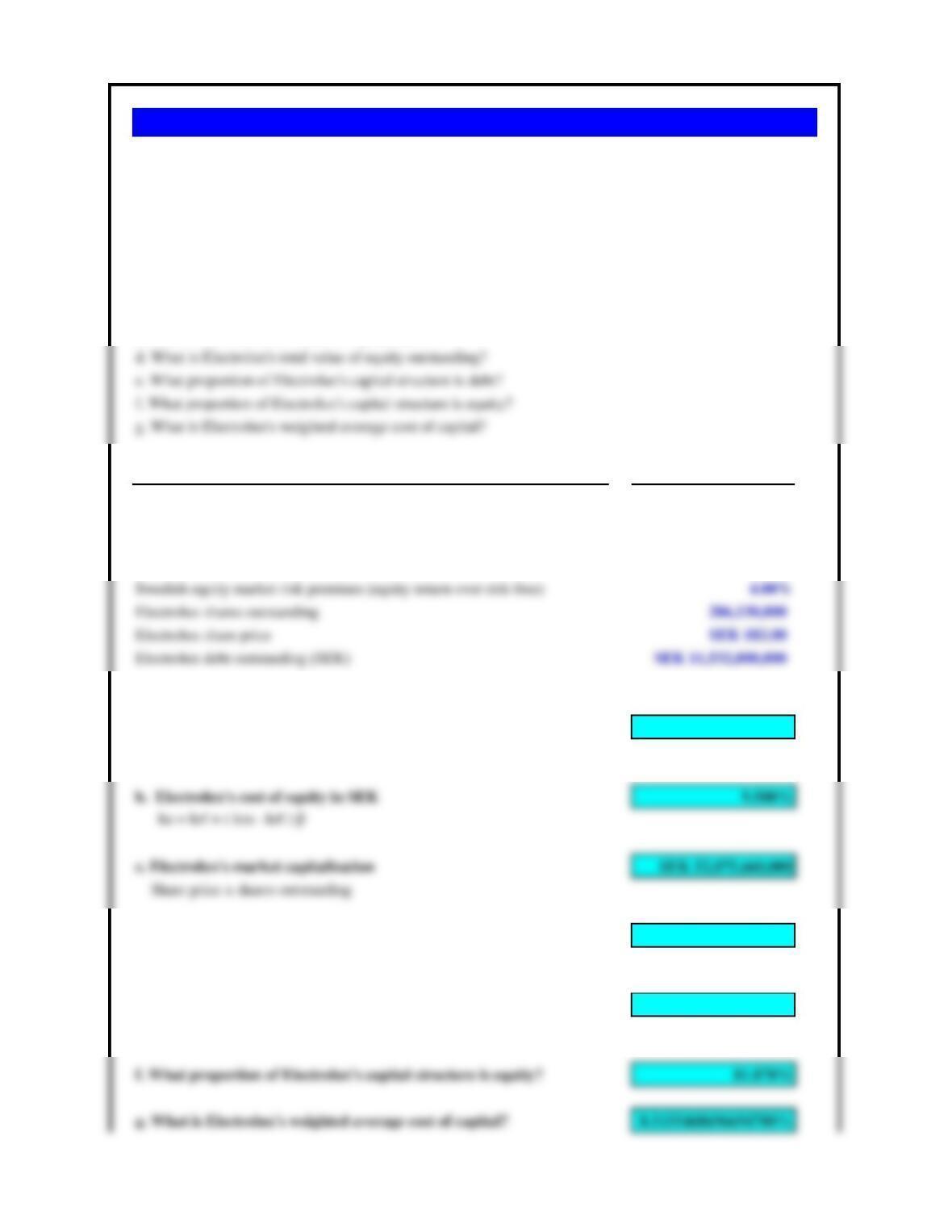

a. What is Electrolux’s cost of debt, after-tax, in SEK?

b. What is Electrolux’s cost of equity in SEK?

c. What is the Electrolux’s market capitalization?

Assumptions Values

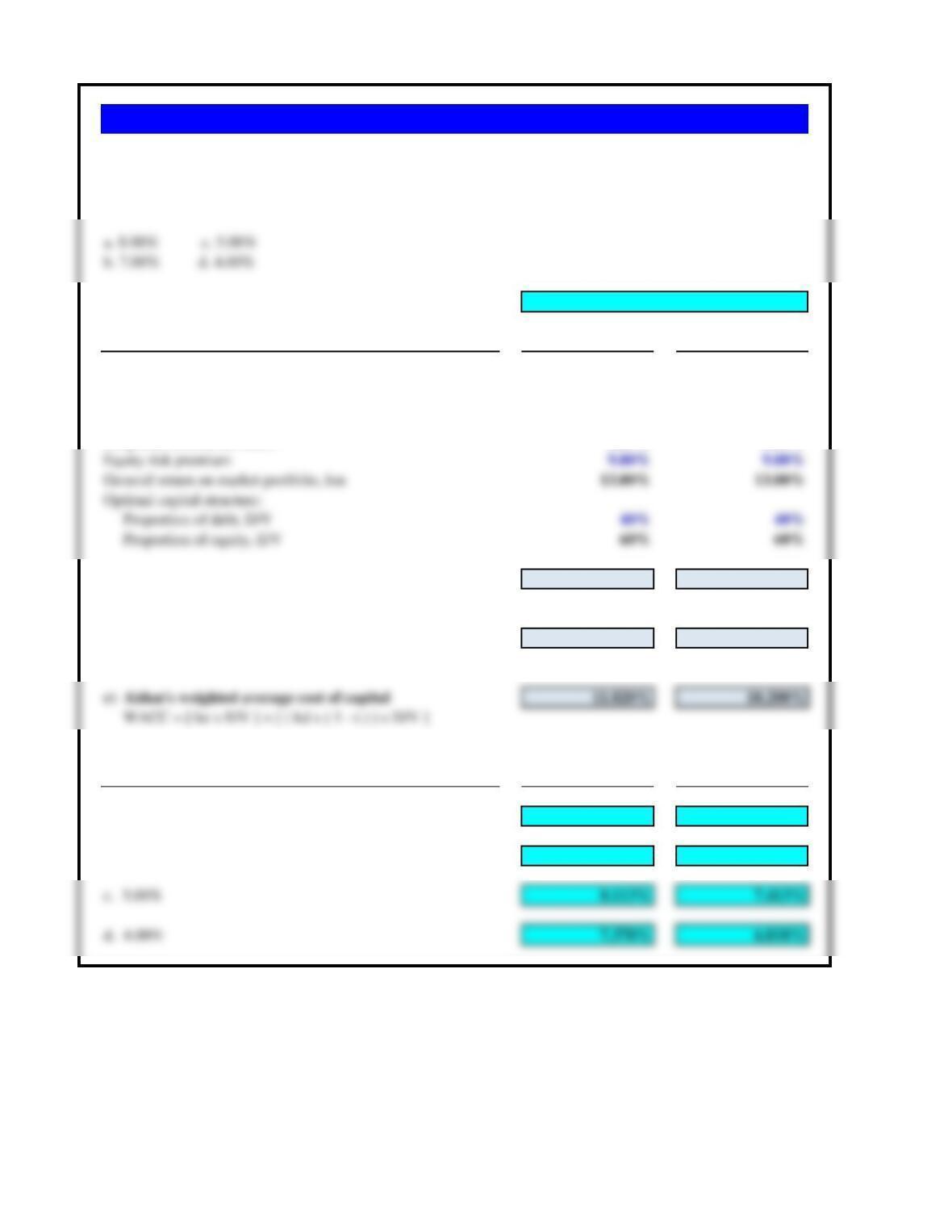

Swedish kroner, government bond rate (10-year) 4.30%

Electrolux credit risk premium 1.20%

Swedish corporate tax rate 26.00%

Electrolux beta 1.30

a. Electrolux’s cost of debt, after-tax, in SEK 4.070%

kd = ( krf + credit risk premium ) x ( 1 – tax rate )

ke = krf + ( km – krf ) β

d. Electrolux’s total value of equity outstanding SEK 52,075,660,000

Share price x shares outstanding

e. What proportion of Electrolux’s capital structue is debt? 18.130%

Debt / ( Debt + Equity )

Problem 13.1 Electrolux of Sweden

Kristian Thalen has just joined the corporate treasury group at Electrolux of Sweden. The multinational

Swedish appliance maker is considering making an offer for GE’s appliance business, and wants to revise its

weighted average cost of capital for its analysis. Kristian has been assigned the task, using the following

assumptions, he goes step by step through the following questions.

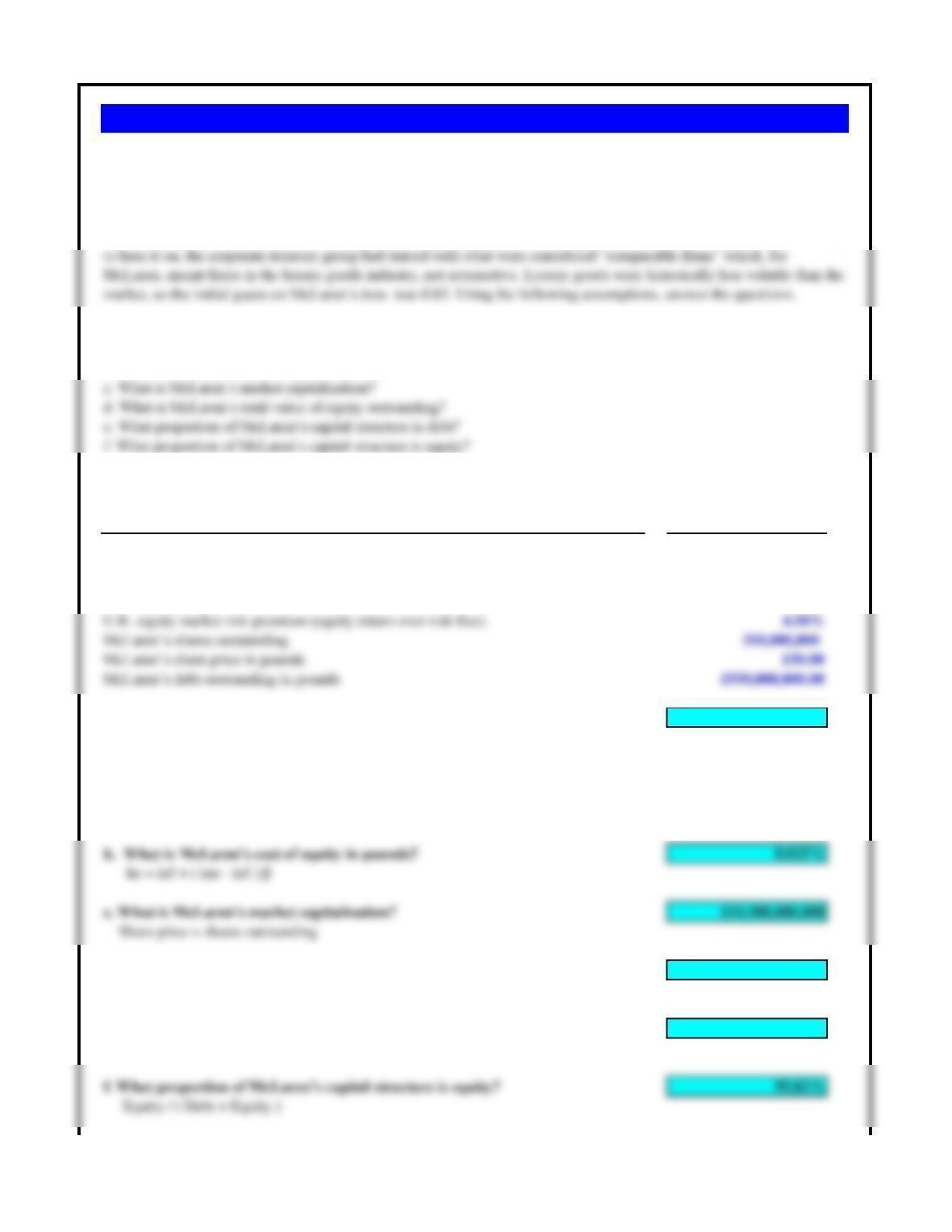

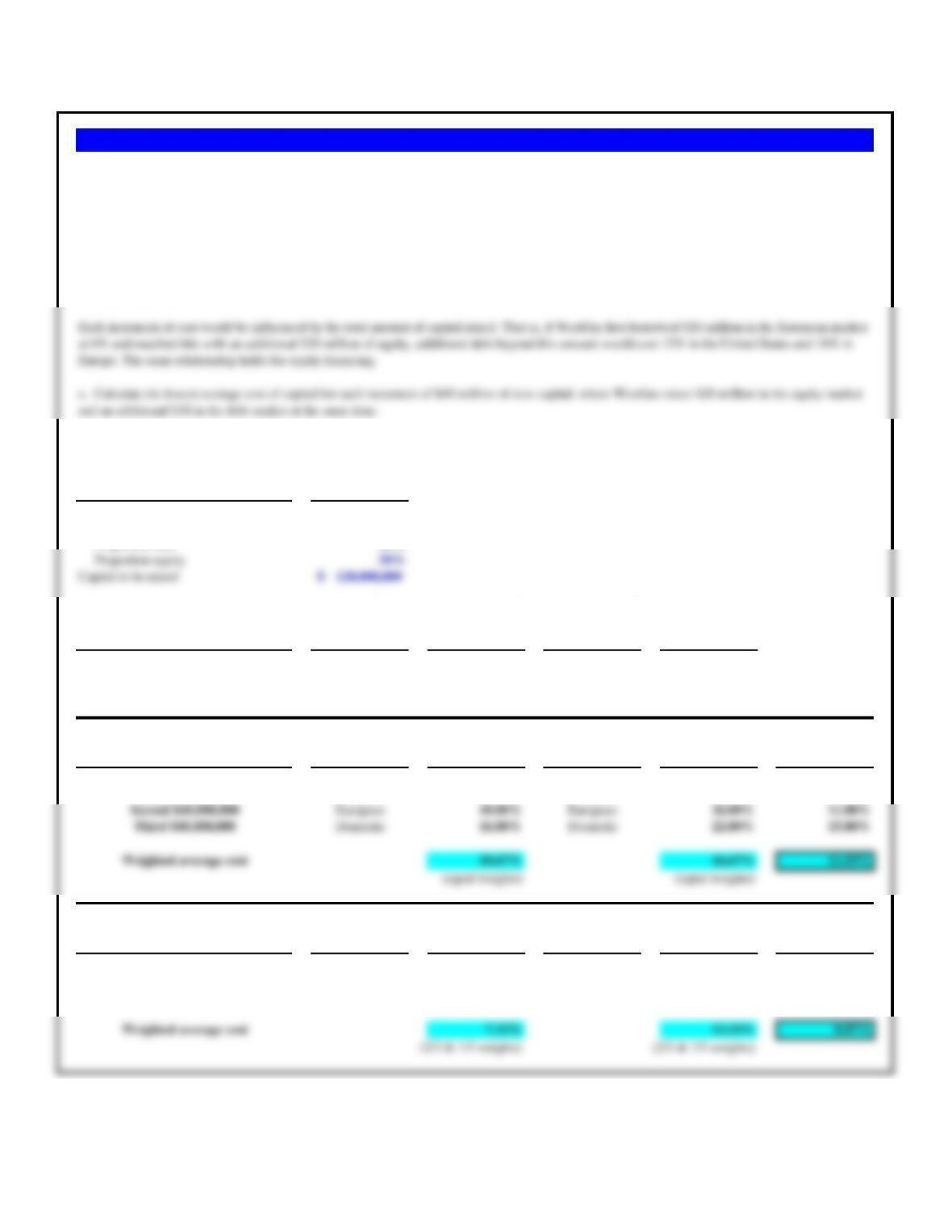

a. What is McLaren’s cost of debt, after-tax in pounds?

b. What is McLaren’s cost of equity in pounds?

g. What is McLaren’s weighted average cost of capital?

h. What is McLaren’s WACC if its beta was higher, like other automotive companies, say 1.30?

Assumptions Values

U.K. risk-free cost of debt in pounds (₤) 4.20%

McLaren’s cost of debt in pounds (₤) 4.00%

U.K. corporate income tax rate 19.00%

McLaren’s prospective beta 0.85

a. What is McLaren’s cost of debt, after-tax in pounds? 3.240%

kd = ( krf + credit risk premium ) x ( 1 – tax rate )

d. What is McLaren’s total value of equity outstanding? £10,500,000,000

Share price x shares outstanding

e. What proportion of McLaren’s capital structure is debt? 4.98%

Debt / ( Debt + Equity )

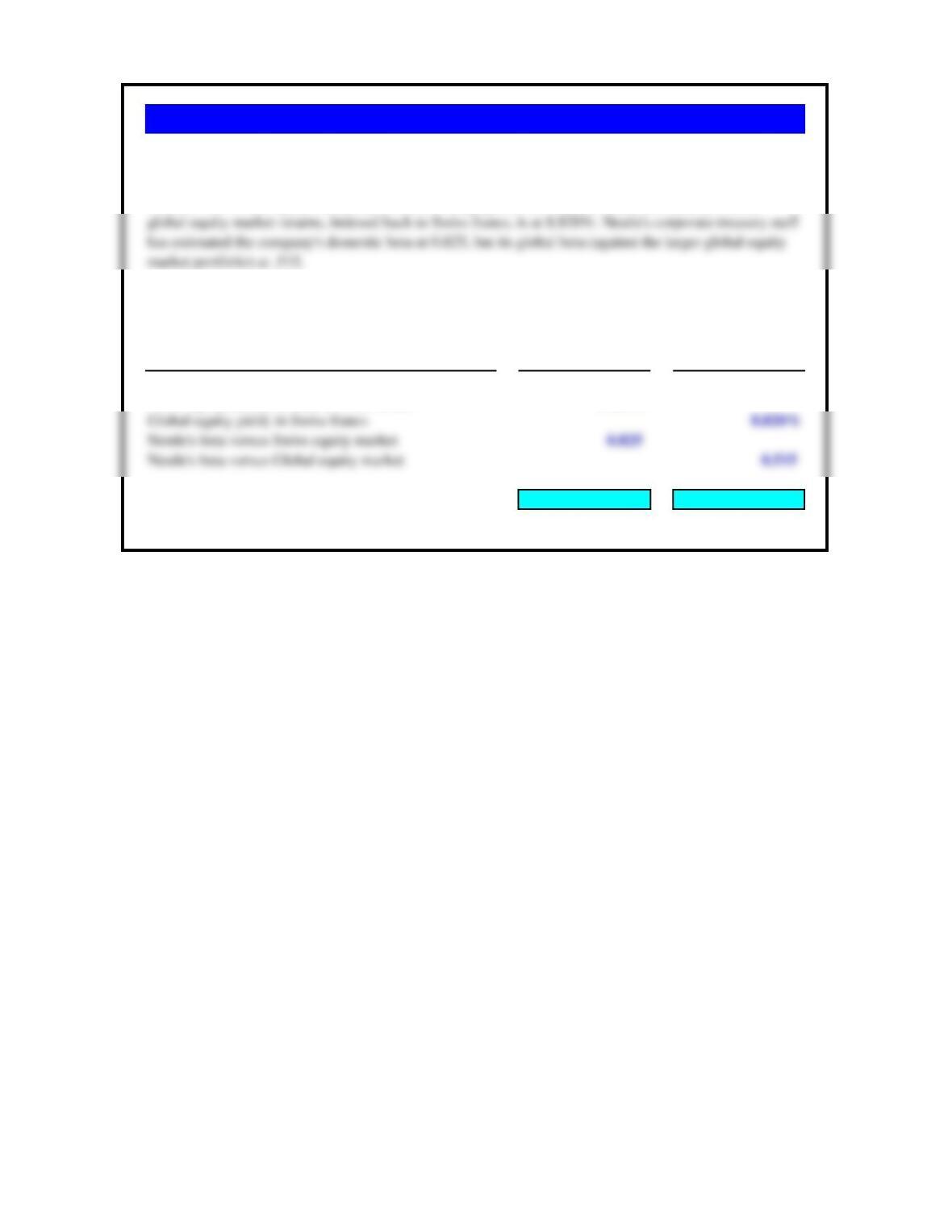

Problem 13.2 McLaren’s IPO and WACC

McLaren, the famous high-performance automotive group, launched its initial public offering (IPO) on October 20,

2019. Although the share price had initially risen to over 60 pounds (£) per share, by the end of the year it had settled to

50 pounds (£). McLaren is owned by Able Group (Ireland) and had never calculated its own cost of capital independent

of Able before. It now needed to, and one of its first challenges was estimating its beta. With only two months of trading

You might notice that McLaren’s cost of debt is actually cheaper than that of the U.K. government. This was true,

and reflected McLaren’s greater-than-U.K. reach for its financial security, while also reflecting U.K.’s continuing

challenge with sovereign debt.

g. What is McLaren’s weighted average cost of capital? 7.79%

WACC = ( kd (1-tax) * D/(D+E)) + ( ke * E/(D+E))

h. What is McLaren’s WACC if its beta was higher, like other automotive

companies, say 1.30?

9.71%

Replacing the beta value above, and using the calculations that follow.

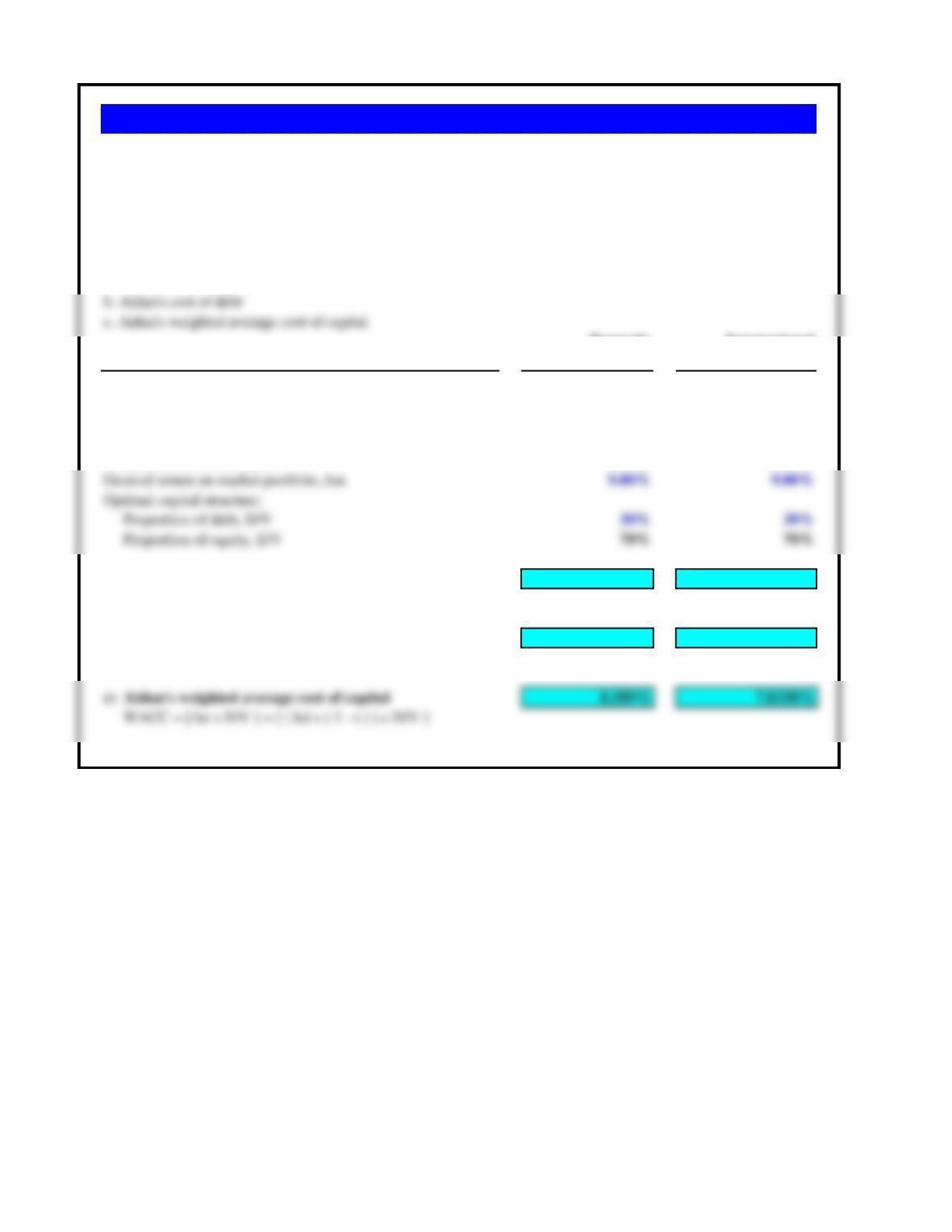

a. Aidan’s cost of equity

b. Aidan’s cost of debt

Assumptions CAPM ICAPM

Aidan’s beta, β 1.05 0.85

Risk-free rate of interest, krf 3.60% 3.60%

Company credit risk premium 4.40% 4.40%

Cost of debt, before tax, kd 8.00% 8.00%

Corporate income tax rate, t 12.5% 12.5%

a) Aidan’s cost of equity 9.270% 8.190%

ke = krf + ( km – krf ) β

b) Aidan’s cost of debt, after tax 7.000% 7.000%

kd x ( 1 – t )

Problem 13.3 Aidan’s Cost of Capital

Terry McDermott now estimates Aidan’s risk-free rate to be 3.60%, the company’s credit risk premium is 4.40%,

the domestic beta is estimated at 1.05, the international beta is estimated at 0.85, and the company’s capital

structure is now 30% debt. All other values remain the same as those presented in the section “Sample

Calculation: Aidan’s Cost of Capital.” For both the domestic CAPM and ICAPM, calculate the following:

a. 8.00% c. 5.00%

Domestic International

Assumptions CAPM ICAPM

Aidan’s beta, β 1.20 0.90

Risk-free rate of interest, krf 4.00% 4.00%

Company credit risk premium 4.40% 4.40%

Cost of debt, before tax, kd 8.40% 8.40%

Corporate income tax rate, t 12.5% 12.5%

a) Aidan’s cost of equity 14.800% 12.100%

ke = krf + ( km – krf ) β

b) Aidan’s cost of debt, after tax 7.350% 7.350%

kd x ( 1 – t )

Differing Equity Risk Premiums CAPM ICAPM

a. 8.00% 10.318% 9.198%

b. 7.00% 9.583% 8.603%

Problem 13.4 Aidan and Equity Risk Premiums

Answer for part a

Using the original weighted average cost of capital data for Aidan used in the section “Sample Calculation:

Aidan’s Cost of Capital,” calculate both the CAPM and ICAPM weighted average costs of capital for the

following equity risk premium estimates.

a. If Thunderhorse beta is estimated at 1.1, what is its weighted average cost of capital?

Assumptions a) Values b) Values

Thunderhorse’s beta 1.10 0.80

Cost of debt, before tax 7.000% 7.000%

Calculation of the WACC

Cost of debt, after-tax 5.250% 5.250%

kd x ( 1 – t )

Cost of equity, after-tax 8.500% 7.000%

ke = krf + ( km – krf ) β

Problem 13.5 Thunderhose Oil

b. If Thunderhorse’s beta is estimated at 0.8, significantly lower because of the continuing profit

prospects in the global energy sector, what is the company‘s weighted average cost of capital?

Thunderhorse Oil is a U.S. oil company. Its current cost of debt is 7%, and the 10-year U.S. Treasury

yield, the proxy for the risk-free rate of interest, is 3%. The expected return on the market portfolio is

8%. The company‘s effective tax rate is 39%. Its optimal capital structure is 60% debt and 40% equity.

a. What is Nestle’s cost of equity based on the domestic portfolio of a Swiss investor?

b. What is Nestle’s cost of equity based on a global portfolio for a Swiss investor?

Assumptions Domestic Portfolio Global Portfolio

Swiss bond index yield, the risk-free rate 0.520% 0.520%

Swiss equity market return, in Swiss francs 8.400%

Nestle’s cost of equity using CAPM 7.0210% 4.7945%

Problem 13.6 Nestle of Switzerland Revisited

Nestle of Switzerland is revisiting its cost of equity analysis in 2014. As a result of extraordinary actions

by the Swiss Central Bank, the Swiss bond index yield (10-year maturity) has dropped to a record low of

0.520%. The Swiss equity markets have been averaging 8.400% returns, while the Financial Times

a. If Corcovado’s beta is estimated at 1.1, what is its weighted average cost of capital?

Assumptions a. Values b. Values

Corcovado’s beta 1.10 0.80

Cost of debt, before tax 7.000% 7.000%

Risk-free rate of interest 3.000% 3.000%

Corporate income tax rate 25.000% 25.000%

Calculation of the WACC

Cost of debt, after-tax 5.250% 5.250%

kd x ( 1 – t )

Problem 13.7 Corcovado Pharmaceuticals

Corcovado Pharmaceutical’s cost of debt is 7%. The risk-free rate of interest is 3%. The expected return

on the market portfolio is 8%. After effective taxes, Corcovado’s effective tax rate is 25%. Its optimal

capital structure is 60% debt and 40% equity.

b. If Corcovado’s beta is estimated at 0.8, significantly lower because of the continuing profit prospects

in the global energy sector, what is its weighted average cost of capital?

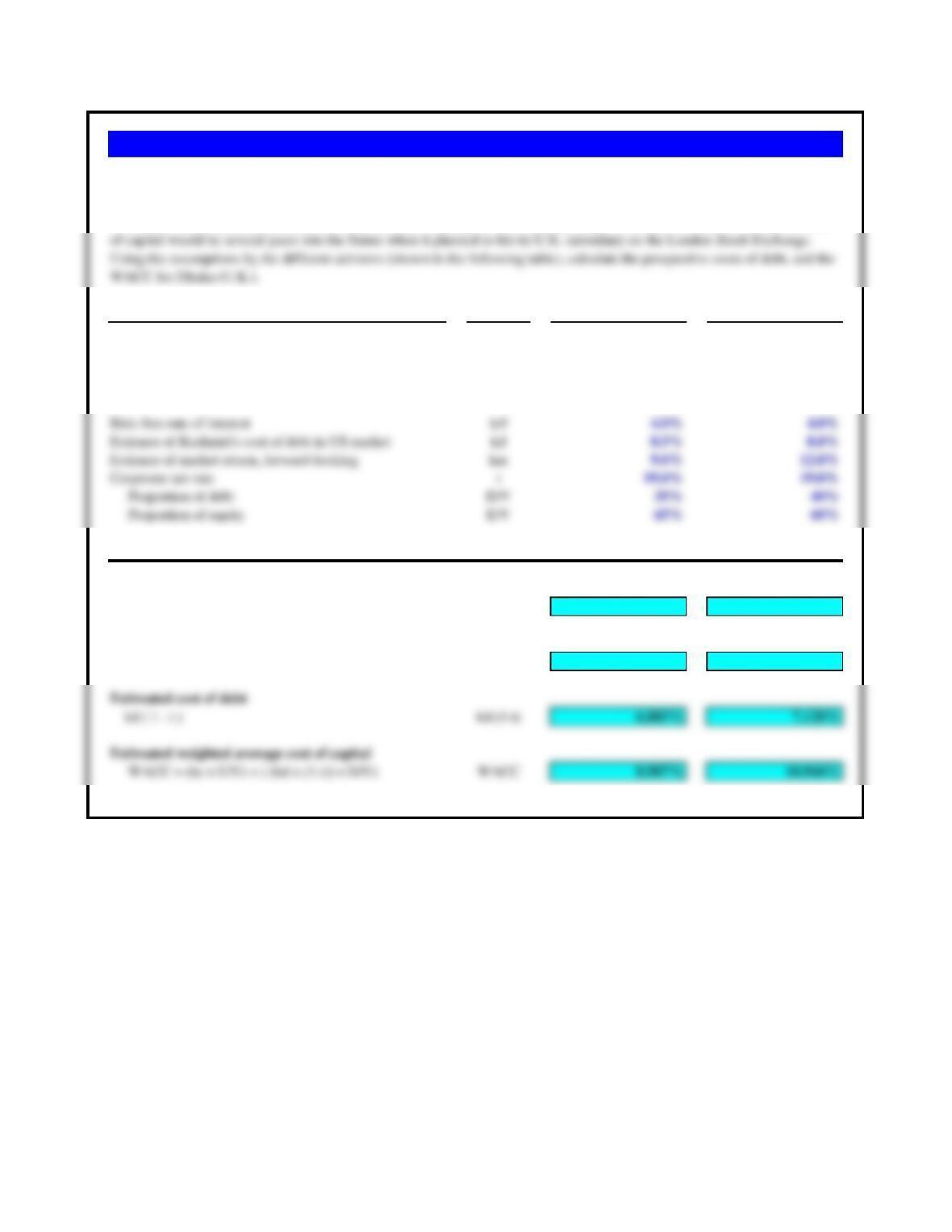

Assumptions Values

Combined federal and state tax rate 40%

Desired capital structure:

Cost of Cost of Cost of Cost of

Domestic Domestic European European

Costs of Raising Capital in the Market Equity Debt Equity Debt

Up to $40 million of new capital 12% 8% 14% 6%

$41 million to $80 million of new capital 18% 12% 16% 10%

Above $80 million 22% 16% 24% 18%

Incremental

a. To raise $120,000,000 Debt Market Debt Cost Equity Market Equity Cost WACC

First $40,000,000 European 6.00% Domestic 12.00% 7.80%

Incremental

b. To raise $60,000,000 Debt Market Debt Cost Equity Market Equity Cost WACC

First $40,000,000 European 6.00% Domestic 12.00% 7.80%

Additional $20,000,000 European 10.00% European 16.00% 11.00%

Problem 13.8 WestGas Conveyance, Inc.

A London bank advises WestGas that U.S. dollars could be raised in Europe at the following costs, also in multiples of $20 million, while maintaining

the 50/50 capital structure.

b. If WestGAs plans an expansion of only $60 million, how should that expansion be financed? What will be the weighted average cost of capital for

the expansion?

at 6% and matched this with an additional $20 million of equity, additional debt beyond this amount would cost 12% in the United States and 10% in

Europe. The same relationship holds for equity financing.

a. Calculate the lowest average cost of capital for each increment of $40 million of new capital, where WestGas raises $20 million in the equity market

and an additional $20 in the debt market at the same time.

WestGas Conveyance, Inc., is a large U.S. natural gas pipeline company that wants to raise $120 million to finance expansion. WestGas wants a capital

structure that is 50% debt and 50% equity. Its corporate combined federal and state income tax rate is 40%. WestGas finds that it can finance in the

domestic U.S. capital market at the rates listed below. Both debt and equity would have to be sold in multiples of $20 million, and these cost figures

show the component costs, each, of debt and equity if raised half by equity and half by debt.

Assumptions Symbol Barclays Northwest

Components of beta: β

Estimate of correlation between security and market

ρjm 0.93 0.88

Estimate of standard deviation of Kashmiri’s returns σj 25.0% 31.0%

Estimate of standard deviation of market’s return

σm19.0% 23.0%

Estimating Costs of Capital

Estimated beta

β = ( ρjm x σj ) / ( σm ) β1.22 1.19

Estimated cost of equity

ke = krf + (km – krf) βke 10.118% 13.489%

Problem 13.9 Dhaka’s Cost of Capital

Dhaka is the largest and most successful garment maker in Dhaka, Bangladesh. It has not yet entered the European market but

is considering establishing both manufacturing and distribution facilities in the United Kingdom through a wholly owned

subsidiary. It has approached two different investment banking advisors, Barclays and NatWest, for estimates of what its cost

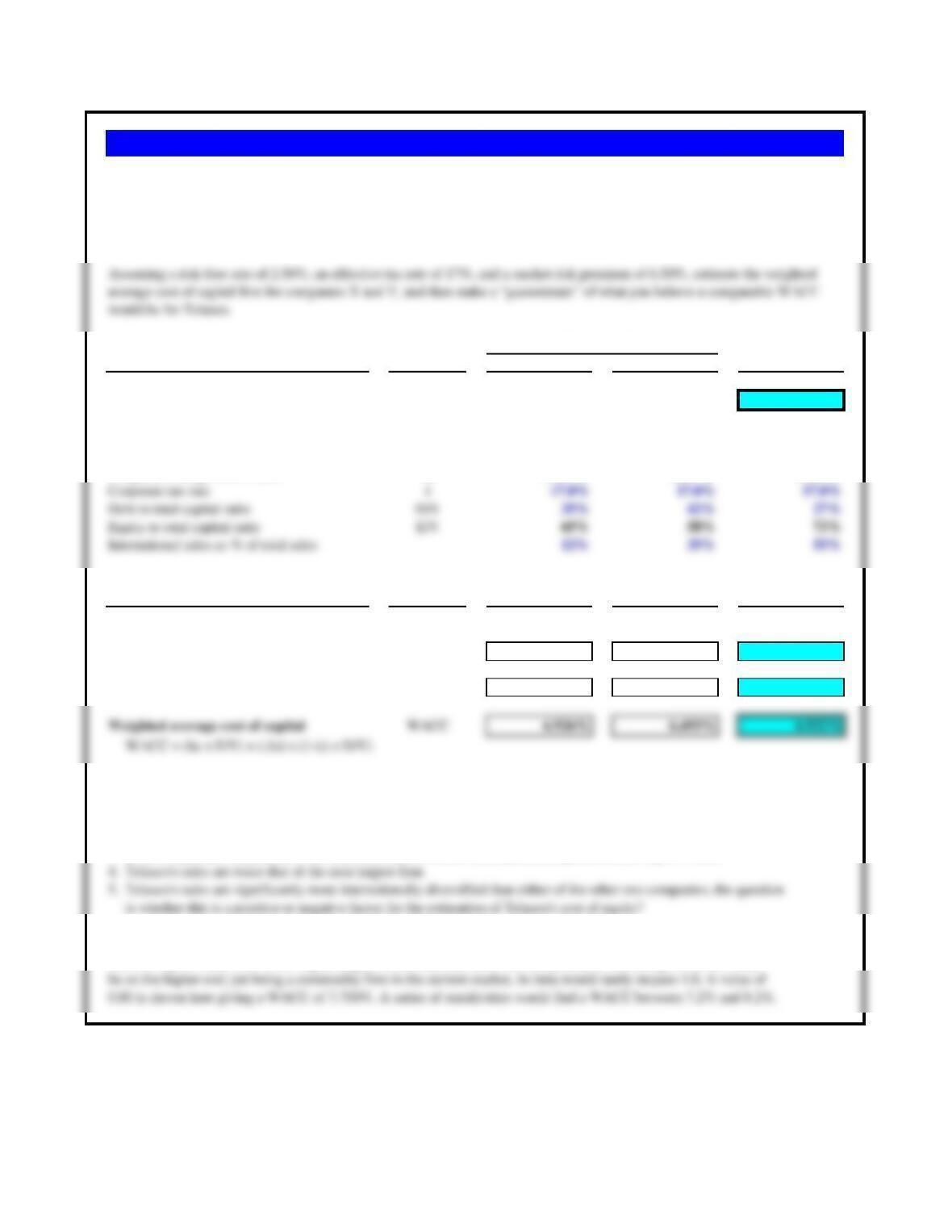

Assumptions Symbol Company X Company Y Telasco

Total sales Sales

$11.0 billion $50 billion $105 billion

Company‘s beta β

0.85 0.70 0.80

Company credit rating S&P AA AAA

Risk-free rate of interest krf 2.5% 2.5% 2.5%

Market risk premium km-krf 6.5% 6.5% 6.5%

Weighted average cost of debt kd 5.885% 6.895% 5.850%

Estimating Costs of Capital Symbol Company X Company Y Telasco

Cost of equity

ke = krf + (km – krf) βke 8.025% 7.050% 7.700%

Cost of debt, after-tax kd ( 1 – t ) 4.885% 5.723% 4.856%

Once the data is organized, the absence of a beta for Telasco is the obvious data deficiency.

A series of observations is then helpful:

1. Note that beta and credit ratings do not necessarily parallel one another

2. Credit rating and cost of debt do follow expected norms; lower the rating, the higher the cost

3. Both comparable companies, in the same industry as Telasco (commodities), possess relatively low betas

If we take the approach that the beta for Cargill has to pick up all the incremental information, the beta would then fall

between say 0.70 and 0.85. If the higher degree of international sales was interpreted as increasing risk, beta would

Problem 13.10 Telasco’s Cost of Capital

Comparables

Telasco is generally considered to be the largest privately held company in South-East Asia. Headquartered in Singapore, the

company has been averaging sales of over S$120 million per year over the past five years. Although the company does not have

publicly traded shares, it is still extremely important for it to calculate its weighted average cost of capital properly in order to

make rational decisions on new investment proposals.

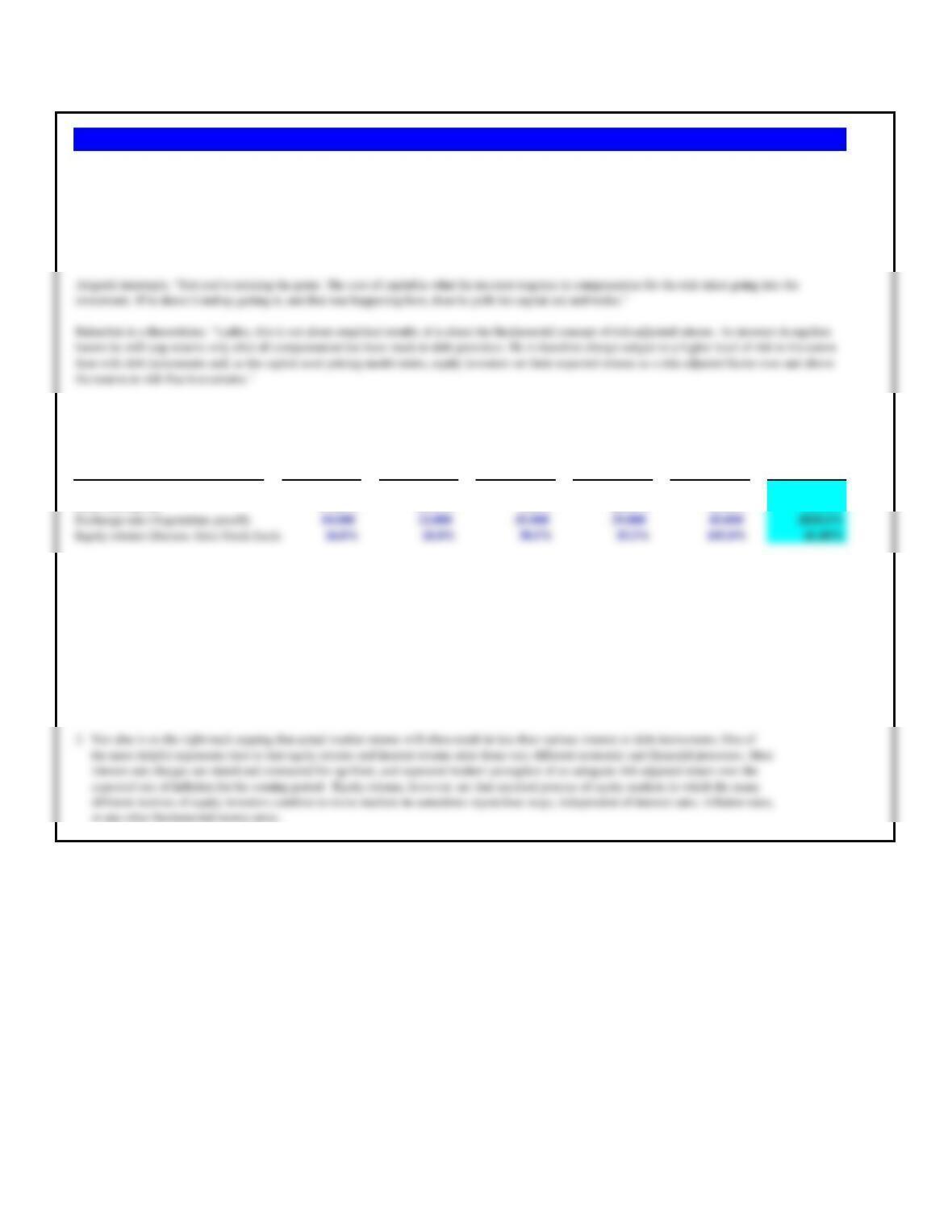

Brazilian Economic Performance 1995 1996 1997 1998 1999 Mean

Inflation rate (IPC) 5.00% 7.50% 6.40% 3.00% 8.45% 6.07%

All three are on the right track. It is mostly a matter of finding the linkages beween their individual arguments.

1. Theoretically, Babchuk is correct in that CAPM assumes that all equity returns are over and above risk-free rates. These are of course,

expected returns, and are the investor’s expectations or requirements going INTO the investment.

2. Arisgashi is also correct in arguing that regardless of what investors may EXPECT, the results are often quite different, sometimes disappointing.

Theoretically, when the investment does not yield at least the expected return, the investor should indeed liquidate their position. However,

in reality, many investors for a variety of reasons (tax implications, investment horizon, etc.), may stay in the investment and just complain

about the past and hope about the future.

Problem 13.11 The Equity

At this point, Ven and Arisgashi simply stare at Babachuk—pause—and order more drinks. Using the Argentinian data presented, comment on this week’s

debate at The Equity.

Ven argues, “It’s all about expected versus delivered. You can talk about what equity investors expect, but they often find that what is delivered for years at

a time is so small—even sometimes negative—that in effect, the cost of equity is cheaper than the cost of debt.

the returns to risk-free instruments.”

Arigashi interrupts, “But you’re missing the point. The cost of capital is what the investor requires in compensation for the risk taken going into the

investment. If he doesn’t end up getting it, and that was happening here, then he pulls his capital out and walks.”

You have joined your friends at the local tavern, The Equity, for your weekly debate on international finance. The topic this week is whether the cost of

equity can ever be cheaper than the cost of debt. The group has chosen Argentina in the mid-1990s as a subject of the debate. One of the group members

has torn out a table of data out of a book, which becomes the subject of the analysis.

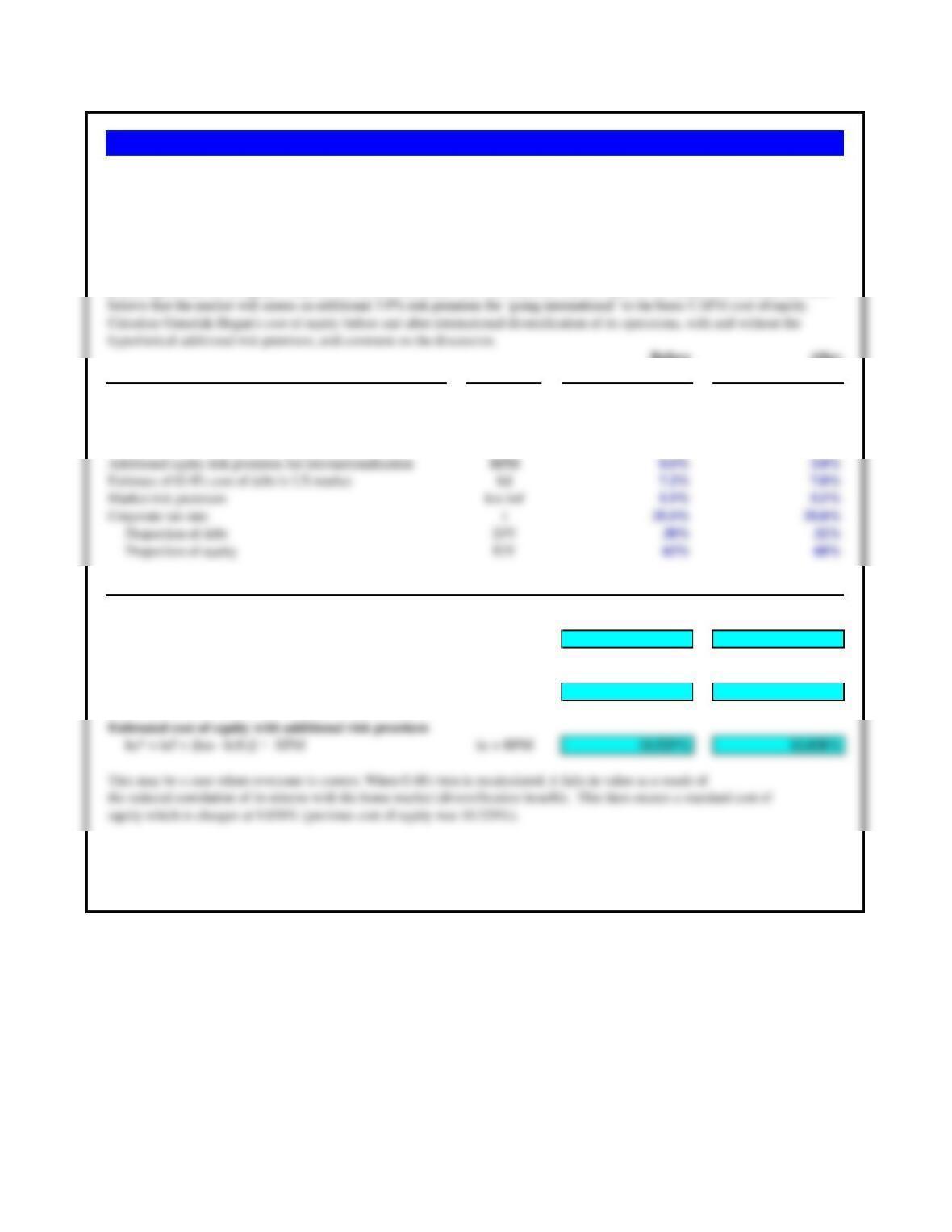

Before After

Assumptions Symbol Diversification Diversification

Correlation between G-H and the market

ρjm 0.88 0.76

Standard deviation of G-H’s returns σj 28.0% 26.0%

Standard deviation of market’s returns

σm18.0% 18.0%

Risk-free rate of interest krf 3.0% 3.0%

Estimating Costs of Capital

Estimated beta

β = ( ρjm x σj ) / ( σm ) β1.37 1.10

Estimated cost of equity

ke = krf + (km – krf) βke 10.529% 9.038%

ke* = krf + (km – krf) β + RPM ke + RPM 10.529% 12.038%

If, however, the market was to add an additional risk premium to the firm’s cost of equity as a result of internationally

diversifying operations, and if that risk premium were on the order of 3.0%, the final risk-adjusted cost of equity is

indeed higher, 12.038% to the before value of 10.529%.

Problem 13.12 Genedak-Hogan Cost of Equity

Use the following information to answer questions 10 through 12. Genedak-Hogan is an American conglomerate which is actively

debating the impacts of international diversification of its operations on its capital structure and cost of capital. The firm is planning

on reducing consolidated debt after diversification.

Senior management at Genedak-Hogan is actively debating the implications of diversification on its cost of equity. Although both

parties agree that the company’s returns will be less correlated with the reference market return in the future, the financial advisors

Calculate Genedak-Hogan’s cost of equity before and after international diversification of its operations, with and without the

hypothetical additional risk premium, and comment on the discussion.

Calculate the weighted average cost of capital for Genedak-Hogan for before and after international diversification.

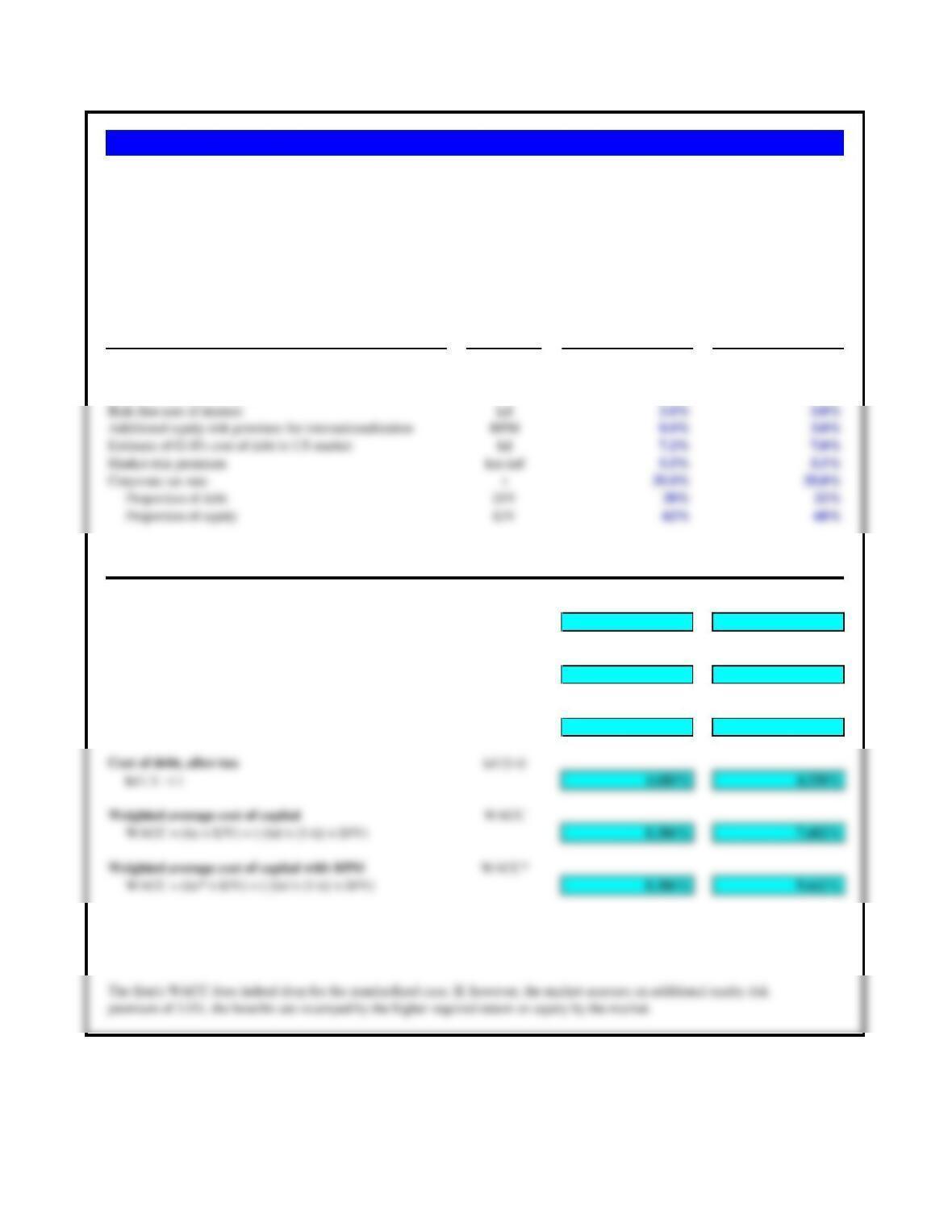

Before After

Assumptions Symbol Diversification Diversification

Correlation between G-H and the market

ρjm 0.88 0.76

Standard deviation of G-H’s returns σj 28.0% 26.0%

Standard deviation of market’s returns

σm18.0% 18.0%

Before After

Estimating Costs of Capital Diversification Diversification

Estimated beta

β = ( ρjm x σj ) / ( σm ) β1.37 1.10

Estimated cost of equity

ke = krf + (km – krf) βke 10.529% 9.038%

Estimated cost of equity with additional risk premium

ke* = krf + (km – krf) β + RPM ke + RPM 10.529% 12.038%

There are a number of different factors at work here. First, as a result of international diversification, their access to debt

has improved, resulting in a lower cost of debt capital. This is not fully appreciated, however, as the firm has chosen to

reduce its overall use of debt post-diversification (common among MNEs).

Problem 13.13 Genedak-Hogan’s WACC

a. Did the reduction in debt costs reduce the firm’s weighted average cost of capital? How would you describe the impact of

international diversification on its costs of capital?

b. Adding the hypothetical risk premium to the cost of equity introduced in problem 10 (an added 3.0% to the cost of equity

because of international diversification), what is the firm’s WACC?

Before After

Assumptions Symbol Diversification Diversification

Correlation between G-H and the market

ρjm 0.88 0.76

Standard deviation of G-H’s returns σj 28.0% 26.0%

Standard deviation of market’s returns

σm18.0% 18.0%

Before After

Estimating Costs of Capital Diversification Diversification

Estimated beta

β = ( ρjm x σj ) / ( σm ) β1.37 1.10

Estimated cost of equity

ke = krf + (km – krf) βke 10.529% 9.038%

ke* = krf + (km – krf) β + RPM ke + RPM 10.529% 12.038%

The reduction in the effective tax rate obviously impacts WACC through the cost of debt. This does have substantial

benefits in the company‘s WACC — as long as additional equity risk premiums are not assessed. Then, even the lower

effective tax rate does not offset the higher equity costs associated with the international risk premium.

Problem 13.14 Genedak-Hogan’s WACC and Effective Tax Rate

Many MNEs have greater ability to control and reduce their effective tax rates when expanding international operations. If Genedak-

Hogan was able to reduce its consolidated effective tax rate from 35% to 32%, what would be the impact on its WACC?