15 Exchange Rates II: The Asset Approach in the Short Run

Notes to Instructor

Chapter Summary

This chapter combines the asset approach, based on the uncovered interest parity (UIP)

condition from Chapter 13, with the monetary approach from Chapter 14 to develop a

comprehensive model of exchange rate determination. Within the model, we can study

Comments

The authors continue to use the case of the United States and the Eurozone as a template

for understanding relative prices and exchange rates in two different regions. Here, a

more generic notation (home versus foreign) is used. This chapter uses some important

building blocks from Chapters 13 and 14:

• Money market: Determination of nominal interest rates, assuming sticky prices in

Next, the monetary approach developed in Chapter 14 is combined with UIP. This

allows students to study the effects of permanent shocks in the short run and the long run,

An alternative presentation would begin with the comprehensive model, studying the

effects of temporary and permanent shocks in the short run and the long run. Although

temporary shocks do not have long-run implications for the variables in the model, the

1. Exchange Rates and Interest Rates in the Short Run: UIP and Forex Market

Equilibrium

a. Risky Arbitrage

2. Interest Rates in the Short Run: Money Market Equilibrium

a. Money Market Equilibrium in the Short Run: How Nominal Interest Rates

Are Determined

i. The Assumptions

ii. The Model

b. Money Market Equilibrium in the Short Run: A Graphical Solution

c. Adjustment to Money Market Equilibrium in the Short Run

d. Another Building Block: Short-Run Money Market Equilibrium

3. The Asset Approach: Applications and Evidence

a. The Asset Approach to Exchange Rates: Graphical Solution

i. The U.S. Money Market

4. A Complete Theory: Unifying the Monetary and Asset Approaches

a. Side Bar: Confessions of a Forex Trader

b. Long-Run Policy Analysis

5. Fixed Exchange Rates and the Trilemma

a. What Is a Fixed Exchange Rate Regime?

6. Conclusions

a. Application: News and the Foreign Exchange Market in Wartime

Lecture Notes

The monetary approach to exchange rate determination is a poor model for predicting

exchange rate changes in the short run because of a key assumption of the monetary

approach: prices are flexible.

For example, consider the prices of a basket of goods in two countries, the United

States and the United Kingdom. Initially, the price of this basket is £100 in the United

The monetary approach predicts the exchange rate should change by 4%, or a 4%

depreciation in the British pound and a 4% appreciation in the U.S. dollar. In actuality,

From the last chapter, we know that there is evidence supporting PPP in the long run

but not in the short run. This suggests another theory is needed to explain these short-run

1 Exchange Rates and Interest Rates in the Short Run: UIP and Forex

Market Equilibrium

Consider two alternative one-year investment strategies:

• a U.S. dollar‒denominated account with interest rate i$

Risky Arbitrage

In risky arbitrage, the investor does not cover her deposits abroad with a forward

contract. She must forecast the expected future exchange rate to find her expected dollar-

denominated return on peso-denominated deposits. From the UIP approximation in

Chapter 13, this yields the arbitrage condition

The UIP condition is the fundamental equation of the asset approach to exchange

rates. Solving for the spot exchange rate, we can see which factors influence the spot

exchange rate, E$/peso:

According to this expression, the current exchange rate depends on home and foreign

interest rates and the expected exchange rate.

Note that the asset approach to exchange rates assumes that the expected exchange

rate and short–term interest rates are known.

Short–Term Interest Rates Short-term interest rates (home and foreign) are observed by

market participants. Investors know the interest rates on deposits at home (the United

Exchange Rate Expectations Exchange rate expectations are based on the monetary

Equilibrium in the Forex Market: An Example

This example mirrors the example in the textbook, except here we use the peso–dollar

exchange rate. In the textbook, the dollar is expected to depreciate against the euro. Here,

the dollar is expected to appreciate against the peso.

(1)

(2)

(3)

(4)

(5)

(6) = (2)

+ (5)

Interest Rate

on Dollar–

Denominated

Deposits

(annual)

Interest Rate

on Peso-

Denominated

Deposits

(annual)

Spot

Exchange

Rate

(today)

Expected

Future

Exchange

Rate (in

one year)

Expected Peso

Appreciation

against Dollar

(in one year)

Expected

Dollar

Return on

Peso

Deposits

(annual)

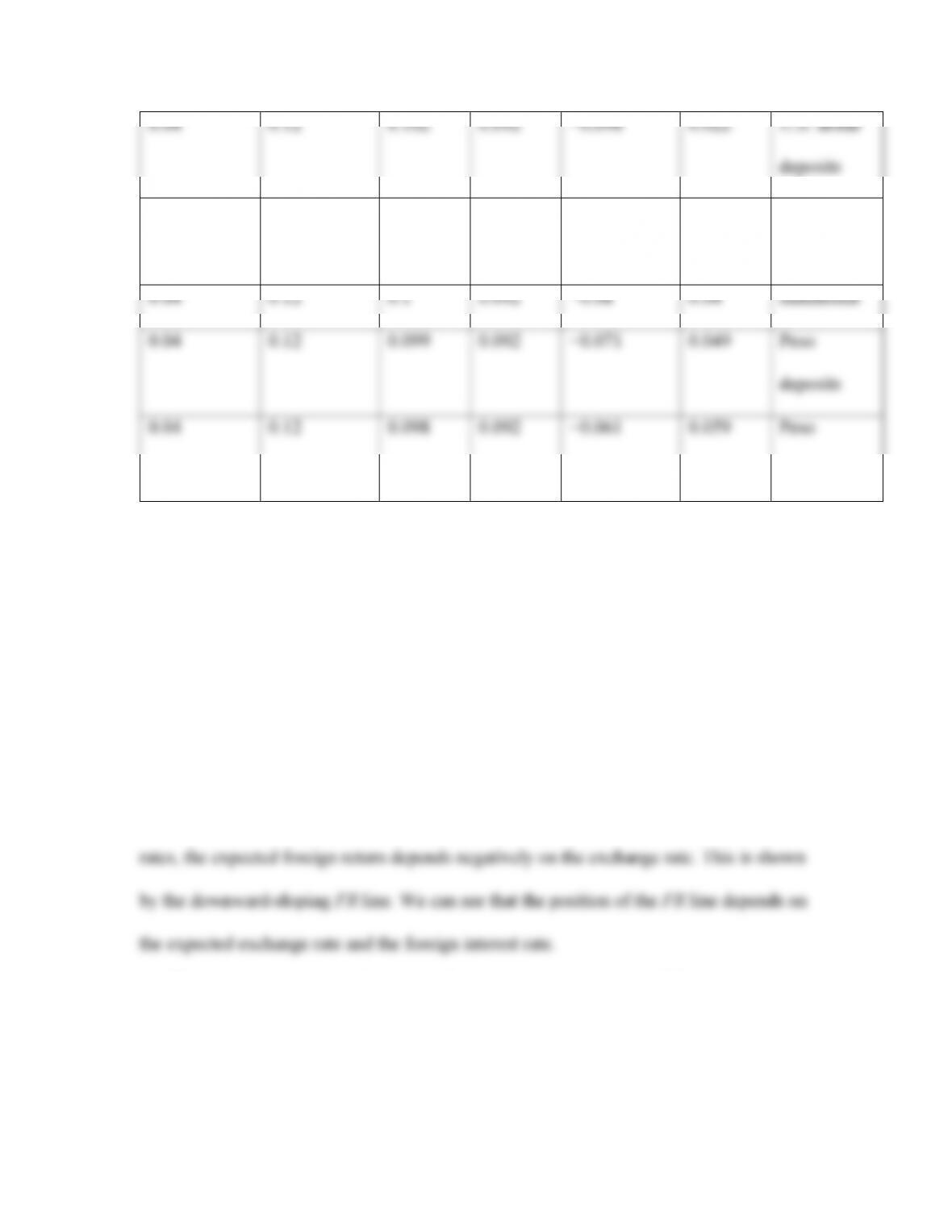

Investors

Prefer

0.04

0.12

0.102

0.092

−0.098

0.022

U.S. dollar

0.04

0.12

0.101

0.092

−0.089

0.031

U.S. dollar

deposits

0.04

0.12

0.1

0.092

−0.08

0.04

Indifferent

0.04

0.12

0.099

0.092

−0.071

0.049

Peso

deposits

0.04

0.12

0.098

0.092

−0.061

0.059

Peso

deposits

The above data, as well as the corresponding examples from the textbook, are included in

the Excel workbook for this chapter. In addition, FX market diagrams are included for all

four examples.

Figure 15-2 is an FX market diagram—our graphical representation of the FX

market. In this diagram, the expected return on two investment strategies (domestic

versus foreign) is illustrated as a function of the spot exchange rate.

In the previous table, we can see that, for given interest rates and expected exchange

The domestic return is independent of the exchange rate because U.S. investors do

not need to convert their currency to invest in U.S. dollar deposits. Therefore, the

domestic return (DR) line is horizontal. The position of this line depends on the domestic

interest rate.

The equilibrium exchange rate is the spot rate that equates the domestic return (1) to

Adjustment to Forex Market Equilibrium

In the table, we see that if the spot exchange rate is more than $0.10 per peso, the return

on U.S. dollar deposits exceeds the return on peso deposits. In this case, investors will

Changes in Domestic and Foreign Returns and Forex Market Equilibrium

Now, we will consider changes in the equilibrium spot exchange rate. In summary:

■ ↑Ee$/peso → ↑E$/peso ($ depreciation, peso appreciation)

In all three of the following cases, the domestic return is less than the foreign return at the

prevailing spot exchange rate, $0.10 per peso. Investors will shift their deposits away

from domestic deposits in favor of foreign deposits. The foreign currency will appreciate

until the two returns are equal.

A Change in the Domestic Interest Rate Suppose that the domestic (United States)

interest rate decreases from 4% to 3%. This is illustrated as a downward shift in the DR

line. The diagram implies that the spot exchange rate will increase.

A Change in the Foreign Interest Rate Suppose that the foreign interest rate increases

A Change in the Expected Future Exchange Rate Suppose the expected future

exchange rate increases to $0.10 per peso. In Figure 15-2, this is illustrated as an upward

shift in the FR line. The diagram implies that the spot exchange rate will increase.

Summary

Figure 15-2 is a graphical illustration of the foreign exchange market. Note that the UIP

2 Interest Rates in the Short Run: Money Market Equilibrium

The model in the preceding section provides us with a way to explain exchange rate

movements based on interest rates and expectations. Now we are ready to explain why

interest rates and expectations change, drawing on the monetary approach we saw in

Chapter 14.

Money Market Equilibrium in the Short Run: How Nominal Interest Rates Are

Determined

Interest rates are determined in the money market. Here, we consider the money market

The Assumptions It is important to distinguish between short–run equilibrium and long-

run equilibrium. When explaining exchange rate movements using the FX market, we

will study both. This provides an important link to Chapter 14.

Short-run assumptions

Long-run assumptions

The price level is fully flexible and adjusts to bring the money market to equilibrium. The

nominal interest rate is fixed and equal to the sum of the world real interest rate and

domestic inflation: i = r* +

π

.

Why is the short run different from the long run?

First, it is common to assume sticky prices, also known as nominal rigidity, in the short

The Model From the monetary approach, we know money market equilibrium is

achieved when real money demand is equal to real money supply. Following the generic

notation used in the lecture notes for Chapter 14, H denotes home country and F denotes

foreign country. In the textbook, the United States is treated as the home country and

Europe is the foreign country.

Money Market Equilibrium in the Short Run: Graphical Solution

Figure 15-4 shows the money market equilibrium based on the general money demand

functions assumed previously.

■ MH is set by the central bank.

Note that both of these variables are independent of the nominal interest rate. Therefore,

the money supply curve is vertical.

Demand for real money balances: L(iH) × YH

Adjustment to Money Market Equilibrium in the Short Run

The nominal interest rate adjusts to equate real money balances demanded and supplied.

If the interest rate is more than the market–clearing rate, then real money supplied will

exceed real money demanded (point 2 on Figure 15-4). The public will seek to reduce its

money holdings, shifting portfolios toward interest–bearing assets. Borrowers will only

pushes up the nominal interest rate.

Another Building Block: Short–Run Money Market Equilibrium

Figure 15-5 summarizes the monetary model, illustrating how a country’s interest rate

Changes in Money Supply and the Nominal Interest Rate

The money supply curve depends on the nominal money supply and the price level. This

section considers the short–run effects.

In the short run, only the central bank can change the real money supply because the

price level is fixed.

Figure 15-6(a) illustrates an increase in the money supply. In summary, changes in

the nominal money supply affect the market as follows:

APPLICATION

Can Central Banks Always Control the Interest Rate? A Lesson from the Crisis of

funds rate cause changes in other interest rates, in the same direction. Despite lowering

the Fed funds rate to zero in 2008, bank loan rates barely changed at all. Banks had

become much more risk averse and were adding a much larger risk premium to their base

interest rates than they had before 2008.

2. Buying nontraditional securities such as commercial paper and mortgage-backed

securities

3. Expanding the list of counterparties from which it would buy securities, to include

some nonbank institutions

The result: M0 more than doubled to over $1 trillion. However, most of this increase was

Did it work? The consensus seems to be that quantitative easing worked to steer the

Changes in Real Income and the Nominal Interest Rate

Figure 15-6(b) illustrates an increase in money demand caused by an increase in real

income. Changes in real income affect money demand because they affect the public’s

desire to spend. When real income rises, the public plans to spend more and therefore

needs more money balances to conduct such transactions. This leads to an increase in

money demand.

In summary, changes in real income affect the market as follows:

The Monetary Model: The Short Run Versus the Long Run

Note that the short–run analysis yields results that differ significantly from those we

found using the monetary approach in the long run.

Because of the differences in the models’ implications, it is important to distinguish

between temporary shocks and permanent shocks. Temporary shocks dissipate before

prices adjust. Permanent shocks affect the economy in the long run and price adjustment

will occur.

It may be useful to emphasize this distinction now. Students often are confused about

temporary versus permanent and short run versus long run.

■ Temporary shocks:

❑ The long-run equilibrium is always the same as the initial equilibrium because

the effects of the shock disappear before price adjustment occurs.

❑ Expected exchange rates will remain unchanged because investors know that

■ Permanent shocks:

❑ The short-run equilibrium and long-run equilibrium are different.

There are some apparent contradictions between the short– and long-run models. In

both the short run and the long run, raising the growth rate of the money supply leads to

an exchange rate depreciation. However, in the short run, low interest rates and currency

depreciation go together; but in the long run, high interest rates and currency depreciation

go together.

The explanation for this apparent contradiction lies in expectations. In the short run,

expectations tend to be inflexible. This is true whether we look at future exchange rates,

the growth rate of the money supply, or the inflation rate. A temporary policy will not

change the nominal anchor and inflexible expectations are, in fact, correct predictors. In

3 The Asset Approach: Applications and Evidence

In this section, we use the previous model to understand how shocks affect the money

The Asset Approach to Exchange Rates: Graphical Solution

The asset approach to exchange rates includes two diagrams: the home money market

The U.S. Money Market [Figure 15-7(a)]

1. MS represents the home real money supply. This line is vertical for two reasons.

2. MD represents home real money demand. This line is downward-sloping because,

as the nominal interest rate rises, the opportunity cost of holding money balances

The Market for Foreign Exchange [Figure 15-7(b)]

1. FR represents the return on foreign deposits in domestic currency. As the spot

exchange rate rises, the home currency depreciates, so the return on foreign-

2. Because domestic investors do not need to convert currency to deposit funds into

a domestic account, the return on these deposits is independent of the spot

Capital Mobility Is Crucial This model of exchange rate determination hinges on

arbitrage. Therefore, if a country imposes capital controls, then the investor no longer has

Putting the Model to Work The two diagrams in Figure 15-7 are linked. The money

market tells us the equilibrium nominal interest rate in the home country. This is

determined by the intersection of MS and MD. The nominal interest rate is DR in the

The foreign interest rate is determined in the foreign money market. Although this is