Money Growth, Inflation, and Depreciation

When developing the theory of PPP, we examined both absolute and relative PPP.

Because economists are often more interested in studying the behavior of inflation rather

than the level of prices, it is convenient to express the fundamental equations in rates of

change rather than in levels.

Define the growth rates of the variables for a given country i as follows:

Note that the expression for the inflation rate comes from the definition of money

demand.

We know from relative PPP that the percentage change in the exchange rate is equal

to the inflation differential:

Inserting the definitions of growth rates from the previous equations yields

We can use this equation to see how changes in the growth rates of money supply and

real income at home and abroad affect the inflation differential and the exchange rate.

↑µH → ↑πH → > 0 (home currency depreciates, foreign appreciates)

3 The Monetary Approach: Implications and Evidence

This section examines empirical evidence and applications of the monetary model.

Exchange Rate Forecasts Using the Simple Model

We can use the monetary model to forecast the future expected level of exchange rates or

to forecast expected changes in the exchange rate. We have already seen how changes in

the money supply and real income (in levels and growth rates) affect expected future

Forecasting Exchange Rates: An Example The following example differs from the one

presented in the book in two ways. First, the numerical values differ from those used in

Case 1: A One-Time Decrease in the Home Money Supply Suppose there is a one–time

10% decrease in the home money supply. State what happens to the home price level,

exchange rate, real money balances, and real income.

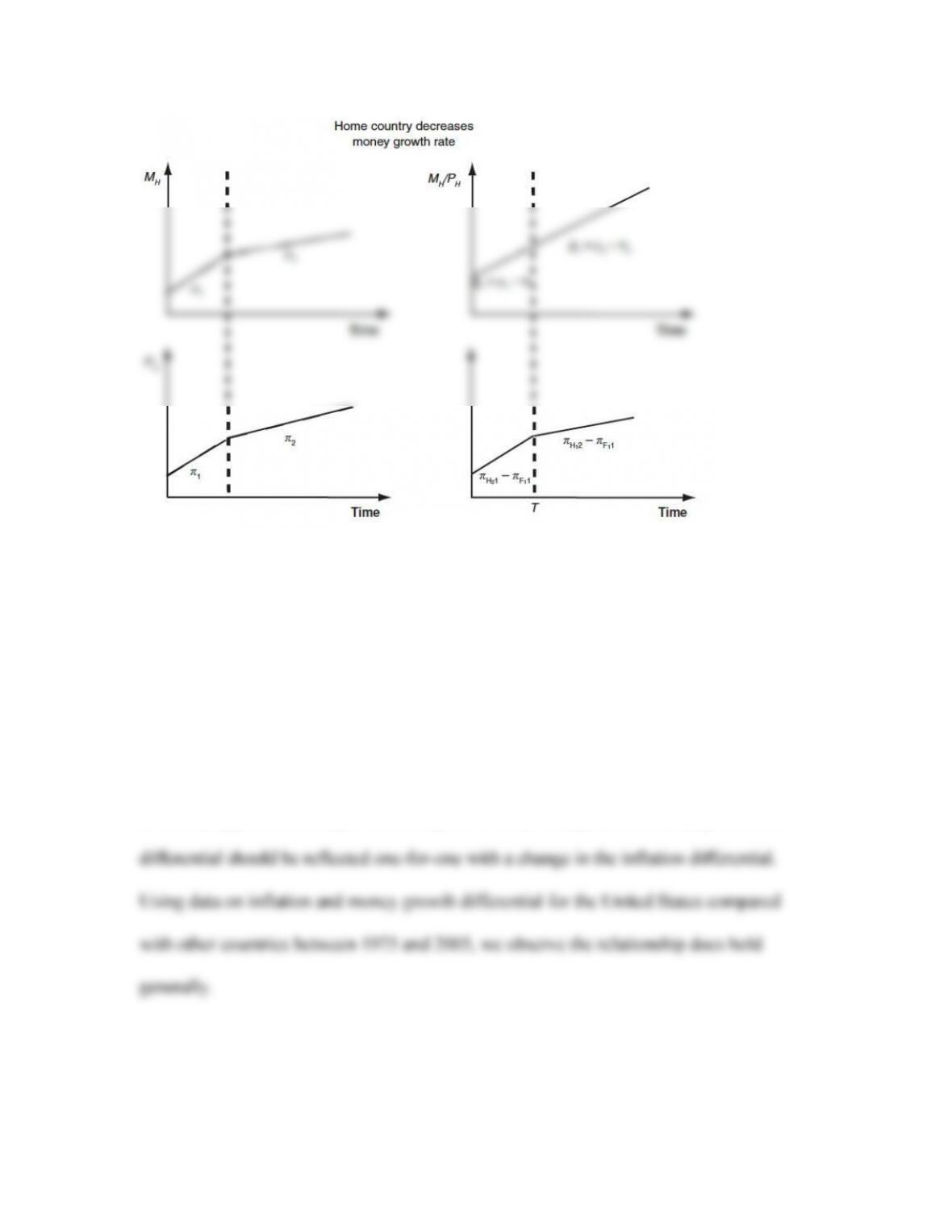

Case 2: A Decrease in the Money Growth Rate Suppose the money growth rate

decreases from 7% to 5% in the home country. State what happens to the home money

supply, the home price level, the home real money balances, and the exchange rate. Plot

out the behavior of each variable over time, before and after the change in the money

growth rate.

First, we can use the fundamental equations to understand how these variables are

behaving before the change in the home money growth rate:

This implies there is no expected change in the exchange rate:

Now, let’s examine what happens when the home country reduces its money growth rate

from 7% to 5%. The inflation rate in the home country will decrease:

The foreign country’s inflation rate remains at 4% because there was no change in the

foreign money supply. Therefore, the inflation differential is now negative:

APPLICATION

Evidence for the Monetary Approach

To test the validity of the simple monetary model shown earlier, we can look at the

relationship between money growth rates and inflation differentials. We did a similar test

for relative PPP. Here, we conduct two tests. First, the fundamental equation of the

monetary approach to the price level implies that any change in the money growth rate

Second, the fundamental equation of the monetary approach to exchange rates implies

that differentials in money growth rates should reflect changes in the exchange rate. In

our previous example, we saw that a 2–point decrease in the money growth rate should

lead to a 2% appreciation in the home country’s currency (e.g., a 2% decrease in the

exchange rate). Using data comparing money growth differentials and exchange rates

APPLICATION

Hyperinflations

A hyperinflation occurs when the average price level rises by more than 50% per month

over a sustained period of time. At that rate, the price level doubles every 52 days. Here’s

why:

Episodes of hyperinflation provide an ideal situation for studying the monetary

PPP in Hyperinflations Figure 14-9 examines several episodes of hyperinflation during

the twentieth century. The empirical test used here is identical to the one used in Figure

14-2 to test relative PPP. We can see from Figure 14-9 that relative PPP seems to hold for

countries with hyperinflation.

Money Demand in Hyperinflations Figure 14-11 uses data from countries with

hyperinflation to examine the relationship between inflation and real money balances.

From this figure, we observe a clear negative relationship—the demand for real money

balances decreases as the inflation rate increases. This indicates that changes in inflation

S I D E B A R

Currency Reform

During hyperinflations, one of the first currency reforms needed is a redefinition of the

currency. The central bank usually starts adding zeroes to the denominations of paper

currency. In Zimbabwe, Z$50 million notes were common. However, once the

government decides to reform the currency, they introduce a new currency unit with

considerably fewer zeros. In the 1980s, Argentina introduced the peso Argentina,

replacing the original peso at a rate of 10,000 to 1. The Argentine currency was redefined

4 Money, Interest, and Prices in the Long Run: A General Model

In this section, we relax the assumption of constant in the simple model to allow us to

The Demand for Money: The General Model

When individuals decide how much money they want to hold, they consider the costs and

benefits of holding money relative to an alternative, less liquid asset. The deciding factors

are nominal income and the interest rate.

■ Benefits of holding money: Individuals hold money to conduct their everyday

■ Costs of holding money: Compared with other assets, money earns little or no

interest. For each $1 held in the form of money, the individual forgoes interest. As

An increase in nominal income (PY) causes a proportionate increase in aggregate

money demand. An increase in the nominal interest rate (i) leads to a decrease in the

Note that the parameter was constant in the simple model. Here, L(i) captures the

portion of money demand that depends on the nominal interest rate. The real money

demand function is

The real money demand function is illustrated in Figure 14-11. The position of the real

money demand curve depends on real income. An increase in real income leads to an

Long–Run Equilibrium in the Money Market

Money market equilibrium is determined by the intersection of real money supply and

real money demand:

Inflation and Interest Rates in the Long Run

To understand how nominal interest rates affect the exchange rate, we can combine two

theories from earlier. First, we know that the percentage depreciation in the home

currency is equal to the inflation differential from relative PPP:

The Fisher Effect

Combining the relative PPP and UIP conditions, we have the following expression:

According to this expression, an increase in the inflation rate in one country leads to a

one-for-one increase in the nominal interest rate in that country. This is known as the

Fisher effect. Note that this relationship hinges on price flexibility as a condition for

Real Interest Parity

The previous condition can be rewritten in terms of real interest rates:

The real interest rate is the inflation–adjusted interest rate. This is calculated as the

nominal interest rate less the inflation rate. In the home country, reH = (iH −

π

eH);

therefore,

If PPP and UIP hold, the expected real interest rate should be the same across countries.

This is known as real interest parity. This condition is the direct result of arbitrage in

the goods market (PPP) and foreign exchange market (UIP).

Because of real interest rate parity, expected real interest rates should be equal across

countries. We can therefore define a world interest rate, r*:

Nominal interest rates in home and foreign are therefore defined as

APPLICATION

Evidence on the Fisher Effect

This application provides an empirical test of the Fisher effect. To test the Fisher effect,

we examine the inflation differentials for the United States compared with other countries

between 1995 and 2005. We know from the theory that these differentials should move

proportionately. According to the data in Figure 14-12, the Fisher effect holds.

The Fundamental Equation Under the General Model

This section derives a fundamental equation for the general model. The main distinction

is that L is no longer a constant:

Exchange Rate Forecasts Using the General Model

We studied a one-time change in the money supply, as well as a change in the growth rate

of the money supply, using the simple model. We can see how these changes affect the

economy by using the general model. The main differences between the two models will

be shown in nominal interest rates.

The following example differs from the one presented in the book in two ways. First,

the numerical values differ from those used in the text. Second, in this example, we allow

output to grow (in the textbook, it is assumed the growth rate of output is constant).

In both cases, assume that real income grows at a rate of 3% in both the home country

and the foreign country. Assume the money supply grows at a rate of 7% in both

countries. Suppose the world real interest rate is equal to 1%.

In the simple model, we saw that a one-time change in the money supply caused a

The same is true of the foreign country. The inflation differentials are equal to zero

because both countries have the same growth rates in money supply and real income.

This implies there is no expected change in the exchange rate.

Now let’s examine what happens when the home country reduces its money growth rate

from 7% to 5%. The inflation rate in the home country will decrease:

The foreign country’s inflation rate remains at 4% because there was no change in the

growth rate of the foreign money supply. Because the home inflation rate has changed,

this implies a change in the home country’s nominal interest rate:

The home country’s nominal interest rate decreases by 2 percentage points. Because the

home country’s nominal interest rate decreased, there will be an increase in the demand

for real money balances. The growth rate of the real money supply is unchanged at 3%

because the decrease in the growth rate of the money supply is matched by a decrease in

the inflation rate. However, there is a one-time increase in the level of the demand for

real money balances.

These variables are plotted over time on the following figure:

Looking Ahead If people know that a change in money growth is coming in the future,

they will adjust their expectations of the inflation rate and exchange rates accordingly.

This highlights the importance of these expectations. Even if a change is not

implemented, the expectations for change can have consequences for the variables in the

model.

5 Monetary Regimes and Exchange Rate Regimes

The monetary approach shows us that nominal variables are linked. These variables are

of interest to policymakers. For example, we can see from the model that if the

government wishes to reduce inflation, then the central bank must reduce the money

growth rate. If the government wants to fix the exchange rate, it must change the money

supply to reflect changes in economic conditions at home and abroad.

A common objective of central bankers is to maintain low inflation. Some central

banks publicly announce an inflation target in the hopes of influencing expectations

The Long Run: The Nominal Anchor

We’ve already seen a list of nominal variables that are viable nominal anchors in the

monetary approach. Each variable anchors the inflation rate but has different drawbacks.

Exchange Rate Target We can use relative PPP to see how the home country’s inflation

rate is related to the exchange rate: