Managing Transaction Exposure ❖ 19

The spot rate of the euro as of today is $1.10. Interest rate parity exists. Indiana Company uses the

forward rate as a predictor of the future spot rate. The annual interest rate in the U.S. is 8% versus an

annual interest rate of 5% in the eurozone. Put options on euros are available with an exercise price of

$1.11, an expiration date of one year from today, and a premium of $.06 per unit. Estimate the dollar

cash flows it will receive as a result of using each strategy. Which hedge is optimal?

ANSWER:

Calculation of Forward Rate

Spot Rate

$1.10

US Interest Rate

0.08

Euro Interest Rate

0.05

p=

0.028571429

Forward Rate =

$1.13

Remain Unhedged

Future Spot Rate

$1.13

Amount of Euros to Convert

5,000,000

Cash flow

$5,657,142

Money Market Hedge

Amount of Receivables

5,000,000

Interest Rate to borrow euros

0.05

Amount in euros borrowed

4,761,904

$ received from converting

$5,238,095

U.S. deposit rate

0.08

$ accumulated after 1 yr

$5,657,142

Cash flow

$5,657,142

Put Option Hedge

Exercise Price

$1.11

Future Spot Rate

$1.13

Premium per Unit

$0.06

Exercise Option? NO

Amount of Receivables

5,000,000

Received per Unit

$1.07

Cash flow

$5,357,142

The money market hedge and unhedged strategy achieve the same outcome, which is more favorable

than the put option strategy.

41. Overhedging. Denver Co. is about to order supplies from Canada that are denominated in

Canadian dollars (C$). It has no other transactions in Canada and will not have any other transactions

in the future. The supplies will arrive in one year at which time payment is due. There is only one

Managing Transaction Exposure ❖ 20

supplier in Canada. Denver submits an order for 3 loads of supplies, which will be priced at C$3

million. The firm purchases C$3 million one year forward, since it anticipates that the Canadian

dollar will appreciate substantially over the year.

The existing spot rate is $.62, and the one-year forward rate is $.64. The supplier is not sure if it will

be able to provide the full order, so it guarantees Denver Co. only that it will ship one load of

supplies, and in this case, the supplies will be priced at C$1 million. Denver Co. will not know

whether it will receive one load or three loads until the end of the year.

Determine Denver’s total cash outflows in U.S. dollars under the scenario that the Canadian supplier

provides only one load of supplies, and that the spot rate of the Canadian dollar at the end of one year

is $.59. Show your work.

ANSWER:

Price per load of supplies (C$)

1,000,000

Loads of supplies needed

3

Total C$ needed

3,000,000

Spot Rate

$0.62

1 yr Forward Rate

$0.64

Spot Rate at end of 1 yr

$0.59

Calculations

Total C$ needed

3,000,000

x forward rate

$0.64

Equals US $ needed

$1,920,000

-$1,920,000

C$ left after 1 load of supplies

2,000,000

x spot rate at end of 1 yr

$0.59

Equals US $ left after purchase

$1,180,000.00

$1,180,000.00

Total cash outflows in US$

-$740,000

42. Long-term Hedging With Forward Contracts. Tampa Co. will build airplanes and export them

to Mexico for delivery in 3 years. The total payment to be received in 3 years for these exports is 900

million pesos. Today the peso’s spot rate is $.10. The annual U.S. interest rate is 4%, regardless of the

debt maturity. The annual Mexican interest rate is 9% regardless of the debt maturity. Tampa plans to

hedge its exposure with a forward contract that it will arrange today. Assume that interest rate parity

exists. Determine the dollar amount that Tampa will receive in 3 years.

ANSWER:

Since interest rate parity exists, determine the forward rate premium based on existing interest rates:

43. Timing the Hedge. Red River Co. (a U.S. firm) purchases imports that have a price of 400,000

Singapore dollars; it has to pay for the imports in 90 days. The firm will use a 90-day forward

contract to cover its payables. Assume that interest rate parity exists. This morning, the spot rate of

the Singapore dollar was $.50. At noon, the Federal Reserve reduced U.S. interest rates, while there

was no change in interest rates in Singapore. The Fed’s actions immediately increased the degree of

uncertainty surrounding the value of the Singapore dollar over the next three months. The Singapore

dollar’s spot rate remained at $.50 throughout the day, and that the U.S. and Singapore interest rates

were the same as of this morning. Also assume that the international Fisher effect holds. If Red River

Co. purchased a currency call option contract at the money this morning to hedge its exposure, would

you expect that its total U.S. dollar cash outflows be MORE THAN, LESS THAN, or THE SAME

AS the total U.S. dollar cash outflows if it had negotiated a forward contract this morning? Explain.

44. Hedging with Forward Versus Option Contracts. Assume that interest parity exists. Today, the

one-year interest rate in Canada is the same as the one-year interest rate in the U.S. Utah Co. uses the

forward rate to forecast the future spot rate of the Canadian dollar that will exist in one year. It needs

to purchase Canadian dollars in one year. Will the expected cost of its payables be lower if it hedges

its payables with a one-year forward contract on Canadian dollars or a one-year at-the-money call

option contract on Canadian dollars? Explain.

45. Hedging with a Bullspread. (See the chapter appendix.) Evar Imports Inc. buys chocolate from

Switzerland and resells it in the U.S. It just purchased chocolate invoiced at SF62,500; payment for

the invoice is due in 30 days. Assume that the current exchange rate of the Swiss franc is $.74. Also

assume that three call options for the franc are available. The first option has a strike price of $.74 and

a premium of $.03; the second option has a strike price of $.77 and a premium of $.01; and the third

option has a strike price of $.80 and a premium of $.006. Evar Imports is concerned about a modest

appreciation in the Swiss franc.

a. Describe how Evar Imports could construct a bullspread using the first two options. What is the

cost of this hedge? When is this hedge most effective? When is it least effective?

b. Describe how Evar Imports could construct a bullspread using the first option and the third

option. What is the cost of this hedge? When is this hedge most effective? When is it least

effective?

c. Given your answers to parts (a) and (b), what is the tradeoff involved in constructing a bullspread

using call options with a higher exercise price?

ANSWER:

a. Evar Imports Inc. would buy the first option and write the second option. It would pay SF62,500

Managing Transaction Exposure ❖ 22

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

b. Evar Imports Inc. would buy the first option and write the third option. It would pay SF62,500 ×

46. Hedging with a Bearspread. (See the chapter appendix.) Marson Inc. has some customers in Canada

and frequently receives payments denominated in Canadian dollars (C$). The current spot rate for the

Canadian dollar is $.75. Two call options on Canadian dollars are available. The first option has an

exercise price of $.72 and a premium of $.03. The second option has an exercise price of $.74 and a

premium of $.01. Marson Inc. would like to use a bearspread to hedge a receivable position of

C$50,000, which is due in one month. Marson is concerned that the Canadian dollar may depreciate

to $.73 in one month.

a. Describe how Marson Inc. could use a bearspread to hedge its position.

b. Assume the spot rate of the Canadian dollar in one month is $.73. Was the hedge effective?

ANSWER:

b. If the spot rate of the Canadian dollar is $.73 in one month, the hedge would have been

47. Hedging with Straddles. (See the chapter appendix.) Brooks, Inc. imports wood from Morocco. The

Moroccan exporter invoices these products in Moroccan dirham. The current exchange rate of the

dirham is $.10. Brooks just purchased wood for 2 million dirham and should pay for the wood in

three months. It is also possible that Brooks will receive 4 million dirham in three months from the

sale of refinished wood in Morocco. Brooks is currently in negotiations with a Moroccan importer

about the refinished wood. If the negotiations are successful, Brooks will receive 4 million dirham in

three months, for a net cash inflow of 2 million dirham. The following option information is

available:

• Call option premium on Moroccan dirham = $.003

• Put option premium on Moroccan dirham = $.002

• Call and put option strike price = $.098

• One option contract represents 500,000 dirham.

Managing Transaction Exposure ❖ 23

a. Describe how Brooks could use a straddle to hedge its possible positions in dirham.

b. Consider three scenarios. In the first scenario, the dirham’s spot rate at option expiration is equal

to the exercise price of $.098. In the second scenario, the dirham depreciates to $.08. In the third

scenario, the dirham appreciates to $.11. For each scenario, consider both the case when the

negotiations are successful and the case when the negotiations are not successful. Assess the

effectiveness of the long straddle in each of these situations by comparing it to a strategy of using

long call options to hedge.

ANSWER:

a. Brooks could construct a long straddle to hedge its positions in dirham. If the negotiations are

b.

Net Cash Flow = +2 million Dirham

Dirham value = $.11 in three

months

Net receipt = (2 million ×

$.11) + (2 million × [$.11 –

$.098]) – (2 million × [$.003

+ $.002] = $234,000

* Brooks converts excess

dirham to dollars in the spot

market.

*It lets the put option expire.

*It exercises its call options

and sells the dirham obtained

from this transaction in the

spot market; the proceeds

recapture part of the premiums

that were paid to for the

options.

Dirham value = $.08 in three

months

Net receipt = (2 million ×

$.098) – (2 million × [$.003

+ $.002]) = $186,000

* Brooks converts excess

dirham to dollars at $.098, by

exercising its put options.

*It lets the call option expire.

Dirham value = $.098 in three

months

Net receipt = (2 million ×

$.098) – (2 million × [$.003 +

$.002]) = $186,000

*Brooks converts excess

dirham to dollars in the spot

market.

*It lets its call options and its

put options expire.

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure ❖ 25

*hedge with one-year forward contract,

*hedge with a money market hedge,

*hedge with at-the-money put options on Swiss francs with a one-year expiration date, or

*remain unhedged.

Which alternative will generate the highest expected amount of dollars? If multiple alternatives are

tied for generating the highest expected amount of dollars, list each of them.

50. PPP and Hedging with Call Options. Visor Inc. (a U.S. firm) has agreed to purchase supplies from

Argentina and will need 1 million Argentine pesos in one year. Interest rate parity presently exists.

The annual interest rate in Argentina is 19%, versus 6% in the U.S. You expect that annual inflation

will be about 11% in Argentina and 4% in the U.S. The spot rate of the Argentine peso is $.30. Call

options on pesos are available with a one-year expiration date, an exercise price of $.29, and a

premium of $0.03 per unit. Determine the expected amount of dollars that you will pay from hedging

with call options (including the premium paid for the options) if you expect that the spot rate of the

peso will change over the next year based on purchasing power parity (PPP).

51. Long-term Forward Contracts. Assume that interest rate parity exists. The annualized interest rate

is presently 5% in the U.S. for any term to maturity and is 13% in Mexico for any term to maturity.

Dokar Co. (a U.S. firm) has an agreement under which it will develop and export software to

Mexico’s government two years from now and will receive 20 million Mexican pesos in two years.

The spot rate of the peso is $.10. Dokar uses a 2-year forward contract to hedge its receivables in two

years. How many dollars will Dokar Co. receive in two years? Show your work.

52. Money Market Versus Put Option Hedge. Narto Co. (a U.S. firm) exports to Switzerland and

expects to receive 500,000 Swiss francs in one year. The one-year U.S. interest rate is 5% when

investing funds and 7% when borrowing funds. The one-year Swiss interest rate is 9% when investing

funds, and 11% when borrowing funds. The spot rate of the Swiss franc is $.80. Narto expects that the

spot rate of the Swiss franc will be $.75 in one year. A put option is available on Swiss francs with an

exercise price of $.79 and a premium of $.02.

Managing Transaction Exposure ❖ 26

a. Determine the amount of dollars that Narto Co. will receive at the end of one year if it

implements a money market hedge.

b. Determine the amount of dollars that Narto Co. expects to receive at the end of one year (after

accounting for the option premium) if it implements a put option hedge.

ANSWER:

53. Forward Versus Option Hedge. Assume that interest parity exists. Today, the one-year interest rate

in Japan is the same as the one-year interest rate in the U.S. You use the international Fisher effect

when forecasting how exchange rates will change over the next year. You will receive Japanese yen

in one year. You can hedge receivables with a one-year forward contract on Japanese yen or a one-

year at-the-money put option contract on Japanese yen. If you use a forward hedge, will your

expected dollar cash flows in one year be higher than, lower than, or the same as if you had used put

options? Explain.

54. Long-term Hedging. Rebel Co. (a U.S. firm) has a contract with the government of Spain and will

receive payments of 10,000 euros in exchange for consulting services at the end of each of the next 10

years. The annualized interest rate in the U.S. is 6% regardless of the term to maturity. The

annualized interest rate for the euro is 6% regardless of the term to maturity. Assume you expect that

the interest rates for the U.S. and for the euro to be the same at any future time, regardless of the term

to maturity. Assume that interest rate parity exists. Rebel considers two alternative strategies:

Strategy (1) – Use forward hedging one year in advance of the receivables, such that at the end of

each year, it creates a new one-year forward hedge for the receivables,

Strategy (2) – Establish a hedge today for all future receivables (a one-year forward hedge for

receivables in one year, a two-year forward hedge for receivables in two years, and so on).

a. Assume that the euro depreciates consistently over the next 10 years. Will strategy 1 result in

higher, lower, or the same cash flows for Rebel Co. as strategy 2?

b. Assume that the euro appreciates consistently over the next 10 years. Will strategy 1 result in

higher, lower, or the same cash flows for Rebel Co. as strategy 2?

Managing Transaction Exposure ❖ 27

ANSWER:

a. Lower, because if the euro depreciates over time, so will the one-year forward rate. Thus, the

55. Long-term Hedging. San Fran Co. imports products. It will pay 5 million Swiss francs for

imports in one year. Mateo Co. will also pay 5 million Swiss francs for imports in one year. San Fran

Co. and Mateo Co. will also need to pay 5 million Swiss francs for imports arriving in 2 years.

Today, Mateo Co. uses a one-year forward contract to hedge its payables in one year. A year from

today, it will use a one-year forward contract to hedge the payables that it must pay two years from

today.

Today, San Fran Co. uses a one-year forward contract to hedge its payables due in one year. Today, it

also uses a two-year forward contract to hedge its payables in two years.

Interest rate parity exists and it continues to exist in the future. You expect that the Swiss franc will

consistently depreciate over the next two years.

Switzerland and the U.S. have similar interest rates, regardless of their maturity, and they will

continue to be the same in the future. Will the total expected dollar cash outflows that San Fran Co.

will pay for its payables be higher than, lower than, or the same as the total expected dollar cash

outflows that Mateo Co. will pay? Explain.

ANSWER: The dollar cash outflows will be higher for San Fran Co. than for Mateo Co. Because

both countries have similar interest rates, the forward rate of the franc will contain neither a discount

56. Comparison of Hedging Techniques. Today, the spot rate of the euro is $1.20, and the one-year

forward rate is $1.16. A one-year call option on euros exists with a premium of $.04 per unit and an

exercise price of $1.17. You think the spot rate is the best forecast of future spot rates. You will need

to pay 10 million euros in one year. Determine whether a money market hedge or a call option hedge

would be more appropriate to hedge your payables.

ANSWER: Money market hedge: Invest in euros today so that you have enough to pay 10 million

Managing Transaction Exposure ❖ 28

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Repay $ dollar loan in 1 year: $11,009,1174 x (1.04) = $11,449,541.

Call option hedge: Since you expect to exercise the call option, Cost per unit = Exercise price of

$1.17 + premium of $.04 = $1.21. So, cost in dollars = $1.21 x 10,000,000 = $12,100,000.

Conclusion: Money market hedge is more appropriate because the cost is lower than the expected cost

of a call option hedge.

57. IRP, PPP, and the Hedging Decision. The one-year U.S. interest rate is presently higher than the

Japanese interest rate. Assume a real rate of interest of zero percent in each country. Assume that

interest rate parity exists. You believe in purchasing power parity (PPP). You have receivables of 10

million Japanese yen that you will definitely receive in one year. Should you hedge? Briefly explain.

58. Cross-Hedging Strategy. Assume that the country of Dreeland has a currency (called the dree) that

tends to move in tandem with the Chile peso and is expected to continue to move in tandem with the

Chilean peso in the future. Indianapolis Co., a U.S. firm, has a large amount of receivables in the

dree. It expects that the dree will depreciate against the dollar over time. No derivatives are available

on the dree. Indianapolis Co. considers the following strategies to reduce its exchange rate risk: (a)

use a money market hedge in which it converts dollars into dree and maintains a deposit in the dree

for one year, (b) use a forward contract to purchase Chilean pesos forward, (c) sell a put option hedge

on Chilean pesos, (d) purchase a call option on Chilean pesos, and (e) use a forward contract in which

it sells Chilean pesos forward. Which strategy is most appropriate?

59. Estimating the Hedged Cost of Payables. Grady Co. is a manufacturer of hockey equipment in

Chicago and will need 3 million Swiss francs (SF) in one year to pay for imported supplies. The U.S.

one-year interest rate is 2% versus 7% for Switzerland. The spot rate of the SF is $.90, and the one-

year forward rate of the SF is $.88. A one-year call option on SF exists with an exercise price of $.90

and a premium of $.03 per unit. As the treasurer of Grady Co., you think the spot rate of the SF is the

best forecast of the future spot rate of the SF.

a. If you use a money market hedge, determine the amount of dollars that you will pay for the

payables.

b. If you use a call option hedge, determine the expected amount of dollars that you will pay for the

payables (account for the option premium within your estimate).

Managing Transaction Exposure ❖ 29

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

b. Cost per unit = Exercise price of $.90 + premium of $.03 = $.93.

Cost in dollars = $.93 x 3,000,000 = $2,790,000.

CRITICAL THINKING

Currency Options Versus Forward Contracts Write a short essay briefly summarizing the advantages

and disadvantages of currency options as compared to forward contracts when hedging payables. Explain

the conditions (regarding your expectations of the future exchange rate and the uncertainty surrounding the

future exchange rate) that might cause you to use currency options instead of forward contracts if you were

exposed to payables. Do you think you would use currency options or forward contracts more frequently?

ANSWER:

Solution to Continuing Case Problem: Blades, Inc.

1. Using a spreadsheet, compare the hedging alternatives for the Thai baht with a scenario under which

Blades remains unhedged. Do you think Blades should hedge or remain unhedged? If Blades should

hedge, which hedge is most appropriate?

ANSWER: (See spreadsheet attached.) Based on the analysis, it appears that Blades should hedge its

Calculation of Net Baht Paid or Received in 90 Days:

Baht-denominated inflow:

Pairs sold

45,000

× Revenue per pair

4,594

= Number of baht received in 90 days

206,730,000

Baht-denominated outflow:

Pairs manufactured

18,000

× Estimated cost per pair

3,000

= Number of baht needed in 90 days

54,000,000

Net inflow (outflow) in baht anticipated in 90 days

152,730,000

Forward Hedge:

Sell baht 90 days forward:

Baht-denominated revenue

152,730,000

– Forward rate of baht

0.0215

= Dollars to be received in 90 days

3,283,695.00

Managing Transaction Exposure ❖ 30

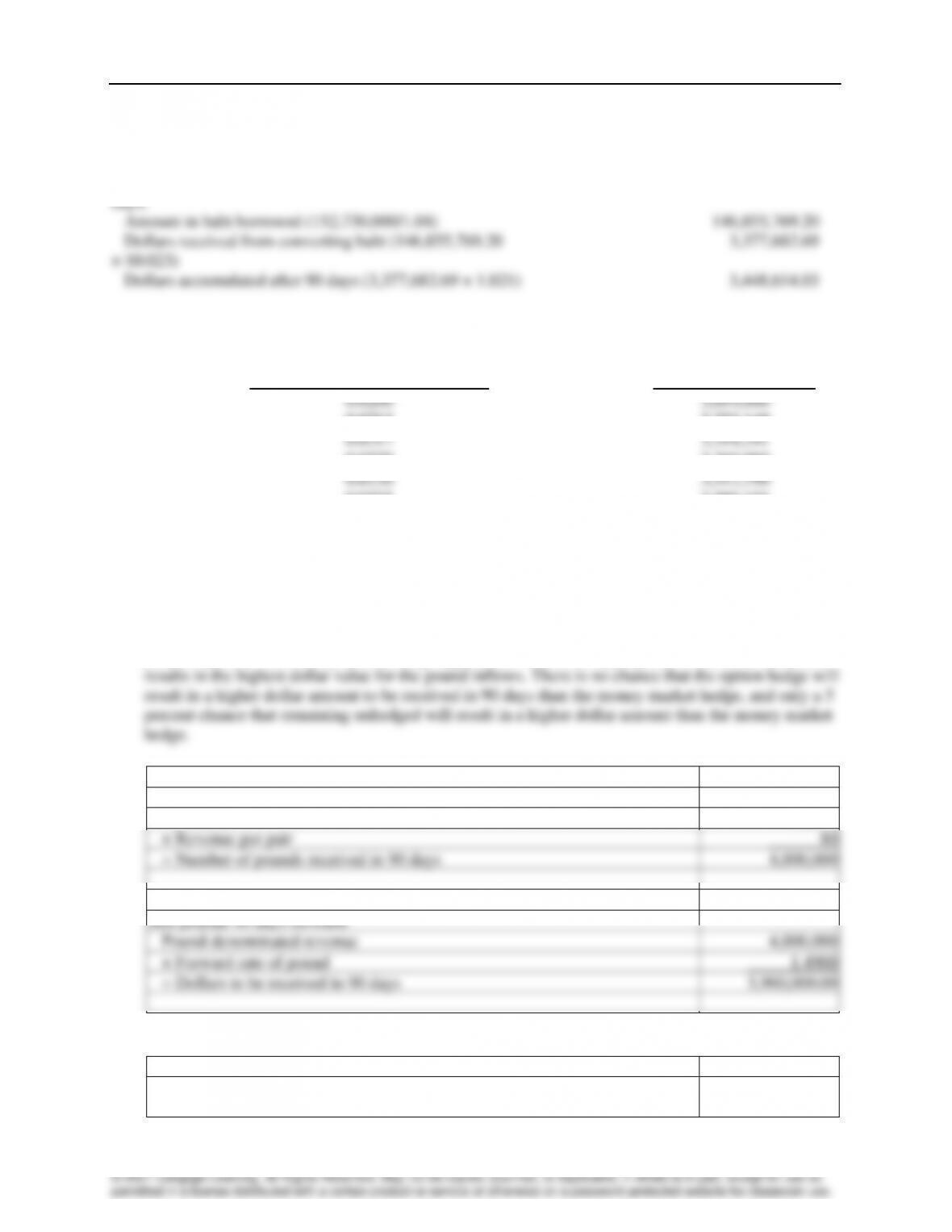

Money Market Hedge:

Borrow baht, convert to $, invest $, use receivables to pay off loan in 90

days:

Amount in baht borrowed (152,730,000/1.04)

146,855,769.20

Dollars received from converting baht (146,855,769.20

× $0.023)

3,377,682.69

Dollars accumulated after 90 days (3,377,682.69 × 1.021)

3,448,614.03

Remain Unhedged:

Total Dollars Received

Possible Spot Rate in 90 Days ($)

from Converting Baht

0.0200

3,054,600

0.0213

3,253,149

0.0217

3,314,241

0.0220

3,360,060

0.0230

3,512,790

0.0235

3,589,155

2. Using a spreadsheet, compare the hedging alternatives for the British pound receivables with a

scenario under which Blades remains unhedged. Do you think Blades should hedge or remain

unhedged? Which hedge is the most appropriate for Blades?

ANSWER: (See spreadsheet attached.) Based on the analysis, it appears that Blades should hedge its

pound exposure. The money market hedge appears to be the most appropriate for Blades, because it

Calculation of Pounds Received in 90 Days:

Pound-denominated inflow:

Pairs sold

50,000

× Revenue per pair

80

= Number of pounds received in 90 days

4,000,000

Forward Hedge:

Sell pounds 90 days forward:

Pound-denominated revenue

4,000,000

× Forward rate of pound

1.4900

= Dollars to be received in 90 days

5,960,000.00

Money Market Hedge:

Borrow pounds, convert to $, invest $, use receivables to pay off loan in 90

days:

Managing Transaction Exposure ❖ 31

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Amount in pounds borrowed (4,000,000/1.02)

3,921,568.63

Dollars received from converting pounds (3,921,568.63 × $1.50)

5,882,352.94

Dollars accumulated after 90 days (5,882,352.94 × 1.021)

6,005,882.35

Put Option Hedge:

Purchase put option:

Total Dollars Total Dollars

Premium Received per Received from

Possible Spot per Unit Unit (after Converting

Rate in 90 Paid for Exercise accounting for 4,000,000

Days ($) Option ($) Option? the premium) Pounds Probability

1.47 0.02 Y 1.45 5,800,000 20%

1.49 0.02 N 1.47 5,880,000 25%

Remain Unhedged:

Possible Spot Total Dollars

Rate in 90 Received from

Days ($) Converting Pounds Probability

$1.45 $5,800,000 5%

1.48 5,920,000 30%

1.50 6,000,000 15%

3. In general, do you think it is easier for Blades to hedge its inflows or its outflows denominated in

foreign currencies? Why?

4. Would any of the hedges you compared in question 2 for the British pounds to be received in 90 days

require Blades to overhedge? Given Blades’ exporting arrangements, do you think it is subject to

overhedging with a money market hedge?

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

5. Could Blades modify the timing of the Thai imports to reduce its transaction exposure? What is the

tradeoff of such a modification?

ANSWER: Blades could import sufficient materials to completely offset the baht-denominated

inflows this period. Since Blades will generate baht-denominated revenue of 45,000 × 4,594 =

6. Could Blades modify its payment practices for the Thai imports in order to reduce its transaction

exposure? What is the tradeoff of such a modification?

7. Given Blades’ exporting agreements, are there any long-term hedging techniques from which Blades

could benefit? For this question only, assume that Blades incurs all of its costs in the United States.

Solution to Supplemental Case: Blackhawk Company

This case uses actual data to show how inaccurate forecasts can be.

a. Using the regression model in which FSR is the dependent variable and FR is the independent

variable, the slope coefficient is about .857 and the standard error of the coefficient is .0825.

Therefore, the t-statistic in testing for a bias is:

Managing Transaction Exposure ❖ 33

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

b. There appears to be a bias, in that the use of the forward rate resulted in negative forecast errors

e. There appears to be a bias, in that the use of the spot rate resulted in negative forecast errors

(overestimation) over the first 9 quarters and then positive forecast errors (under-estimation) over 7 of

= 9.457%

If the NZ$ rises by 9.457%, the FSR will be $.589 (1.09457) = about $.645.

h. The probability distribution for FSR is:

Probability FSR

40% $.6450

40% $.5878

20% $.5890

Managing Transaction Exposure ❖ 34

i. The probability distribution for payments if Blackhawk does not hedge is:

$ Amount

Probability Needed

40% $516,000

40% $470,240

20% $471,200

j. The probability distribution for the real cost of hedging is determined below:

$ Amount $ Amount

Needed if Needed if Real Cost

Probability Hedged Unhedged of Hedging

40% $470,240 $516,000 –$45,760

40% $470,240 $470,240 $0

20% $470,240 $471,200 –$960

k. The probability distribution of payments when owning a call option is shown below:

Exercise

Probability FSR Option? $ Needed (incl. prem.)

(1.021)

= NZ$783,545

Amount of $ to borrow = NZ$783,545 × $.589

= $461,508

Managing Transaction Exposure ❖ 35

Hedging Decisions by the Sports Exports Company

1. Determine the amount of dollars received by the Sports Exports Company if it does not hedge the

receivables to be received in one month under each of the two exchange rate scenarios.

ANSWER:

Scenario I: A 3% rate of depreciation reflects a future spot rate (in one month) of:

2. Determine the amount of dollars received by the Sports Exports Company if it uses a put option to

hedge receivables in one month under each of the two exchange rate scenarios.

ANSWER:

Scenario I: The put option would be hedged, resulting in the conversion of 10,000 pounds at an

exchange rate of $1.645:

3. Determine the amount of dollars received by the Sports Exports Company if it uses a forward hedge

to hedge receivables in one month under each of the two exchange rate scenarios.

Managing Transaction Exposure ❖ 36

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

ANSWER: The forward rate is $1.645. Therefore, the amount of dollars to be received regardless of

the exchange rate scenario is:

10,000 × $1.645 = $16,450

4. Summarize the results of dollars received based on an unhedged strategy, a put option strategy, and a

forward hedge strategy. Select the strategy that you prefer based on the information provided.

ANSWER:

Results Based Results Based

on Scenario I on Scenario II

Unhedged Strategy $16,005 $16,830