If the government adopts a fixed exchange rate regime, or sets the percentage change in

the exchange rate equal to a constant, this will keep the inflation rate constant. The

drawback of this approach is that the home country’s inflation rate changes each time the

foreign country’s inflation rate changes. Therefore, if the foreign country experiences

Money Supply Target The inflation rate depends on the money growth rate and growth

in real income, derived from the quantity theory of money:

Here, the central bank sets the money growth rate equal to a value to achieve the desired

inflation rate. This means the central bank has virtually no discretion to change the

money growth rate in response to changes in output. The drawback of this approach is

that real income growth may be unstable, especially in the short run. If the money growth

rate is kept constant, this may lead to deviations in the inflation target, at least in the short

run.

Inflation Target plus Interest Rate Policy We observe another possible anchor, the

nominal interest rate from the Fisher effect:

π

H = iH − r*

As long as the world real interest rate is constant, there is a direct relationship between

nominal interest rates and inflation in the long run.

The Choice of a Nominal Anchor and Its Implications There are two important

implications we can draw from the regime choices given previously. First, choosing more

than one target is problematic. Often, the regimes will call for different policies. We can

APPLICATION

Nominal Anchors in Theory and Practice

The adoption of targets increased dramatically in the 1990s, replacing regimes that had

no nominal anchor previously. The number of countries using both exchange rate and

inflation targets has increased. Also, several countries use more than one target, through

monitoring a range, rather than an explicit target.

Most of these policies have been credible, owing mainly to political changes that have

6 Conclusions

This chapter uses arbitrage conditions in the goods market and the foreign exchange

market to develop a theory of long-run exchange rate determination known as the

monetary approach. Using the theory of PPP from this chapter, combined with UIP from

Teaching Tips

Teaching Tip 1: The data for the Big Mac PPP test in the Excel workbook for this

chapter can also be used to calculate real exchange rates since qgUS/F = (E$/FORPgFOR)/PgUS,

where FOR is the foreign country. Assign each student a country, and have that student

Teaching Tip 2: Students are always fascinated by hyperinflations. Some of the best

stories come from the German interwar period. Have your students track down tales of

how behavior changed during this period. Here is a couple to get you started.

Teaching Tip 3: When we think of money, we usually think of currency issued by the

central bank or checkable deposits. But there are also private currencies in limited use

around the world. The website of the E. F. Schumacher Society includes a link to issuers

Teaching Tip 4: A paper by Joan Sweeney and Richard James Sweeney discussed the

authors’ experiences as part of a babysitting cooperative in the late 1970s (“Monetary

Theory and the Great Capitol Hill Baby Sitting Co-op Crisis: Comment,” Sweeney, Joan,

IN–CLASS PROBLEMS

1. Suppose that two countries, Brazil and Mexico, produce bananas. Brazil uses the real,

Mexico uses the peso. In Mexico, bananas sell for 10 pesos per pound of bananas.

The exchange rate is 0.5 reals per peso, Ereals/pesos = 0.5. The peso–dollar exchange

rate is Epesos/$ = 10.

a. If LOOP holds, what is the price of bananas in Brazil? What is the price in the

United States?

Answer: The prices implied by LOOP are as follows:

b. Suppose the price of bananas in Brazil is 5.5 reals per pound. At the same time,

the price of bananas in the United States is $1.00 per pound. Based on this

information, where does LOOP hold?

Answer: LOOP holds in the United States but not in Brazil. In the United States,

c. How will banana traders respond to the previous situation? In which markets will

traders buy bananas? Where will they sell them? What will happen to the prices of

bananas in Mexico, Brazil, and the United States?

Answer: Banana traders will buy in Mexico and the United States and sell in

2. For each of the following goods and services, indicate whether you expect LOOP to

hold. Explain briefly why you believe each good or service satisfies the assumptions

necessary for LOOP to hold.

a. Wheat

Answer: LOOP holds. Because wheat is not differentiated and traded in

b. Child care

Answer: LOOP does not hold. In most cases, child care is a nontraded good. It is

c. Automobiles

Answer: LOOP does not hold. Because automobiles are differentiated according

d. Milk

Answer: LOOP does not hold. Because milk is not differentiated, the market is

e. MP3 players

Answer: LOOP does not hold. Because MP3 players are differentiated according

f. Attorney services

Answer: LOOP does not hold. Attorney services are a nontraded service. It is

3. PPP is the macroeconomic counterpart to LOOP. Suppose the assumptions needed for

LOOP hold. Are there situations in which PPP may not hold when LOOP does?

Explain briefly.

Answer: Yes, there are situations in which LOOP holds but PPP does not. Recall that

4. Using the fundamental equations from the simple monetary approach, describe how

each of the following will affect the home and foreign price level, real money

balances, and the exchange rate, EH/F. Also, state whether the home currency

appreciates or depreciates for each.

a. An increase in home money supply

b. An increase in the foreign money supply

Answer: There is an increase in the foreign price level and a decrease in the

c. An increase in home real income

Answer: There is a decrease in the home price level and a decrease in the

d. A decrease in foreign real income

Answer: There is an increase in the foreign price level and a decrease in the

5. Using the fundamental equations from the general monetary approach, describe how

each of the following will affect the home and foreign price level, real money

balances, and the exchange rate, EH/F. Also, state whether the home currency

appreciates or depreciates for each.

a. A decrease in the foreign money supply

Answer: There is a decrease in the foreign price level and an increase in the

b. A decrease in home real income

Answer: There is an increase in the home price level and an increase in the

c. A decrease in the foreign nominal interest rate

Answer: There is an increase in foreign demand for real money balances, leading

6. This question considers long-run policies in Turkey relative to its largest trading

partner: Europe. Assume Turkey’s money growth rate is currently 15% and Turkey’s

output growth is 9%. Europe’s money growth rate is 4% and its output growth is 3%.

For the following questions, use the conditions associated with the simple monetary

model. Treat Turkey as the home country and define the exchange rate as Turkish lira

per euro, EL/€.

a. Calculate the inflation rate in Turkey.

b. Calculate the inflation rate in Europe.

c. Calculate the expected rate of depreciation in the Turkish lira relative to the euro.

d. Suppose the central bank of the Republic of Turkey decreases the money growth

rate from 15% to 11%. If nothing in Europe changes, what is the new inflation

rate in Turkey?

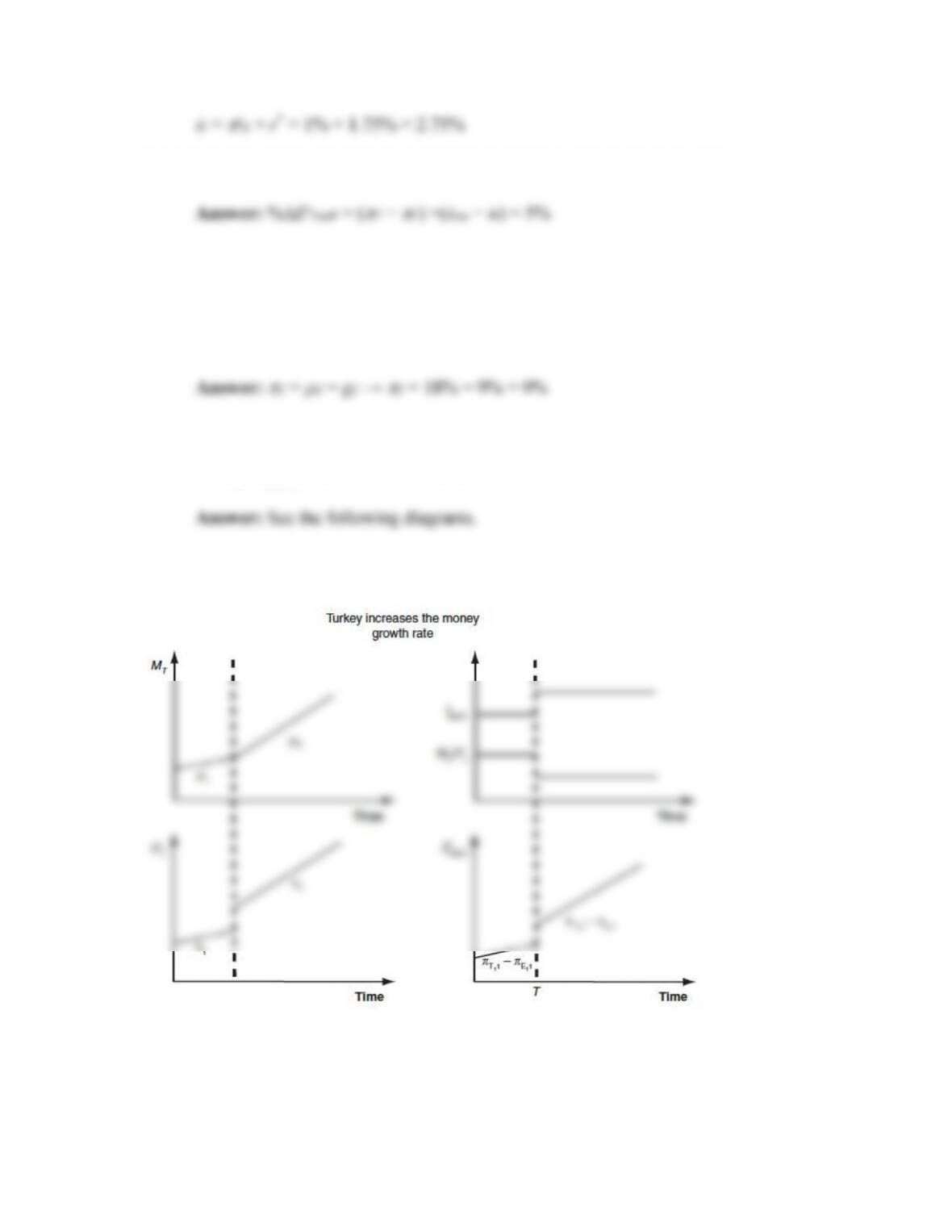

e. Illustrate how the change in (d) affects the following variables: MT, PT, real

money supply, and EL/. over time.

Answer: See the following figures.

f. Suppose the central bank of the Republic of Turkey sought to implement policy

that would cause the Turkish lira to appreciate relative to the euro. What ranges of

the money growth rate (assuming positive values) would allow the central bank to

achieve this objective? What range of values does this imply for Turkey’s

inflation rate?

Answer: Objective: %∆Eelira/€ < 0%

*T − gT) − (

7. This question follows from the analysis of Turkey and Europe in Question 6. Assume

Turkey’s money growth rate is currently 15% and Turkey’s output growth is 9%.

Europe’s money growth rate is 4% and its output growth is 3%. Also, assume the

world real interest rate is 1.75%. For the questions below, use the conditions

associated with the general monetary model. Treat Turkey as the home country and

define the exchange rate as Turkish lira per euro, EL/€.

a. Calculate the nominal interest rate in Turkey and in Europe.

Answer: From the Fisher effect:

ilira =

π

eT + r* = 6% + 1.75% = 7.75%

i€ =

π

eE + r* = 1% + 1.75% = 2.75%

b. Calculate the expected rate of depreciation in the Turkish lira relative to the euro.

c. Suppose the central bank of the Republic of Turkey increases the money growth

rate from 15% to 18%. If nothing in Europe changes, what is the new inflation

rate in Turkey?

d. Illustrate how the change in (c) affects the following variables: MT, PT, real

money supply, iT, and EL/€ over time.

e. Suppose Turkey wants to maintain a fixed exchange rate relative to the euro.

What money growth rate and nominal interest rate would achieve this objective?

Answer: Objective: %∆Eelira/€ = 0%

*T − gT) − (

8. This question considers long-run policies in Mexico relative to Canada. Assume

Mexico’s money growth rate is currently 4% and its inflation rate is 2%. Canada’s

money growth rate is 6% with 3.25% inflation rate. The world real interest rate is

0.75%. For the following questions, use the conditions associated with the general

monetary model. Treat Mexico as the home country and define the exchange rate as

Mexican pesos per Canadian dollar, EM/C$.

a. Calculate the growth rate of real income in each country.

b. Calculate the nominal interest rate in each country.

eM + r* = 2% + 1.75% = 3.75%

iC$ =

π

c. Calculate the expected rate of depreciation in the Mexican peso relative to the

Canadian dollar. Is the peso appreciating or depreciating against the Canadian

dollar?

d. Suppose that Mexico’s central bank wants to maintain a fixed exchange rate

against the Canadian dollar. Assuming that nothing in Canada changes, what must

the central bank do to achieve this long-run objective? What money growth rate

for Mexico’s money supply will make this possible?

Answer: Objective: %∆Eepeso/C$ = 0%

*M − gM) − (

e. Calculate Mexico’s new inflation rate and nominal interest rate after this policy is

implemented.

*M =

*M − gM = 5.25% − 2% = 3.25% =

f. Now suppose that Canada’s inflation rate increases from 3.5% to 5%. If Mexico

wants to maintain the fixed exchange rate, what will happen to its inflation rate?

Answer: If Canada’s inflation rate increases from 3.25% to 5%, then Mexico will

have to increase its money growth rate to maintain the fixed exchange rate.

*M − gM) −

9. Consider data on annual inflation rates across countries over time (refer to Side Bar:

Nominal Anchors in Theory and Practice). How has the experience of advanced

countries differed from that of emerging markets and developing countries? What

might explain the increased use of nominal anchors? Which nominal anchors are most

common?

Answer: Advanced countries have experienced a steady decline in inflation since

10. Both the Federal Reserve in the United States and the European Central Bank monitor

growth in the money supply over time, but use nominal interest rates to implement

policy. Provide an example of a situation in which these two approaches to targeting

require different central bank responses. Provide an example in which these two

approaches are compatible. [Hint: Recall that prices are sticky in the short run, so

expected inflation and actual inflation may differ].

Answer: These two approaches will be incompatible if the central bank wishes to

target the nominal anchor in response to an unexpected change in real income growth.

11. Consider a country that has experienced a hyperinflation. In general, countries with

higher inflation rates tend to have less stability in the inflation rate, making it difficult

to forecast. If this country wants to reduce its inflation rate, state which of the

following monetary regimes is least likely to succeed: exchange rate target, money

supply target, nominal interest rate policy. Which approach is most likely to succeed?

Explain.

Answer: The nominal interest rate policy is least likely to succeed because it relies on

the central bank’s ability to control expected inflation. During a hyperinflation, even