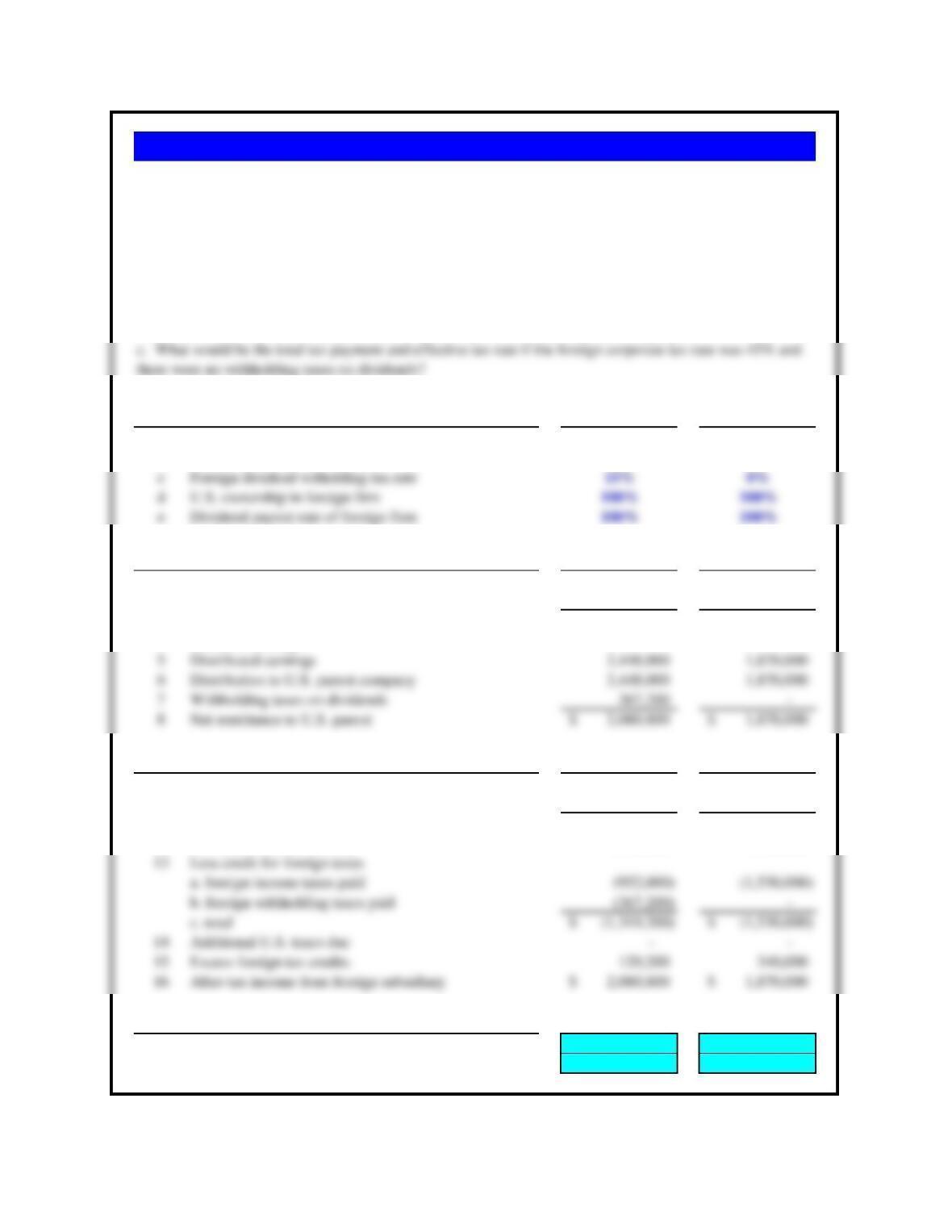

Baseline Values Case 1 Case 2

a Foreign corporate income tax rate 28% 45%

b U.S. corporate income tax rate 35% 35%

Foreign Subsidiary Tax Computation

1 Taxable income of foreign subsidiary 3,400,000$ 3,400,000$

2 Foreign corporate income tax (952,000) (1,530,000)

3 Net income available for distribution 2,448,000$ 1,870,000$

4 Retained earnings – –

U.S. Corporate Tax Computation on Foreign-Source Income

9 Dividend received (before withholding) 2,448,000$ 1,870,000$

10 Add-back foreign deemed-paid tax 952,000 1,530,000

11 Grossed-up foreign dividend 3,400,000$ 3,400,000$

12 Tentative U.S. tax liability 1,190,000 1,190,000

Tax Burden Measurement

17 Total taxes paid on remitted income 1,319,200$ 1,530,000$

18 Effective tax rate on foreign income 38.8% 45.0%

b. What is the effective tax rate paid on this income by the U.S.-based parent company?

c. What would be the total tax payment and effective tax rate if the foreign corporate tax rate was 45% and

there were no withholding taxes on dividends?

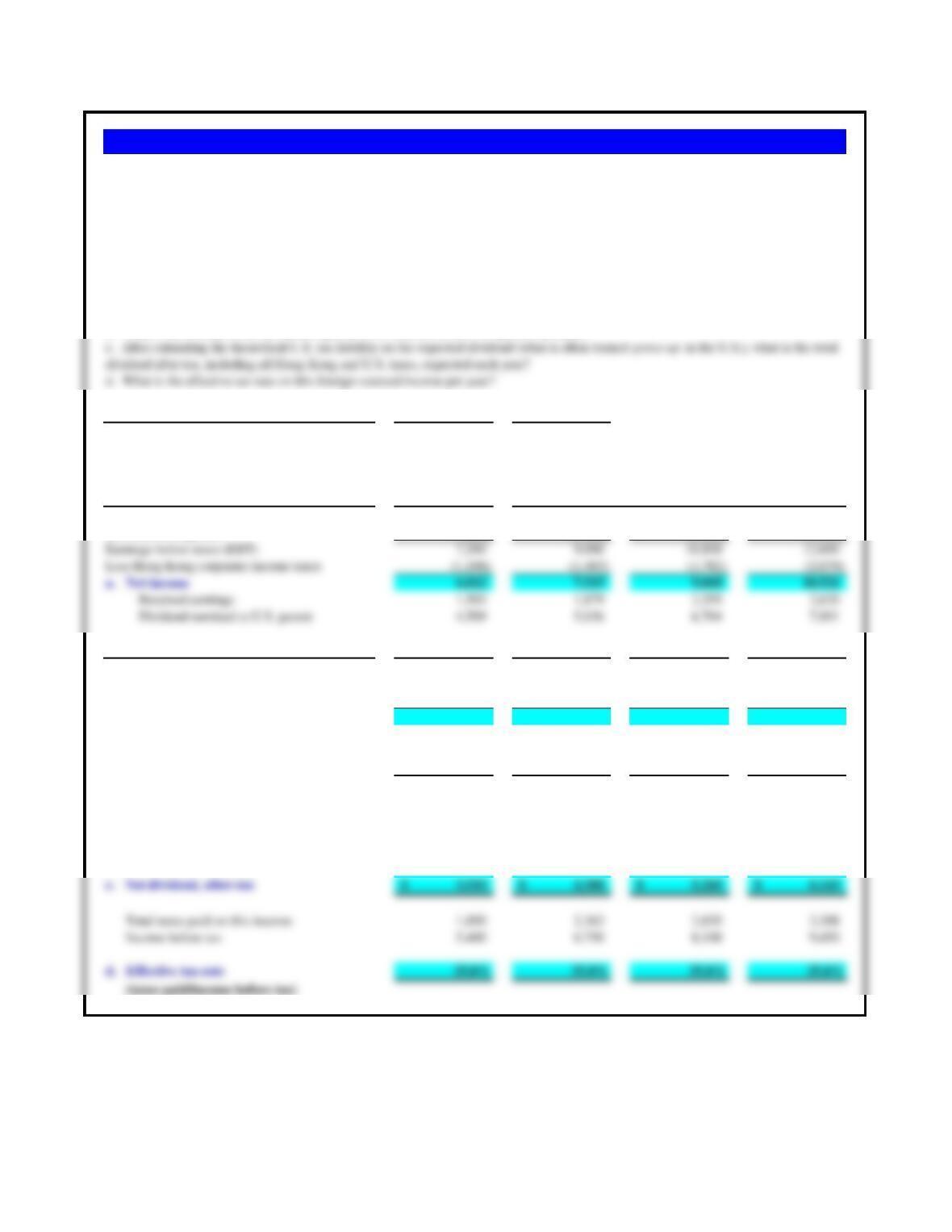

Problem 15.1 Avon’s Foreign-Source Income

a. What is the total tax payment, foreign and domestic combined, for this income?

Avon is a U.S.-based direct seller of a wide array of products for women. Avon markets leading beauty,

fashion and home products in more than 100 countries. As part of the training in its corporate treasury

offices, it has its interns build a spreadsheet analysis of the following hypothetical subsidiary

earnings/distribution analysis. Use the spreadsheet presented in Exhibit 15.7 for your basic structure.

Country Hong Kong United States

Corporate income tax rate 16.5% 35.0%

Dividend payout rate 75.0%

Withholding tax on dividends 0.0%

Jewel Hong Kong Income Items (millions US$) 2011 2012 2013 2014

Earnings before interest and taxes (EBIT) 8,000 10,000 12,000 14,000

Less interest expenses (800) (1,000) (1,200) (1,400)

United States Taxation: Grossup 2011 2012 2013 2014

Gross dividend remitted 4,509$ 5,636$ 6,764$ 7,891$

Less withholding taxes – – – –

b. Net dividend remitted 4,509$ 5,636$ 6,764$ 7,891$

Add back proportion of corp income tax 891$ 1,114$ 1,337$ 1,559$

Add back withholding taxes paid – – – –

Grossed-up dividend for US tax purposes 5,400$ 6,750$ 8,100$ 9,450$

Theoretical US tax liability (1,890) (2,363) (2,835) (3,308)

Foreign tax credits (FTCs) (891) (1,114) (1,337) (1,559)

Additional US taxes due? (999) (1,249) (1,499) (1,748)

Excess foreign tax credits? – – – –

c. After estimating the theoretical U.S. tax liability on the expected dividend (what is often termed gross-up in the U.S.), what is the total

dividend after tax, including all Hong Kong and U.S. taxes, expected each year?

d. What is the effective tax rate on this foreign-sourced income per year?

Problem 15.2 Pacific Jewel Airlines (Hong Kong)

Pacific Jewel Airlines is a U.S.-based air freight firm with a wholly owned subsidiary in Hong Kong. The subsidiary, Jewel Hong Kong,

has just completed a long-term planning report for the parent company in San Francisco, in which it has estimated the following expected

earnings and payout rates for the years 2011–2014.

The current Hong Kong corporate tax rate on this category of income is 16.5%. Hong Kong imposes no withholding taxes on dividends

remitted to U.S. investors (per the Hong Kong-United States bilateral tax treaty). The U.S. corporate income tax rate is 35%. The parent

company wants to repatriate 75% of net income as dividends annually.

b. What is the amount of the dividend expected to be remitted to the U.S. parent each year?

a. Calculate the net income available for distribution by the Hong Kong subsidiary for the years 2011–2014.

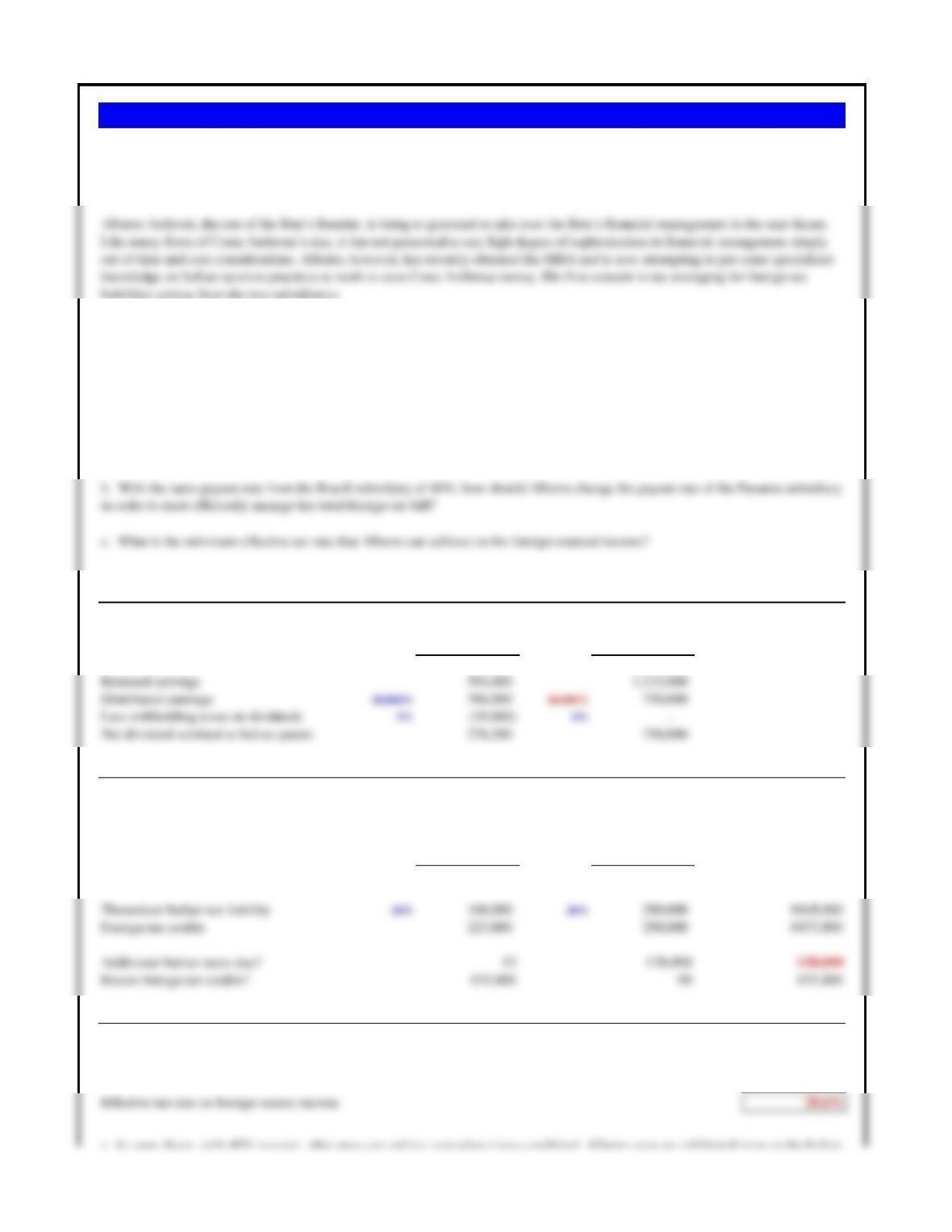

Assumptions Part a) Part b) Part b)

Dividend payout rate 50.0% 40.0% 60.0%

Corporate income tax rate, retained 45.0% 45.0% 45.0%

Corporate income tax rate, distributed 30.0% 30.0% 30.0%

Added tax for retained over distributed 15.0% 15.0% 15.0%

Kraftstoff’s Income Items (€)

Distributed income € 169,225,000 € 135,380,000 € 203,070,000

Less any added corporate tax – – –

Distributed income after-tax € 169,225,000.0 € 135,380,000.0 € 203,070,000.0

Retained income € 169,225,000 € 203,070,000 € 135,380,000

Problem 15.3 Kraftstoff of Germany

Kraftstoff’s primary problem is that the German corporate income tax code applies a different income tax rate to income

depending on whether it is retained (45%) or distributed to stockholders (30%).

a. If Kraftstoff planned to distribute 50% of its net income, what would be its total net income and total corporate tax bills?

Kraftstoff is a German-based company that manufactures electronic fuel-injection carburetor assemblies for several large

automobile companies in Germany, including Mercedes, BMW, and Opel. The firm, like many firms in Germany today, is

revising its financial policies in line with the increasing degree of disclosure required by firms if they wish to list their shares

publicly in or out of Germany. The company’s earnings before tax (EBT) is €483,500,000.

Problem 15.4 Costa Ambrosa SpA’s Tax Averaging

Subsidiary Income Statement BRAZIL PANAMA Total Income

Earnings before taxes €1,500,000 €2,500,000

Less corporate income tax 34% (510,000) 25% (625,000)

Net income €990,000 €1,875,000

Italian Tax Calculation (individually)

Net dividend remitted €376,200 €750,000 €1,126,200

Gross-up:

Withholding taxes paid 19,800 –

Foreign corporate income tax paid 204,000 250,000

Grossed-up dividend €600,000 €1,000,000 €1,600,000

TAX AVERAGING (combined)

Total additional Italian taxes due after averaging €0

Excess FTCs to carry forward/back? €25,800

b. With the same payout rate from the Brazil subsidiary of 40%, how should Alberto change the payout rate of the Panama subsidiary

in order to most efficiently manage her total foreign tax bill?

a. If Alberto Ambrosi assumes a 40% payout rate from each subsidiary, what are the additional taxes due on foreign-sourced income

from Brazil and Panama individually? How much additional Italian taxes would be due if Alberto averaged the tax credits/liabilities

of the two units?

Costa Ambrosa SpA is a relatively new Italian-based retailer of specialty furniture and wood carvings. The firm is vertically

integrated with wood raw materials subsidiaries in Central and South America and distribution outlets throughout Europe. Costa

Ambrosa’s two South American subsidiaries are in Brazil and Panama.

out of time and cost considerations. Alberto, however, has recently obtained his MBA and is now attempting to put some specialized

knowledge on Italian taxation practices to work to save Costa Ambrosa money. His first concern is tax averaging for foreign tax

liabilities arising from the two subsidiaries.

Panama operations are slightly more profitable than Brazil, which is particularly good since Panama is a relatively low-tax country.

Panama’s corporate taxes are a flat 25%, and there are no withholding taxes imposed on dividends paid by foreign firms with

operations there. Brazil has a higher corporate income tax rate at 34% and imposes a 5% withholding tax on all dividends distributed

to foreign investors. The current Italian corporate income tax rate is 28%.

a. As seen above, with 40% payouts, after gross-up and tax averaging (cross-crediting), Alberto owes no additional taxes to the Italian

tax authorities. He has a €25,800 tax credit to carry forward. The effective tax rate on foreign source income is then 29.6%.

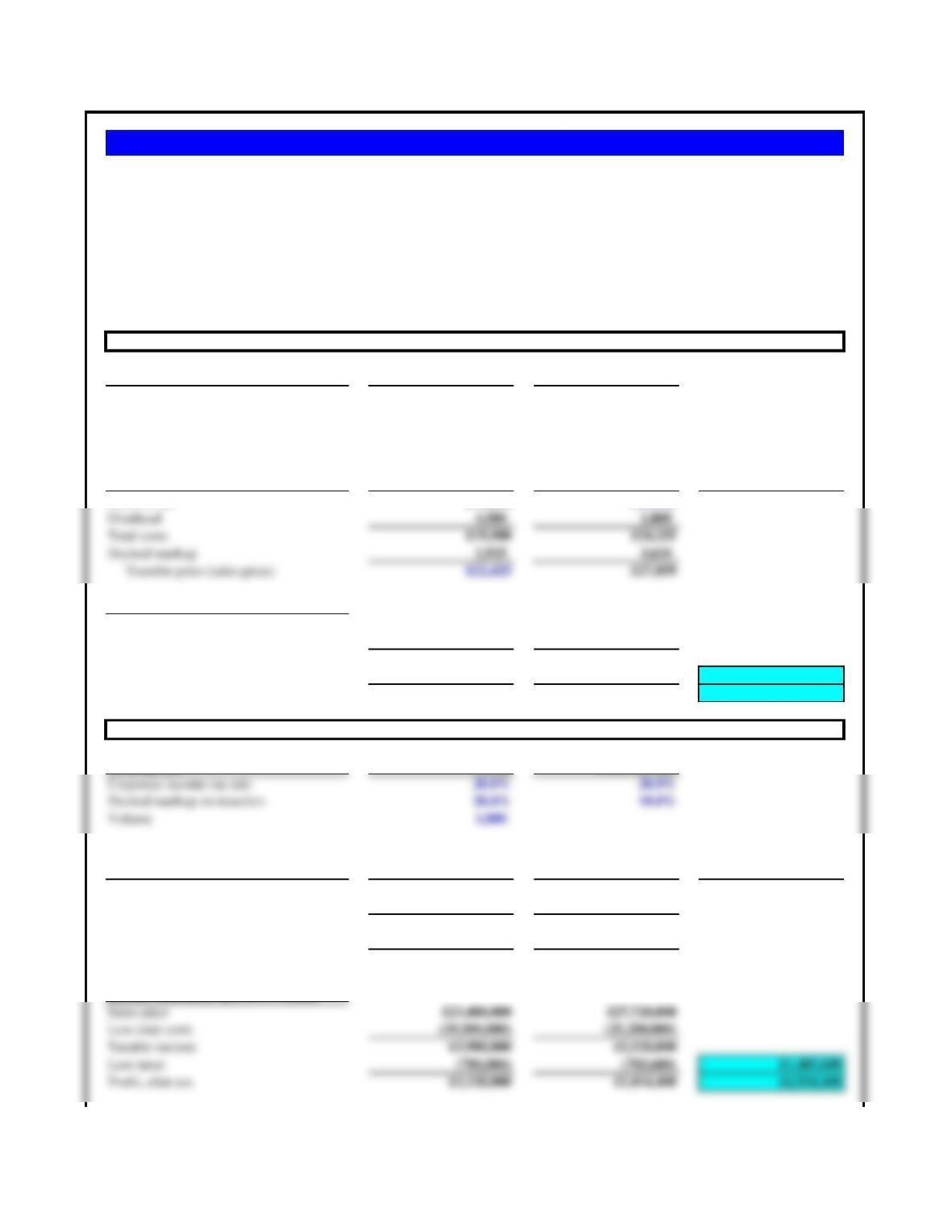

Assumptions China Great Britain

Corporate income tax rate 20.0% 28.0%

Desired markup on transfers 15.0% 15.0%

Volume 1,000

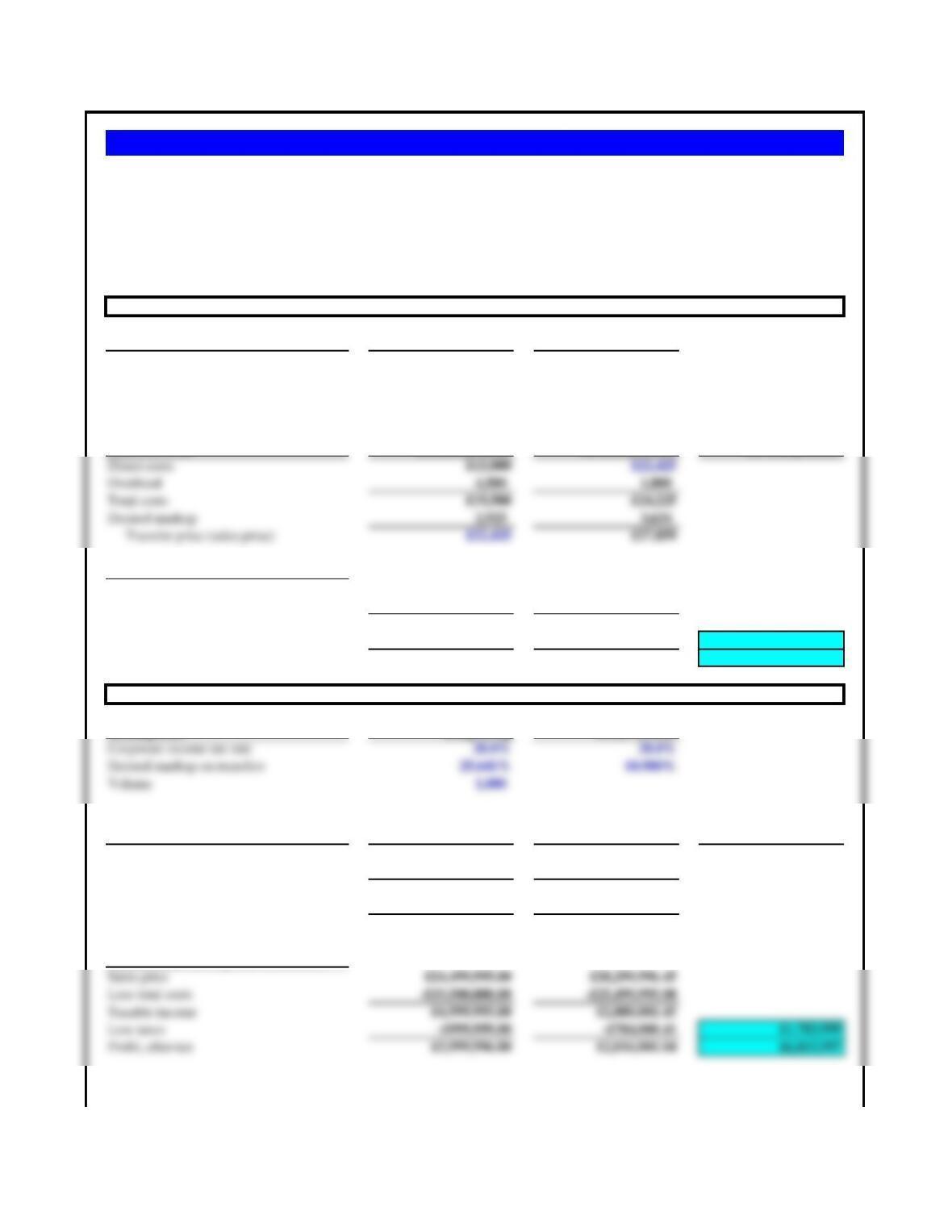

Constructing Transfer (Sales) Kaili Razor Supermax Consolidated

Price Per Unit (British pounds) (British pounds) (British pounds)

Income Statement (prices x volume)

Sales price £22,425,000 £27,858,750

Less total costs (19,500,000) (24,225,000)

Taxable income £2,925,000 £3,633,750

Less taxes (585,000) (1,017,450) £1,602,450

Profit, after-tax £2,340,000 £2,616,300 £4,956,300

Assumptions China Great Britain

Constructing Transfer (Sales) Chinglish Dirk Torrington Edge Consolidated

Price Per Unit (British pounds) (British pounds) (British pounds)

Direct costs £15,000 £23,400

Overhead 4,500 1,800

Total costs £19,500 £25,200

Desired markup 3,900 2,520

Transfer price (sales price) £23,400 £27,720

Problem 15.5 Kaili Razor (A)

Baseline Analysis

Repositioned Profits

Use the following company case to answer Problems 15.5 through 15.7. Kaili Razor (China) exports razor blades to its wholly

owned parent company, Supermax (Great Britain). China tax rates are 20% and British tax rates are 28%. Kaili calculates its profit

per container as follows (all values in British pounds).

Corporate management of Supermax is considering repositioning profits within the multinational company. What happens to the

profits of Kaili Razor and Supermax, and the consolidated results of both, if the markup at Kaili was increased to 20% and the

markup at Supermax was reduced to 10%? What is the impact of this repositioning on consolidated tax payments?

By increasing the markup in China, the company has repositioned more of its profits in the lower tax environment,

China, where the tax rate is 20% compared to Great Britain’s 28%. Note that the final sales price has actually fallen.

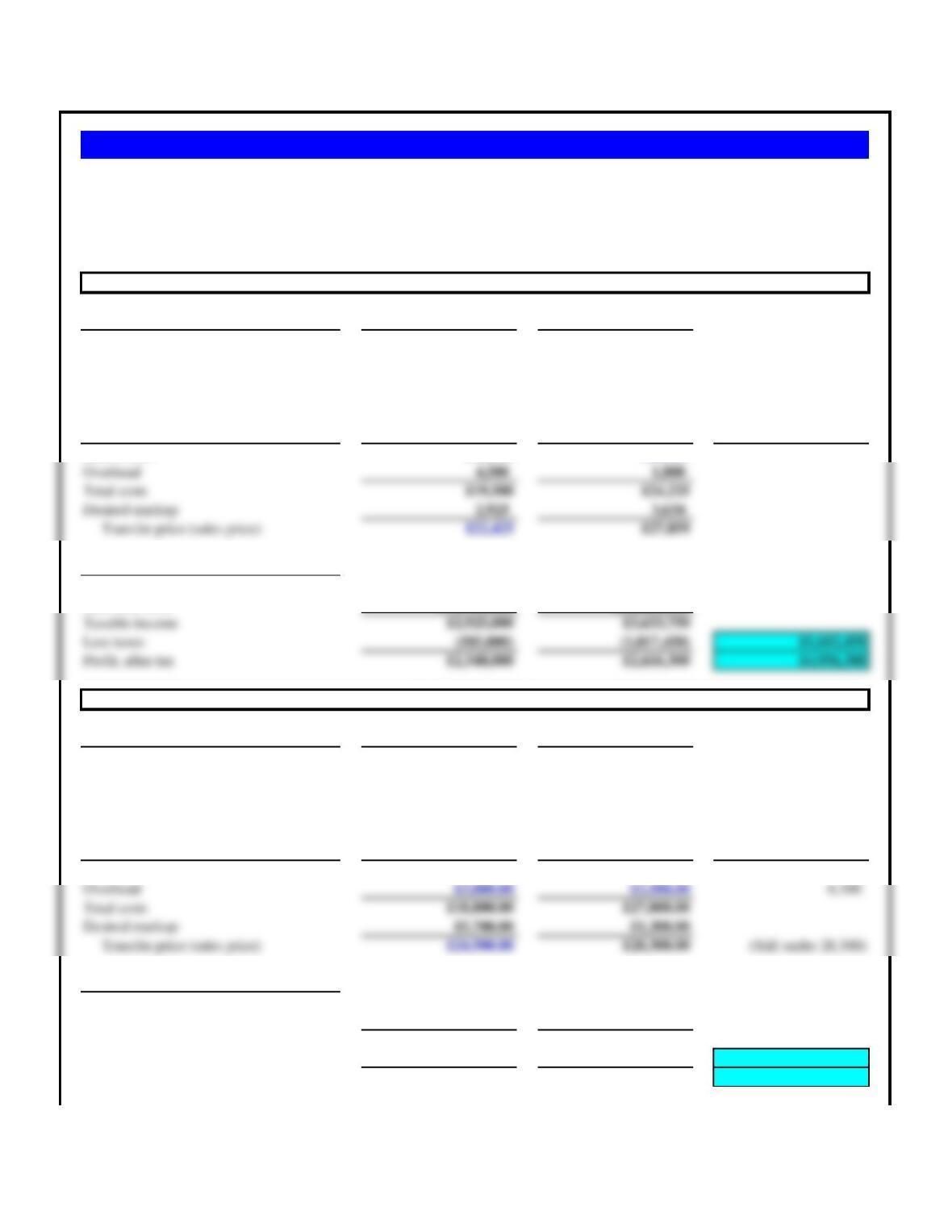

Baseline Repositioned Change

Consolidated profits, after-tax £4,956,300 £4,934,400 -0.44%

Consolidated tax payments £1,602,450 £1,485,600 -7.29%

Assumptions China Great Britain

Corporate income tax rate 20.0% 28.0%

Desired markup on transfers 15.0% 15.0%

Volume 1,000

Constructing Transfer (Sales) Kaili Razor Supermax Consolidated

Price Per Unit (British pounds) (British pounds) (British pounds)

Income Statement (prices x volume)

Sales price £22,425,000 £27,858,750

Less total costs (19,500,000) (24,225,000)

Taxable income £2,925,000 £3,633,750

Less taxes (585,000) (1,017,450) £1,602,450

Profit, after-tax £2,340,000 £2,616,300 £4,956,300

Constructing Transfer (Sales) Kaili Razor Supermax Consolidated

Price Per Unit (British pounds) (British pounds) (British pounds)

Direct costs £15,000.00 £24,500.00

Overhead £4,500.00 £1,000.00

Total costs £19,500.00 £25,500.00

Desired markup £5,000.00 £2,800.00

Transfer price (sales price) £24,500.00 £28,300.00

Income Statement (prices x volume)

The company is working with two constraints. First, the final sales price by Supermax needs to be 28,300 or

less. Secondly, the British tax authorities have established a maximum transfer price on the blades at 24,500.

Problem 15.6 Kaili Razor (B)

Baseline Analysis

Repositioned Profits

Encouraged by the results in the previous problem’s analysis, corporate management of Supermax wishes to continue to reposition

profit in China. It is, however, facing two constraints. First, the final sales price in Great Britain must be ₤28,300 or less to remain

competitive. Second, the British tax authorities – working with Supermax’s cost accounting staff – have established a maximum

transfer price allowed (from China) of ₤24,500. What combination of markups do you recommend for Supermax to institute? What

is the impact of this repositioning on consolidated profits on after-tax and total tax payments?

Assumptions China Great Britain

Corporate income tax rate 20.0% 28.0%

Desired markup on transfers 15.0% 15.0%

Volume 1,000

Constructing Transfer (Sales) Kaili Razor Supermax Consolidated

Price Per Unit (British pounds) (British pounds) (British pounds)

Direct costs £15,000 £22,425

Income Statement (prices x volume)

Sales price £22,425,000 £27,858,750

Less total costs (19,500,000) (24,225,000)

Assumptions China Great Britain

Corporate income tax rate 20.0% 28.0%

Desired markup on transfers 30.31913% 4.81482%

Volume 1,000

Constructing Transfer (Sales) Kaili Razor Supermax Consolidated

Price Per Unit (British pounds) (British pounds) (British pounds)

Direct costs £15,000.00 £24,500.00

Income Statement (prices x volume)

Sales price £24,499,996.44 £28,299,997.67

Less total costs -£18,800,000.00 -£26,999,996.44

Taxable income £5,699,996.44 £1,300,001.23

Less taxes -£1,139,999.29 -£364,000.34 £1,504,000

Profit, after-tax £4,559,997.15 £936,000.88 £5,495,998

Problem 15.7 Kaili Razor (C)

Baseline Analysis

Repositioned Profits

Not to leave any potential tax repositioning opportunities unexplored, Supermax wants to combine the components of Problem 15.6

with a redistribution of overhead costs. If overhead costs could be reallocated between the two units, but still total £6,300, and

maintain a minimum of £3,800 per unit in Hong Kong, what is the impact of this repositioning on consolidated profits after tax and

total tax payments?

By both increasing the markup in China (and decreasing it in Great Britain), and reallocating overhead cost to

Great Britain, Supermax’s consolidated profits improve once again by positioning profits (losses) in the low-tax (high-tax)