3 (14) Exchange Rates I: The Monetary Approach in the Long Run

1. Discovering Data: In recent years China has been routinely accused of currency

manipulation. Use The Economist’s Big Mac Index to investigate these claims. Go to

http://www.economist.com/content/big-mac–index to access the full dataset.

Answers will depend on the data used. Here I use the January 2017 publication of the

raw index.

a. What is the most recent price of a Big Mac in China? What is the implied

yuan/dollar exchange rate from this price?

b. Does this measure suggest that the Chinese yuan is overvalued or undervalued

relative to the dollar? Why might this be beneficial to the Chinese economy?

c. The fundamental assumption of this index is that the cost of producing a Big Mac is

identical across countries. Why might this assumption be violated? How might this

violation affect your answer in part (b)?

Answer: There may be a number of factors of production that differ in price across

d. Which three countries are most undervalued relative to the U.S. dollar in the most

recent year? Which three are most overvalued?

2. Suppose that two countries, Vietnam and Côte d’Ivoire, produce coffee. The currency

unit used in Vietnam is the dong (VND). Côte d’Ivoire is a member of Communauté

Financière Africaine (CFA), a currency union of West African countries that use the

CFA franc (XOF). In Vietnam, coffee sells for 4,500 dong (VND) per pound. The

exchange rate is 40 VND per 1 CFA franc, EVND/XOF = 30.

a. If the law of one price holds, what is the price of coffee in Côte d’Ivoire,

measured in CFA francs?

Answer: According to LOOP, the price of coffee should be the same in both

markets:

b. Assume the price of coffee in Côte d’Ivoire is actually 160 CFA francs per pound

of coffee. Compute the relative price of coffee in Côte d’Ivoire versus Vietnam.

Where will coffee traders buy coffee? Where will they sell coffee in this case?

How will these transactions affect the price of coffee in Vietnam? In Côte

d’Ivoire?

Answer: With an exchange rate of 30 VND per 1 CFA franc, the

3. Consider each of the following goods and services. For each, identify whether the law

of one price will hold, and state whether the relative price, qgUS/Foreign, is greater than,

less than, or equal to 1. Explain your answer in terms of the assumptions we make

when using the law of one price.

a. Rice traded freely in the United States and Canada

b. Sugar traded in the United States and Mexico; the U.S. government imposes a

quota on sugar imports into the United States

c. The McDonald’s Big Mac sold in the United States and Japan

d. Haircuts in the United States and the United Kingdom

4. Use the table that follows to answer this question. Treat the country listed as the home

country, and the United States as the foreign country. Suppose the cost of the market

basket in the United States is PUS = $190. Check to see whether PPP holds for each of the

countries listed, and determine whether we should expect a real appreciation or real

depreciation for each country (relative to the United States) in the long run. For the

answer, create a table similar to the one shown and fill in the blank cells. (Hint: Use a

spreadsheet application such as Excel.)

Answer: See the following table. Note that the United States is treated as the foreign

country relative to each “home” country listed in the table.

Country

(currency

measured

in FX

units)

Per $,

EFX/$

Price of

Market

Basket

(in FX)

Price of U.S.

Basket in FX

(PUS times

EFX/$)

Real

Exchange

Rate

qCOUNTRY/US

Does

PPP

Hold?

(yes/no)

Is FX Currency

Overvalued or

Undervalued?

Is FX

Currency

Expected to

Have Real

Appreciation

or

Depreciation?

4.07

520

773.3

1.49

No

Real undervalued

Real exchange

depreciate

68.51

12,000

13016.9

1.084

No

Real exchange

depreciate

Mexico

(peso)

18.89

1,800

3589.1

1.99

No

Peso undervalued

Real exchange

rate will

depreciate

depreciate

101,347

4,000,000

19,225,930.00

4.81

No

Real exchange

appreciate

In the previous table:

• PPP holds only when the real exchange rate qCountry/US = 1. This implies that the

5. Table 3–1(14-1) in the text shows the percentage undervaluation or overvaluation in

the Big Mac, based on exchange rates in January 2016. The table that follows shows

the local currency price as well as the U.S. dollar price for the previous year in

January 2015. Suppose purchasing power parity holds in the long run, so that these

deviations would be expected to disappear. Suppose the local currency prices of the

Big Mac remained unchanged. Exchange rates on January 4, 2016, were as follows

(Data from: IMF):

Based on these data and Table 3–1(14-1), calculate the change in the exchange rate

from 2015 to 2016, and state whether the direction of change was consistent with the

PPP-implied exchange rate using the Big Mac Index. How might you explain the

failure of the Big Mac Index to correctly predict the change in the nominal exchange

rate between January 2015 and January 2016?

Country

Per U.S. $

Local Currency Price

Price in U.S. Dollars

Australia (A$)

0.73

5.3

4.32

3.91

13.5

5.32

1.38

5.7

4.64

6.83

34.5

5.38

Eurozone (euro)

0.92

3.68

4.26

India (rupee)

66.33

116.25

1.89

120.5

370

3.14

17.25

49

3.35

Sweden (krona)

8.35

40.7

4.97

In Local

Currency

In U.S.

$

Implied

by PPP

Actual,

January

2016

Over (+) /

Under (−)

Valuation

against

Dollar, %

Exchange

Rate

Actual,

January

2015

(Local

Currency

per U.S. $)

Percent

Change

January

2015–

January

2016

PPP Correct

or Not?

(1)

(2)

(3)

(4)

(5)

United States

$

4.93

4.93

—

—

—

—

—

—

Australia

A$

5.3

3.74

1.08

1.42

−24

0.73

94.5%

Correct,

3.91

larger

1.38

C$ depreciated

Denmark

krone

30

4.32

6.09

6.94

−12

6.83

1.6%

predicted

further

Eurozone

euro

3.72

4.99

0.75

0.93

−19

0.92

1%

predicted

66.33

predicted a

120.5

predicted

17.25

Answer:

Exchange rate (local currency per U.S. dollar)

Big Mac prices

We can see from the table that during this time, PPP could be used to correctly

Work It Out

You are given the following information. The current dollar–pound exchange rate is

$1.5 per pound. A U.S. basket that costs $100 would cost $120 in the United

Kingdom. For the next year, the Federal Reserve is predicted to keep U.S. inflation at

2% and the Bank of England is predicted to keep U.K. inflation at 3%. The speed of

convergence to absolute PPP is 15% per year.

b. What is the current U.S. real exchange rate, qUS/UK, with the United Kingdom?

Answer: The current real exchange rate is:

c. How much is the dollar overvalued/undervalued?

d. What do you predict the U.S. real exchange rate with the United Kingdom will be

in one year’s time?

Answer: We can use the information on convergence to compute the implied

8.35

is overvalued

and should

have

depreciated

according to

PPP, as it has

here

e. What is the expected rate of real depreciation for the United States (versus the

United Kingdom)?

Answer: From (d), the real exchange rate will decrease by 0.0375. Therefore, the

f. What is the expected rate of nominal depreciation for the United States (versus

the United Kingdom)?

g. What do you predict will be the dollar price of one pound a year from now?

Answer: The current nominal exchange rate is $1.5 per pound and we expect a

6. Describe how each of the following factors might explain why PPP is a better guide

for exchange rate movements in the long run versus the short run: (i) transactions

costs, (ii) nontraded goods, (iii) imperfect competition, (iv) price stickiness. As

markets become increasingly integrated, do you suspect PPP will become a more

useful guide in the future? Why or why not?

Answer: Each of these factors hinders trade more in the short run than in the long

run. Specifically, each is a reason to expect that the condition of frictionless trade is

not satisfied. For this reason, PPP is more likely to hold in the long run than in the

short run.

7. Consider two countries: Japan and South Korea. In 1996 Japan experienced relatively

slow output growth (1%), whereas South Korea had relatively robust output growth

(6%). Suppose the Bank of Japan allowed the money supply to grow by 2% each

year, while the Bank of Korea chose to maintain relatively high money growth of

15% per year.

For the following questions, use the simple monetary model (where L is constant).

You will find it easiest to treat South Korea as the home country and Japan as the

foreign country.

a. What is the inflation rate in South Korea? In Japan?

Answer:

b. What is the expected rate of depreciation in the Korean won relative to the

Japanese yen (¥)?

c. Suppose the Bank of Korea decreases the money growth rate from 15% to 12%. If

nothing in Japan changes, what is the new inflation rate in Korea?

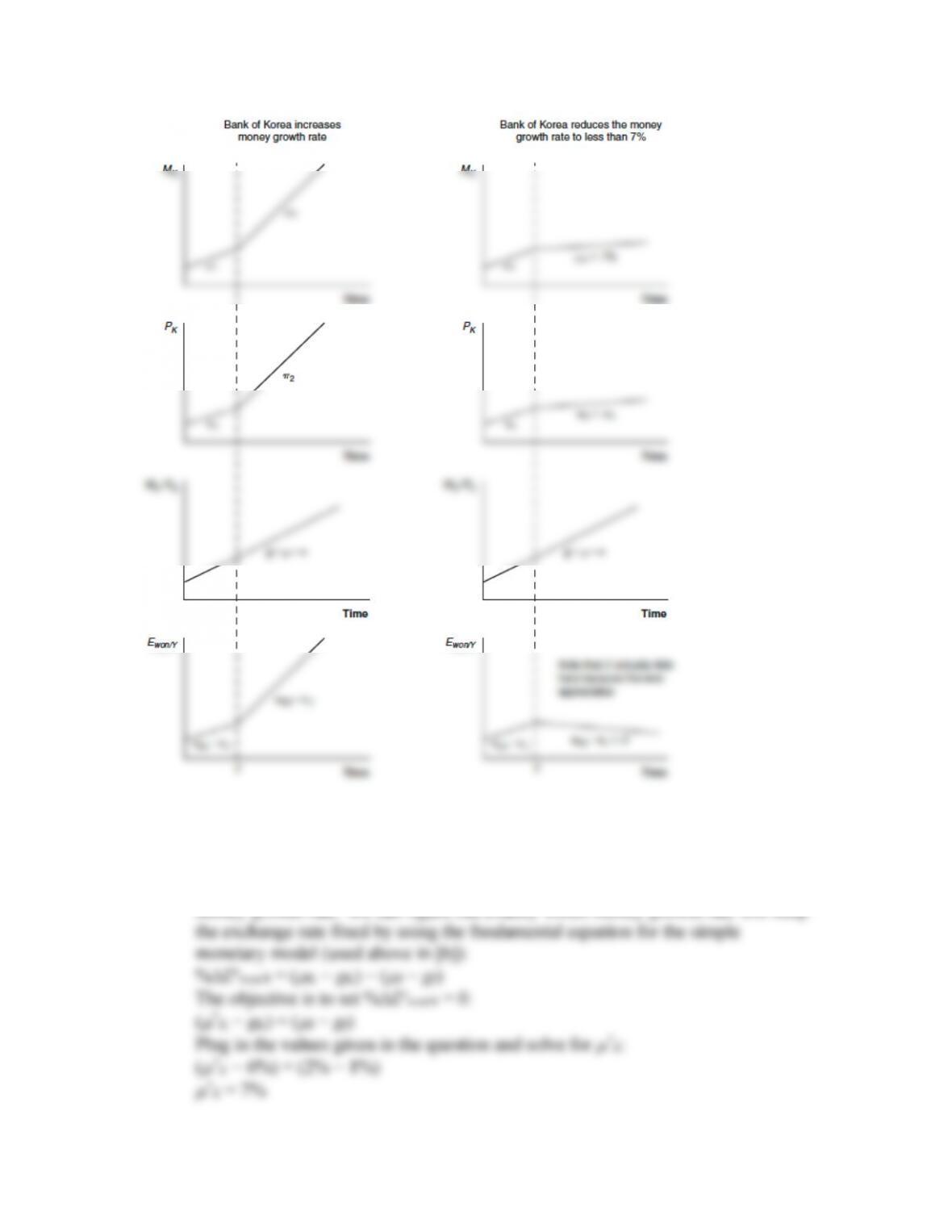

d. Using time series diagrams, illustrate how this increase in the money growth rate

affects the money supply MK, South Korea’s interest rate, prices PK, real money

supply, and Ewon/¥ over time. (Plot each variable on the vertical axis and time on

the horizontal axis.)

Answer: See the following diagrams.

e. Suppose the Bank of Korea wants to maintain an exchange rate peg with the

Japanese yen. What money growth rate would the Bank of Korea have to choose

to keep the value of the won fixed relative to the yen?

Answer: To keep the exchange rate constant, the Bank of Korea must lower its

money growth rate. We can figure out exactly which money growth rate will keep

f. Suppose the Bank of Korea sought to implement policy that would cause the

Korean won to appreciate relative to the Japanese yen. What ranges of the money

growth rate (assuming positive values) would allow the Bank of Korea to achieve

this objective?

Answer: Using the same reasoning as previously, the objective is for the won to

8. This question uses the general monetary model, where L is no longer assumed

constant and money demand is inversely related to the nominal interest rate. Consider

the same scenario described in the beginning of the previous question. In addition, the

bank deposits in Japan pay a 3% interest rate, i¥ = 3%.

a. Compute the interest rate paid on South Korean deposits.

Answer: Assuming that the relative PPP holds, the exchange rate depreciation

b. Using the definition of the real interest rate (nominal interest rate adjusted for

inflation), show that the real interest rate in South Korea is equal to the real

interest rate in Japan. (Note that the inflation rates you computed in the previous

question will be the same in this question.)

Answer:

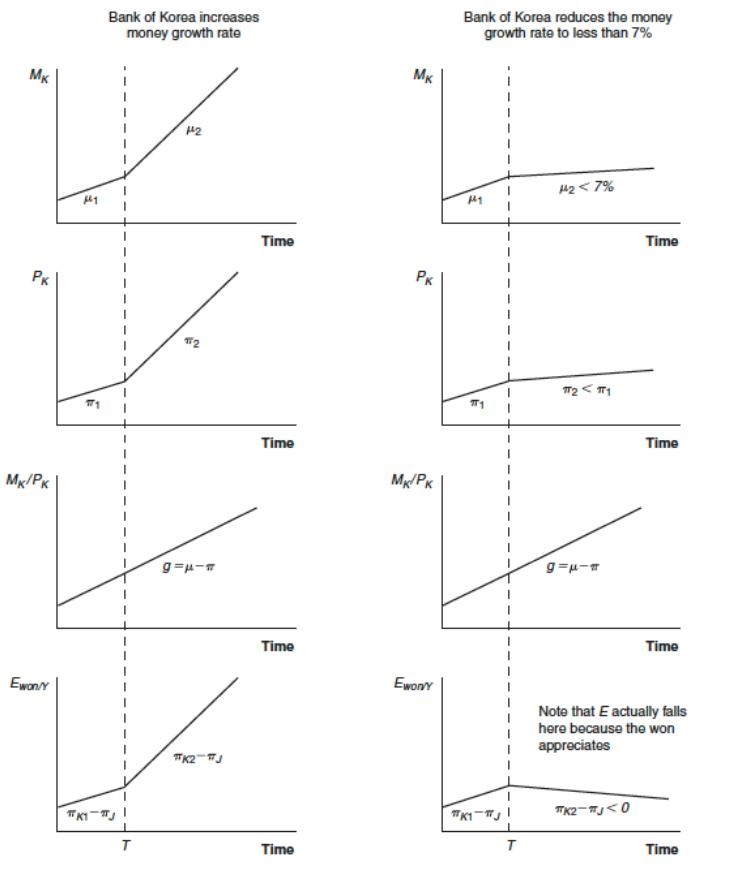

c. Suppose the Bank of Korea decreases the money growth rate from 15% to 12%

and the inflation rate falls proportionately (one for one) with this increase. If the

nominal interest rate in Japan remains unchanged, what happens to the interest

rate paid on South Korean deposits?

Answer: We know that the inflation rate in Korea will increase to 9%. We also

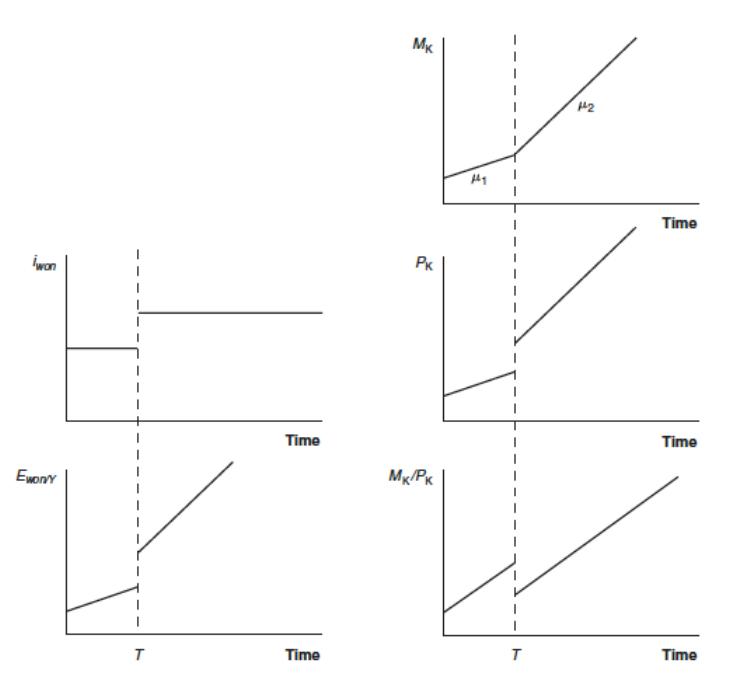

d. Using time series diagrams, illustrate how this decrease in the money growth rate

affects the money supply MK; South Korea’s interest rate; prices PK; real money

supply; and Ewon/¥ over time. (Plot each variable on the vertical axis and time on

the horizontal axis.)

Answer: See the following diagrams. As the interest rate rises due to expected

9. Both advanced economies and developing countries have experienced a decrease in

inflation since the 1980s (see Table 3-3[14-3] in the text). This question considers

how the choice of policy regime has influenced this global disinflation. Use the

monetary model to answer this question.

a. Consider a period when the Swiss Central Bank targeted its money growth rate to

achieve policy objectives. Suppose Switzerland has output growth of 2% and

money growth of 3% each year. What is Switzerland’s inflation rate in this case?

Describe how the Swiss Central Bank could achieve an inflation rate of 2% in the

long run through the use of a nominal anchor.

b. Consider a period when the Reserve Bank of New Zealand used an interest rate

target. Suppose the Reserve Bank of New Zealand maintains a 5% interest rate

target and the world real interest rate is 1.5%. What is the New Zealand inflation

rate in the long run? In 1997 New Zealand adopted a policy agreement that

required the bank to maintain an inflation rate no higher than 2.5%. What interest

rate targets would achieve this objective?

c. Consider a period when, prior to euro entry, the central bank of Lithuania

maintained an exchange rate band relative to the euro—at the time this was a

prerequisite for joining the Eurozone. The rules said that Lithuania had to keep its

exchange rate within ±15% of the central parity of 3.4528 litas per euro. Compute

the exchange rate values corresponding to the upper and lower edges of this band.

Suppose PPP holds. Assuming Eurozone inflation was 2% per year and inflation

in Lithuania was 6%, compute the PPP–implied rate of depreciation of the lita.

Could Lithuania maintain the band requirement? For how long? Does your

answer depend on where in the band the exchange rate currently sits? A primary

objective of the European Central Bank is price stability (low inflation) in the

current and future Eurozone. Is an exchange rate band a necessary or sufficient

condition for the attainment of this objective?

Answer: From relative PPP: πL = %∆Eelita/€ – π€. Plug in the inflation rates for the

10. Several countries that have experienced hyperinflation adopt dollarization as a way to

control domestic inflation. For example, Ecuador has used the U.S. dollar as its

domestic currency since 2000. What does dollarization imply about the exchange rate

between Ecuador and the United States? Why might countries experiencing

hyperinflation adopt dollarization? Why might they do this rather than just fixing

their exchange rate?

Answer: Dollarization implies a country is adopting dollar as its currency. Because

11. You are the central banker for a country that is considering the adoption of a new

nominal anchor. When you take the position as chairperson, the inflation rate is 5%

and your position as the central bank chairperson requires that you achieve a 2.5%

inflation target within the next year. The economy’s growth in real output is currently

1%. The world real interest rate is currently 1.5%. The currency used in your country

is the lira. Assume prices are flexible.

a. Why is having a nominal anchor important for you to achieve the inflation target?

What is the drawback of using a nominal anchor?

Answer: The central bank uses a nominal anchor to control the inflation rate.

b. What is the growth rate of the money supply in this economy? If you choose to

adopt a money supply target, which money supply growth rate will allow you to

meet your inflation target?

c. Suppose the inflation rate in the United States is currently 2% and you adopt an

exchange rate target relative to the U.S. dollar. Compute the percent

appreciation/depreciation in the lira needed for you to achieve your inflation

target. Will the lira appreciate or depreciate relative to the U.S. dollar?

d. Your final option is to achieve your inflation target using interest rate policy.

Using the Fisher equation, compute the current nominal interest rate in your

country. What nominal interest rate will allow you to achieve the inflation target?