Chapter 11

Managing Transaction Exposure

Lecture Outline

Policies for Hedging Transaction Exposure

Hedging Most of the Exposure

Selective Hedging

Hedging Exposure to Payables

Forward or Futures Hedge on Payables

Money Market Hedge on Payables

Call Option Hedge on Payables

Comparison of Techniques for Hedging Payables

Evaluating Past Decisions on Hedging Payables

Hedging Receivables

Forward or Futures Hedge

Money Market Hedge

Put Option Hedge

Limitations of Hedging

Limitation of Hedging an Uncertain Payment

Limitation of Repeated Short-term Hedging

Alternative Methods to Reduce Exchange Rate Risk

Leading and Lagging

Cross-Hedging

Currency Diversification

Managing Transaction Exposure ❖ 2

Chapter Theme

A primary objective of the chapter is to provide an overview of hedging techniques. Yet, transaction

exposure cannot always be hedged in all cases. Even when it can be hedged, the firm must decide

whether a hedge is feasible. An MNC can incorporate its expectations about future exchange rates, future

inflows and outflows, as well as its degree of risk aversion to make hedging decisions.

Topics to Stimulate Class Discussion

1. Is transaction exposure relevant?

2. Why should a firm bother identifying net transaction exposure?

3. Should management of transaction exposure be conducted at the subsidiary level or at the centralized

level? Why?

POINT/COUNTER-POINT:

Should an MNC Risk Overhedging?

POINT: Yes. MNCs have some “unanticipated” transactions that occur without any advance notice. They

should attempt to forecast the net cash flows in each currency due to unanticipated transactions based on

the previous net cash flows for that currency in a previous period. Even though it would be impossible to

forecast the volume of these unanticipated transactions per day, it may be possible to forecast the volume

on a monthly basis. For example, if an MNC has net cash flows between 3,000,000 and 4,000,000

Philippine pesos every month, it may presume that it will receive at least 3,000,000 pesos in each of the

next few months unless conditions change. In this case, it can hedge a position of 3,000,0000 in pesos by

selling that amount of pesos forward or buying put options on that amount of pesos. Any amount of net

cash flows beyond 3,000,000 pesos will not be hedged, but at least the MNC was able to hedge the

minimum expected net cash flows.

COUNTER-POINT: No. MNCs should not hedge unanticipated transactions. When they overhedge the

expected net cash flows in a foreign currency, they remain exposed to exchange rate risk. If they sell more

currency as a result of forward contracts than their net cash flows, they will be adversely affected by an

increase in the value of the currency. Their initial reasons for hedging were to protect against the

weakness of the currency, but the overhedging described here would simply shift their exposure.

Overhedging does not insulate an MNC against exchange rate risk. It just changes the means by which the

MNC is exposed.

WHO IS CORRECT? Use the Internet to learn more about this issue. Offer your own opinion on this

issue.

Managing Transaction Exposure ❖ 3

ANSWER: If the MNC is confident that it will receive net cash flows in a currency that will likely

Answers to End of Chapter Questions

1. Hedging in General. Explain the relationship between hedging (discussed in this chapter)

measuring exposure (discussed in Chapter 10).

2. Money Market Hedge on Receivables. Assume that Stevens Point Co. has net receivables of

100,000 Singapore dollars in 90 days. The spot rate of the S$ is $.50, and the Singapore interest rate

is 2% over 90 days. Suggest how the U.S. firm could implement a money market hedge. Be precise.

3. Money Market Hedge on Payables. Assume that Hampshire Co. has net payables of 200,000

Mexican pesos in 180 days. The Mexican interest rate is 7% over 180 days, and the spot rate of the

Mexican peso is $.10. Suggest how the U.S. firm could implement a money market hedge. Be

precise.

4. Net Transaction Exposure. Why should an MNC identify net exposure before hedging?

5. Hedging with Futures. Explain how a U.S. corporation could hedge net receivables in euros with

futures contracts. Explain how a U.S. corporation could hedge net payables in Japanese yen with

futures contracts.

6. Hedging with Forward Contracts. Explain how a U.S. corporation could hedge net receivables in

Malaysian ringgit with a forward contract.

Explain how a U.S. corporation could hedge payables in Canadian dollars with a forward contract.

7. Real Cost of Hedging Payables. Assume that Loras Corp. imported goods from New Zealand and

needs 100,000 New Zealand dollars 180 days from now. It is trying to determine whether to hedge

this position. Loras has developed the following probability distribution for the New Zealand dollar:

Possible Value of

New Zealand Dollar in 180 Days Probability

$.40 5%

.45 10%

.48 30%

.50 30%

.53 20%

.55 5%

The 180–day forward rate of the New Zealand dollar is $.52, and the spot rate of the New Zealand dollar is

$.49. Develop a table showing a feasibility analysis for hedging. That is, determine the possible

differences between the costs of hedging versus no hedging. What is the probability that hedging will be

more costly to the firm than not hedging? Determine the expected value of the additional cost of hedging.

ANSWER:

Possible Spot Rate

of New Zealand

Dollar

Probability

Nominal Cost of

Hedging 100,000

NZ$

Amount of U.S.

Dollars Needed to

Buy 100,000 NZ$ if

Firm Remains

Unhedged

Real Cost of

Hedging

$.40

5%

$52,000

$40,000

$12,000

$.45

10%

$52,000

$45,000

$7,000

$.48

30%

$52,000

$48,000

$4,000

$.50

30%

$52,000

$50,000

$2,000

$.53

20%

$52,000

$53,000

-$1,000

$.55

5%

$52,000

$55,000

-$3,000

ANSWER: There is a 75% probability that hedging will be more costly than no hedge.

5%($12,000) + 10%($7,000) + 30%($4,000) + 30%($2,000) + 20%(–$1,000) + 5%(–$3,000)

= $600 + $700 + $1200 + $600 – $200 – $150

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

8. Benefits of Hedging. If hedging is expected to be more costly than not hedging, why would a firm

even consider hedging?

9. Real Cost of Hedging Payables. Assume that Suffolk Co. negotiated a forward contract to purchase

200,000 British pounds in 90 days. The 90-day forward rate was $1.40 per British pound. The

pounds to be purchased were to be used to purchase British supplies. On the day the pounds were

delivered in accordance with the forward contract, the spot rate of the British pound was $1.44. What

was the real cost of hedging the payables for this U.S. firm?

10. Hedging Decision. Kayla Co. imports products from Mexico, and it will make payment in pesos

in 90 days. Interest rate parity holds. The prevailing interest rate in Mexico is very high, which

reflects the high expected inflation there. Kayla expects that the Mexican peso will depreciate over

the next 90 days, yet, it plans to hedge its payables with a 90-day forward contract. Why may Kayla

believe that it will pay a smaller amount of dollars when hedging than if it remains unhedged?

11. Hedging Payables. Assume the following information:

90-day U.S. interest rate = 4%

90-day Malaysian interest rate = 3%

90-day forward rate of Malaysian ringgit = $.400

Spot rate of Malaysian ringgit = $.404

Assume that the Santa Barbara Co. in the United States will need 300,000 ringgit in 90 days. It

wishes to hedge this payables position. Would it be better off using a forward hedge or a money

market hedge? Substantiate your answer with estimated costs for each type of hedge.

ANSWER: If the firm uses the forward hedge, it will pay out 300,000($.400) = $120,000 in 90 days.

12. Hedging Decision on Receivables. Assume the following information:

180-day U.S. interest rate = 8%

180-day British interest rate = 9%

180-day forward rate of British pound = $1.50

Spot rate of British pound = $1.48

Assume that Riverside Corp. from the United States will receive 400,000 pounds in 180 days. Would

it be better off using a forward hedge or a money market hedge? Substantiate your answer with

estimated revenue for each type of hedge.

ANSWER: If the firm uses a forward hedge, it will receive 400,000($1.50) = $600,000 in 180 days.

13. Currency Options. Relate the use of currency options to hedging net payables and receivables. That

is, when should a firm purchase currency puts, and when should it purchase currency calls? Why

would Cleveland, Inc., consider hedging net payables or net receivables with currency options rather

than forward contracts? What are the disadvantages of hedging with currency options as opposed to

forward contracts?

14. Currency Options. Can Brooklyn Co. determine whether currency options will be more or less

expensive than a forward hedge when considering both hedging techniques to cover net payables in

euros? Why or why not?

15. Long-term Hedging. How can a firm hedge its long-term currency positions? Elaborate on each

method.

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

16. Leading and Lagging. Under what conditions would Zona Co.’s subsidiary consider using a

“leading” strategy to reduce transaction exposure? Under what conditions would Zona Co.’s

subsidiary consider using a “lagging” strategy to reduce transaction exposure?

17. Cross-Hedging. Explain how a firm can use cross-hedging to reduce transaction exposure.

18. Currency Diversification. Explain how a firm can use currency diversification to reduce its

transaction exposure.

19. Hedging with Put Options. As treasurer of Tucson Corp. (a U.S. exporter to New Zealand), you

must decide how to hedge (if at all) future receivables of 250,000 New Zealand dollars 90 days from

now. Put options are available for a premium of $.03 per unit and an exercise price of $.49 per New

Zealand dollar. The forecasted spot rate of the NZ$ in 90 days follows:

Future Spot Rate Probability

$.44 30%

.40 50

.38 20

Given that you hedge your position with options, create a probability distribution for U.S. dollars to

be received in 90 days.

ANSWER:

Possible

Spot Rate

Put Option

Premium

Exercise

Option?

Amount per

Unit Received

Accounting

for Premium

Total Amount

Received for

NZ$250,000

Probability

$.44

$.03

Yes

$.46

$115,000

30%

$.40

$.03

Yes

$.46

$115,000

50%

$.38

$.03

Yes

$.46

$115,000

20%

20. Forward Hedge. Would Oregon Co.’s real cost of hedging Australian dollar payables every 90 days

have been positive, negative, or about zero on average over a period in which the Australian dollar

strengthened consistently? What does this imply about the forward rate as an unbiased predictor of

the future spot rate? Explain.

21. Implications of IRP for Hedging. If interest rate parity exists, would a forward hedge be more

favorable than, the same as, or less favorable than a money market hedge on euro payables? Explain.

22. Real Cost of Hedging. Would Montana Co.’s real cost of hedging Japanese yen payables have been

positive, negative, or about zero on average over a period in which the yen weakened consistently?

Explain.

23. Forward versus Options Hedge on Payables. Suppose your firm is a U.S. importer of Mexican goods

and you believe that today’s forward rate of the peso is a very accurate estimate of the future spot rate.

Do you think Mexican peso call options would be a more appropriate hedge than the forward hedge?

Explain.

24. Forward versus Options Hedge on Receivables. Your firm exports of goods to the United

Kingdom, and you believe that today’s forward rate of the British pound substantially underestimates

the future spot rate. Company policy requires you to hedge your British pound receivables in some

way. Would a forward hedge or a put option hedge be more appropriate? Explain.

25. Forward Hedging. Explain how a Malaysian firm can use the forward market to hedge periodic

purchases of U.S. goods denominated in U.S. dollars. Explain how a French firm can use forward

contracts to hedge periodic sales to United States importers that are invoiced in dollars. Explain how a

British firm can use the forward market to hedge periodic purchases of Japanese goods denominated

in yen.

Managing Transaction Exposure ❖ 9

ANSWER: A Malaysian firm can purchase dollars forward with ringgit, which locks in the exchange

rate at which it trades its ringgit for dollars.

26. Continuous Hedging. Cornell Co. purchases computer chips denominated in euros on a monthly

basis from a Dutch supplier. To hedge its exchange rate risk, this U.S. firm negotiates a three-month

forward contract three months before the next order will arrive. In other words, Cornell is always

covered for the next three monthly shipments. Because Cornell consistently hedges in this manner, it

is not concerned with exchange rate movements. Is Cornell insulated from exchange rate

movements? Explain.

27. Hedging Payables with Currency Options. Malibu, Inc., is a U.S. company that imports British

goods. It plans to use call options to hedge payables of 100,000 pounds in 90 days. Three call

options are available that have an expiration date 90 days from now. Fill in the number of dollars

needed to pay for the payables (including the option premium paid) for each option available under

each possible scenario.

Spot Rate

of Pound Exercise Price Exercise Price Exercise Price

90 Days = $1.74; = $1.76; = $1.79;

Scenario from Now Premium = $.06 Premium = $.05 Premium = $.03

1 $1.65

2 1.70

If each of the five scenarios had an equal probability of occurrence, which option would you choose?

Explain.

ANSWER:

Spot Rate

of Pound Exercise Price Exercise Price Exercise Price

90 Days = $1.74; = $1.76; = $1.79;

Scenario from Now Premium = $.06 Premium = $.05 Premium = $.03

1 $1.65 $171,000 $170,000 $168,000

3 1.75 180,000 180,000 178,000

28. Forward Hedging. Wedco Technology of New Jersey exports plastics products to Europe. Wedco

decided to price its exports in dollars. Telematics International, Inc. (of Florida), exports computer

network systems to the United Kingdom (denominated in British pounds) and other countries.

Telematics decided to use hedging techniques such as forward contracts to hedge its exposure.

a. Does Wedco’s strategy of pricing its materials for European customers in dollars avoid economic

exposure? Explain.

b. Explain why the earnings of Telematics were affected by changes in the value of the pound. Why

might this firm leave its exposure unhedged sometimes?

ANSWER: Telematics International, Inc. has sales to European customers, which are denominated in

29. The Long-term Hedge Dilemma. St. Louis Inc., which relies on exporting, denominates its exports in

pesos and receives pesos every month. It expects the peso to weaken over time. St. Louis recognizes the

limitation of monthly hedging. It also recognizes that it could eliminate its transaction exposure by

denominating the exports in dollars but that it is still would be subject to economic exposure. The long-

term hedging techniques have limitations as the firm does not know how many pesos it will receive in

the future, so it would have difficulty even if a long-term hedging method was available. How can this

business realistically deal with this dilemma to reduce its exposure over the long-term?

30. Long-term Hedging. Since Obisbo Inc. conducts much business in Japan, it is likely to have cash

flows in yen that will periodically be remitted by its Japanese subsidiary to the U.S. parent. What are

the limitations of hedging these remittances one year in advance over each of the next 20 years?

What are the limitations of creating a hedge today that will hedge these remittances over each of the

next 20 years?

ANSWER: If Obisbo Inc. hedges one year in advance, the forward rate negotiated at the beginning of each

year will be based on the spot rate of the yen (and the difference between the Japanese interest rate and

31. Hedging during a Crisis. Describe how a crisis in Asia could reduce the cash flows of a U.S. firm

that exports products (denominated in U.S. dollars) to Asian countries. How could a U.S. firm that

exports products (denominated in U.S. dollars) to Asia insulate itself from any currency effects of a

future crisis while continuing to export to Asia?

ANSWER: The weakness of the Asian currencies would cause the Asian importers to reduce their

Advanced Questions

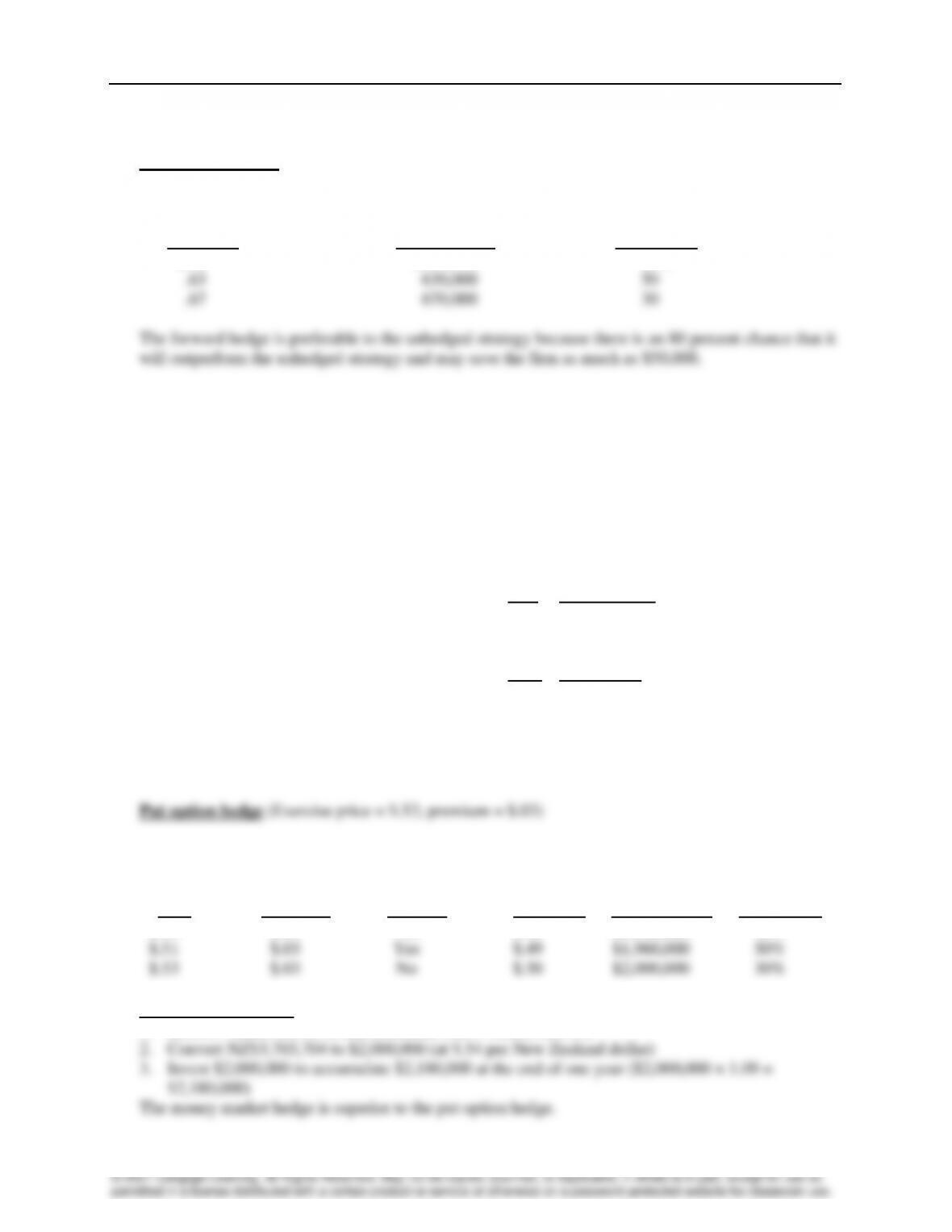

32. Comparison of Techniques for Hedging Receivables.

a. Assume that Carbondale Co. expects to receive S$500,000 in one year. The existing spot rate of

the Singapore dollar is $.60. The one-year forward rate of the Singapore dollar is $.62.

Carbondale created the following probability distribution for the future spot rate in one year:

Future Spot Rate Probability

$.61 20%

.63 50

.67 30

Assume that one-year put options on Singapore dollars are available, with an exercise price of

$.63 and a premium of $.04 per unit. One-year call options on Singapore dollars are available

with an exercise price of $.60 and a premium of $.03 per unit. Assume the following money

market rates:

U.S. Singapore

Deposit rate 8% 5%

Borrowing rate 9 6

Given this information, determine whether a forward hedge, money market hedge, or a currency

options hedge would be most appropriate. Then compare the most appropriate hedge to an

unhedged strategy and decide whether Carbondale should hedge its receivables position.

ANSWER:

Forward hedge

Money market hedge

Managing Transaction Exposure ❖ 12

© 2021 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Put option hedge (Exercise price = $.63; premium = $.04)

Possible Spot

Rate

Option

Premium per

Unit

Exercise

Amount

Received per

Unit (also

accounting

for premium)

Total Amount

Received for

S$500,000

Probability

$.61

$.04

Yes

$.59

$295,000

20%

$.63

$.04

Yes or No

$.59

$295,000

50%

$.67

$.04

No

$.63

$315,000

30%

The forward hedge is superior to the money market hedge and has a 70% chance of outperforming the

put option hedge. Therefore, the forward hedge is the optimal hedge.

Unhedged Strategy

Possible Spot Rate

Total Amount Received for

S$500,000

Probability

$.61

$305,000

20%

$.63

$315,000

50%

$.67

$335,000

30%

b. Assume that Baton Rouge, Inc. expects to need S$1 million in one year. Using any relevant

information in part (a) of this question, determine whether a forward hedge, a money market

hedge, or a currency options hedge would be most appropriate. Then, compare the most

appropriate hedge to an unhedged strategy, and decide whether Baton Rouge should hedge its

payables position.

ANSWER:

Forward hedge

Money market hedge

1. Need to invest S$952,381 (S$1,000,000/1.05 = S$952,381)

Amount Paid Total

Option per Unit Amount

Possible Premium Exercise (including Paid for

Spot Rate per Unit Option? the premium) S$1,000,000 Probability

Managing Transaction Exposure ❖ 13

The optimal hedge is the forward hedge.

Unhedged Strategy

Total

Possible Amount Paid

Spot Rate for S$500,000 Probability

$.61 $610,000 20%

33. Techniques for Hedging Receivables. SMU Corp. has future receivables of 4,000,000 New Zealand

dollars (NZ$) in one year. It must decide whether to use options or a money market hedge to hedge

this position. Use any of the following information to make the decision. Verify your answer by

determining the estimate (or probability distribution) of dollar revenue to be received in one year for

each type of hedge.

Spot rate of NZ$ = $.54

One-year call option: Exercise price = $.50; premium = $.07

One-year put option: Exercise price = $.52; premium = $.03

U.S. New Zealand

One-year deposit rate 9% 6%

One-year borrowing rate 11 8

Rate Probability

Forecasted spot rate of NZ$ $.50 20%

.51 50

.53 30

ANSWER:

Possible Spot

Rate

Put Option

Premium

Exercise

Option?

Amount per

Unit Received

Accounting

for Premium

Total Amount

Received

for

NZ$4,000,000

Probability

$.50

$.03

Yes

$.49

$1,960,000

20%

$.51

$.03

Yes

$.49

$1,960,000

50%

$.53

$.03

No

$.50

$2,000,000

30%

Money market hedge

1. Borrow NZ$3,703,704 (NZ$4,000,000/1.08 = NZ$3,703,704)

34. Exposure to September 11. If you were a U.S. importer of products from Europe, explain

whether the September 11, 2001 terrorist attack on the U.S. would have caused you to hedge your

payables (denominated in euros) due a few months later. Keep in mind that the attack was followed

by a reduction in U.S. interest rates.

ANSWER: The attack would have caused expectations of weak U.S. stock prices and lowered U.S.

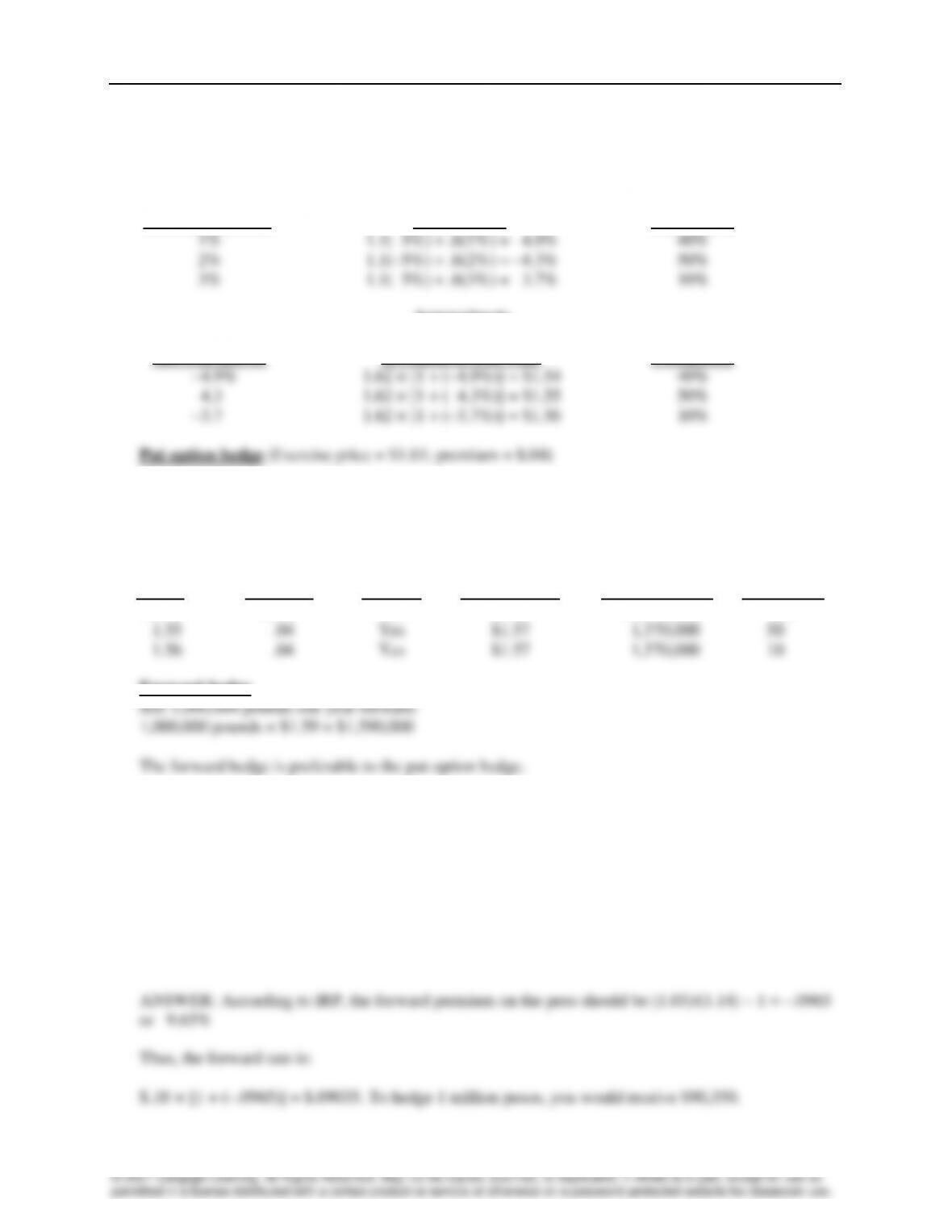

35. Hedging with Forward versus Option Contracts. As treasurer of Tempe Corp., you are confronted

with the following problem. Assume the one-year forward rate of the British pound is $1.59. You

plan to receive 1 million pounds in one year. A one-year put option is available; it has an exercise

price of $1.61. The spot rate as of today is $1.62, and the option premium is $.04 per unit. Your

forecast of the percentage change in the spot rate was determined from the following regression

model:

et = a0 + a1DINFt-1 + a2DINTt + u

where et = percentage change in the value of the British pound over period t

DINFt-1 = differential in inflation between the United States and the United

Kingdom in period t–1

DINTt = average differential between the U.S. interest rate and the British

interest rate over period t

a0, a1, and a2 = regression coefficients

u = error term

The regression model was applied to historical annual data, and the regression coefficients were

estimated as follows:

a0 = 0.0

a1 = 1.1

a2 = 0.6

Assume last year’s inflation rates were 3 percent for the United States and 8 percent for the United

Kingdom. Also assume that the interest rate differential (DINTt) is forecasted as follows for this

year:

Forecast of DINTt Probability

1% 40%

2 50

3 10

Managing Transaction Exposure ❖ 15

Using any of the available information, should you as treasurer choose the forward hedge or the put

option hedge? Show your work.

ANSWER:

Forecast of DINTt Forecast of et Probability

Approximate

Forecast of et Forecasted Spot Rate

(derived above) of Pound in One Year Probability

Possible

Spot Rate of Amount

Pound in Received

One Year Put per Unit Total Amount

(derived Option Exercise (accounting Received for One

above) Premium Option? for premium) Million Pounds Probability

$1.54 $.04 Yes $1.57 $1,570,000 40%

Forward hedge

36. Hedging Decision. You believe that IRP presently exists, whereas the nominal annual interest rate in

Mexico is 14%. The nominal annual interest rate in the U.S. is 3%. You expect that annual inflation

will be about 4% in Mexico and 5% in the U.S. The spot rate of the Mexican peso is $.10. Put options

on pesos are available with a one-year expiration date, an exercise price of $.1008, and a premium of

$0.014 per unit.

You will receive 1 million pesos in one year.

a. Determine the amount of dollars that you will receive if you use a forward hedge.

Managing Transaction Exposure ❖ 16

b. Determine the expected amount of dollars that you will receive if you do not hedge and believe in

purchasing power parity (PPP).

ANSWER: The expected percentage change in the Mexican peso according to PPP is:

c. Determine the amount of dollars that you will expect to receive if you use a currency put option

hedge. Account for the premium you would pay on the put option.

ANSWER: Since the expected spot rate is $.10096 based on PPP, you could receive $.10096 per unit

37. Forecasting with IFE and Hedging. Assume that Calumet Co. will receive 10 million pesos in

15 months. It does not have a relationship with a bank at this time, and therefore can not obtain a

forward contract to hedge its receivables at this time. However, in three months, it will be able to

obtain a one-year (12-month) forward contract to hedge its receivables. Today the three-month U.S.

interest rate is 2% (not annualized), the 12-month U.S. interest rate is 8%, the three-month Mexican

peso interest rate is 5% (not annualized), and the 12-month peso interest rate is 20%. Assume that

interest rate parity exists.

Assume the international Fisher effect exists, and the existing interest rates are expected to

remain constant over time. The spot rate of the Mexican peso today is $.10. Based on this

information, estimate the amount of dollars that Calumet Co. will receive in 15 months.

ANSWER:

38. Forecasting from Regression Analysis and Hedging. You apply a regression model to annual data

in which the annual percentage change in the British pound is the dependent variable, and INF

(defined as annual U.S. inflation minus U.K. inflation) is the independent variable. A regression

analysis produces an estimate of 0.0 for the intercept and +1.4 for the slope coefficient. You believe

that your model will be useful to predict exchange rate movements in the future.

You expect that inflation in the U.S. will be 3%, versus 5% in the U.K. There is an 80% chance of

that scenario becoming reality. However, you think that oil prices could rise, and if so, the annual

U.S. inflation rate will be 8% instead of 3% (and the annual U.K. inflation will still be 5%). There is a

20% chance that this scenario will occur. You think that the inflation differential is the only variable

that will affect the British pound’s exchange rate over the next year.

Managing Transaction Exposure ❖ 17

The spot rate of the pound as of today is $1.80. The annual interest rate in the U.S. is 6% versus an

annual interest rate in the U.K. of 8%. Call options are available with an exercise price of $1.79, an

expiration date of one year from today, and a premium of $.03 per unit.

Your firm in the U.S. expects to need 1 million pounds in one year to pay for imports. You can use

any one of the following strategies to deal with the exchange rate risk:

a. unhedged strategy

b. money market hedge

c. call option hedge

Estimate the dollar cash flows you will need as a result of using each strategy. If the estimate for a

particular strategy involves a probability distribution, show the distribution. Which hedge is optimal?

ANSWER:

The results of the regression analysis and the forecasts of the future inflation rates can be used to

Unhedged strategy:

Possible spot

rate in one year

Probability

Cost of payables

$1.7496

80.00%

$1,496,600

$1.8756

20.00%

$1,875,600

Money market hedge:

To receive £1,000,000 at the end of the year, invest £935,926 now:

Call option hedge

Managing Transaction Exposure ❖ 18

Possible spot rate

in one year

Probability

Cost of hedging

£1,000,000 (including

the option premium)

1.7496

80.00%

$1,779,600

1.8756

20.00%

$1,820,000

39. Forecasting Cash Flows and Hedging Decision. Virginia Co. has subsidiaries in both Hong Kong

and Thailand. Assume that the Hong Kong dollar is pegged at $.13 per Hong Kong dollar and it will

remain pegged. The Thai baht fluctuates against the dollar and is presently worth $.03. The firm

expects that during this year, the U.S. inflation rate will be 2%, the Thailand inflation rate will be

11%, while the Hong Kong inflation rate will be 3%. Virginia Co. expects that purchasing power

parity will hold for any exchange rate that is not fixed (pegged). The parent of Virginia Co. will

receive 10 million Thai baht and 10 million Hong Kong dollars at the end of one year from its

subsidiaries.

a. Determine the expected amount of dollars to be received by the U.S. parent from the Thai

subsidiary in one year when the baht receivables are converted to U.S. dollars.

b. The Hong Kong subsidiary will send HK$1 million to make a payment for supplies to the Thai

subsidiary. Determine the expected amount of baht that will be received by the Thai subsidiary

when the Hong Kong dollar receivables are converted to Thai baht.

c. Assume that interest rate parity exists. Also assume that the real one-year interest rate in the U.S.

is 1.0%, whereas the real interest rate in Thailand is 3.0%. Determine the expected amount of

dollars to be received by the U.S. parent if it uses a one-year forward contract today to hedge the

receivables of 10 million baht that will arrive in one year.

ANSWER:

40. Hedging Decision. Indiana Company expects to receive 5 million euros in one year from exports.

It can use any one of the following strategies to deal with the exchange rate risk. Estimate the dollar

cash flows received as a result of using the following strategies:

a. unhedged strategy

b. money market hedge

c. option hedge