Chapter 13 (2)

National Income Accounting and

the Balance of Payments

◼ Chapter Organization

The National Income Accounts

National Product and National Income

Capital Depreciation and International Transfers

Gross Domestic Product

National Income Accounting for an Open Economy

Consumption

Investment

Government Purchases

The National Income Identity for an Open Economy

An Imaginary Open Economy

The Current Account and Foreign Indebtedness

Saving and the Current Account

Private and Government Saving

Case Study: The Mystery of the Missing Deficit

The Balance of Payments Accounts

Examples of Paired Transactions

The Fundamental Balance of Payments Identity

The Current Account, Once Again

The Capital Account

The Financial Account

Net Errors and Omissions

Official Reserve Transactions

Case Study: The Assets and Liabilities of the World’s Biggest Debtor

Summary

70 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Tenth Edition

◼ Chapter Overview

This chapter introduces the international macroeconomics section of the text. The chapter begins with

a brief discussion of the focus of international macroeconomics. You may want to contrast the type of

topics studied in international trade, such as the determinants of the patterns of trade and the gains from

trade, with the issues studied in international finance, which include unemployment, savings, trade

imbalances, and money and the price level. You can then “preview” the manner in which the theory taught

in this section of the course will enable students to better understand important and timely issues such as

the U.S. trade deficit, the experience with international economic coordination, the European Economic

and Monetary Union, and the financial crises in Asia and other developing countries.

The core of this chapter is a presentation of national income accounting theory and balance of payments

accounting theory. A solid understanding of these topics proves useful in other parts of this course when

students need to understand concepts such as the intertemporal nature of the current account or the way in

which net export earnings are required to finance external debt. Students will have had some exposure to

closed economy national income accounting theory in previous economics courses. You may want to

stress that GNP can be considered the sum of expenditures on final goods and services or, alternatively,

the sum of payments to domestic factors of production. You may also want to explain that separating GNP

into different types of expenditures allows us to focus on the different determinants of consumption,

investment, government spending, and net exports.

The relationships among the current account, savings, investment, and the government budget deficit

should be emphasized. It may be useful to draw an analogy between the net savings of an individual and

the net savings of a country to reinforce the concept of the current account as the net savings of an

economy. Extending this analogy, you may compare the net dissavings of many students when they are

in college, acquiring human capital, and the net dissavings of a country that runs a current account deficit

to build up its capital stock. You may also want to contrast a current account deficit that reflects a lot of

investment with a current account deficit that reflects a lot of consumption to make the point that all

current account deficits are not the same nor do they all warrant the same amount of concern. Balance of

payments accounting will be new to students. The text stresses the double-entry bookkeeping aspect of

balance of payments accounting. The 2012 U.S. balance of payments accounts provide a concrete example

of these accounts.

Note that the book uses the new current/financial/capital account definitions. The old capital account is

now the financial account. The current account is the same except that unilateral asset transfers (debt

forgiveness or immigrants moving wealth with them) are now in the new capital account. Credits and

debits are marked in the same manner; if money comes into a country, it is a credit. A description of the

changes along with revised estimates for 1982–1998 can be found in the article by Christopher Bach

(see references). These changes were made in conjunction with the IMF’s new standards. A description

of these new standards can be found in the Survey of Current Business article listed at the end of the

references.

The chapter also includes a discussion of official reserve transactions. You may want to stress that, from

the standpoint of financing the current account, these official capital flows play the same role as other

financial flows. You may also briefly mention that there are additional macroeconomic implications of

central-bank foreign asset transactions. A detailed discussion of these effects will be presented in

Chapter 18(7).

The chapter concludes with a case study examining the foreign assets and liabilities of the United States. A

breakdown of the different components of the U.S. international investment position is presented. Of

particular importance is that although the United States is the world’s largest debtor, American debt

relative to American GDP is significantly lower than many other countries. The chapter also includes a

Chapter 13(2) National Income Accounting and the Balance of Payments 71

discussion of how the value of a nation’s foreign debt may be affected by exchange rate changes, a nice

segue into the next chapter relating exchange rates and the asset market.

◼ Answers to Textbook Problems

1. No, because the product produced in the year 2013 is a part of that particular year’s GDP. Hence, it cannot be

included while calculating the GDP for 2014.

We cannot take the value of bonds and stocks sold in the market into account while evaluating the

GDP. This is because the sale of stocks and bonds only transfers the ownership of the assets. This

does not add any production value to the country’s GDP. Hence, it is excluded.

2. Equation 13(2)-2 can be written as CA = (Sp – I) + (T – G). Higher U.S. barriers to imports may have

little or no impact upon private savings, investment, and the budget deficit. If there were no effect on

these variables, then the current account would not improve with the imposition of tariffs or quotas.

It is possible to tell stories in which the effect on the current account goes either way. For example,

investment could rise in industries protected by the tariff, worsening the current account. (Indeed,

tariffs are sometimes justified by the alleged need to give ailing industries a chance to modernize

3. a. The purchase of the German stock is a debit in the U.S. financial account. There is a

corresponding credit in the U.S. financial account when the American pays with a check on

b. Again, there is a U.S. financial account debit as a result of the purchase of a German stock by an

American. The corresponding credit in this case occurs when the German seller deposits the U.S.

check in his German bank and that bank lends the money to a German importer (in which case

c. The foreign exchange intervention by the Korean government involves the sale of a U.S. asset,

the dollars it holds in the United States, and thus represents a debit item in the U.S. financial

account. The Korean citizens who buy the dollars may use them to buy American goods, which

d. Suppose the company issuing the traveler’s check uses a checking account in France to make

payments. When this company pays the French restaurateur for the meal, its payment represents

e. There is no credit or debit in either the financial or the current account because there has been no

market transaction.

72 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Tenth Edition

4. The purchase of the answering machine is a current account debit for New York and a current

account credit for New Jersey. When the New Jersey Company deposits the money in its New York

bank, there is a financial account credit for New York and a corresponding debit for New Jersey.

If the transaction is in cash, then the corresponding debit for New Jersey and credit for New York

5. a. Because noncentral bank financial inflows fell short of the current account deficit by

$500 million, the balance of payments of Pecunia (official settlements balance) was

b. By dipping into its foreign reserves, the central bank of Pecunia financed the portion of the

country’s current account deficit not covered by private financial inflows. Only if foreign

central banks had acquired Pecunian assets could the Pecunian central bank have avoided using

c. If foreign official capital inflows to Pecunia were $600 million, the central bank now increased

its foreign assets by $100 million. Put another way, the country needed only $1 billion to

cover its current account deficit, but $1.1 billion flowed into the country (500 million private and

600 million from foreign central banks). The Pecunian central bank must, therefore, have used

the extra $100 million in foreign borrowing to increase its reserves. The balance of payments is

d. Along with noncentral bank transactions, the accounts would show an increase in foreign official

reserve assets held in Pecunia of $600 million (a financial account credit, or inflow)

and an increase Pecunian official reserve assets held abroad of $100 million (a financial

account debit, or outflow). Of course, total net financial inflows of $1 billion just cover the

current account deficit.

6. The exchange rate represents the amount of domestic currency (e.g. Rupee) needed to buy one unit of

foreign currency (e.g. US$). Higher CAD shows higher import over export. To finance these imports

the domestic economy demands more dollars. This may cause the downward movement of domestic

7. The official settlements balance, also called the balance of payments, shows the net change in

international reserves held by U.S. government agencies, such as the Federal Reserve and the

Treasury, relative to the change in dollar reserves held by foreign government agencies. This account

provides a partial picture of the extent of intervention in the foreign exchange market. For example,

Chapter 13(2) National Income Accounting and the Balance of Payments 73

8. A country could have a current account deficit and a balance of payments surplus at the same time

if the financial and capital account surpluses exceeded the current account deficit. Recall that the

balance of payments surplus equals the current account surplus plus the financial account surplus plus

the capital account surplus. If, for example, there is a current account deficit of $100 million, but

there are large capital inflows and the financial account surplus is $102 million, then there will be a

$2 million balance of payments surplus.

This problem can be used as an introduction to intervention (or lack thereof) in the foreign exchange

market, a topic taken up in more detail in Chapter 18(7). The government of the United States did not

intervene in any appreciable manner in the foreign exchange markets in the first half of the 1980s.

9. If both assets and liabilities pay 5 percent, then the net payments on the net foreign debt would be

1.25 percent. While not trivial, this is probably not too bad a burden. At 100 percent net foreign debt-

10. The United States receives a substantially higher rate of return on its assets held abroad than

foreigners are earning on U.S. assets. One reason is that a substantial amount of foreign assets are in

low-interest-rate Treasury bills.

11. The currency depreciation will make the domestic commodity cheaper to foreign buyers. Hence, the

export of both countries will increase compared to import. Since the devaluation of Chinese Yuan is

more, it is expected that the Chinese export will be more than that of India. This would reduce the

CAD. Since the export of China is more than that of India, the CAD will remain relatively high in

India in comparison to China.

The capital account surplus may cause the CAD in China. This is because an increase in investment

12. To incorporate capital gains or losses, one would have to consider these valuation changes as part of

national income. We would thus change Equation 13(2)-1 to read:

where “GAIN” is defined as the net capital gain on net foreign assets. Although such an adjustment

would more directly measure the change in net foreign assets, it would not be as useful a measure of

the income of a country. Nonrealized gains do not show up as income, nor do they provide the means

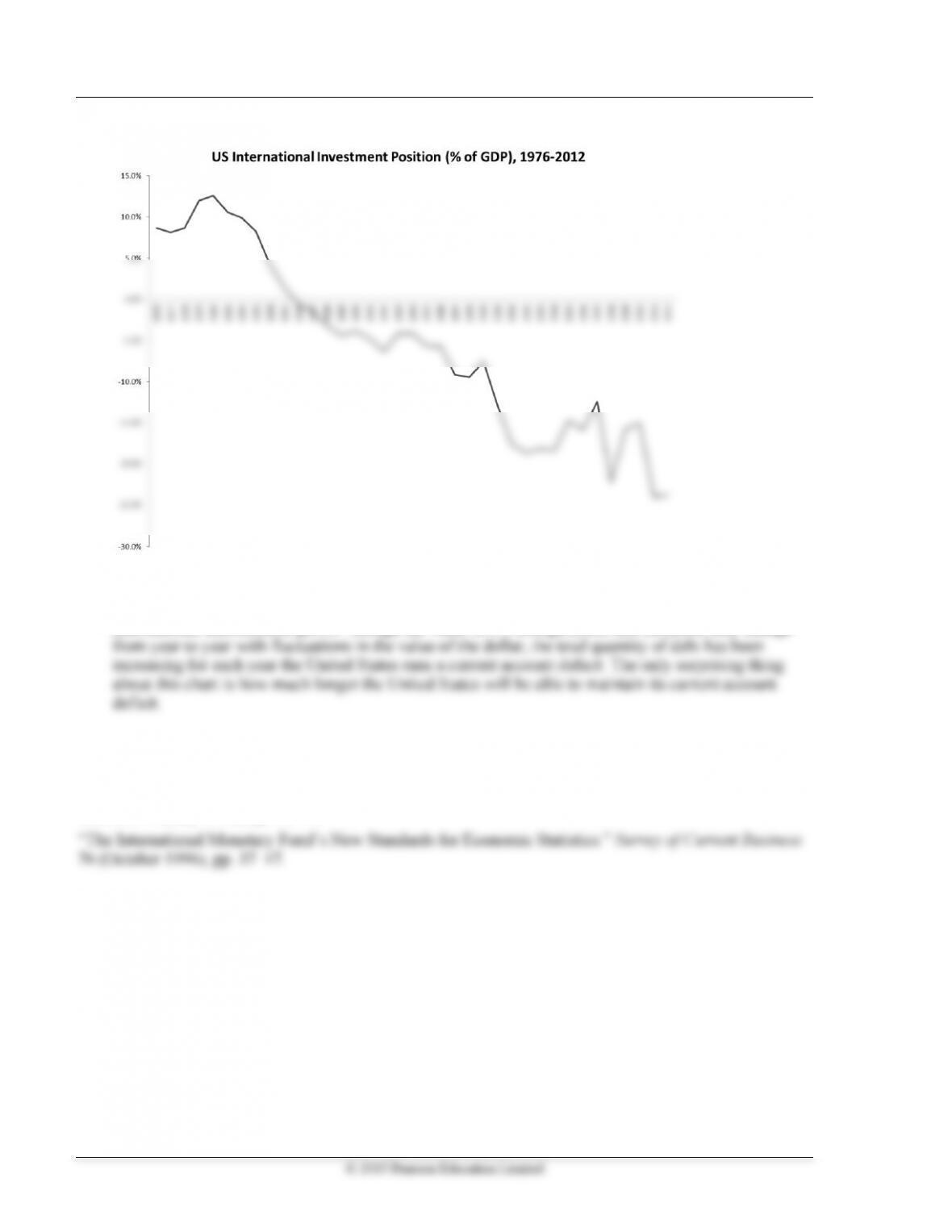

13. Collecting data on the U.S. international investment position and nominal GDP over the period 1976–

2012 allows us to generate the following chart:

74 Krugman/Obstfeld/Melitz • International Economics: Theory & Policy, Tenth Edition

As the U.S. current account has been negative since 1980, it should not be surprising that the U.S.

international investment position has been declining since 1980. To finance a current account deficit,

a country must borrow from abroad. Thus, every year a country runs a current account deficit, its

international indebtedness grows. Though the value of US foreign assets and liabilities may change

◼ References

Christopher Bach. “U.S. International Transactions, Revised Estimates for 1982–1998.” Survey of Current

Business 79 (July 1999), pp. 60–74.