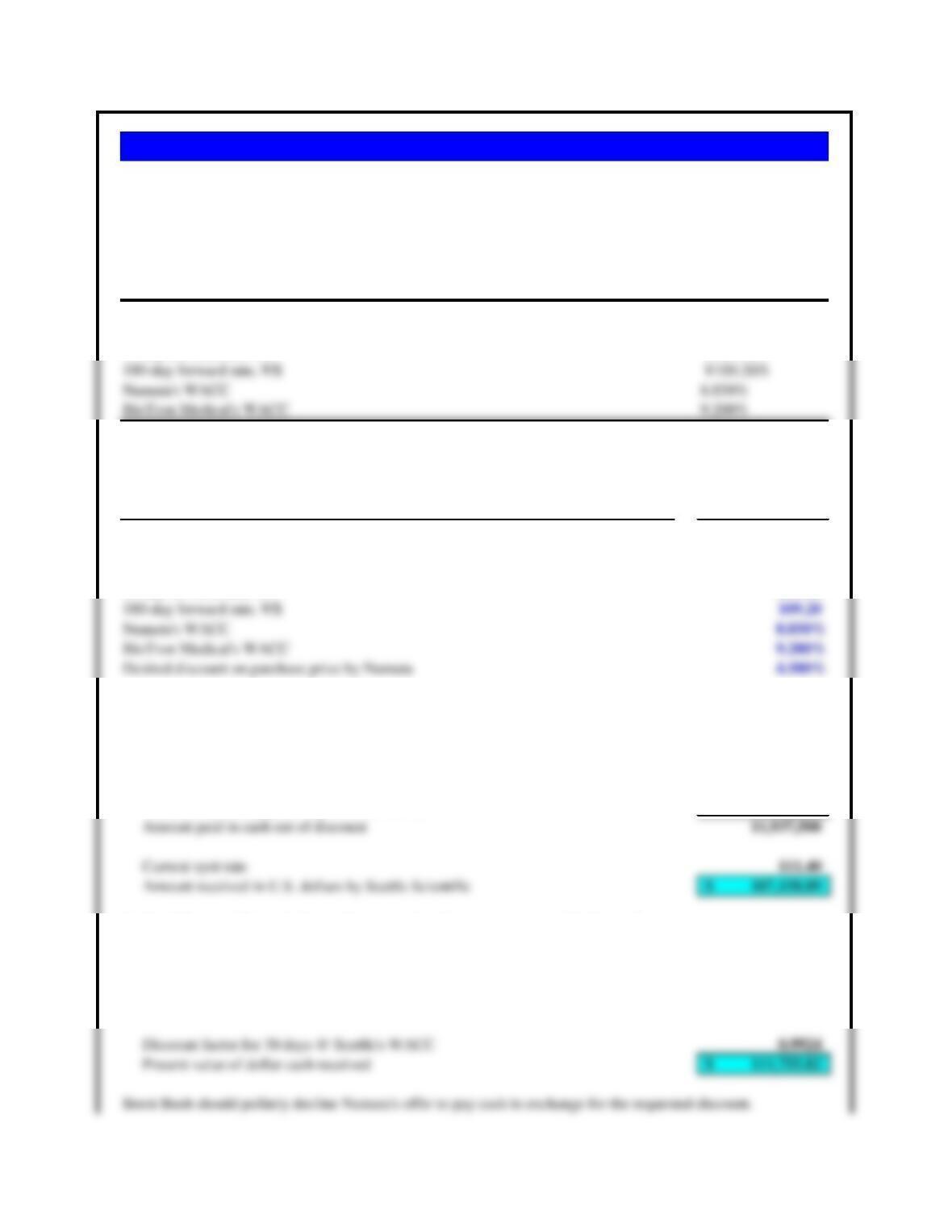

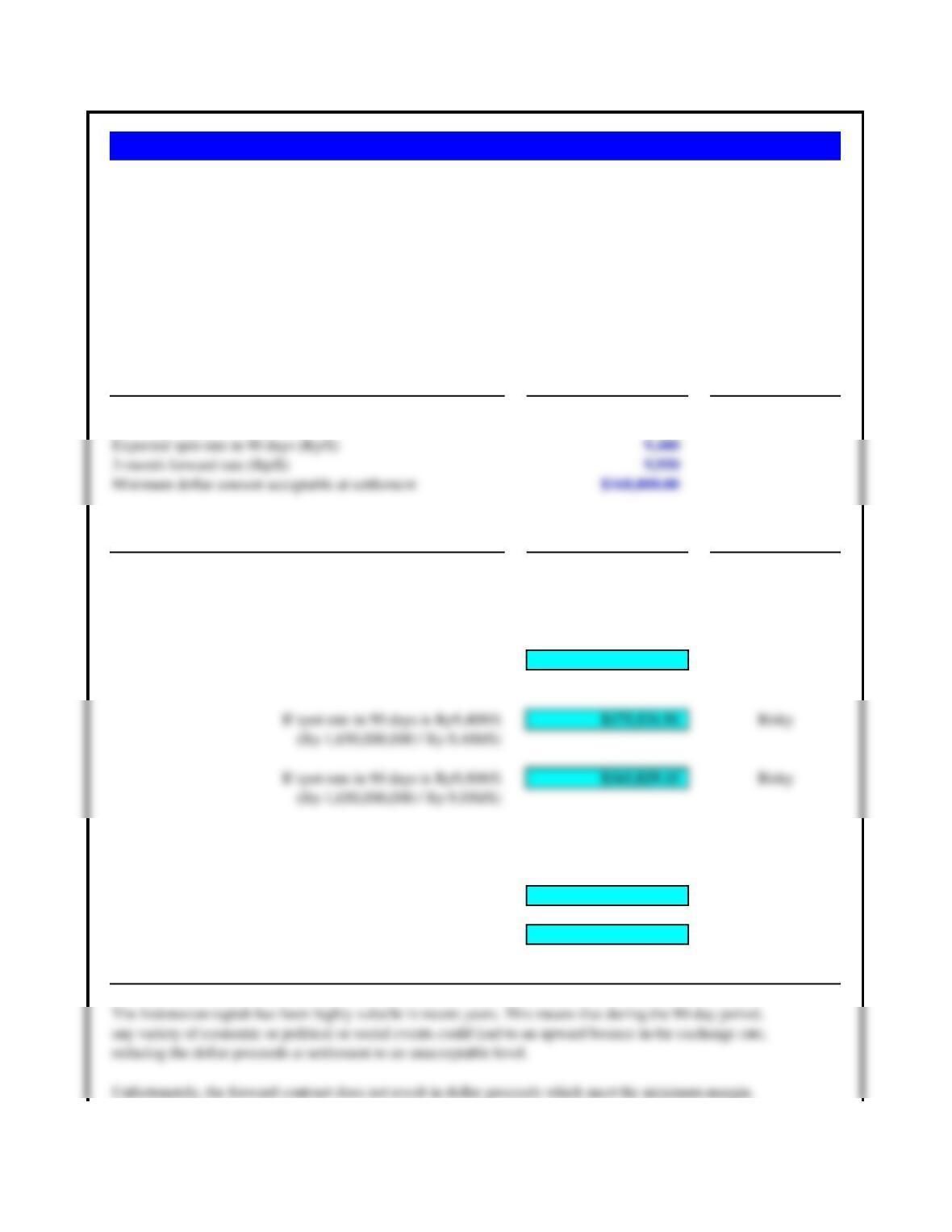

Spot rate, ¥/$ ¥111.40/$

30-day forward rate, ¥/$ ¥111.00/$

90-day forward rate, ¥/$ ¥110.40/$

180-day forward rate, ¥/$ ¥109.20/$

Assumptions Values

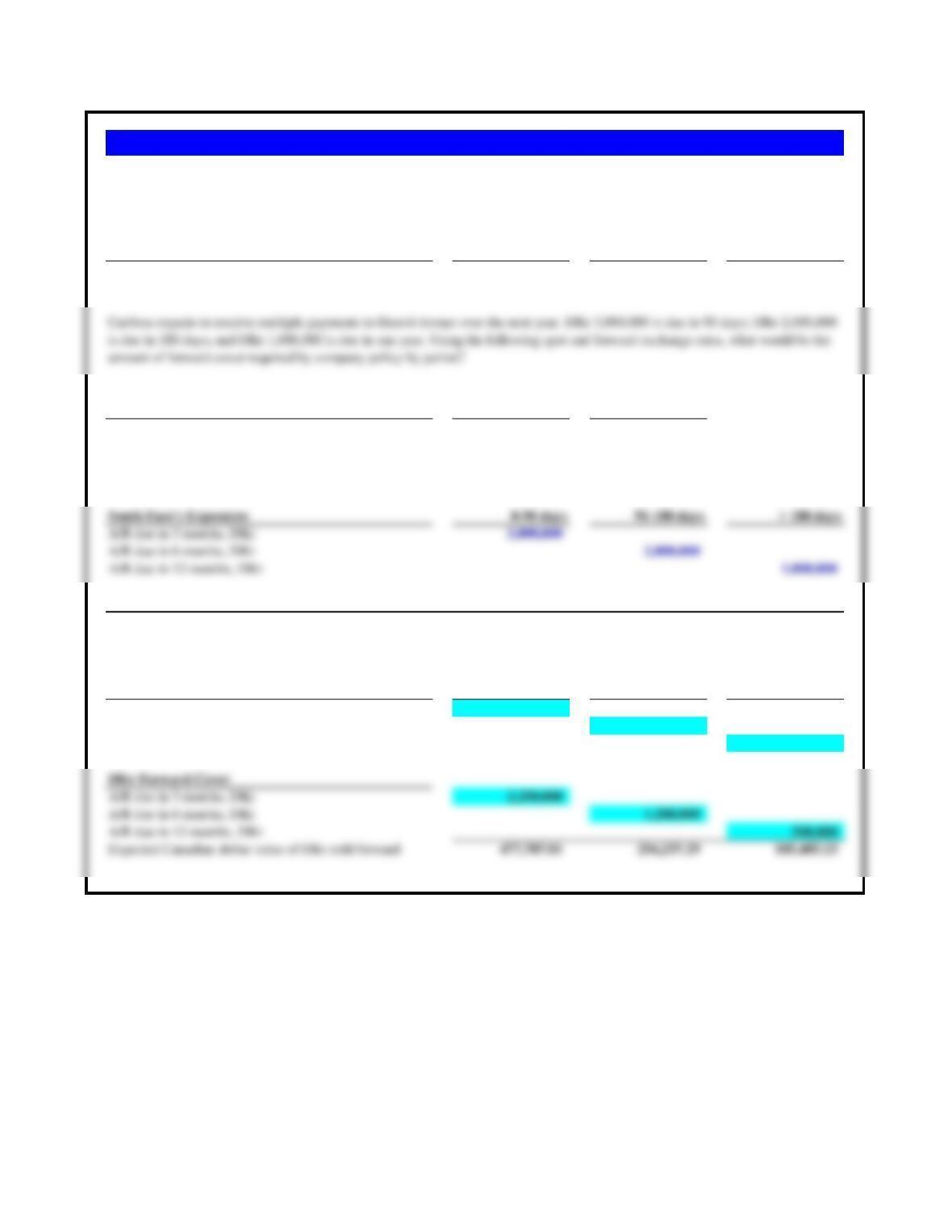

BioTron’s 30-day account receivable, Japanese yen 12,500,000

Spot rate, ¥/$ 111.40

30-day forward rate, ¥/$ 111.00

90-day forward rate, ¥/$ 110.40

180-day forward rate, ¥/$ 109.20

Brent Bush should compare two basic alternatives, both of which eliminate the currency risk.

1. Allow the discount and receive payment in Japanese yen in cash

Account recievable (yen) 12,500,000

Discount for cash payment up-front (4.500%) (562,500)

2. Not offer any discounts for early payment and cover exposure with forwards

Account receivable (yen) 12,500,000

30-day forward rate 111.00

Amount received in cash in dollars, in 30 days 112,612.61$

Problem 10.1 BioTron Medical, Inc.

How much in U.S. dollars will BioTron Medical receive 1) with the discount and 2) with no discount but fully

covered with a forward contract?

Brent Bush, CFO of a medical device manufacturer, BioTron Medical, Inc., was approached by a Japanese

customer, Numata, with a proposal to pay cash (in yen) for its typical orders of ¥12,500,000 every other month if

it were given a 4.5% discount. Numata’s current terms are 30 days with no discounts. Using the following quotes

and estimated cost of capital for Numata, Bush will compare the proposal with covering yen payments with

forward contracts.

Assumptions Values

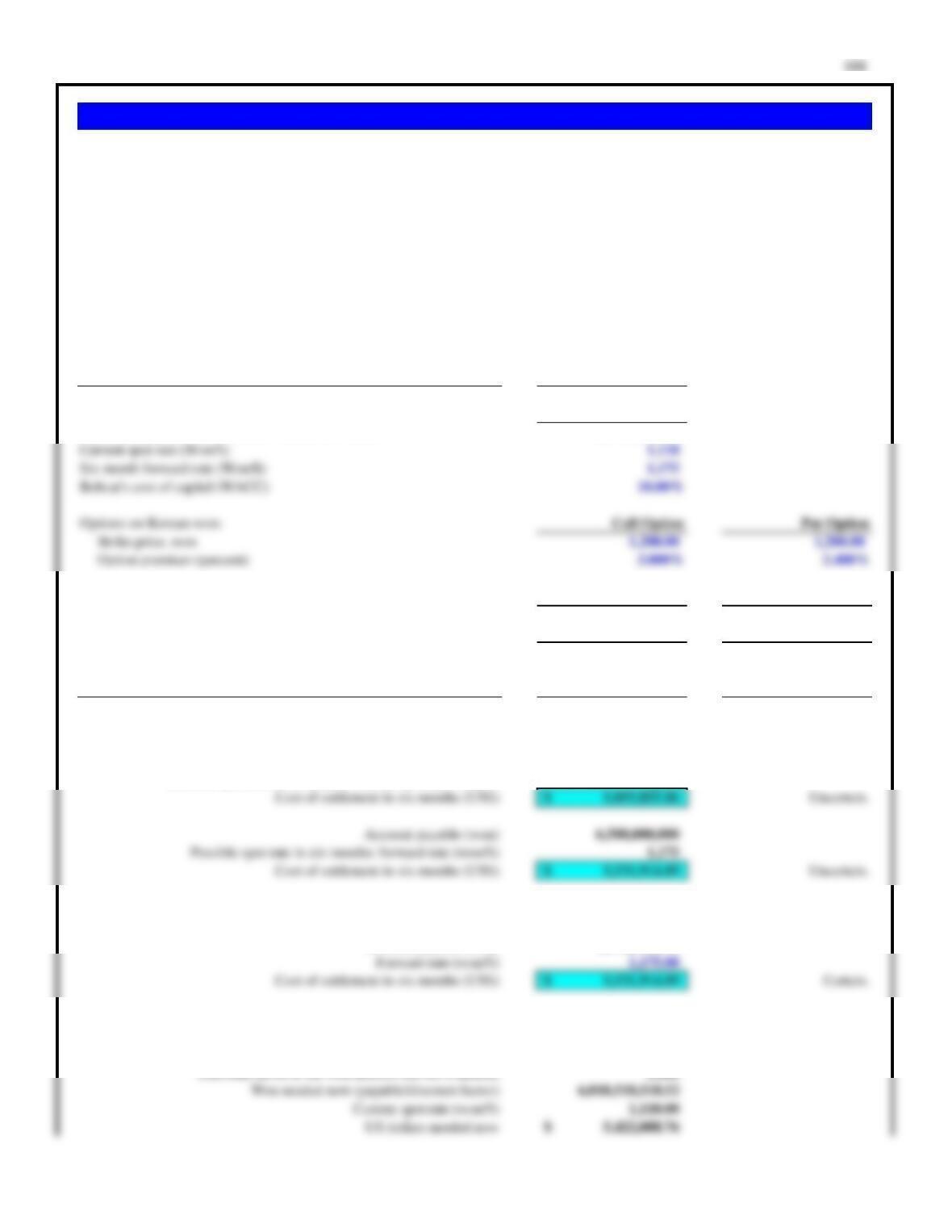

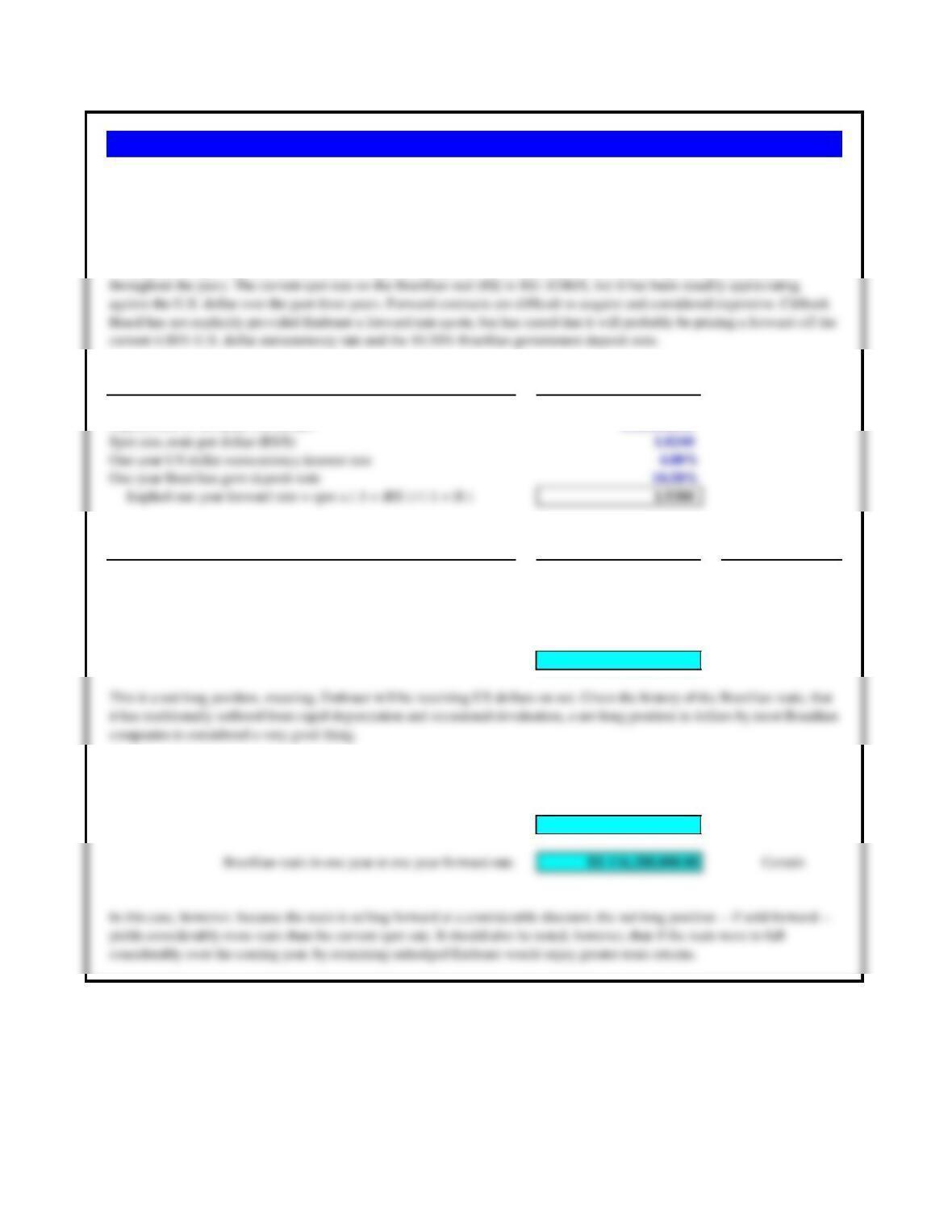

Purchase price of Korean manufacturer, in Korean won 7,500,000,000

Less initial payment, in Korean won (1,000,000,000)

Net settlement needed, in Korean won, in six months 6,500,000,000

United States Korea

Six-month investment (not borrowing) interest rate (per annum) 4.000% 16.000%

Borrowing premium of 2.000% 2.000% 2.000%

Six-month borrowing rate (per annum) 6.000% 18.000%

Risk Management Alternatives Values Certainty

1. Remain uncovered, making the won payment in 6 months

at the spot rate in effect at that date

Account payable (won) 6,500,000,000

Possible spot rate in six months: current spot rate (won/$) 1,110

2. Forward market hedge. Buy won forward six months

Account payable (won) 6,500,000,000

3. Money market hedge. Exchange dollars for won now, invest for six months.

Account payable (won) 6,500,000,000

Problem 10.2 Bobcat Company

Bobcat can invest at the rates given above, or borrow at 2% per annum above those rates. Bobcat’s weighted average cost of capital is

10%. Compare alternate ways that Bobcat might deal with its foreign exchange exposure. What do you recommend and why?

Bobcat Company, U.S.-based manufacturer of industrial equipment, just purchased a Korean company that produces plastic nuts and

bolts for heavy equipment. The purchase price was Won7,500 million. Won1,000 million has already been paid, and the remaining

Won6,500 million is due in six months. The current spot rate is Won1,110/$, and the 6-month forward rate is Won1,175/$. The six-

month Korean won interest rate is 16% pe annum, the six-month US dollar rate is 4% per annum. Bobcat can invest at these interest

rates, or borrow at 2% per annum above those rates. A six-month call option on won with a 1200/$ strike rate has a 3.0% premium, while

the six-month put option at the same strike rate has a 2.4% premium.

4. Call option hedge. (Need to buy won = call on won)

If exercised If not exercised

Option principal 6,500,000,000

Current spot rate (won/$) 1,110.00 1,300.00

Premium cost of option (%) 3.000%

Option premium (principal/spot rate x % pm) 175,675.68$

Assumptions Value

US dollar debt taken out in June 1997 50,000,000$

US dollar borrowing rate on debt 8.400%

Calculation of Foreign Exhange Loss on Repayment of Loan

At the time the loan was acquired, the scheduled repayment of dollar

and baht amounts would have been as follows:

Scheduled Repayment:

Repayment of US dollar debt: Principal 50,000,000$

Repayment of US dollar debt: Interest 4,200,000

Total repayment 54,200,000$

Net interest to be paid, in Thai baht 105,000,000

Actual Repayment:

Repayment of US dollar debt: Principal 50,000,000$

Repayment of US dollar debt: Interest 4,200,000

Total repayment 54,200,000$

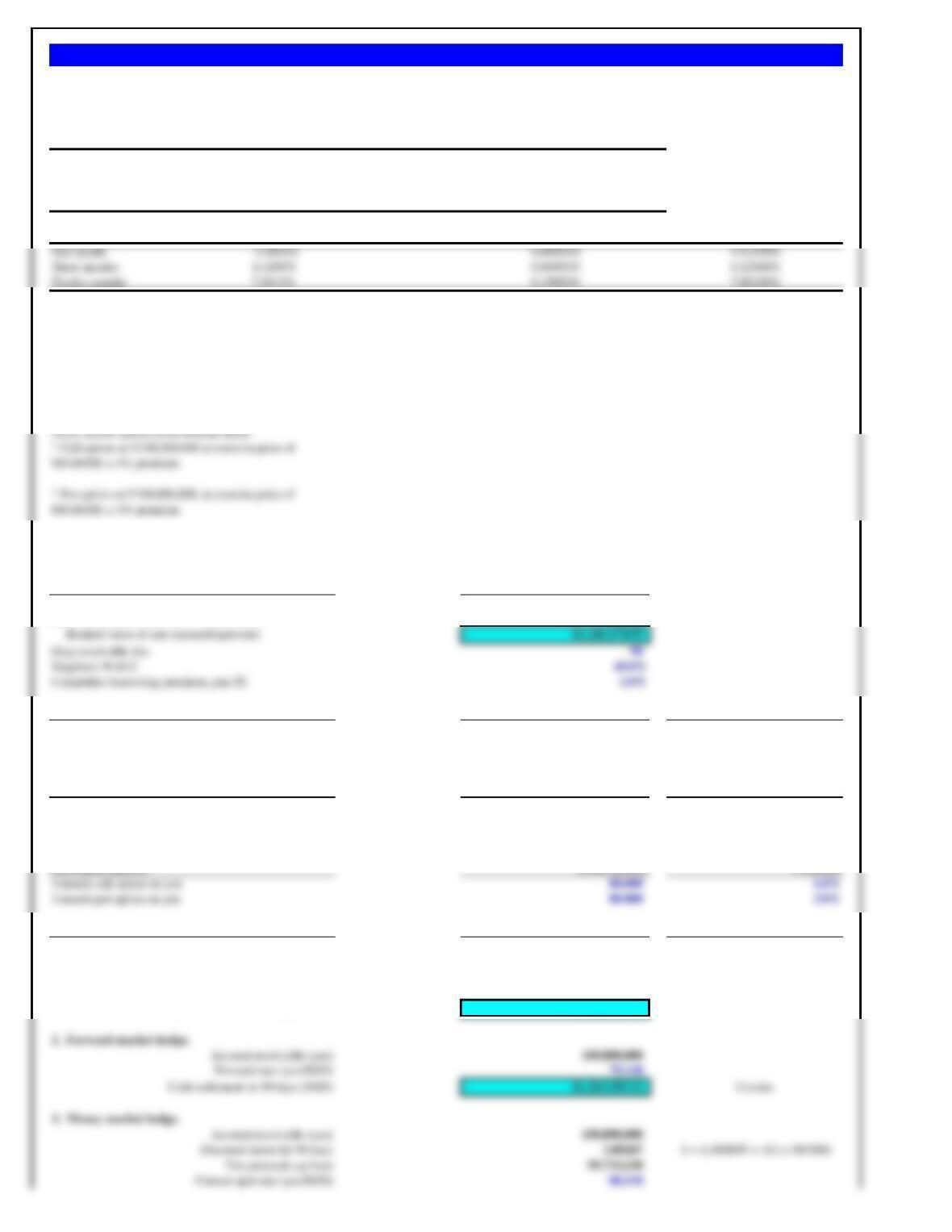

Siam Cement, the Bangkok-based cement manufacturer, suffered enormous losses with the coming of the

Asian crisis in 1997. The company had been pursuing a very aggressive growth strategy in the mid-1990s,

taking on massive quantities of foreign currency denominated debt (primarily U.S. dollars). When the Thai

baht (B)was devalued from its pegged rate of B25.0/$ in July 1997, Siam’s interest payments alone were

Problem 10.3 Siam Cement

Assumptions Values

180-day account payable, Japanese yen (¥) 8,500,000

Spot rate (¥/$) 120.60

Spot rate, rupees/dollar (Rs/$) 47.75

Implied (calculated) spot rate (¥/Rs) 2.5257 (120.60 / 47.75)

Spot Risk

Hedging Alternatives Values Rate (Rp/$) Assessment

1. Remain Uncovered, settling A/P in 180 days at spot rate

If spot rate in 180 days is same as current spot 3,365,464.34 2.5257 Risky

2. Buy Japanese yen forward 180 days

Settlement amount at forward rate (Rs) 3,541,666.67 2.4000 Certain

3. Money Market Hedge

Principal A/P (¥) 8,500,000.00

discount factor for yen investing rate for 180 days 0.9926

Principal needed to meet A/P in 180 days (¥) 8,436,724.57

Current spot rate (¥/Rs) 2.5257

4. Indian Currency Agent Hedge

Principal A/P (¥) 8,500,000.00

Current spot rate (¥/Rs) 2.5257

Current A/P (Rs) 3,365,464.34

Evaluation of Alternatives

The currency agent is the lowest total cost, in CERTAIN future rupee value, of all certain alternatives.

Problem 10.4 P & G India

Proctor and Gamble’s affiliate in India, P & G India, procures much of its toiletries product line from a Japanese company. Because of the

shortage of working capital in India, payment terms by Indian importers are typically 180 days or longer. P & G India wishes to hedge a 8.5

million Japanese yen payable. Although options are not available on the Indian rupee (Rs), forward rates are available against the yen.

Additionally, a common practice in India is for companies like P & G India to work with a currency agent who will, in this case, lock in the

current spot exchange rate in exchange for a 4.85% fee. Using the following exchange rate and interest rate data, recommend a hedging

strategy.

Assumptions Values At Spot

Receivable due in 3 months, in Indonesian rupiah (Rp) Rp1,650,000,000 $174,603.17

Spot rate (Rp/$) 9,450

Risk

Alternatives Values Assessment

1. Remain Uncovered.

Settle A/R in 90 days at current spot rate.

If spot rate in 90 days is same as current $174,603.17 Risky

(Rp 1,650,000,000 / Rp 9,450/$)

2. Sell Indonesian rupiah forward.

A/R sold forward 90 days $165,829.15 Certain

“Cost of cover” is the forward discount on Rp -20.1%

Analysis

Problem 10.5 Elan Pharmaceuticals

Elan Pharmaceuticals, a U.S.-based multinational pharmaceutical company, is evaluating an export sale of its

cholesterol-reduction drug with a prospective Indonesian distributor. The purchase would be for 1,650 million

Indonesian rupiah (Rp), which at the current spot exchange rate of Rp9,450/$, translates into nearly $175,000.

Although not a big sale by company standards, company policy dictates that sales must be settled for at least a

minimum gross margin, in this case, a cash settlement of $168,000. The current 90-day forward rate is Rp9,950/$.

Although this rate appeared unattractive, Elan had to contact several major banks before even finding a forward

quote on the rupiah. The consensus of currency forecasters at the moment, however, is that the rupiah will hold

relatively steady, possibly falling to Rp9,400/$ over the coming 90 to 120 days. Analyze the prospective sale and

make a hedging recommendation.

The cost of forward cover, 20.1%, is indicative of the “artificial interest rates” used by some financial

institutions while pricing derivatives in emerging, illiquid, and volatile markets.

Assumptions Values

Receivable due in one year, US dollars $80,000,000

Risk

Analysis Values Assessment

Net exposure at time of cash settlements:

One year A/R due $80,000,000

One year A/P due ($20,000,000)

Net exposure $60,000,000 Certain

Cash settlement of the net position:

Brazilian reais in one year at current spot rate R$ 109,440,000.00 Risky

Problem 10.6 Embraer of Brazil

Embraer of Brazil is one of the two leading global manufacturers of regional jets (Bombardier of Canada is the other).

Regional jets are smaller than the traditional civilian airliners produced by Airbus and Boeing, seating between 50 and 100

people on average. Embraer has concluded an agreement with a regional U.S. airline to produce and deliver four aircraft one

year from now for $80 million. Although Embraer will be paid in U.S. dollars, it also possesses a currency exposure of inputs –

it must pay foreign suppliers $20 million for inputs one year from now (but they will be delivering the sub-components

Spot exchange rate: ¥80.310 ¥80.31/$ (closing mid-rates)

One-month forward rate: ¥79.960 5.25%

Three-month forward: ¥79.140 5.91%

One-year forward: ¥74.870 7.27%

Money Rates United States Japan Differential

a) What are the costs and benefits of alternative hedges? Which would you recommend, and why?

b) What is the break-even reinvestment rate when comparing forward and money market alternatives?

Assumptions Values

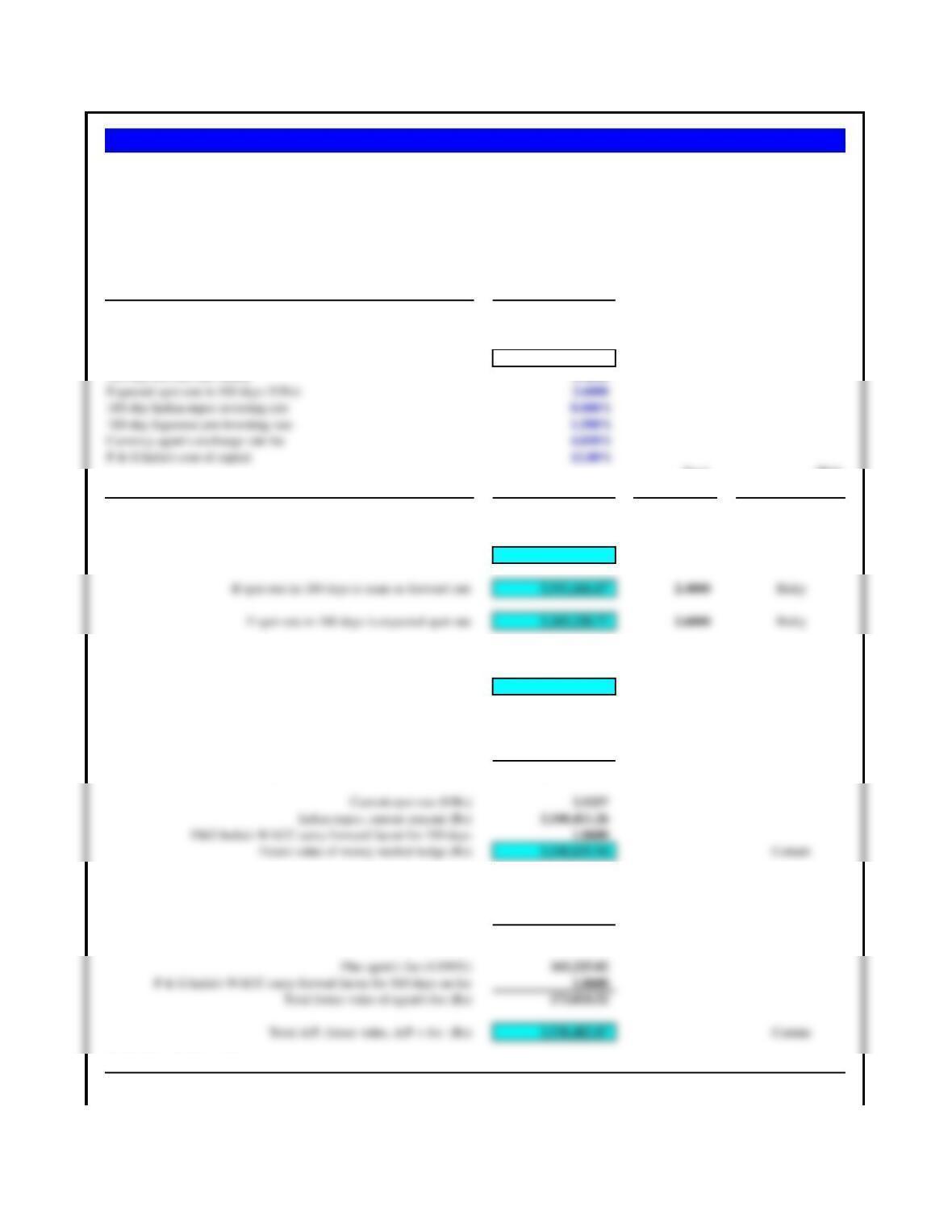

Amount of receivable, Japanese yen (¥)100,000,000

Spot exchange rate at time of sale (¥/SGD) 80.310

Competitor borrowing premium, yen (¥)1.0%

Forward rates and premiums Forward Rate Premium

One-month forward rate (¥/SGD) 79.960 5.25%

Three-month forward rate (¥/SGD) 79.140 5.91%

One-year forward rate (¥/SGD) 74.870 7.27%

Investment rates, % per annum Singapore Japan

1 month 5.9850% 0.06950%

3 months 6.1895% 0.06950%

12 months 7.9515% 0.15050%

a. Alternative Hedges Values Certainty

1. Remain uncovered.

Account receivable (yen) 100,000,000

Possible spot rate in 90 days (yen/SGD)

80.310

Cash settlement in 90 days (SGD)

$1,245,174.95 Uncertain.

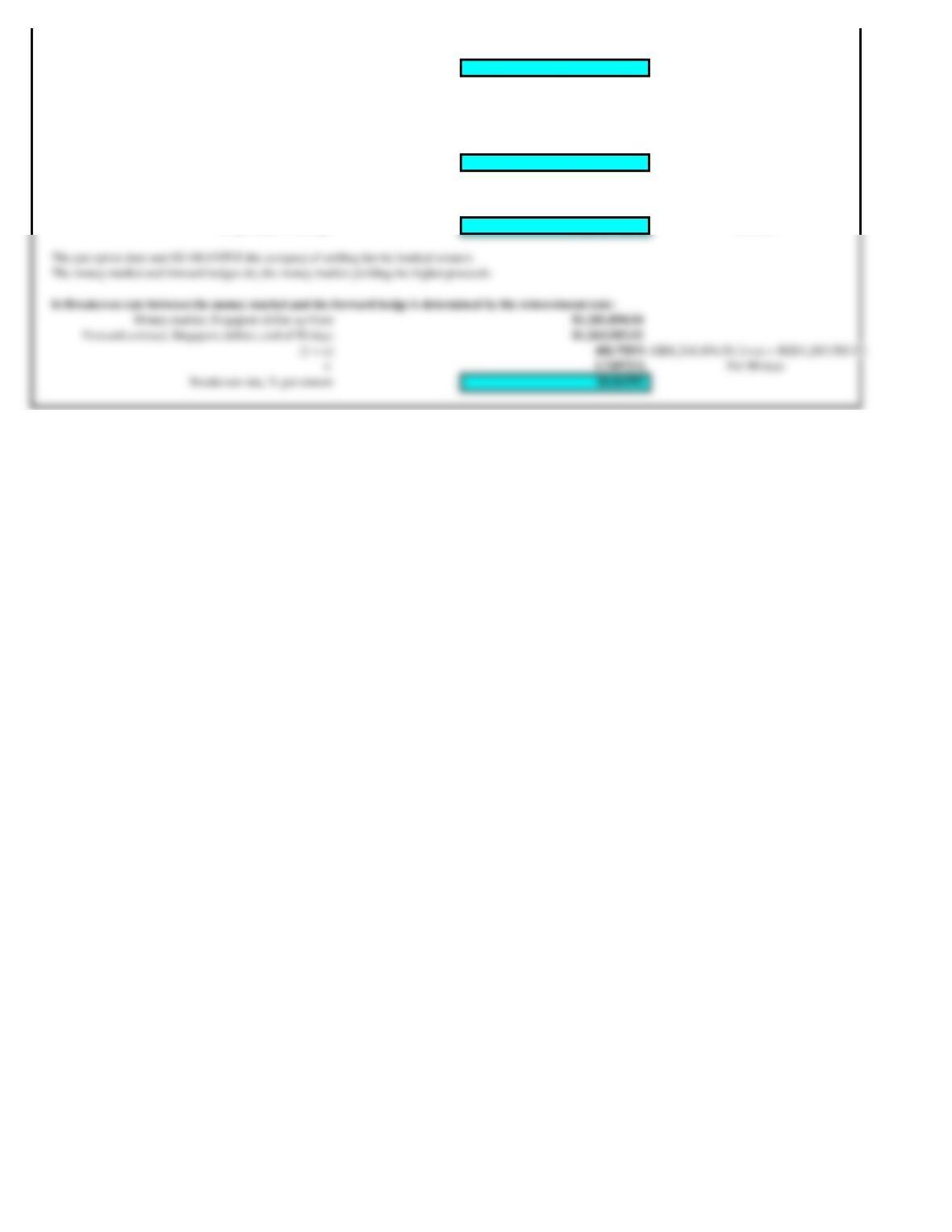

Problem 10.7 Singflux

Singflux is a Singapore-based company that manufactures, sells, and installs water-treatment plants. On June 1, the company sold a water-treatment plant to the

City of Hiroshima, Japan, for installation in Hiroshima’s famous cherry blossom gardens. The sale was priced in yen at ¥100,000,000, with payment due in three

months.

Singflux’s Japanese competitors are currently borrowing from Japanese banks at a spread of one percentage point above the Japanese money rate. Singflux’s

weighted average cost of capital is 10%, and the company wishes to protect the Singapore dollar value of this receivable.

Note: The interest rate differentials vary slightly from the forward discounts on the yen because of time differences for the quotes. The spot ¥80.31/S$, for

example, is a mid-point range. On June 1, the spot yen traded in London from ¥80.36/S$ to ¥79.86/S$.

Singapore dollars received now $1,241,854.54

Carry forward at Singflux’s WACC

1.0250 1 + (.10 x 90/360)

Proceeds in 90 days

$1,272,900.90 Certain.

4. Put option hedge. (Need to sell yen = put on yen)

Option principal 100,000,000

Current spot rate (yen/SGD) 80.310

Premium cost of option (%)

3.000%

Option pm (principal/spot rate x % pm)

$37,355.25

If option exercised, Singapore dollar proceeds $1,250,000.00

Less Pm carried forward 90 days

(38,289.130) 1.025 carry-forward rate

Net proceeds in 90 days

$1,211,710.87 Minimum.

Caribou River’s Manadatory Forward Cover 0-90 days 91-180 days > 180 days

Paying the points forward 75% 60% 50%

Receiving the points forward 100% 90% 50%

Forward

Assumptions Values Discount

Spot rate, DKr/C$ 4.70

3-month forward rate, DKr/C$ 4.71 -0.85%

6-month forward rate, DKr/C$ 4.72 -0.85%

12-month forward rate, DKr/C$ 4.74 -0.84%

Analysis & Exposure Management

The Danish krone is selling forward at a discount versus the Canadian dollar: it takes more DKr/C$ forward.

Caribou River is receiving foreign currency, DKr, at future dates (“long DKr”).

Caribou River is therefore expecting to PAY THE POINTS FORWARD.

Required Forward Cover for Compass Rose: 0-90 days 91-180 days > 180 days

A/R due in 3 months, DKr 75%

A/R due in 6 months, DKr 60%

A/R due in 12-months, DKr 50%

Problem 10.8 Caribou River

Caribou River, Ltd., a Canadian manufacturer of raincoats, does not selectively hedge its transaction exposure. Instead, if the date of

the transaction is known with certainty, all foreign currency-denominated cash flows must utilize the following mandatory forward

contract cover formula:

Caribou expects to receive multiple payments in Danish kroner over the next year. DKr 3,000,000 is due in 90 days; DKr 2,000,000

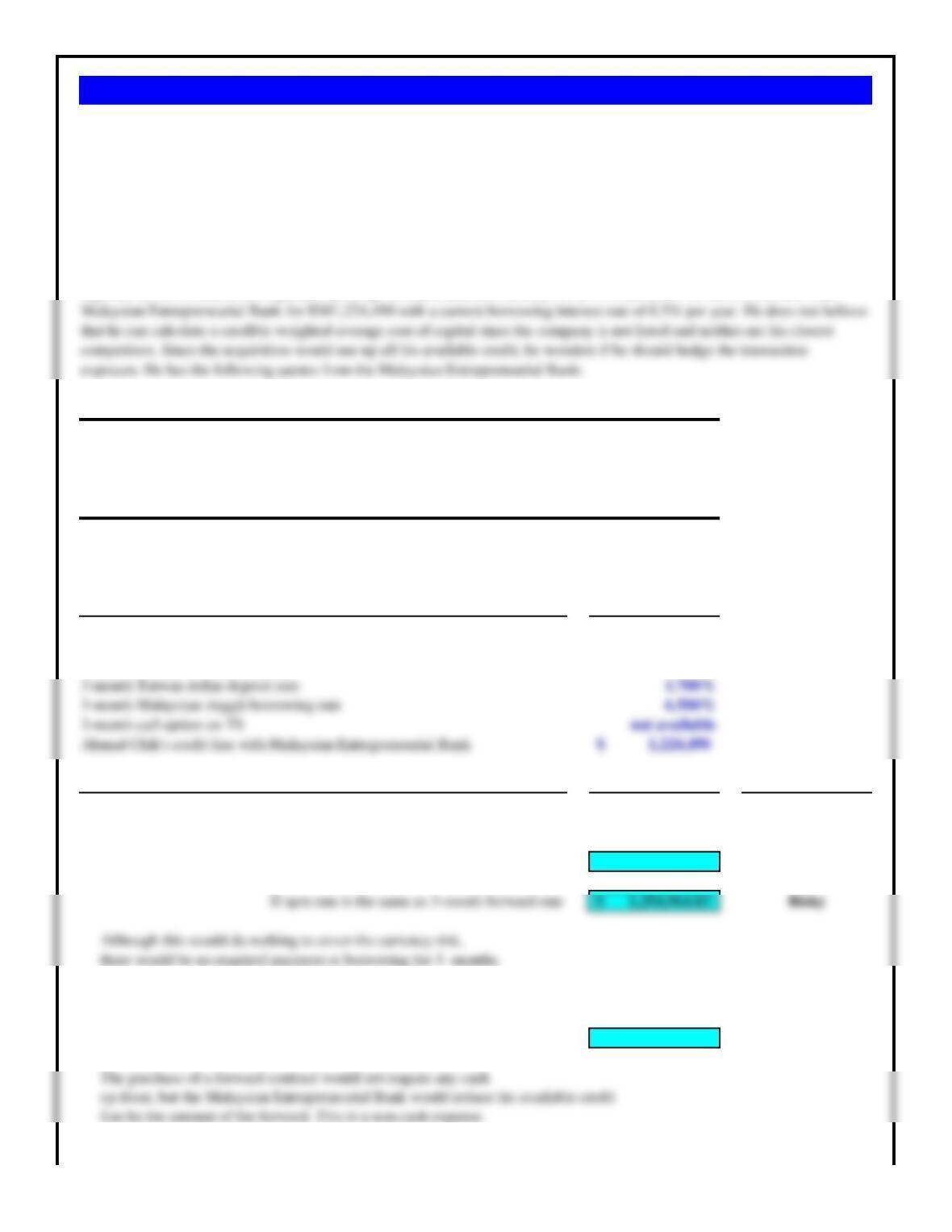

Spot rate (T$/RM) 7.35

3-month forward rate (T$/RM) 6.95

3-month Taiwan dollar deposit rate 1.700%

3-month Malaysian ringgit borrowing rate 6.500%

3-month call option on T$ not available

Assumptions Values

Acquisition price & 3-month A/P, NewTaiwan dollars (T$) 9,000,000

Spot rate (T$/MYR) 7.35

3-month forward rate (T$/MYR) 6.95

Evaluation of Alternatives Cost Certainty

1. Do Nothing — Wait 3 months and buy T$ spot

If spot rate is the same as current spot rate 1,224,489.80$ Risky

2. Buy T$ forward 3-months

Assured cost of T$ at 3-month forward rate 1,294,964.03$ Certain

3. Money Market Hedge: Exchanging Malaysian Ringgit for T$ now, depositing for 3-months until payment

Problem 10.9 Kraftangan Ornamentals

Kraftangan Ornamentals, a Malaysian, 100% privately-owned ornamentals company, has signed an agreement to acquire a

60% ownership share of Taiwan Ornamentals, a Taiwan-based, privately-owned ornamental company specializing in

customized figurines from Thailand and Indonesia. The acquisition price is 9 million Taiwan dollars (T$), payable in cash in

three months.

Ahmad Chik, the owner of Kraftangan Ornamentals, believes the Taiwan dollar will either remain stable or decline slightly

over the next three months. At the present spot rate of T$7.35/RM, the amount of cash required is only RM1,224,490, but

even this relatively modest amount will need to be borrowed personally by Ahmad Chik. The Taiwanese interest-bearing

Analyze the cost and risks of each alternative, and then make a recommendation as to which alternative Ahmad Chik should

choose.

Acquisition price in T$ needed in 3-months 9,000,000

Discounted back 3-months at T$ deposit rate 0.9958

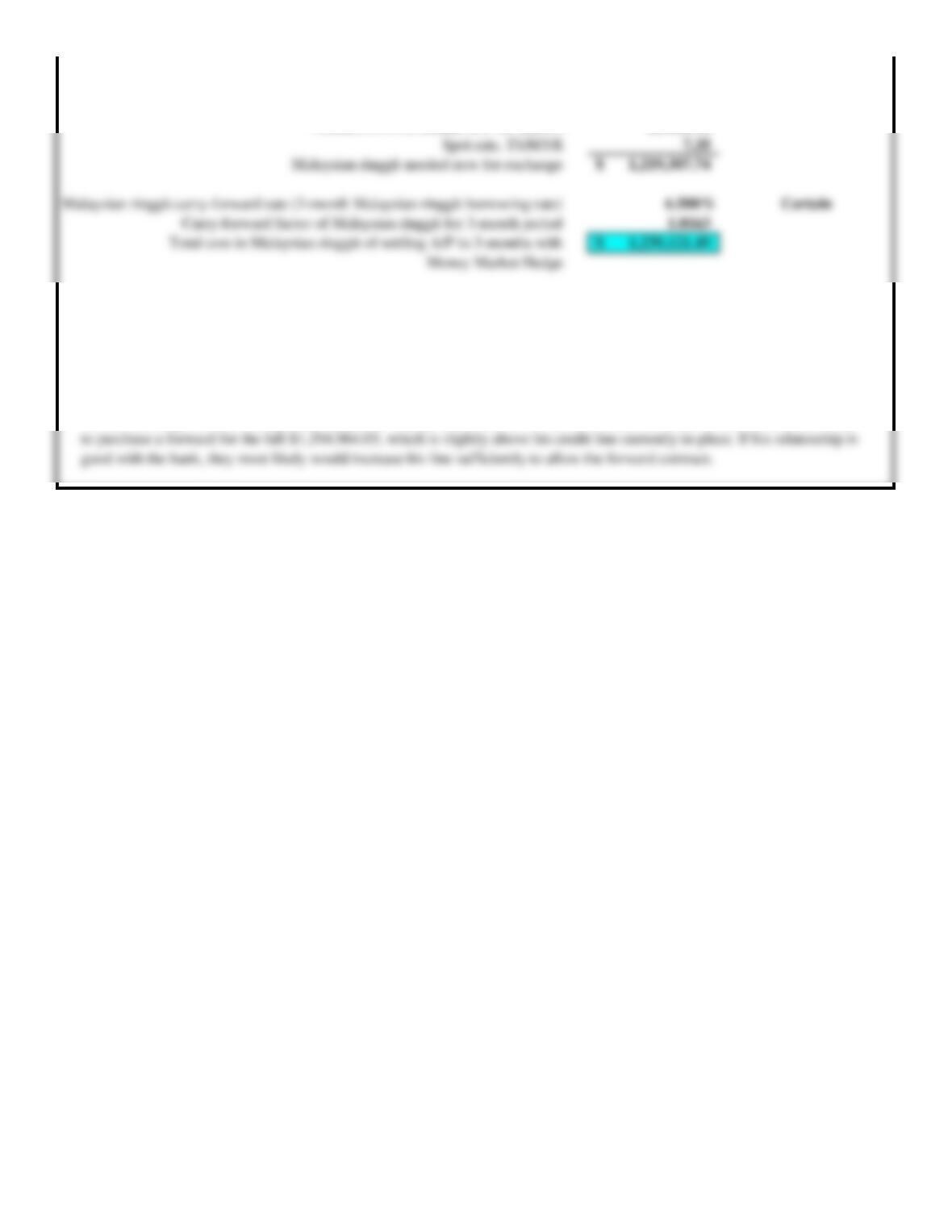

Discussion.

This is a difficult decision. The forward contract appears to be the preferable choice, protecting him against an appreciating

T$, and creating a certain cash purchase payment. The problem, however, will be whether the Bank of Hawaii will allow him

to purchase a forward for the full $1,294,964.03, which is slightly above his credit line currently in-place. If his relatonship is

good with the bank, they most likely would increase his line sufficiently to allow the forward contract.

The currency risk is eliminated, but since Ahmad Chik would have to exchange the money up-front, it would require him to

borrow the money, increasing his debt outstanding for the entire 3 months.