22 Topics in International Macroeconomics

Notes to Instructor

Chapter Summary

This chapter covers extensions to the models presented in earlier chapters. There are four

topics covered:

■ purchasing power parity (PPP), especially the issue of why price levels are higher

in richer countries;

■ uncovered interest parity (UIP), and the implications of the fact that forex traders

Comments

This chapter provides extensions to earlier models presented in the textbook. These

sections can be presented independently. There are some connections made between the

sections in the conclusion following each, and in the conclusion section for the chapter.

1. Exchange Rates in the Long Run: Deviations from Purchasing Power Parity.

2. Exchange Rates in the Short Run: Deviations from Uncovered Interest

Parity. This section reconsiders empirical tests of the UIP condition and the

3. Debt and Default. This section models the repayment of sovereign debt as a

contingent claim based on the benefits and costs of default. The costs of default

4. Case Study: The Global Macroeconomy and the Global Financial Crisis. This

section begins with a review of the behavior of emerging market (EM) economies

market (DM) economies were the borrowers. Much of this massive flow was used

An outline of the chapter follows.

1. Exchange Rates in the Long Run: Deviations from Purchasing Power Parity

a. Limits to Arbitrage

b. Application: It’s Not Just the Burgers That Are Cheap

c Nontraded Goods and the Balassa‒Samuelson Model

i. A Simple Model

ii. Changes in Productivity

iii. Generalizing

d. Overvaluations, Undervaluations, and Productivity Growth: Forecasting

Implications for Real and Nominal Exchange Rates

iv. Convergence + Trend

v. Forecasting the Nominal Exchange Rate

vi. Adjustment to Equilibrium

e. Application: Real Exchange Rates in Emerging Markets

i. China: Yuan Undervaluation?

ii. Argentina: Was the Peso Overvalued?

iii. Slovakia: Obeying the Rules?

2. Exchange Rates in the Short Run: Deviations from Uncovered Interest Parity

a. Application: The Carry Trade

i. The Long and Short of It

ii. Carry Trade Summary

b. Headlines: Mrs. Watanabe’s Hedge Fund

c. Application: Peso Problems

d. The Efficient Markets Hypothesis

e. Limits to Arbitrage

i. Trade Costs Are Small

f. Conclusion

3. Debt and Default

a. A Few Peculiar Facts About Sovereign Debt

i. Summary

b. A Model of Default, Part One: The Probability of Default

i. Assumptions

c. Application: Is There Profit in Lending to Developing Countries?

d. A Model of Default, Part Two: Loan Supply and Demand

i. Loan Supply

ii. Loan Demand

iii. An Increase in Volatility

e. Application: The Costs of Default

Rate Crises

f. Conclusion

g. Application: The Argentina Crisis of 2001–2002

i. Background

ii. Dive

4. Case Study: The Global Macroeconomy and the Global Financial Crisis Crisis

a. Headlines: Is the IMF “Pathetic”?

b. Backdrop to the Crisis

i. Preconditions for the Crisis

c. Panic and the Great Recession

i. A Very Modern Bank Run

ii. Financial Decelerators

5. Conclusion: Lessons for Macroeconomics

Lecture Notes

In this chapter, we will examine four key questions and extension of models and analysis

from earlier in the textbook:

■ Is PPP a viable theory of exchange rates in the long run? Here, we develop an

■ Is UIP a viable theory of exchange rates in the short run? In reality, forex traders

make large profits, and these returns may be predictable. This runs contrary to the

■ Why do lenders loan resources to governments, even if they may default on their

debt? This chapter develops a model that studies the risk of default, the conditions

■ What went wrong during the 2007‒2009 financial crisis that led to the Great

Recession? Beginning with a discussion of the large financial flows from

1 Exchange Rates in the Long Run: Deviations from Purchasing Power

Parity

When we examine living standards across countries, measured in U.S. dollars, we

observe large differences that are partially attributed to deviations from PPP. That is,

although a country such as China may have low per capita income (7.5% of U.S. per

Limits to Arbitrage

First, we assume there are costs associated with trading goods. The trade cost, c, is

assumed to be equal to some fraction of the price of the good at its source. Therefore, the

price of the good when sold in the foreign country is

The existence of this trade cost affects the arbitrage incentives of traders. Prices in the

two locations, P (Home price) and EP* (Foreign price), can be different. Arbitrage will

only occur if the difference in the prices is large enough to compensate the trader for the

trade cost. Recall that the real exchange rate is defined as q= EP*/P.

■ Traders will buy the good in Home and sell in Foreign only if:

■ Traders will buy the good in Foreign and sell in Home only if:

This gives us a new no–arbitrage condition:

Implications:

■ Zero costs. When there are no trade costs (c = 0), q = 1, and the law of one price

(LOOP) holds exactly. This is shown in Figure 22-1, panel (a).

■ Low costs. When c is low, the deviations from PPP (and LOOP) will be small.

■ High costs. When c is large, the deviations from PPP (and LOOP) will be large.

The real exchange rate can fluctuate within a larger no-arbitrage band, shown in

Figure 22-1, panel (c).

When the costs of arbitrage are higher, the deviations from PPP and LOOP will be larger.

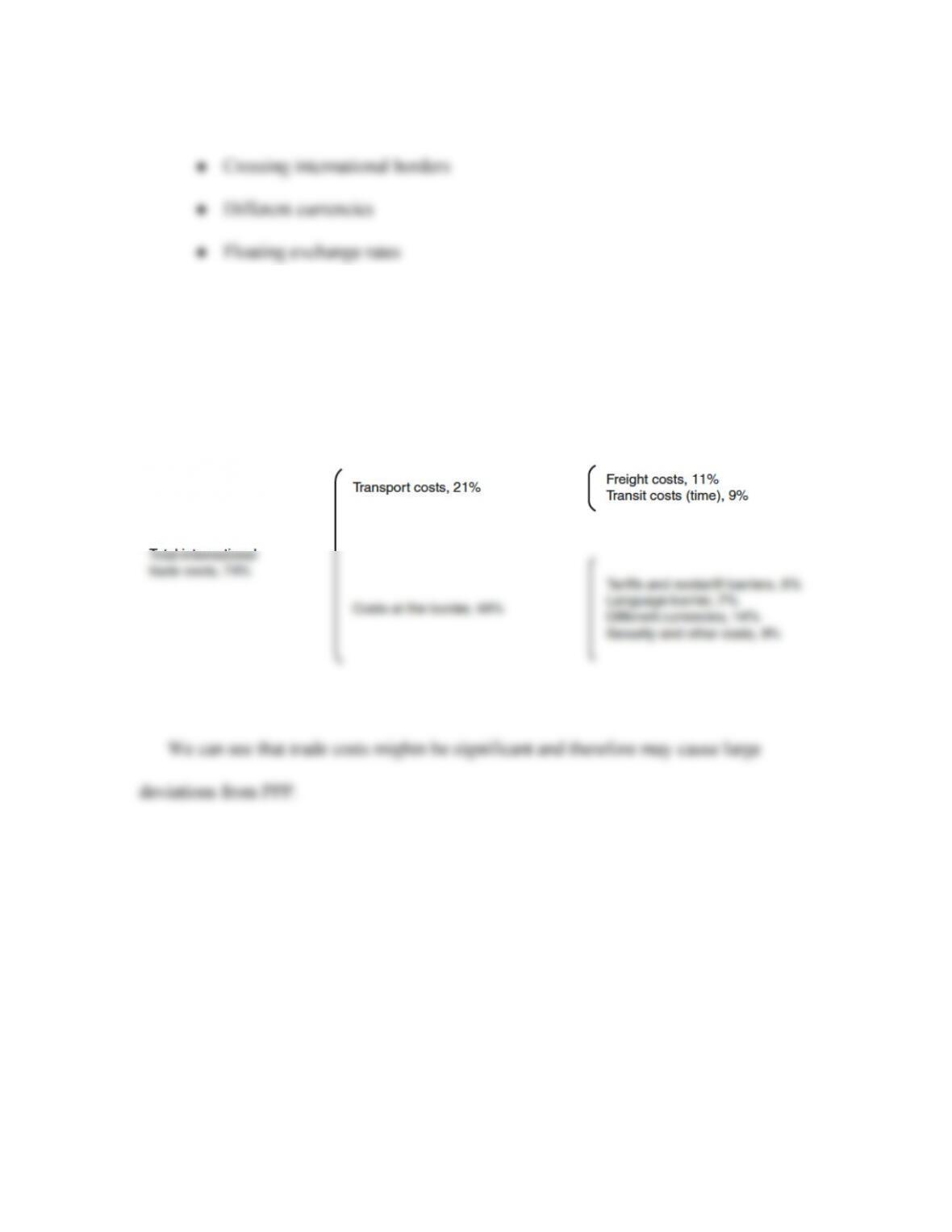

Trade Costs in Practice Recent research indicates that trade costs are affected by market

conditions, characteristics of goods, and economic policy. We consider these factors in

turn:

■ Transportation costs:

■ Trade policy:

● Average tariffs are 5% for advanced economies, 10% for developing

countries.

■ Other costs may arise from:

● Distance between markets

A recent summary of international trade costs for advanced countries estimates the trade

costs, expressed as a percent-age markup over the pre-shipment price of the goods, are

equal to 74% (averaged over all goods), disaggregated by source:

APPLICATION

It’s Not Just the Burgers That Are Cheap

Trade costs imply that the real exchange rate will not equal 1. This application examines

the size of these deviations using The Economist’s Big Mac Index.

■ Deviations in PPP are not random.

● Big Macs tend to be cheaper in poorer countries.

■ This can be explained by the existence of nontraded goods.

● The Big Mac is produced using a combination of traded goods (flour, beef,

and special sauce) and nontraded goods (cooks, cleaners, etc.).

● Figure 22-2, panel (a): The dollar price of the Big Mac is strongly correlated

with the local hourly wage (in dollars).

Most goods have some local, nontraded content–local value added or retail and/or

Nontraded Goods and the Balassa‒Samuelson Model

This section outlines a model with two goods: one traded and the other nontraded. An

overview of the model follows:

■ Two countries: Home and Foreign

● Both goods are produced in competitive markets and labor is the only input

used.

A Simple Model Solve the model in three steps:

1. The traded good has the same price in both countries. Because these goods have

no trade costs, they should sell for the same price in both countries. Prices are

denoted:

Note that LOOP holds for this good.

2. Productivity in traded goods determines wages. Each worker can produce A units

of the traded good per hour. The worker’s wage will be equal to $A (since the

price of the good is $1). Competition implies that each worker is paid his or her

3. Wages determine the prices of nontraded goods. Each worker can produce one

unit of the nontraded good per hour. Competition means that the dollar price of a

good is equal to the wage paid (the marginal cost). Therefore,

The model has the following implications:

■ The overall price level in the economy depends on the share of nontraded goods

in the consumption basket and on the productivity in traded goods.

Changes in Productivity Home productivity increases (A rises). The change in the price

level is calculated as the weighted average of the change in prices in traded and

nontraded goods:

For the foreign country,

Changes in productivity affect the overall price index:

■ When the productivity of traded good increases by x%, wages must increase by

the same percentage.

■ The nontraded goods price will rise by the same x% because the price of the

Generalizing A country has relatively low wages because it has relatively low

productivity in the production of traded goods. This low productivity keeps the price of

nontraded goods and the overall price index low.

appreciation in the real exchange rate, meaning its price level is rising.

Overvaluations, Undervaluations, and Productivity Growth: Forecasting

Implications for Real and Nominal Exchange Rates

The Balassa‒Samuelson effect tells us that overall price levels should be higher in richer

countries. This is shown in Figure 22-3. In the figure, the line that best fits the data (a

Forecasting the Real Exchange Rate Forecasting the real exchange rate, q can be

broken down into two problems:

Convergence Empirical estimates suggest the half-life of deviations from PPP is five

years. In this example, after five years, the real exchange rate will increase by half of the

approximately 2% each year.

Trend We now consider whether the equilibrium real exchange rate will change. To see

Convergence + Trend We can now calculate the implied change in the real exchange

Forecasting the Nominal Exchange Rate If we are able to forecast the real exchange

rate, this will help forecast the nominal exchange rate. From the definition of the real

Adjustment to Equilibrium The previous expression shows us that changes in the

nominal exchange rate occur because of:

■ the Balassa–Samuelson effect—changes in the real exchange rate stemming from

Based on the model, we know:

■ Real undervaluation—home goods will become more expensive.

● Home goods’ prices must increase, or

APPLICATION

Real Exchange Rates in Emerging Markets

Here, we apply the previous model to study the behavior of the exchange rates relative to

the U.S. dollar. The data are from Figure 22-3.

China: Yuan Undervaluation?

■ Chinese yuan, 2000

● Balassa‒Samuelson model prediction: = 0.319

■ What will happen to the real exchange rate?

● Convergence: Model predicts China will experience a 38% real appreciation

to close the gap (0.088/0.231).

● Trend: China’s growth rate exceeds that of the United States by 6%, implying

● Convergence + Trend: Model predicts a real appreciation of 5.9% (= 3.5 +

■ Forecasting the nominal exchange rate

● Nominal appreciation of yuan or increase in China’s inflation rate

● China pegged the yuan to the U.S. dollar but then adopted a crawling peg to

Argentina: Was the Peso Overvalued?

■ Argentine peso, 2000

■ What will happen to the real exchange rate?

● Model predicts Argentina will experience a 22% real depreciation to close the

■ What did happen?

● To maintain the peg, Argentina’s prices must decrease relative to the United

● Deflation meant wage and price cuts, and the overvalued peso hurt demand

for Argentine goods. An eventual crisis in the government and financial

Slovakia: Obeying the Rules?

■ Slovakian koruna in 2000

● Planned to join the EU and eventually the Eurozone. This required

■ Model predictions:

(0.252/0.656). Using the half-life estimates, this implies a 7.5% real

appreciation per year.

● Because Slovakia is growing more rapidly than the rest of the EU, this will

● Combined effects: real appreciation of 8.5% to 9.5% per year

■ Dilemma:

● Slovakia experienced real appreciation of 5% to 10% per year from 1992 to

2004.

● EU membership requires low inflation (within 2% of the lowest in the EU). In

Conclusion

In general, PPP does not hold. Prices of goods are not the same in all countries. Arbitrage

fails because of trade costs. The final stake in the heart of PPP is the Balassa‒Samuelson

theorem, which incorporates nontraded goods into the model. These effects mean that the