231

Chapter 9 Cash Flow and Capital Budgeting

Chapter Overview

The Opening Focus looks at the law passed by President Obama in 2010 as a part of the Tax Relief,

Unemployment Insurance Reauthorization, and Job Creation Act. This act allowed business (one

of many things the law allowed) to claim depreciation expense at a much fast rate than had been

previously allowed. Businesses could claim up to 50% of the new asset put into use during the

year it was purchased. How did this act help in capital budgeting of new projects?

Discussion Questions

1. What other business elements – besides depreciation – of any industry will have an impact on

future cash flows?

2. Once you identify these elements which are the most uncertain aspects of this enterprise?

This chapter looks at:

9-1 Types of Cash Flows

Technology

1. Smart Practices Video features Paul Sevastano, director of Information Technology for

2. Smart Concepts Animation shows a step-by-step explanation of opportunity costs.

4. Smart Practices Video shows David Nickel, controller of Intel Corp., talk about the role of the

capital budgeting function in funding programs.

6. Smart Solutions provide a step-by-step solution to Problem P9-1 about calculating present

value using different depreciation amounts and P9-19, an NPV and EAC problem for three dif-

ferent project cash flows.

Lecture Guide

In order to calculate the NPV of a project, you need to know future cash flows and a discount rate.

While it is not true that the only function of forecasting is to make astrology look good, it is diffi-

cult to project cash flows into the future. The company must look at strategic considerations – does

the project fit in with company goals? Can we raise the money for the project? Do we have the

232 Instructor’s Manual

capacity to handle the new project? The firm also must look at economic profit – is the project go-

ing to add to shareholders’ wealth?

9.1 Types of Cash Flows

9.1a Cash Flow versus Accounting Profit

Cash flows should be evaluated on an after tax basis. The cost of capital is the return required

by investors after corporate taxes, in other words, an after-tax weighted cost of capital. There is no

simple relationship between the pre tax and post tax return. Some companies calculate cash flows

on a pre-tax basis, and then use a higher discount rate. This is not accurate. The only area where

ly be known to the target company preparing the cash flows.

Students should be wary of allocated overhead. While in the real world, many firms do incor-

rectly put allocated overhead costs, students should know that these too must pass the test: will a

cash flow change because of the addition of a project? If the answer is yes, then the cash flow is

Focusing on Incremental Cash Flows

It is very important to discount incremental cash flows – only those cash flows that will change

if a project is accepted. This is often a difficult thing for students to isolate and an example will

help.

Financing Costs and Considering Taxes

When discounting free cash flows using the weighted average cost of capital, the company is

Chapter 9 Cash Flow and Capital Budgeting 233

Cash Flow and Non-Tax Expenses

It is important to use only actual cash flows – those for which you actually write a check, like labor

9.1b Depreciation

Again, depreciation itself is not important; it is the tax impact of depreciation that matters in the

9.1c Fixed Asset Expenditures

Most of the time, the manager can be reasonably certain about the initial investment of a pro-

9.1d Net Working Capital Expenditures

Note that most analyses tie increases in working capital to increases in sales. This is a very

Working Capital for Calendar Sales Booth

This section provides a numerical example of calculating increases in working capital that are rele-

vant to the capital budgeting decision.

9.1e Terminal Value

Note that it is very difficult to forecast out too far in the future, and most year by year forecasts

last 5 to 10 years. Most cash flow forecasts assume that after a given year cash flows will grow at

a steady rate, often the nominal growth rate, the real growth rate plus an inflation premium. At this

234 Instructor’s Manual

Terminal Value of SDL Acquisition

This section provides a numerical example of calculating terminal values.

9-2 Incremental Cash Flows

Capital budgeting rules clearly state that sunk costs are irrelevant and should not be included.

Sometimes this is a difficult, subjective decision also. For example, again take the drug company.

Research Animal Testing Human Trials Test Marketing Production

9-2a Sunk Costs

Technically all costs before the production phase are sunk costs. In reality, a company that

only covered its production costs and failed to cover its extensive research and testing costs would

not stay in business very long. So, how does a company account for these? Typically a company

9.2b Opportunity Costs

There is an opportunity cost every time there is an alternate use for a resource. The resource

9.2c Cannibalization

9.3 Cash Flows for Protect IT, Incorporated

This section of the chapter follows a cash flow analysis step-by-step through the entire process.

Table 9.2 Projections for Protect IT’s Investment Project

Chapter 9 Cash Flow and Capital Budgeting 235

Table 9.3 Annual Net Cash Flow Estimates for Protect IT’s Investment Project

9.4 Special Problems in Capital Budgeting

9.4a Capital Rationing

A Fundamental Question: If there are multiple projects with positive NPVs, why not accept all

of them? Finance theory states that a firm with positive net present value projects will be able to

9.4b Equipment Replacement and Unequal Lives and Equivalent Annual Cost

Note to students that equivalent annual cost is generally the easiest way to compute cost differ-

ences. Note that you do not need to know revenues. You can assume that revenues will be the

For example, suppose you have a choice of two projects with the following cash flows:

Year 0 1 2

Project A cash flow -50 100 200

Project B cash flow -100 50 175

Assuming a 10% discount rate, project A has an NPV of $40.9. Project B has an NPV of

$62.8. Since 63 is greater than 41, Project B looks like it is a better project. However, you could

do two project As for the price of one project B. Two times Project A’s NPV is 40.9 x 2 = $81.8.

Table 9.4 Capital Rationing and Profitability Index

Table 9.5 Operating and Replacement Cash Flows for Two Devices (all values are outflows)

9.4c Excess Capacity

This is another example of an opportunity cost. Just because a resource is available does not

236 Instructor’s Manual

9.5 The Human Face of Capital Budgeting

Student Interaction: Ask them to think of mistakes they have seen made in businesses that

were public in nature. Point out to students that it is very difficult to admit that a past decision you

Cash Flow and Capital Budgeting Summary

A financial manager needs to consider all aspects of a capital budgeting decision. In the real world

there are many uncertainties that make this a complex and difficult decision.

Enrichment Exercise

Have students work in groups to solve a capital budgeting problem. Give confidential assignments

to each group member. In the discussion following, talk about the group process as well as the an-

swer to the capital budgeting problem. Some examples of confidential assignments include:

1. Your confidential assignment is to try to get all group members to express their opinions.

Draw out other members and encourage minority points.

Answers to Concept Review Questions

1. a. It’s important for financial analysts to focus on incremental cash flows so that the analysts

b. An analyst should ignore financing costs for individual projects, and instead should use a

c. Analysts should consider taxes’ influence the capital budgeting decision because taxes can

Chapter 9 Cash Flow and Capital Budgeting 237

d. Analysts must recognize the importance of non-cash expenses if these expenses reduce the

2. Changes in net working capital are generally more important than the absolute level of working

capital associated with a project. The company starts out with a certain amount of working cap-

3. The higher the growth rate of cash flows, the higher the terminal value of the project. A project

4. A sunk cost is a cost that has already been paid and is therefore not recoverable. Cannibaliza-

tion is the “substitution effect” that frequently occurs when a firm introduces a new product.

5. The cost to the real estate firm for using the space itself is the opportunity cost of not renting

6. NPV based on net income could be higher if the company has low depreciation and high addi-

7. Cannibalization is not likely in this case because the new product line is quite different from

8. Protect IT might have assumed a stable perpetuity, rather than a growing perpetuity, which

would have given it a lower terminal value.

10. When managers are constrained by the availability of funds and they cannot invest in every

project that has a positive NPV, they face so-called capital-rationing. Whenever managers

have to choose from a set of possible investments they must choose a combination of projects

that maximizes shareholder wealth, subject to the constraint of limited funds. The profitability

238 Instructor’s Manual

11. Using equivalent annual cost (EAC) method to compare substitutable projects with different

lives is more efficient when it would take a large number of repetitions of the NPV calculations

12. You could compute two NPVs – now and a year from now, with appropriate changes in the

13. The cost of excess capacity would be zero if there were no current or future uses for that excess

14. Managers tend to be favorably biased toward projects stemming from their own ideas. They

may consciously or unconsciously manipulate the projects they favor to show positive cash

Answers to Self-Test Problems

ST9-1. Claross, Inc. wishes to determine the relevant operating cash flows associated with the

proposed purchase of a new piece of equipment having an installed cost of $10 million and

falling into the 5-year MACRS asset class. The firm’s financial analyst estimated that the

relevant time horizon for analysis is 6 years. She expects the revenues attributable to the

equipment to be $15.8 million in the first year and to increase at 5% per year through year

6. Similarly, she estimates all expenses other than depreciation attributable to the equip-

ment to total $12.2 million in the first year and to increase by 4% per year through year 6.

She plans to ignore any cash flows after year 6. The firm has a marginal tax rate of 40%

and its required return on the equipment investment is 13%. (Note: Round all cash flow

calculations to the nearest $0.01 million.)

a. Find the relevant incremental cash flows for years zero through 6.

b. Using the cash flows found in part a, determine the NPV and IRR for the proposed

equipment purchase.

c. Based on your findings in part b, would you recommend that Claross, Inc. purchase the

equipment? Why?

Chapter 9 Cash Flow and Capital Budgeting 239

A: a. ($million)

Year:

0

1

2

3

4

5

6

Initial investment

-10

Revenue (+5%/yr)

Expenses (+4%/yr

EBDT

-Depreciation*

EBT

-Taxes (40%)

EAT

+Depreciation*

Total cash flow

-10

*Depreciation:

Year Rate(from Table 9.1) Cost Depreciation

1 0.2000 10.0 2.00

2 0.3200 10.0 3.20

ST9-2. Atech Industries wants to determine whether it would be advisable for it to replace an ex-

isting, fully depreciated machine with a new one. The new machine will have an after-tax

installed cost of $300,000 and will be depreciated under a 3-year MACRS schedule. The

old machine can be sold today for $80,000 after taxes. The firm is in the 40% tax bracket

and requires a minimum return on the replacement decision of 15% The firm’s estimates

of its revenues and expenses (excluding the depreciation) for both the new and the old ma-

chine (in $thousands) over the next four years are given below.

New Machine Old Machine

Year Revenue Expenses Revenue Expenses

(excl. depr (excl. depr.)

1 $ 925 $740 $625 $580

2 990 780 645 595

3 1,000 825 670 610

4 1,100 875 695 630

240 Instructor’s Manual

Atech also estimates the values of various current accounts that would be impacted by the

proposed replacement. They are shown below for both the new and old machine over the

next four years. Currently (at time 0) the firm’s net investment in these current accounts is

assumed to be $110,000 with the new machine and $75,000 with the old machine.

New Machine

Year: 1 2 3 4 .

Cash $20,000 $25,000 $ 30,000 $ 36,000

Atech indicates that after four years of detailed cash flow development, it will assume in

analyzing this replacement decision that the year 4 incremental cash flows of the new ma-

chine over the old machine will grow at a compound annual rate of 2% from the end of

year 4 to infinity.

a. Find the incremental operating cash flows (including any working capital investment)

for years 1 to 4 for Atech’s proposed machine replacement decision.

A: a.

Year: 0 1 2 3 4

NEW MACHINE

Investment -300,000

Revenue 925,000 990,000 1,000,000 1,100,000

Chapter 9 Cash Flow and Capital Budgeting 241

OLD MACHINE

(2) Operating CF 15,000 25,000 31,000 36,000

INCR. CF[(1)-(2)] -220,000 16,006 5,990 22,342 66,662

* New Asset Depreciation:

Year Rate Cost Depreciation

** New Machine Working Capital Investment:

NWC = Cash + Accounts Receivable + Inventory-Accounts Payable

*** Old Machine Working Capital Investment

NWC= Cash + Accounts Receivable + Inventory − Accounts Payable

∆NWC = NWC − [Prior year’s NWC]

b. Year 5 operating CF = $66,662 (1+.02)1 = $67,995

Terminal value at end of Year 4 = $67,995 = $523,038

242 Instructor’s Manual

Year Cash Flow

0 -$220,000

e. Atech should undertake the proposed machine replacement because the NPV of

ST9-3. Performance, Inc. is faced with choosing between two mutually exclusive projects with

differing lives. It requires a return of 12% on these projects. Project A requires an initial

outlay at time 0 of $5,000,000 and is expected to require annual maintenance cash outflows

of $3,100,000 per year over its two-year life. Project B requires an initial outlay at time 0

of $6,000,000 and is expected to require annual maintenance cash outflows of $2,600,000

A: a. Project A NPV = -$10,239,158

Project B NPV = –$12,244,761

b. Project A would be recommended because it has the lower cost NPV. The problem

with this comparison is that Project A provides service for only 2 years versus Project

B’s three-year service life.

Answers to End-of-Chapter Questions

Q9–1. In capital budgeting analysis, why do we focus on cash flow rather than accounting profit?

Chapter 9 Cash Flow and Capital Budgeting 243

A9-1. Accounting numbers may not accurately reflect when revenues are received or when pay-

ments are made. Net present value focuses on when money is actually received or paid and

Q9–2. To finance a certain project, a company must borrow money at 10 percent interest. How

should it treat interest payments when it analyzes the project’s cash flows?

A9-2. Interest expense should be ignored and should not be treated as a cash outflow. The dis-

Q9–3. Does depreciation affect cash flow in a positive or negative manner? From a net present

value perspective, why is accelerated depreciation preferable? Is it acceptable to utilize one

depreciation method for tax purposes and another for financial reporting purposes? Which

method is relevant for determining project cash flows?

A9-3. Depreciation positively impacts cash flow. Depreciation reduces taxable income. The low-

Q9–4. In what sense does an increase in accounts payable represent a cash inflow?

A9-4. An increase in accounts payable is a cash inflow in the sense that the firm is asking its

Q9–5. List several ways to estimate a project’s terminal value.

A9-5. Terminal value can be calculated using the growing perpetuity model, which states that

Q9–6. What are the tax consequences of selling an investment asset for more than its book value?

Does this have an effect on project cash flows that must be accounted? What is the effect if

the asset is sold for less than its book value?

A9-6. If an investment is sold for more than its book value, then the firm has a capital gain on the

difference between market price and book value and must pay capital gains taxes on that

244 Instructor’s Manual

Q9–7. Why must incremental after-tax cash flows rather than total cash flows be evaluated in pro-

ject analysis?

A9-7. Incremental cash flows matter because the project evaluator is looking at what will change

Q9–8. Differentiate between sunk costs and opportunity costs. Which of these costs should be

included in incremental cash flows, and which should be excluded?

A9-8. Sunk costs should not be included in a cash flow analysis. These are costs that have already

been paid. Accepting or rejecting the project will not impact these costs. These are not in-

Q9–9. Why is it important to consider cannibalization in situations where a company is consider-

ing adding substitute products to its product line?

A9-9. Cannibalization is the “substitution effect” that frequently occurs when a firm introduces a

new product. Typically, some of the new product’s sales will come at the expense of the

Q9-10. Before entering graduate school, a student estimated the value of earning an MBA at

$300,000. Based on that analysis, the student decided to go back to school. After complet-

ing the first year, the student ran the NPV calculations again. How would you expect the

NPV to look after the student has completed one year of the program? Specifically, what

portion of the analysis must be different than it was the year before?

Q9-11. Punxsutawney Taxidermy Inc. (PTI) operates a chain of taxidermy shops across the Mid-

west, with a handful of locations in the South. A rival firm, Heads Up Corp., has a few

Midwestern locations, but most of its shops are located in the South. PTI and Heads Up

decide to consolidate their operations by trading ownership of a few locations. PTI will ac-

quire four Heads Up locations in the Midwest, and in exchange will relinquish control of

its Southern locations. No cash changes hands up front. Does this mean that an analyst

working for either company can evaluate the merits of this deal by assuming that the pro-

ject has no initial cash outlay? Explain.

A9-11. There are two ways to approach this problem. First, each company could estimate the cash

value of the stores that it is giving up. This is the cash price that the firm might obtain from

another buyer, and therefore represents the opportunity cost of this deal. This could be

Chapter 9 Cash Flow and Capital Budgeting 245

treated as the initial cash outflow. Next, analysts would compare this cash outflow to the

present value of cash inflows generated by the stores it is acquiring to determine the overall

NPV.

But what about the cash inflows that the company loses on the stores it gives up? Isn’t

that another opportunity cost? The answer is that it depends. If analysts treat the opportuni-

Q9-12. What is the only relevant decision for independent projects if an unlimited capital budget

exists? How does your response change if the projects are mutually exclusive? How does

your response change if the firm faces capital rationing?

A9-12. If the capital budget is unlimited, managers should rank the available projects according to

their PIs and invest in all projects with a PI > 1, respectively all projects with a NPV >0. If

Q9-13. Explain why the equivalent annual cost (EAC) method helps firms evaluate alternative in-

vestments with unequal lives.

A9-13. The EAC method provides a present value per year. This means one can look at the yearly

contribution of an investment, rather than just the total investment. In other words, it might

Q9-14. Why isn’t excess capacity free?

A9-14. Excess capacity is not free. It was originally accounted for when the project was first cho-

sen – that size equipment that produced the excess capacity was included in those project

cash flows. If there truly is no use for excess capacity, now or in the future, for the original

Answers to End-of-Chapter Problems

Types of Cash Flows

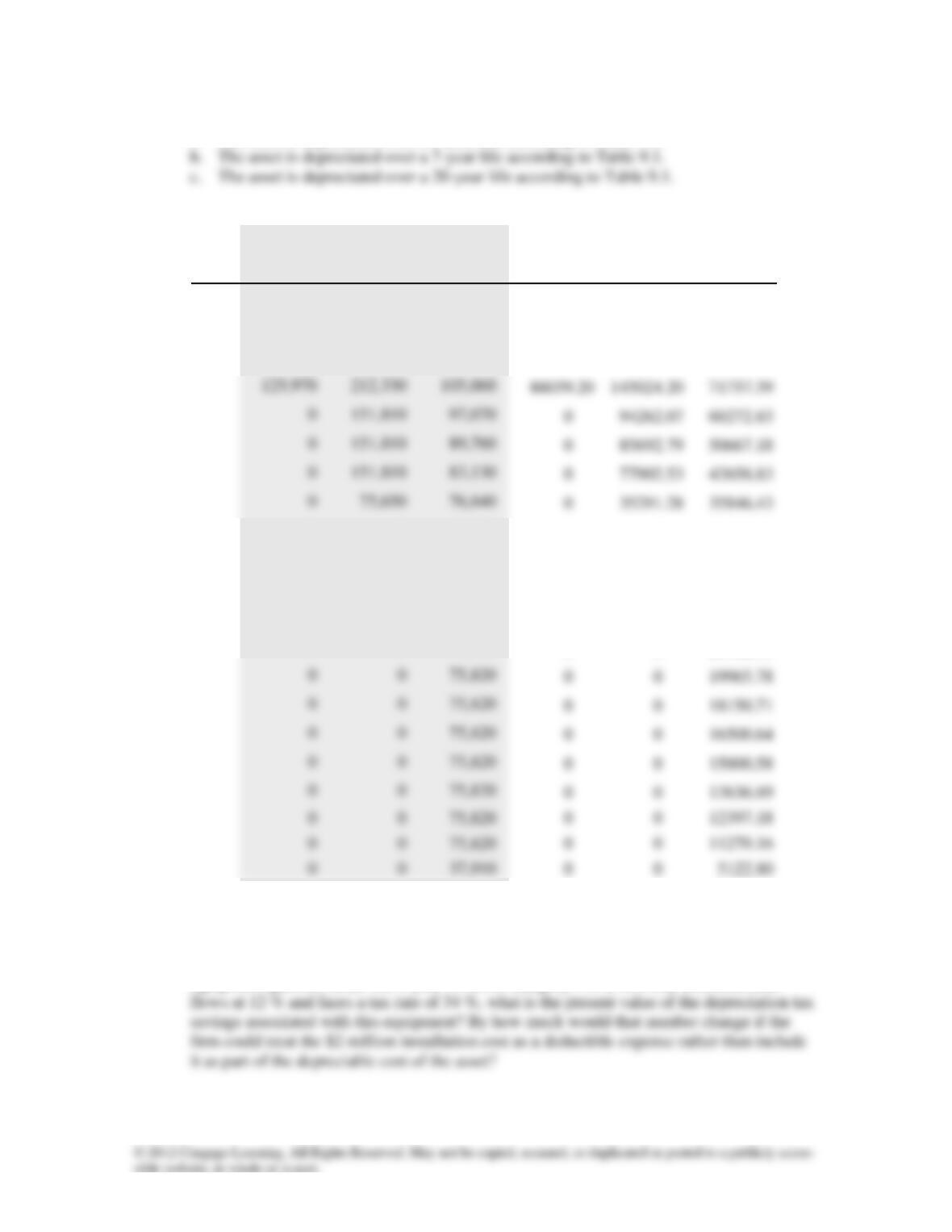

P9-1. Calculate the present value of depreciation tax savings on a depreciable asset with a pur-

chase price of $5 million and zero salvage value, assuming a 10 % discount rate, a 34 %

246 Instructor’s Manual

a. The asset is depreciated over a 3-year life according to Table 9.1.

A9-1.

Depreciation A/T ($)

Present Values ($)

3

7

20

a. 3

b. 7

c. 20

566,610

242,930

63,750

515100.00

220845.50

57954.55

755,650

416,330

122,740

624504.10

344074.40

101438.00

251,770

297,330

113,560

189158.50

223388.40

85319.31

125,970

212,330

105,060

86039.20

145024.20

71757.39

0

151,810

97,070

0

94262.07

60272.83

0

151,810

89,760

0

85692.79

50667.18

0

151,810

83,130

0

77902.53

42658.83

0

75,650

76,840

0

35291.28

35846.43

0

0

75,820

0

0

32155.08

0

0

75,820

0

0

29231.89

0

0

75,820

0

0

26574.45

0

0

75,820

0

0

24158.59

0

0

75,820

0

0

21962.35

0

0

75,820

0

0

19965.78

0

0

75,820

0

0

18150.71

0

0

75,820

0

0

16500.64

0

0

75,820

0

0

15000.58

0

0

75,820

0

0

13636.89

0

0

12397.18

PV of Depreciation Tax Savings

$1,414,802

$1,226,481

$752,042

P9-2. A certain piece of equipment costs $32 million plus an additional $2 million to install. This

equipment qualifies under the 5-year MACRS category. For a firm that discounts cash

Chapter 9 Cash Flow and Capital Budgeting 247

A9-2.

End of

Year

Depr. %

Depr. Tax

Savings

PV Depr. Tax

Savings

Tax Savings

w/o Exp.

PV Tax Savings

w/o Exp.

0

$ 680,000*

1

20.0

$2,312,000

$2,064,286

$2,176,000

1,942,857

2

32.0

3,699,200

2,948,980

3,481,600

2,775,510

3

19.2

2,219,520

1,579,810

2,088,960

1,486,880

4

11.52

1,331,712

1,253,376

5

11.52

1,331,712

1,253,376

6

5.76

depreciate

The present value of the write-offs when including the installation cost as part of the de-

preciable base is $178,093 less ($8,710,489 – $8,532,396) than had the installation cost

been expensed up front.

P9-3. The government is considering a proposal to allow even greater accelerated depreciation

deductions than those specified by MACRS.

a. For which type of company would this change be more valuable, a company facing a

A9-3. a. The company with the higher tax rate will receive more benefit from accelerated de-

preciation than the company with the lower tax rate.

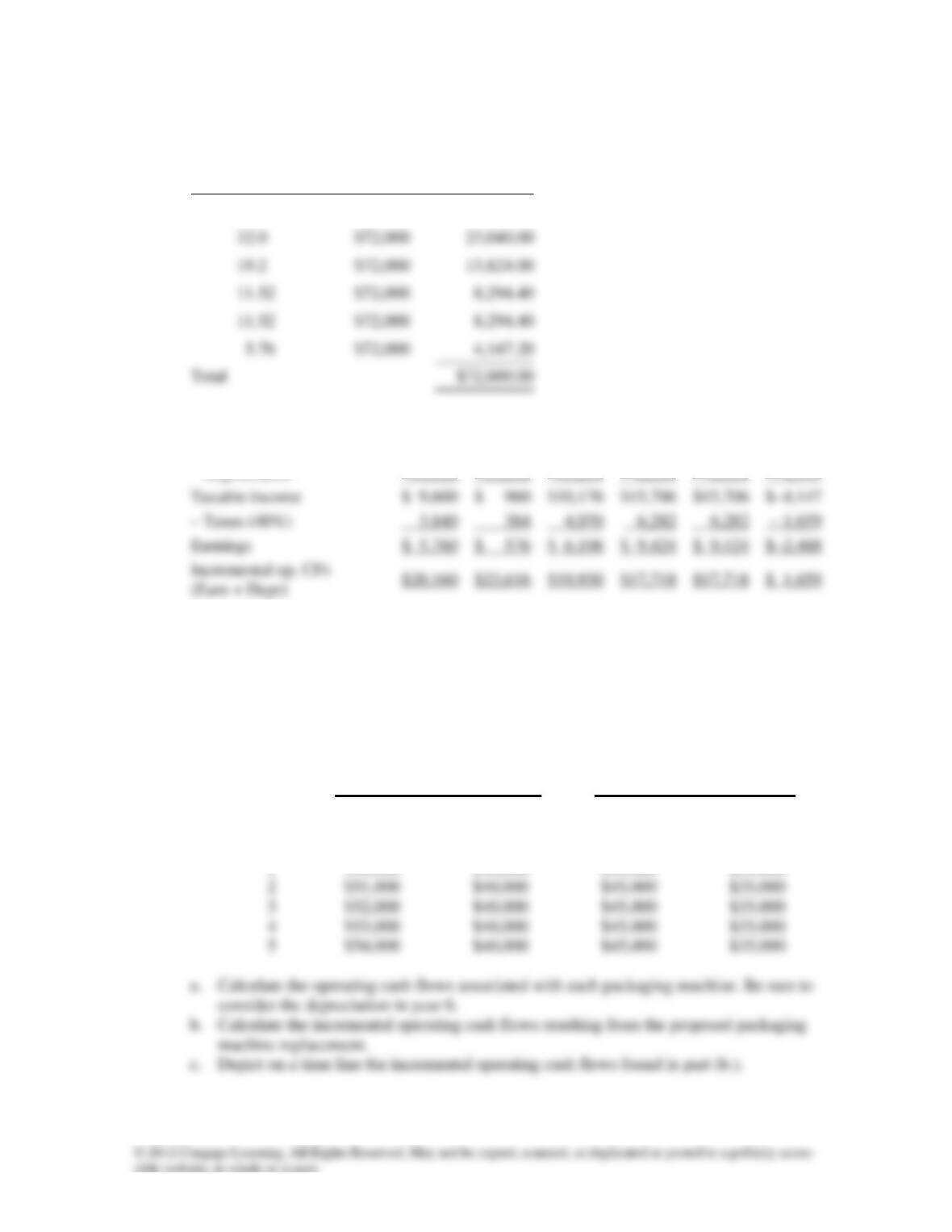

P9-4. Taylor United is considering overhauling its equipment to meet increased demand for its

product. The cost of the equipment overhaul is $3.8 million plus $200,000 in installation

costs. The firm will depreciate the equipment modifications under MACRS using a 5-year

recovery period. Additional sales revenue from the overhaul should amount to $2.2 million

248 Instructor’s Manual

A9-4.

Year

5-Year

MACRS %

Installed Cost

Depreciation

Amount

1

20.0

$4,000,000

$ 800,000

2

32.0

$4,000,000

1,280,000

3

19.2

$4,000,000

4

11.52

$4,000,000

5

11.52

$4,000,000

Totals

Year:

1

2

3

4

5

6

Sales

$2,200,000

$2,200,000

$2,200,000

$2,200,000

$2,200,000

$2,200,000

– Expenses (35%)

770,000

770,000

770,000

770,000

770,000

770,000

Taxable income

$ 630,000

$1,199,600

– Taxes (40%)

252,000

479,840

Earnings

$ 378,000

$ 719,760

b. See earnings line in table above.

c. See increase in op. CFs line in table above.

P9-5. Wilbur Corporation is considering replacing a machine. The replacement will cut operating

expenses by $24,000 per year for each of the five years the new machine is expected to

Chapter 9 Cash Flow and Capital Budgeting 249

A9-5.

5-Year

MACRS %

Installed

Cost

Depreciation

20.0

$72,000

$14,400.00

Year

0

1

2

3

4

5

6

Reduced expenses

$24,000

$24,000

$24,000

$24,000

$24,000

$ 0

– Depreciation

14,400

23,040

13,824

8,294

8,294

4,147

Taxable income

$ 9,600

$ 960

$10,176

$15,706

$15,706

3,840

384

4,070

6,282

6,282

Earnings

$ 5,760

$ 576

$ 6,106

$ 9,424

$ 9,424

(Earn + Depr)

P9-6. Advanced Electronics Corporation is considering purchasing a new packaging machine to

replace a fully depreciated packaging machine that will last five more years. The new ma-

chine is expected to have a 5-year life and depreciation charges of $4,000 in year 1; $6,400

in year 2; $3,800 in year 3; $2,400 in both year 4 and year 5; and $1,000 in year 6. The

firm’s estimates of revenues and expenses (excluding depreciation) for the new and old

packaging machines are shown in the following table. Advanced Electronics is subject to a

40 % tax rate on ordinary income.

New Packaging Machine .

Old Packaging Machine .

Year

Revenue

Expenses

(excluding

depreciation)

Revenue

Expenses

(excluding

depreciation)

1

$50,000

$40,000

$45,000

$35,000

3

$52,000

$40,000

$45,000

$35,000

5

$54,000

$40,000

$45,000

$35,000

250 Instructor’s Manual

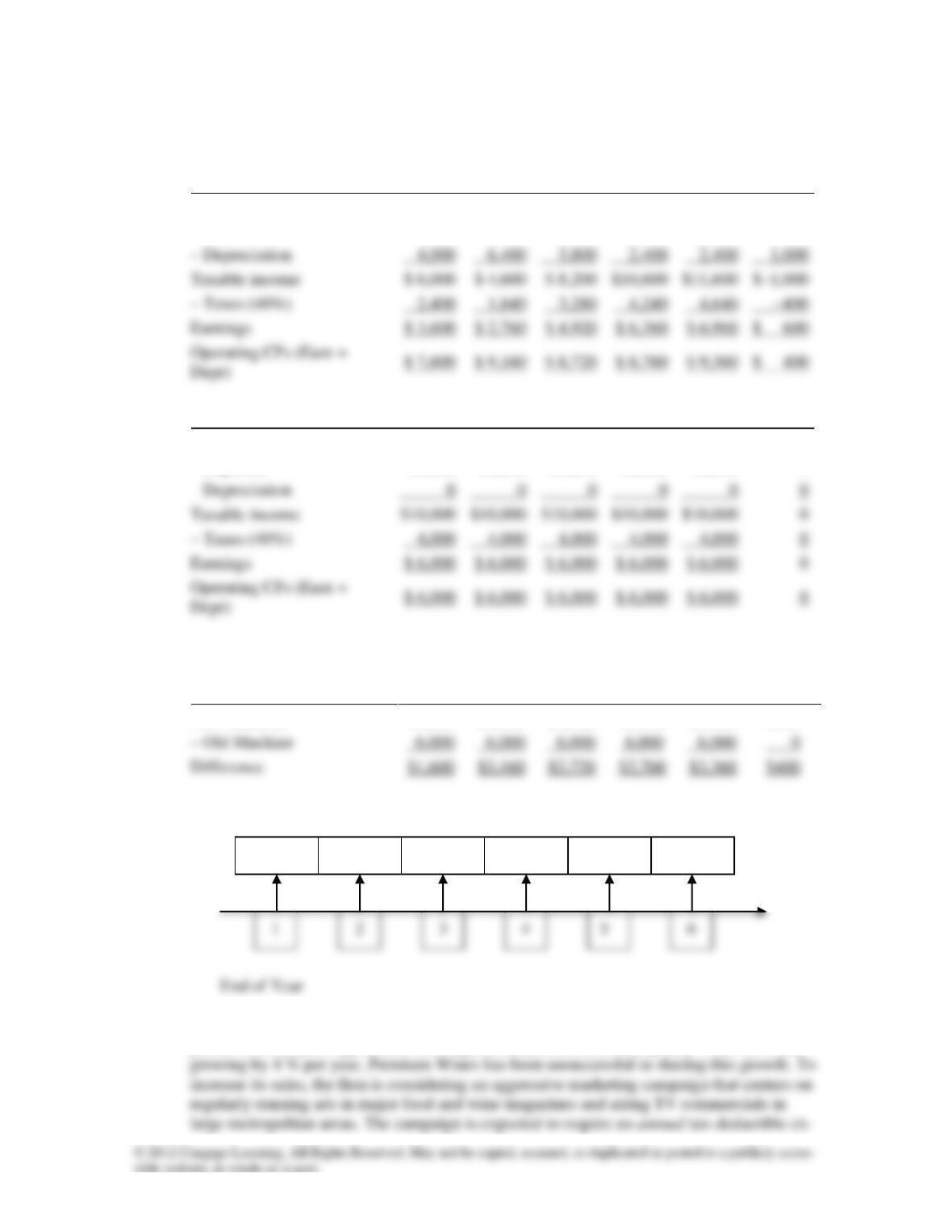

A9-6.

a.

New Machine

0

1

2

3

4

5

6

Sales

$50,000

$51,000

$52,000

$53,000

$54,000

$ 0

– Expenses

40,000

40,000

40,000

40,000

40,000

0

Taxable income

$10,600

$11,600

– Taxes (40%)

–400

Earnings

$ –600

Depr)

Old Machine

0

1

2

3

4

5

6

Sales

$45,000

$45,000

$45,000

$45,000

$45,000

0

– Expenses

35,000

35,000

35,000

35,000

35,000

0

– Depreciation

0

0

0

0

0

0

– Taxes (40%)

4,000

4,000

4,000

4,000

0

Earnings

0

b. Incremental operating cash flows

Year

0

1

2

3

4

5

6

New Machine

$7,600

$9,160

$8,720

$8,760

$9,360

$400

– Old Machine

6,000

6,000

6,000

6,000

0

c.

P9-7. Premium Wines, a producer of medium-quality wines, has maintained stable sales and

profits over the past eight years. Although the market for medium-quality wines has been

$1,600

$3,160

$2,720

$2,760

$3,360

$400