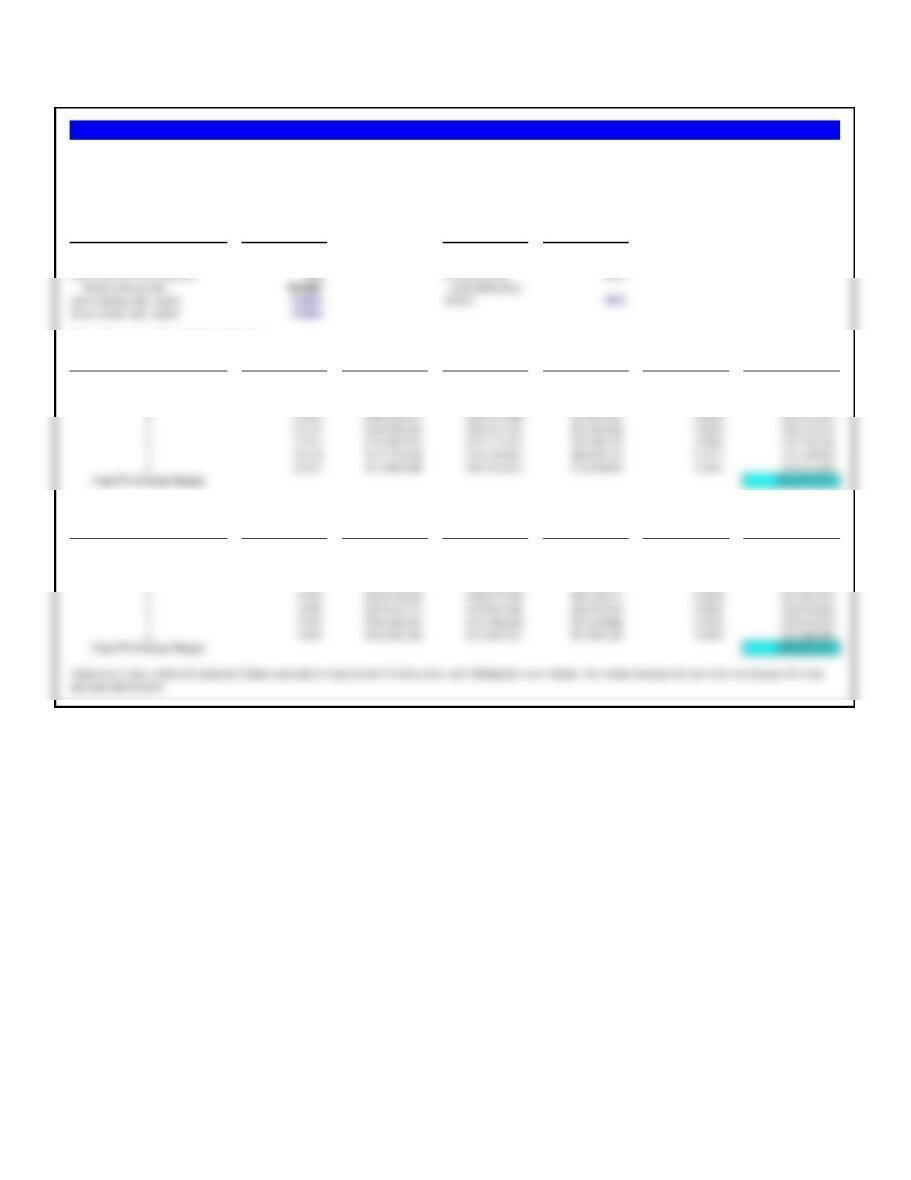

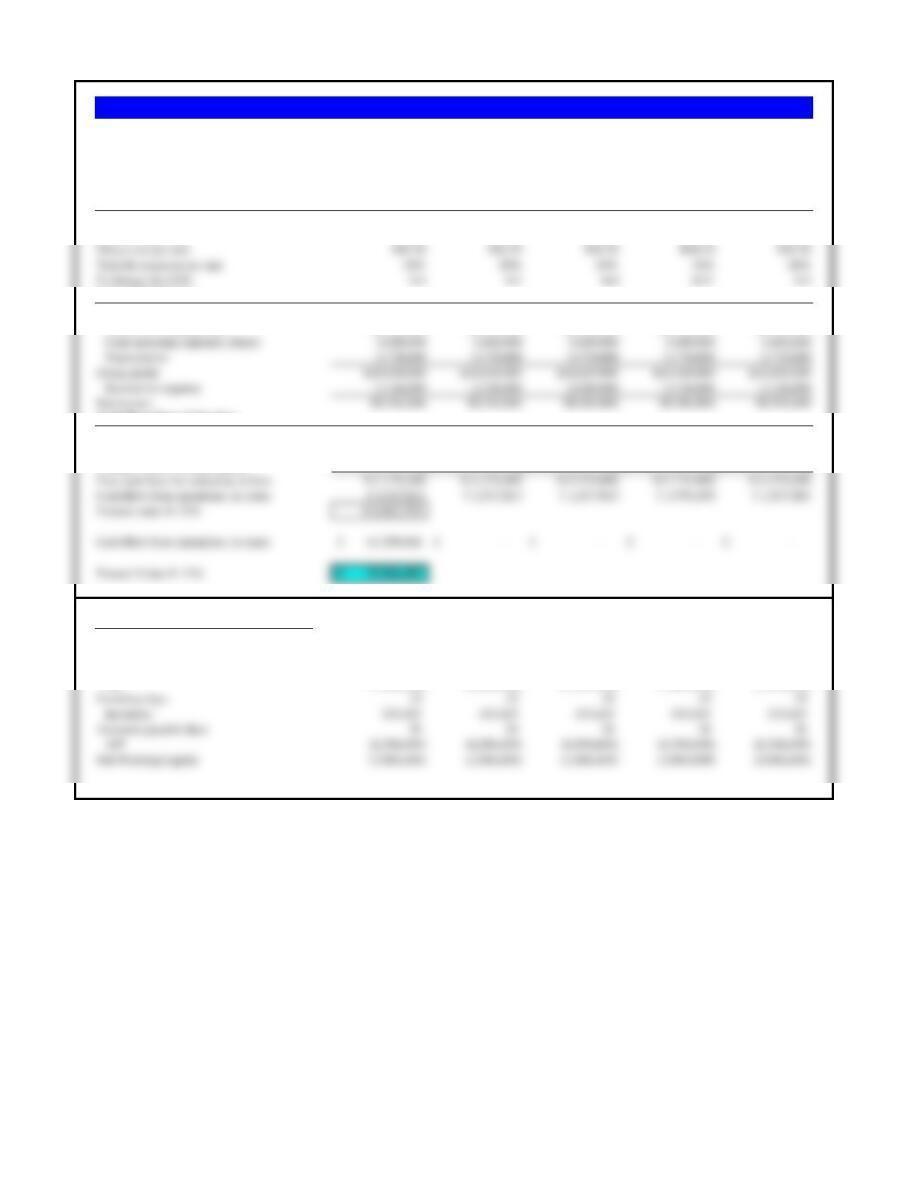

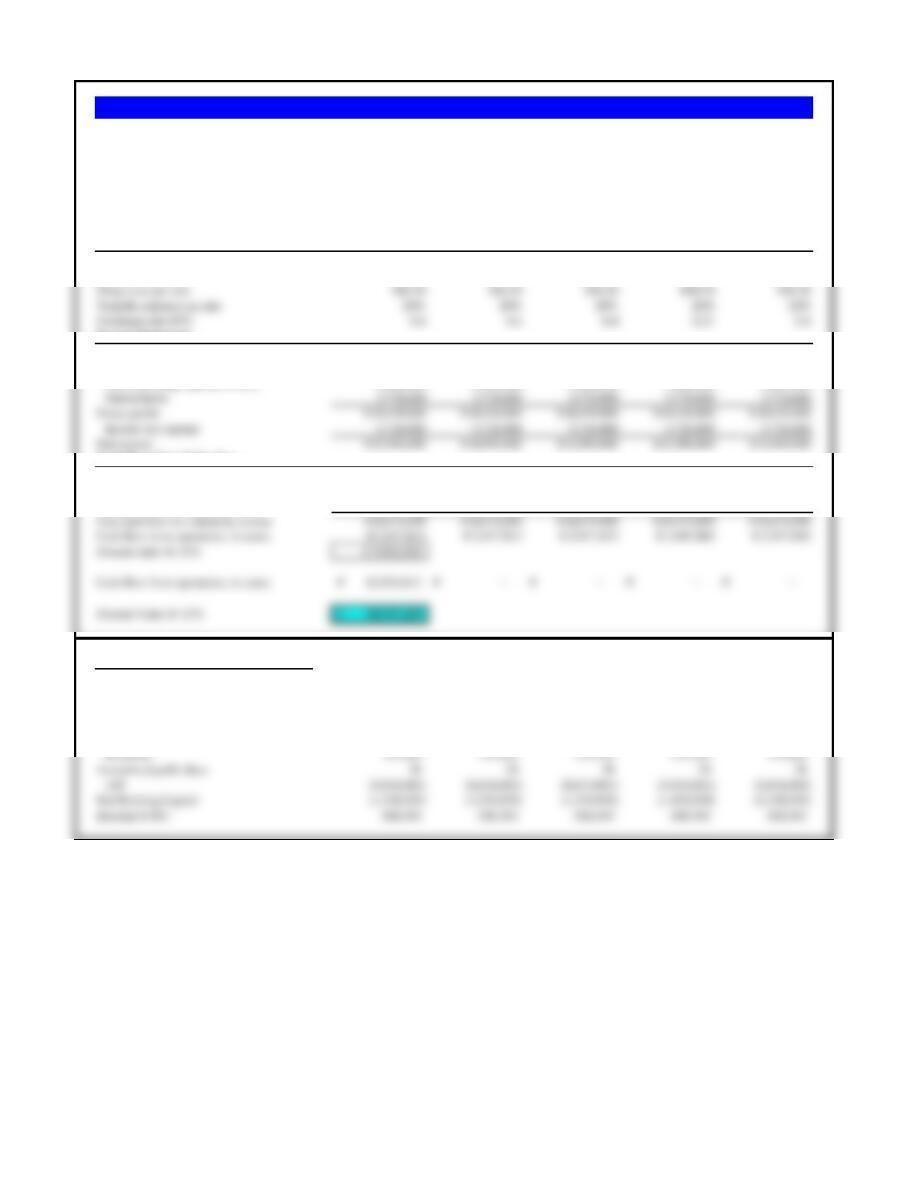

a. How much should Mauna Loa borrow in yen?

Mauna Loa receives cash collections of one hundred million yen per month. This is the source of repayment of any

balance sheet hedge. If Mauna Loa wants to be covered for one year at a time, it would need to borrow one year’s

cash flow plus interest, and convert the borrowed yen to US dollar at once. A sample calculation would be:

Sample Values Units

One month’s cash flow 100,000,000 Yen

Months per year 12

One year’s cash flow 1,200,000,000 Yen

Realistically, Mauna Loa would probably want to be covered for the long term. In that case, the 1.2 billion yen loan

could be structured so that it could be renewed annually with interest reset annually. This would only cover the

foreign exchange and interest rate risk for a year at a time, but would probably be acceptable to a bank lender.

Also unknown are the expected sales for year 2 and beyond.

b. What should be the terms of payment on the loan?

The loan should be repaid out of the monthly cash flow, with payments on principal only. The interest payment one

year hence has already been covered by borrowing both principal and interest up-front.

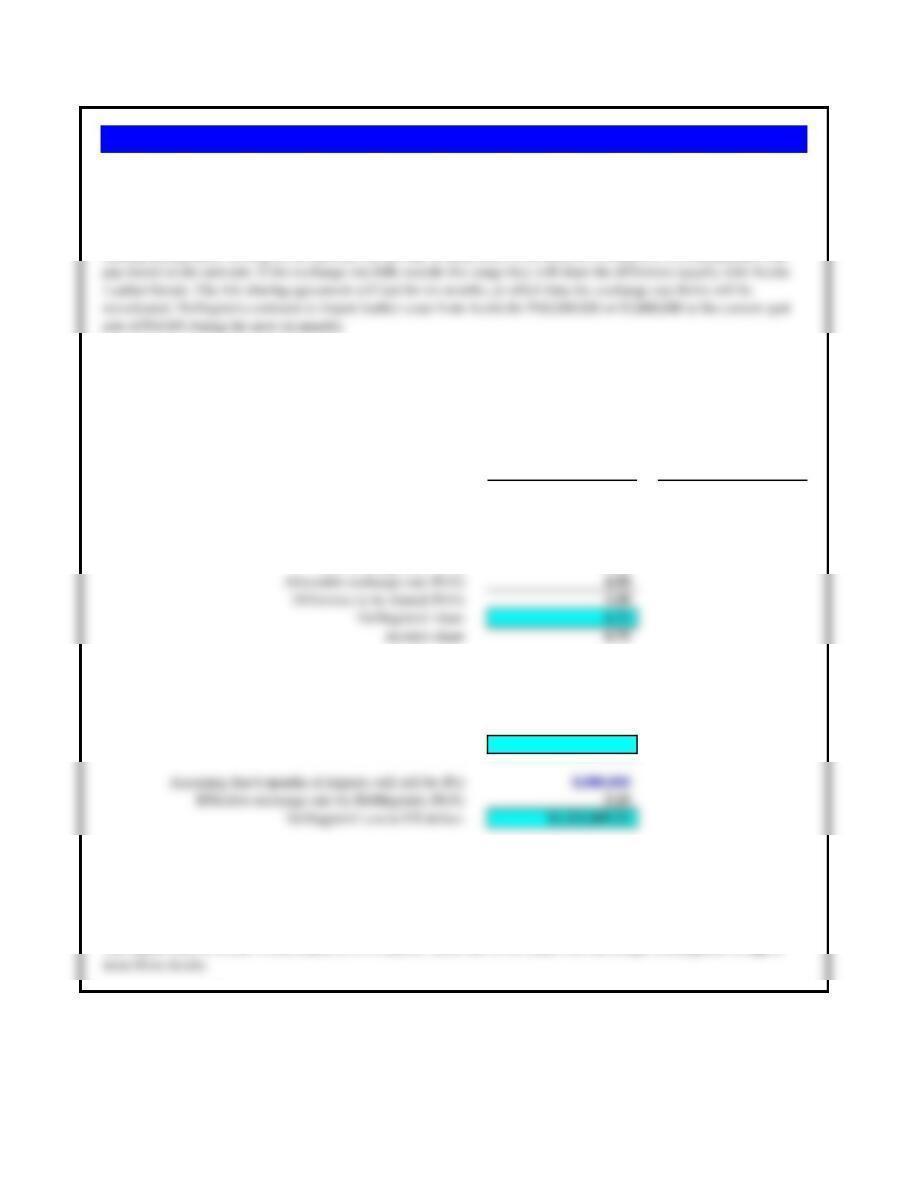

Problem 12.1 Mauna Loa Macadamia

Mauna Loa, a macadamia nut subsidiary of Hershey‘s with planations on the slopes of its namesake volcano in Hilo, Hawaii,

exports Macadamia nuts worldwide. The Japanese market is its biggest export market, with average annual sales invoiced in yen

to Japanese customers of ¥1,200,000,000. At the present exchange rate of ¥125/$ this is equivalent to $9,600,000. Sales are

relatively equally distributed during the year. They show up as a ¥250,00,000 account receivable on Mauna Loa’s balance sheet.

Credit terms to each customer allow for 60 days before payment is due. Monthly cash collections are typically ¥100,000,000.

Bottom Top

The allowable range of exchange rates is (Ps/$) 3.50 4.50

Outside of this range the trading partners will share the extra risk equally.

New exchange rate (Ps/$) 6.00

Therefore, DeMagistris will use the following effective exchange rate after risk-sharing:

Top of range 4.50

DeMagistris’ share 0.75

Effective total of risk-sharing 5.25

b. At Ps6.00/$, what will be the peso export sales in Acuña to DeMagistris?

Problem 12.2 Acuña Leather Goods

However, the lower cost of importing might lead to higher DeMagistris’ sales and therefore a higher import total than Ps 8

million.

a. If the exchange rate changes immediately to Ps6.00/$, what will be the dollar cost of 6 months of imports to

Pucini?

a. If the exchange rate changes immediately to Ps6.00/$, what will be the dollar cost of 6 months of imports to

b. At Ps6.00/$, what will be the peso export sales in Acuña Leather Goods to DeMagistris Fashion Company?

DeMagistris Fashion Company, based in New York City, imports leather coats from Acuña Leather Goods, a reliable and

longtime supplier, based in Buenos Aires, Argentina. Payment is in Argentine pesos. When the peso lost its parity with the

U.S. dollar in January 2002 it collapsed in value to Ps 4.0/$ by October 2002. The outlook was for a further decline in the

peso’s value. Since both DeMagistris and Acuña wanted to continue their longtime relationship they agreed on a risk–

rate of Ps4.0/$ during the next six months.

Assumptions Values

Sales volume per year 10,000

US dollar price per unit $24,000

Direct costs as % of US$ sales price 75%

Case 1 Case 2

Sales to China Same Yuan Price Same US$ Price

US dollar price per unit $21,391.30 $24,000.00

Unit volume 10,000 9,000

Problem 12.3 Manitowoc Crane (A)

Manitowoc Crane (U.S.) exports heavy crane equipment to several Chinese dock facilities. Sales are currently

10,000 units per year at the yuan equivalent of $24,000 each. The Chinese yuan (renminbi) has been trading at

Yuan8.20/$, but a Hong Kong advisory service predicts the renminbi will drop in value next week to Yuan9.00/$,

a. What would be the short-run (one year) impact of each pricing strategy?

b. Which do you recommend?

Assumptions Values Assumptions Values

Sales volume per year

10,000 Volume change 1%

US dollar price per unit

$24,000 (if price increased)

8.2000 WACC 10%

9.2000

Alternative 1: Keep Same Chinese Sales Price

Gross Present Value Present Value

Year Volume Revenue Direct Costs Margin Factor of Margin

1 10,000 $213,913,043 $180,000,000 $33,913,043 0.9091 $30,830,040

2 11,200 $239,582,609 $201,600,000 $37,982,609 0.8264 $31,390,586

3 12,544 $268,332,522 $225,792,000 $42,540,522 0.7513 $31,961,324

Alternative 2: Raise Chinese Sales Price

Gross Present Value Present Value

Year Volume Revenue Direct Costs Margin Factor of Margin

19,000 $216,000,000 $162,000,000 $54,000,000 0.9091 $49,090,909

2 9,090 $218,160,000 $163,620,000 $54,540,000 0.8264 $45,074,380

3 9,181 $220,341,600 $165,256,200 $55,085,400 0.7513 $41,386,476

4 9,273 $222,545,016 $166,908,762 $55,636,254 0.6830 $38,000,310

Manitowoc Crane is better off raising the Chinese sales price to maintain the US dollar price, and suffering the lower volumes. The volume decrease does not offset the stronger US dollar

price per unit received.

Problem 12.4 Manitowoc Crane (B)

Assume the same facts as in Manitowoc Crane (A). Additionally, financial management believes that if it maintains the same yuan sales price, volume will increase at 12% per annum for

eight years. Dollar costs will not change. At the end of ten years, Manitowoc’s patent expires and it will no longer export to China. After the yuan is devalued to Yuan9.20/$, no further

devaluations are expected. If Manitowoc Crane raises the yuan price so as to maintain its dollar price, volume will increase at only 1% per annum for eight years, starting from the lower

initial base of 9,000 units. Again dollar costs will not change and at the end of eight years Manitowoc Crane will stop exporting to China. Manitowoc’s weighted average cost of capital is

10%. Given these considerations, what should be Manitowoc’s pricing policy?

Assumptions Values

Invoice price of car £32,000

Spot exchange rate, NZ$/£ 1.6400

Risk-sharing band, percentage +/- 5.00%

Sales to New Zealand Distributors Lower Band Upper Band

a. What are the outside ranges? 1.7220 1.5580

(initial spot rate + or – 5%)

b. Cost to the Kiwi distributor for 10 cars

New current spot rate (N$/£) 1.7000

c. Cost to the Kiwi distributor for 10 cars

New current spot rate (N$/£) 1.6500

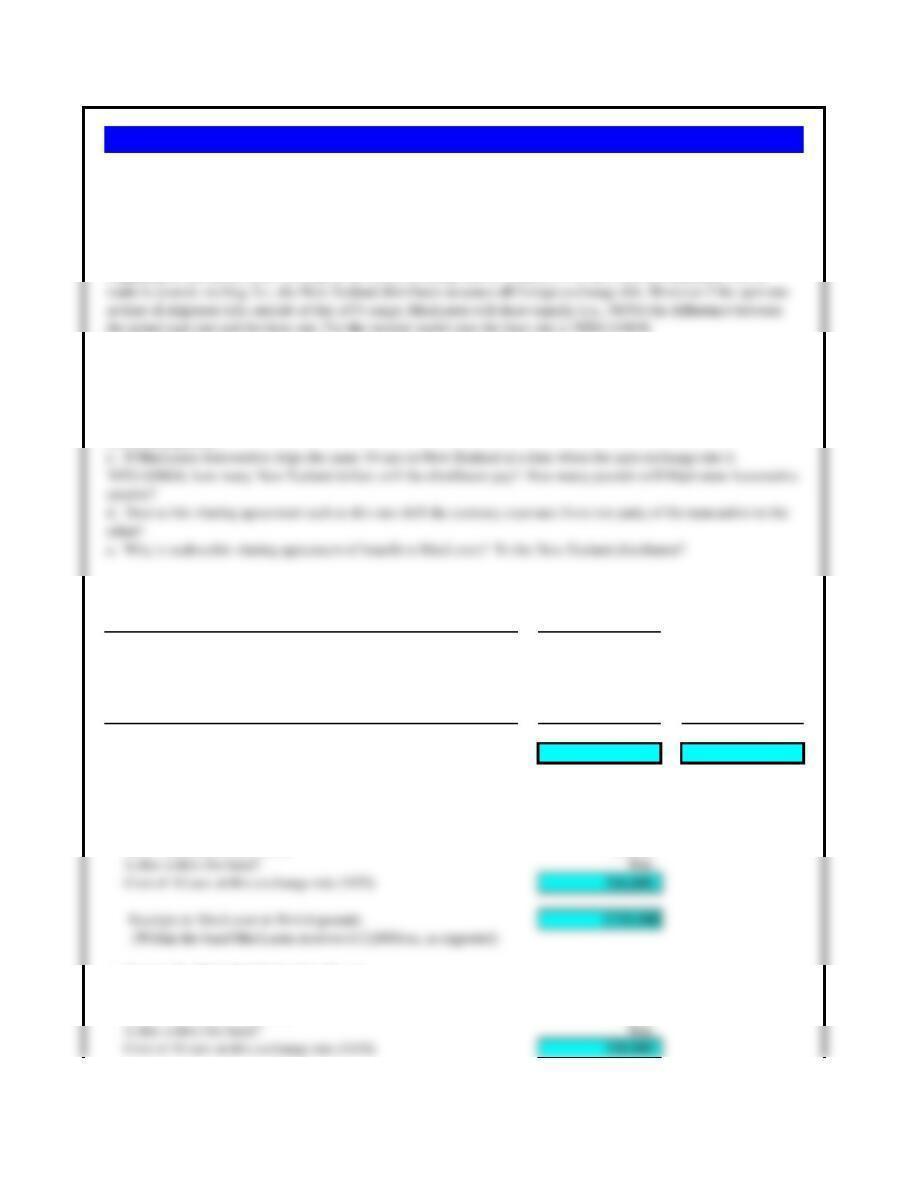

Problem 12.5 MacLoren Automotive

MacLoren Automtive manufactures British sports cars, a number of which are exported to New Zealand for payment in

pounds sterling. The distributor sells the sports cars in New Zealand for New Zealand dollars. The New Zealand

distributor is unable to carry all of the foreign exchange risk, and would not sell MacLoren models unless MacLoren

could share some of the foreign exchange risk. MacLoren has agreed that sales for a given model year will initially be

priced at a “base” spot rate between the New Zealand dollar and pound sterling set to be the spot mid-rate at the

the actual spot rate and the base rate. For the current model year the base rate is NZ$1.6400/£.

a. What are the outside ranges within which the New Zealand importer must pay at the then current spot rate?

b. If MacLoren ships 10 sports cars to the New Zealand distributor at a time when the spot exchange rate is

NZ$1.7000/£, and each car has an invoice cost £32,000, what will be the cost to the distributor in New Zealand

dollars? How many pounds will MacLoren receive, and how does this compare with McLaren’s expected sales receipt

Receipts to MacLoren in British pounds £320,000

(Within the band MacLoren receives £12,000/car)

d. How does this shift the currency risk?

e. Who benefits from this risk-sharing agreement?

Both parties in practice. The manufacturer has predictable revenues within the range, while the distributor bears a

Assumptions 2014 2015 2016 2017 2018

Sales volume (units) 1,000,000 1,000,000 1,000,000 1,000,000 1,000,000

Sales price per unit ₺80.50 ₺80.50 ₺80.50 ₺80.50 ₺80.50

Income Statement

Sales Revenue ₺80,500,000 ₺80,500,000 ₺80,500,000 ₺80,500,000 ₺80,500,000

Direct cost of goods sold -60,500,000 -60,500,000 -60,500,000 -60,500,000 -60,500,000

Cash flows from Valuation

Net income ₺8,504,000 ₺8,504,000 ₺8,504,000 ₺8,504,000 ₺8,504,000

Add back depreciation 3,770,000 3,770,000 3,770,000 3,770,000 3,770,000

Net Working Capital Calculations

Day of sales -€ 165,753 -€ 165,753 -€ 165,753 -€ 165,753 -€ 165,753

Day of direct COGS € 15,342 € 15,342 € 15,342 € 15,342 € 15,342

Accounts receivable days 45 45 45 45 45

Exhibit 12.6 Aidan Turkey—All Domestic Competitors

Using the Aidan Turkey analysis in Exhibits 12.5 and 12.6 where the Turkish lira depreciates, how would prices, costs, and volumes change if

Aidan Turkey was operating in a nearly purely domestic mature market with major domestic competitors?

Assumptions 2014 2015 2016 2017 2018

Sales volume (units) 1,400,000 1,400,000 1,400,000 1,400,000 1,400,000

Sales price per unit ₺80.50 ₺80.50 ₺80.50 ₺80.50 ₺80.50

Income Statement

Sales Revenue ₺112,700,000 ₺112,700,000 ₺112,700,000 ₺112,700,000 ₺112,700,000

Direct cost of goods sold -84,700,000 -84,700,000 -84,700,000 -84,700,000 -84,700,000

Cash flows from Valuation

Net income ₺14,904,000 ₺14,904,000 ₺14,904,000 ₺14,904,000 ₺14,904,000

Add back depreciation 3,770,000 3,770,000 3,770,000 3,770,000 3,770,000

Changes in net working capital 0 0 0 0 0

Net Working Capital Calculations

Day of sales -€ 232,055 -€ 232,055 -€ 232,055 -€ 232,055 -€ 232,055

Day of direct COGS € 15,342 € 15,342 € 15,342 € 15,342 € 15,342

Accounts receivable days 45 45 45 45 45

A/R (10,442,466) (10,442,466) (10,442,466) (10,442,466) (10,442,466)

Inventory days 10 10 10 10 10

Exhibit 12.7 Aidan Turkey—All Foreign Competitors

Aidan Turkey is now competing in a number of international (export) markets, growth markets, in which most of its competitors are foreign. Now

how would you expect Aidan Turkey’s operating exposure to respond to the depreciation of the Turkish lira?

Aidan Turkey would most likely try to profit from its now weak-currency home country, and would try and increase sales volumes dramatically in a

growth market by keeping the price in liras the same. The result is something like case 2 in the chapter discussion, where volume could jump

dramatically (thinking positive).

a. If each International Aero Engines turbofan engine is initially priced at €10.5 million, how has the price of that engine changed over the period shown when priced in Brazilian real at the current spot rate?

Date 1Q 2016 2Q 2016 3Q 2016 4Q 2016 1Q 2017 2Q 2017 3Q 2017 4Q 2017 1Q 2018 2Q 2018 3Q 2018 4Q 2018

b. What is the cumulative percentage change in the price of the engine in Brazilian real for the threeyear period?

Using the basic percentage change formula of (P2 – P1)/(P1), the percentage change is: 9.9%

d. Compare the prices and volumes for the first quarter of each of the three years shown in table (b) above. Who has benefited the most from the exchange rate changes?

1Q 2016 1Q 2017 1Q 2018 % Chg

Price (in millions of £)10.50€ 10.50€ 10.50€ 0.0%

Spot rate (€/£)3.9527 4.0898 4.2158

Price (in millions of €)€ 41.50 € 42.94 € 44.27 6.7%

Total cost to Airbus (millions of €)€ 4,150.34 € 5,153.15 € 6,197.23 49.3%

Total revenue to RR (millions of £)£1,050.00 £1,260.00 £1,470.00 40.0%

Problem 12.8 International Aero Engines Turbofan Engines

International Aero Engines is reevaluating its pricing strategy with a number of major customers in Brazil, particularly Embraer S.A. Since International Aero Engines is a Swiss company with most manufacturing of the Embraer T50

turbofan engines in France, costs are predominantly denominated in euros. But in the period shown in table (a) below, the euro steadily appreciated against the Brazilian real. International Aero Engines has traditionally denominated its

sales contracts with Embraer in Embraer’s home currency, the Brazilian real. After completing the following table, answer the questions that follow.

c. If the price elasticity of demand for International Aero Engines turbofan engines is relatively inelastic, and the price of the engine in euros never changes over the period, what does this price change mean for International

Aero Engines’ total sales revenue on sales to Embraer for this engine?

Exchange rate Prices in

Assumptions US dollar prices (R$/$) Brazilian reais

Existing sales price per unit $200.00 →3.4000 →680

If the reais falls in value, the new implied US$ price:

New dollar price if no reais price change $170.00 ←4.0000 ←680

Unit volume 50,000

Decrease in unit volume from price increase -20.0%

New lower unit volume 40,000

Alternative #2: Raise price in reais (and accept lower volume):

Sales revenue (R$800 x 40,000 ) / (R$4.000/$) $8,000,000

Less direct costs (US$120 x 40,000) 4,800,000

Contribution margin in US dollars $3,200,000

Discussion

Problem 12.9 Hurte-Paroxysm Products, Inc. (A)

Alternative #2 is preferable. In the short run (one year), HP Products would be better off to increase its sales price in reais in Brazil and accept the

lower sales volume. The contribution margin if reais prices are raised is $3,200,000, whereas if the price in reais is left unchanged HP Product’s

Hurte-Paroxysm Products, Inc. (HP) of the United States exports computer printers to Brazil, whose currency, the reais (symbol R$) has been

trading at R$3.40/US$. Exports to Brazil are currently 50,000 printers per year at the reais equivalent of $200 each. A strong rumor exists that the

reais will be devalued to R$4.00/$ within two weeks by the Brazilian government. Should the devaluation take place, the reais is expected to

remain unchanged for another decade. Accepting this forecast as given, HP Products faces a pricing decision which must be made before any

actual devaluation: HP Products may either (1) maintain the same reais price and in effect sell for fewer dollars, in which case Brazilian volume

will not change, or (2) maintain the same dollar price, raise the reais price in Brazil to compensate for the devaluation, and experience a 20% drop

Assumptions Value

Initial sales volume 50,000

End Contribution 12%

of year Sales volume US$ Revenue Direct Costs Margin PV Factor Present Value

1 50,000 $8,500,000 $6,000,000 $2,500,000 0.8929 $2,232,143

2 55,000 $9,350,000 $6,600,000 $2,750,000 0.7972 $2,192,283

Present value of contribution margins $12,809,008

Assumptions Value

Initial sales volume 40,000

End Contribution 12%

of year Sales volume US$ Revenue Direct Costs Margin PV Factor Present Value

1 40,000 $8,000,000 $4,800,000 $3,200,000 0.8929 $2,857,143

2 41,600 $8,320,000 $4,992,000 $3,328,000 0.7972 $2,653,061

Problem 12.10 Hurte-Paroxysm Products, Inc. (B)

Alternative #1: Maintain current Brazilian sales price and volume grows 10% per annum

Alternative #2: Raise Brazilian sales price to R$400 and volume grows only 4% per annum from a lower volume base

Assume the same facts as in Hurte-Paroxysm Products, Inc. (A). HP Products also believes that if it maintains the same price in Brazilian reais as a permanent policy,

volume will increase at 10% per annum for six years. Dollar costs will not change. At the end of six years HP Products’ patent expires and it will no longer export to

Brazil. After the reais is devalued to R$4.00/US$ no further devaluation is expected. If HP Products raises the price in reais so as to maintain its dollar price, volume will

increase at only 4% per annum for six years, starting from the lower initial base of 40,000 units. Again dollar costs will not change, and at the end of six years HP

Products will stop exporting to Brazil. HP Products’ weighted average cost of capital is 12%. Given these considerations, what do you recommend for HP Products’

pricing policy? Justify your recommendation.

3 43,264 $8,652,800 $5,191,680 $3,461,120 0.7118 $2,463,557

The buyer accepted the counterproposal in 48 hours and a sale agreement was signed and posted. The deal was done.

Contract value per year

¥2,925,000,000

b. What is the amount of the currency exposure for Centurion?

Contract value per year

¥2,925,000,000

Quarterly payment to Truckee

¥731,250,000 Truckee will receive a payment of 731.25 million Japanese yen ever quarter for three years.

Period (quarter number) 1 2 3 4 5 6 7 8 9 10 11 12

c. If the swap agreement is for a 3-year loan at 3.000% quarterly, what is the principal amount of the loan obligation (notional principal)?

Contract term (years)

3.00

Amortizing JPY Loan

Quarter number 1 2 3 4 5 6 7 8 9 10 11 12

Japanese loan interest payment -¥62.71 -¥57.70 -¥52.65 -¥47.56 -¥42.43 -¥37.26 -¥32.06 -¥26.82 -¥21.53 -¥16.21 -¥10.85 -¥5.44

a. Given the final contract value, what would the Japanese buyer believe they are paying per battery?

Problem 12.11 Centurion Batteries’ Japanese Yen Exposure

Centurion Batteries Ltd. is a privately held battery manufacturer located just outside of Melbourne, Australia. The company is one of the leading manufacturers of calcium plated batteries, specifically for the automobile market. Centurion

has been in intense contract negotiations with a Japanese automaker for months. It was late December 2016, and both sides wanted to conclude a deal before the new year.

The Japanese automaker wanted a two-year supply agreement for 200,000 Calcium-plated 12V battery packs per year. Battery prices had been dropping dramatically for years, but Centurion’s current sales price of A$180 per battery for

the 12V model (Ultra Hi Performance NS40ZLX MF Centurion) had held firm for months. The buyer was pushing for a lower unit price, but Centurion wanted a longer contract with higher volumes in return. After months of negotiations,

the buyer agreed to increase the contract to a three-years and increase annual purchases to 300,000 units. But in return, the buyer wanted a price of $147 per unit, and it wanted to pay in Japanese yen. Centurion had countered with the

following proposal. At an average price of $150 per unit, and a current spot exchange rate of ¥75.00/A$, Centurion proposed a contract of 260,000 units per year, for 3 years, with an annual purchase amount of:

Almost immediately, the corporate treasury group at Centurion was upset about the contract. They argued that the Japanese yen had begun to plummet in value against the Australian dollar in the past two months, so accepting the payment

in Japanese yen was too risky. Also, the quote had been based on a spot rate of ¥76.00/A$, but the rate had moved to ¥78.00/A$ over the past two weeks.

Centurion’s corporate treasury wanted to move immediately to hedge the longterm exposure. (Internally, the group had discussed that it was technically an anticipated transaction exposure, not a pure operating exposure, since it was a

receive Australian dollars. Their banker offered a swap where Centurion would receive Australian dollar LIBOR in return for paying Japanese yen at 3.000%. The swap agreement would be for three years and all payments made

Japanese loan principal payment -¥668.54 -¥673.55 -¥678.60 -¥683.69 -¥688.82 -¥693.99 -¥699.19 -¥704.44 -¥709.72 -¥715.04 -¥720.41 -¥725.81

Japanese loan, total quarterly payment -¥731.25 -¥731.25 -¥731.25 -¥731.25 -¥731.25 -¥731.25 -¥731.25 -¥731.25 -¥731.25 -¥731.25 -¥731.25 -¥731.25

d.The sales team had clearly not updated their exchange rate assumption prior to making the final contractual offer. As a result, assuming the swap was executed the same day as the closing spot rate quote, what was the

actual exchange rate locked for the three-year period?