Multinational Capital Budgeting ❖ 32

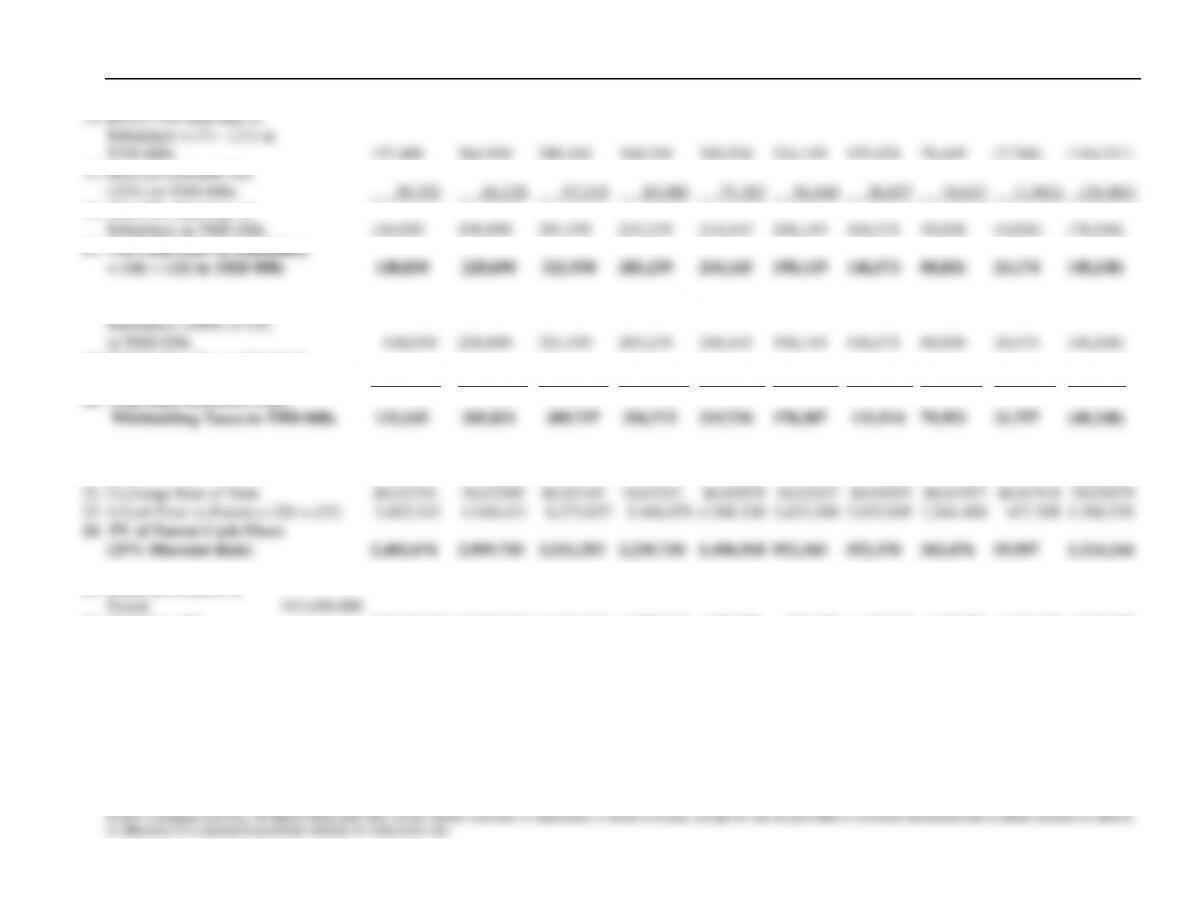

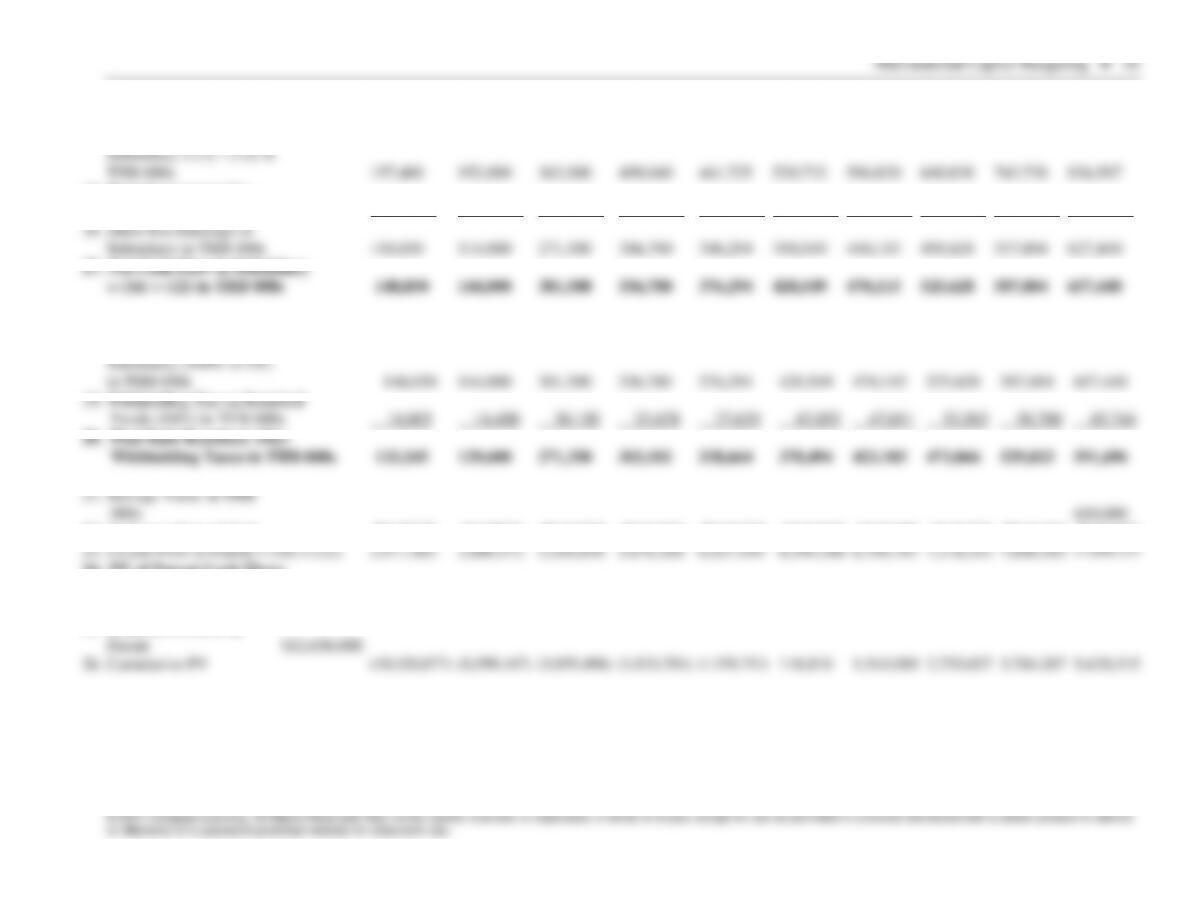

14. Before-Tax Earnings of

Subsidiary = (7) – (13) in

THB 000s

157,400

264,920

389,240

340,318

285,526

224,159

155,428

78,449

(7,768)

(104,331)

15. Host Government Tax

(25%) in THB 000s

39,350

66,230

97,310

85,080

71,382

56,040

38,857

19,612

(1,942)

(26,083)

16. After-Tax Earnings of

Subsidiary in THB 000s

118,050

198,690

291,930

255,239

214,145

168,119

116,571

58,836

(5,826)

(78,248)

17. Net Cash Flow to Subsidiary

= (16) + (12) in THB 000s

148,050

228,690

321,930

285,239

244,145

198,119

146,571

88,836

24,174

(48,248)

18. Thai Baht Remitted by

Subsidiary (100% of CF)

in THB 000s

148,050

228,690

321,930

285,239

244,145

198,119

146,571

88,836

24,174

(48,248)

19. Withholding Tax on Remitted

Funds (10%) in THB 000s

14,805

22,869

32,193

28,524

24,414

19,812

14,657

8,884

2,417

—

20. Thai Baht Remitted After

Withholding Taxes in THB 000s

133,245

205,821

289,737

256,715

219,730

178,307

131,914

79,953

21,757

(48,248)

21. Salvage Value in THB

000s

650,000

22. Exchange Rate of Baht

$0.02254

$0.02209

$0.02165

$0.02121

$0.02079

$0.02037

$0.01997

$0.01957

$0.01918

$0.01879

23. $ Cash Flow to Parent = (20) × (22)

3,003,342

4,546,421

6,272,057

5,446,070

4,568,230

3,632,900

2,633,905

1,564,480

417,208

1,308,530

24. PV of Parent Cash Flows

(25% Discount Rate)

2,402,674

2,909,710

3,211,293

2,230,710

1,496,918

952,343

552,370

262,476

55,997

1,214,244

25. Initial Investment by

Parent

$12,650,000

26. Cumulative PV

(10,247,326)

(7,337,617)

(4,126,323)

(1,895,613)

(398,695)

553,648

1,106,018

1,368,494

1,424,490

2,638,735

Answer to Question c:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

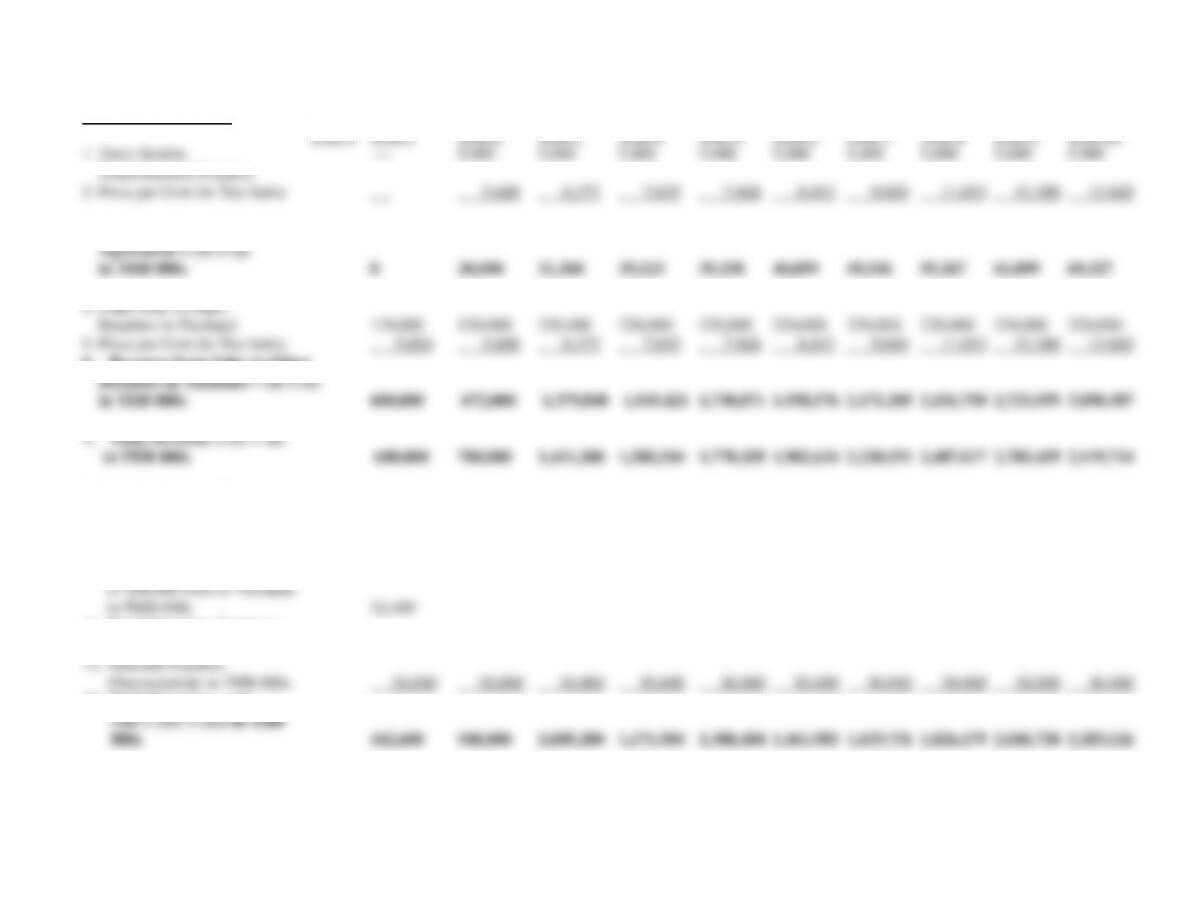

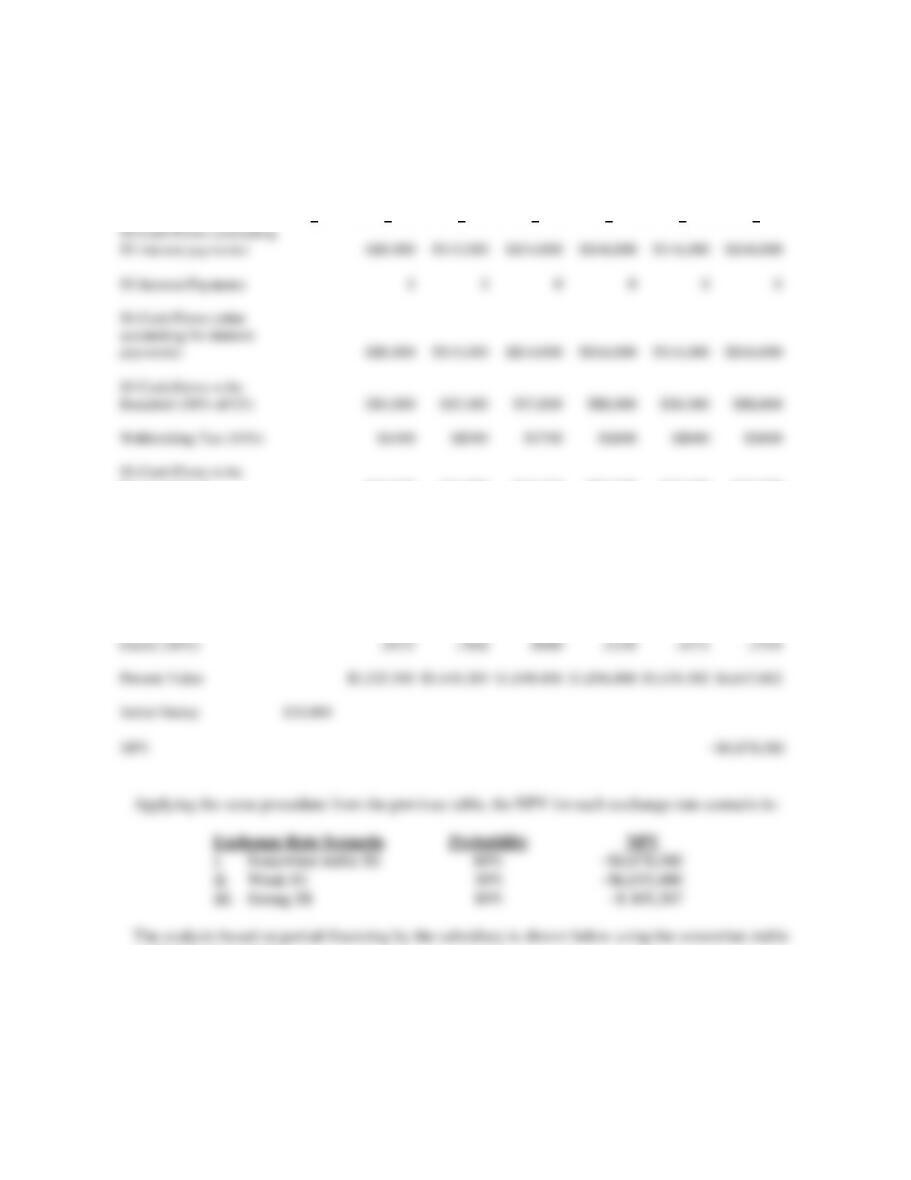

1. Units Sold to

Entertainment Products

—

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

2. Price per Unit (in Thai baht)

—

5,600

6,272

7,025

7,868

8,812

9,869

11,053

12,380

13,865

3. Revenue from Contractual

Agreement = (1) × (2)

in THB 000s

0

28,000

31,360

35,123

39,338

44,059

49,346

55,267

61,899

69,327

4. Units Sold to Other

Retailers in Thailand

120,000

120,000

220,000

220,000

220,000

220,000

220,000

220,000

220,000

220,000

5. Price per Unit (in Thai baht)

5,000

5,600

6,272

7,025

7,868

8,812

9,869

11,053

12,380

13,865

6. Revenue from Sales to Other

Retailers in Thailand = (4) × (5)

in THB 000s

600,000

672,000

1,379,840

1,545,421

1,730,871

1,938,576

2,171,205

2,431,750

2,723,559

3,050,387

7. Total Revenue = (3) + (6)

in THB 000s

600,000

700,000

1,411,200

1,580,544

1,770,209

1,982,634

2,220,551

2,487,017

2,785,459

3,119,714

8. Variable Cost per Unit (in

Thai baht)

3,500

3,920

4,390

4,917

5,507

6,168

6,908

7,737

8,666

9,706

9. Total Variable Cost = [(1) +

(4)] × (8) in THB 000s

420,000

490,000

987,840

1,106,381

1,239,146

1,387,844

1,554,385

1,740,912

1,949,821

2,183,800

10. Less Cost Savings from Production

of 108,000 Pairs in Thailand

in THB 000s

32,400

—

—

—

—

—

—

—

—

—

11. Fixed Operating Expenses

(in Thai baht 000s)

25,000

28,000

31,360

35,123

39,338

44,059

49,346

55,267

61,899

69,327

12. Noncash Expense

(Depreciation) in THB 000s

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

13. Total Expenses = (9) –

(10) + (11) + (12) in THB

000s

442,600

548,000

1,049,200

1,171,504

1,308,484

1,461,903

1,633,731

1,826,179

2,041,720

2,283,126

Multinational Capital Budgeting ❖ 35

Answer to Question d:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

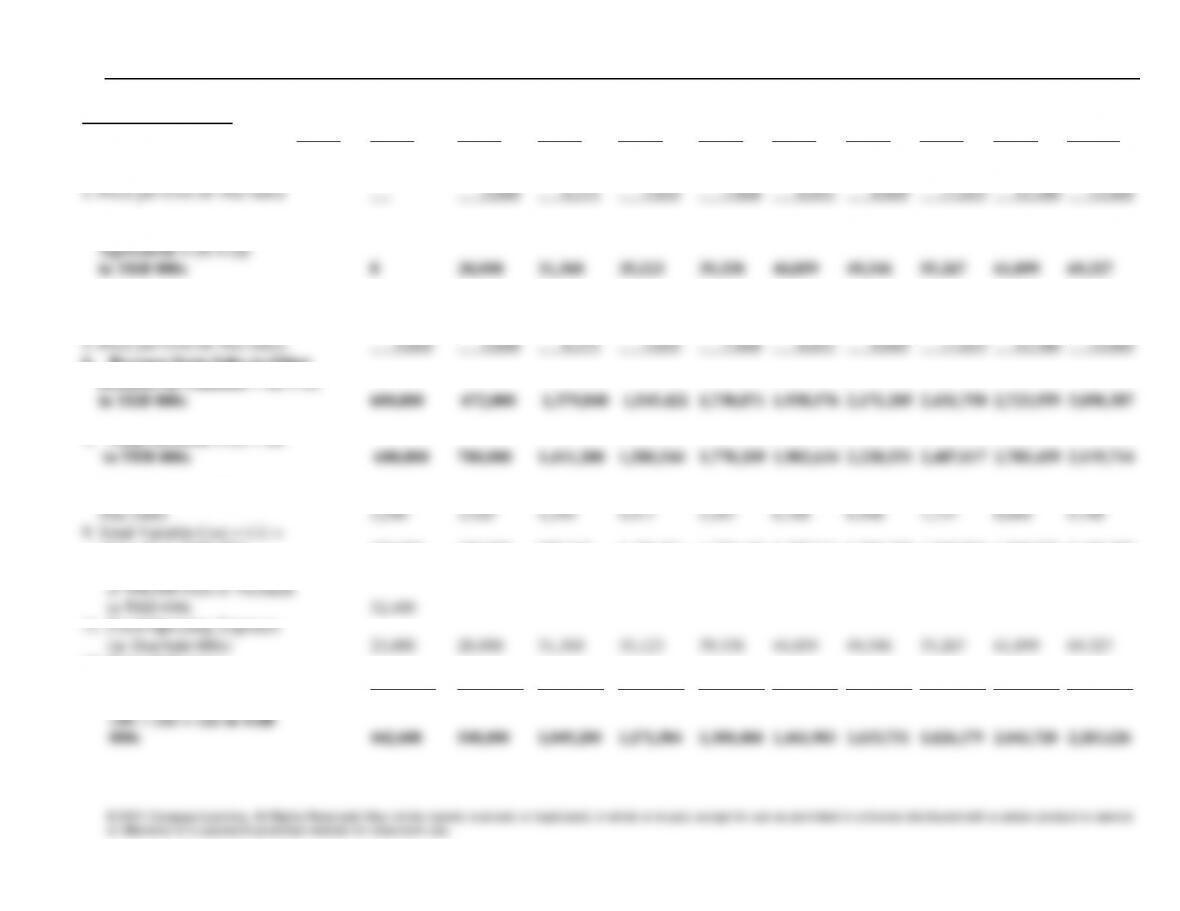

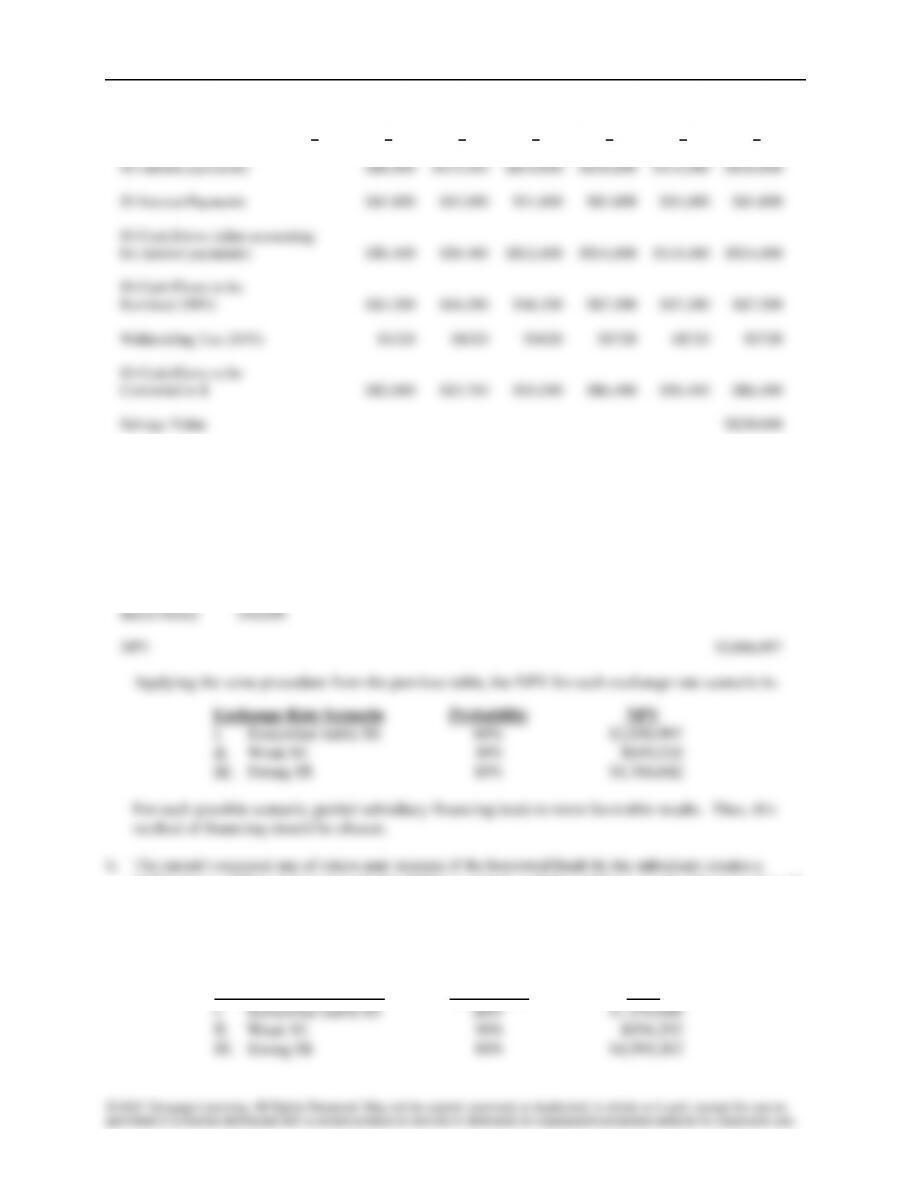

1. Units Sold to

Entertainment Products

—

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

2. Price per Unit (in Thai baht)

—

5,600

6,272

7,025

7,868

8,812

9,869

11,053

12,380

13,865

3. Revenue from Contractual

Agreement = (1) × (2)

in THB 000s

0

28,000

31,360

35,123

39,338

44,059

49,346

55,267

61,899

69,327

4. Units Sold to Other

Retailers in Thailand

120,000

120,000

220,000

220,000

220,000

220,000

220,000

220,000

220,000

220,000

5. Price per Unit (in Thai baht)

5,000

5,600

6,272

7,025

7,868

8,812

9,869

11,053

12,380

13,865

6. Revenue from Sales to Other

Retailers in Thailand = (4) × (5)

in THB 000s

600,000

672,000

1,379,840

1,545,421

1,730,871

1,938,576

2,171,205

2,431,750

2,723,559

3,050,387

7. Total Revenue = (3) + (6)

in THB 000s

600,000

700,000

1,411,200

1,580,544

1,770,209

1,982,634

2,220,551

2,487,017

2,785,459

3,119,714

8. Variable Cost per Unit (in

Thai baht)

3,500

3,920

4,390

4,917

5,507

6,168

6,908

7,737

8,666

9,706

9. Total Variable Cost = [(1) +

(4)] × (8) in THB 000s

420,000

490,000

987,840

1,106,381

1,239,146

1,387,844

1,554,385

1,740,912

1,949,821

2,183,800

10. Less Cost Savings from Production

of 108,000 Pairs in Thailand

in THB 000s

32,400

—

—

—

—

—

—

—

—

—

11. Fixed Operating Expenses

(in Thai baht 000s)

25,000

28,000

31,360

35,123

39,338

44,059

49,346

55,267

61,899

69,327

12. Noncash Expense

(Depreciation) in THB 000s

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

13. Total Expenses = (9) –

(10) + (11) + (12) in THB

000s

442,600

548,000

1,049,200

1,171,504

1,308,484

1,461,903

1,633,731

1,826,179

2,041,720

2,283,126

Multinational Capital Budgeting ❖ 37

Answer to Question e:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

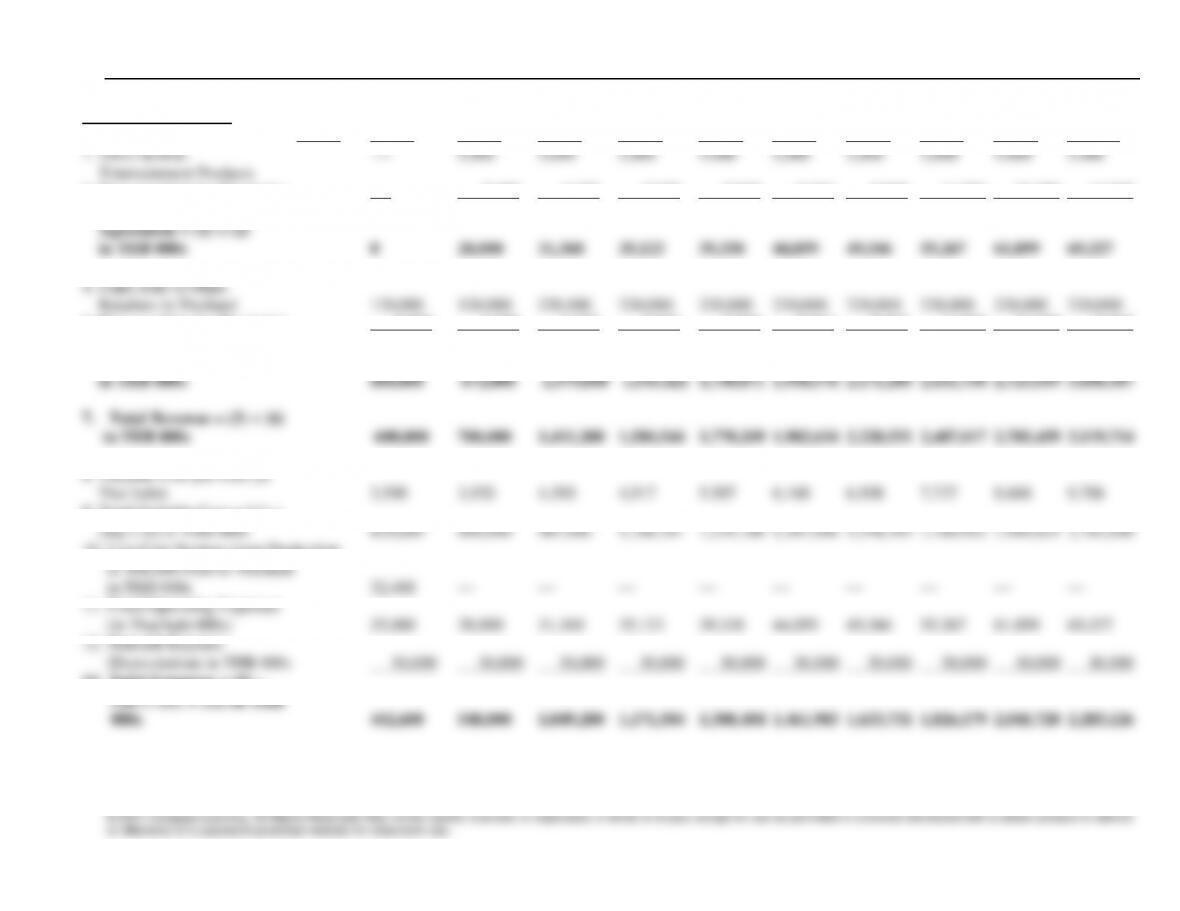

1. Units Sold to

Entertainment Products

—

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

5,000

2. Price per Unit (in Thai baht)

—

5,600

6,272

7,025

7,868

8,812

9,869

11,053

12,380

13,865

3. Revenue from Contractual

Agreement = (1) × (2)

in THB 000s

0

28,000

31,360

35,123

39,338

44,059

49,346

55,267

61,899

69,327

4. Units Sold to Other

Retailers in Thailand

120,000

120,000

220,000

220,000

220,000

220,000

220,000

220,000

220,000

220,000

5. Price per Unit (in Thai baht)

5,000

5,600

6,272

7,025

7,868

8,812

9,869

11,053

12,380

13,865

6. Revenue from Sales to Other

Retailers in Thailand = (4) × (5)

in THB 000s

600,000

672,000

1,379,840

1,545,421

1,730,871

1,938,576

2,171,205

2,431,750

2,723,559

3,050,387

7. Total Revenue = (3) + (6)

in THB 000s

600,000

700,000

1,411,200

1,580,544

1,770,209

1,982,634

2,220,551

2,487,017

2,785,459

3,119,714

8. Variable Cost per Unit (in

Thai baht)

3,500

3,920

4,390

4,917

5,507

6,168

6,908

7,737

8,666

9,706

9. Total Variable Cost = [(1) +

(4)] × (8) in THB 000s

420,000

490,000

987,840

1,106,381

1,239,146

1,387,844

1,554,385

1,740,912

1,949,821

2,183,800

10. Less Cost Savings from Production

of 108,000 Pairs in Thailand

in THB 000s

32,400

—

—

—

—

—

—

—

—

—

11. Fixed Operating Expenses

(in Thai baht 000s)

25,000

28,000

31,360

35,123

39,338

44,059

49,346

55,267

61,899

69,327

12. Noncash Expense

(Depreciation) in THB 000s

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

30,000

13. Total Expenses = (9) –

(10) + (11) + (12) in THB

000s

442,600

548,000

1,049,200

1,171,504

1,308,484

1,461,903

1,633,731

1,826,179

2,041,720

2,283,126

Solution to Supplemental Case: North Star Company

a. The analysis based on total parent financing is shown below using the somewhat stable exchange rate

scenario (in 1,000s):

0 1 2 3 4 5 6

Converted to $ S$3,600 S$4,500 S$6,300 S$7,200 S$7,200 S$7,200

Salvage Value S$30,000

Exchange Rate of S$ $.50 $.51 $.48 $.50 $.52 $.48

$ Cash Flows $1,800 $2,295 $3,024 $3,600 $3,744 $17,856

Present Value Interest

exchange rate scenario.

Multinational Capital Budgeting ❖ 40

(Cash amounts in thousands)

0 1 2 3 4 5 6

S$ Cash Flows (excluding

Exchange Rate of S$ $.50 $.51 $.48 $.50 $.52 $.48

$ Cash Flows $1,440 $1,927.8 $2,678.4 $3,240 $3,369.6 $12,710.4

Present Value Interest

Factor (18%) .8475 .7182 .6096 .5158 .4371 .3704

Present Value $1,219.68 $1,384.16 $1,631.145 $1,671.84 $1,472.515 $4,702.848

higher degree of financial leverage for the MNC as a whole, which could increase the risk perception of

the MNC. If so, the discount rate used should reflect the higher required rate of return.

c. When using a 20 percent withholding tax instead of a 10 percent withholding tax, the results change

as follows (based on partial financing by the subsidiary):

Exchange Rate Scenario Probability NPV