COUNTY OF SACRAMENTO

PROPRIETARY FUNDS

STATEMENT OF NET ASSETS

JUNE 30, 2009

(amounts expressed in thousands)

Page 2 of 2 Busi ness–type Activiti es – Enterprise Funds

Gover nme ntal

Water Nonmaj or Act ivities-Internal

Airport Solid Waste Agency Enterprise Funds Total Service Funds

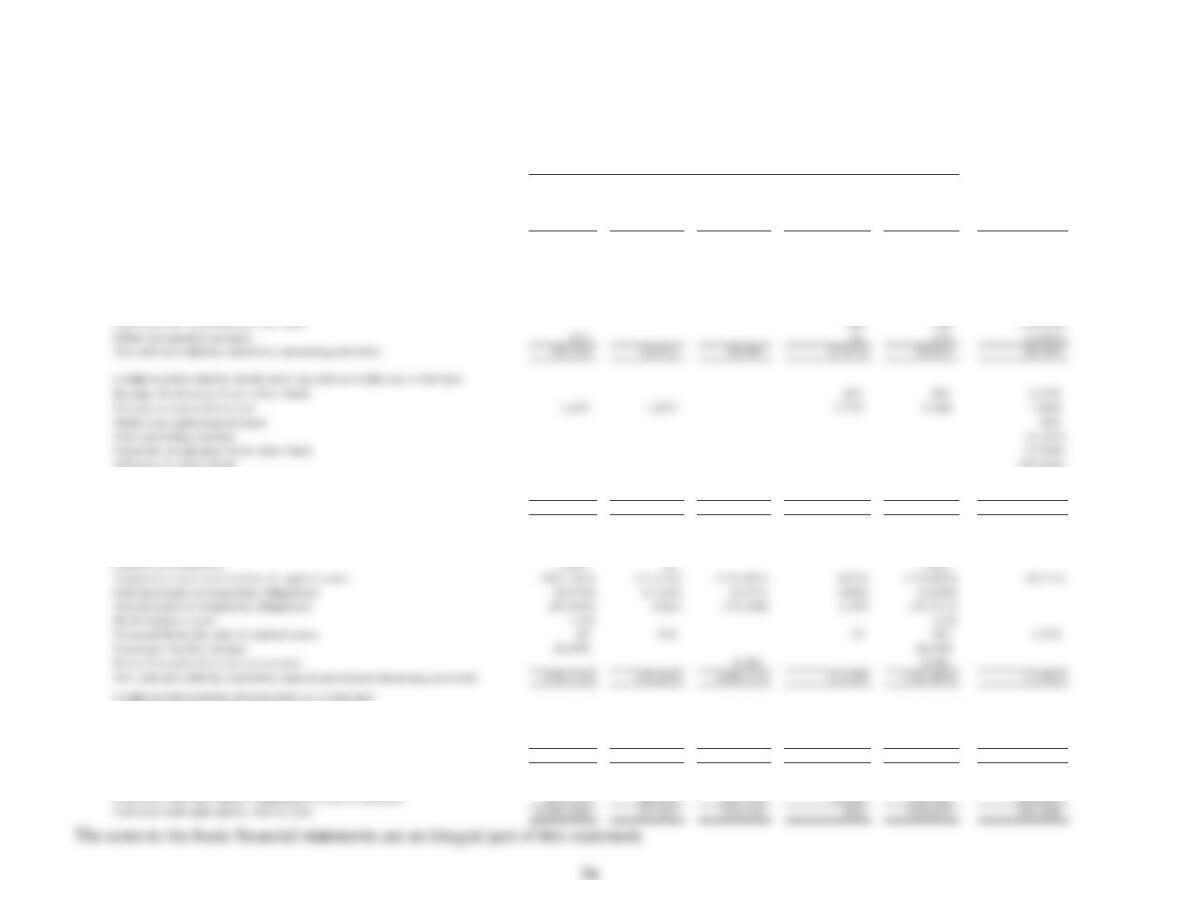

Liabiliti es:

Current li abiliti es:

Warrants payable 14,977 $ 292 410 23 15,702 5,896

Accrued liabilities 5,517 2,848 12,725 189 21,279 19,724

Intergovernmental payable 442 76 518 7,353

Total current liabilities 92,477 10,196 22,904 901 126,478 93,374

Noncurrent liabil ities:

Insura nce c laims pa ya ble 120,542

Long-term debt obligat ions 548,921 19,763 443,300 1,873 1,013,857

Compensated absences 3,351 1,777 808 3 5,939 16,932

Other post employment benefits 164 112 125 4 405 991

Long-term advances from other funds 491 491 15,579

Invested in capital assets, net of related debt 175,059 95,700 305,277 1,869 577,905 62,077

Restricted for:

La nd f ill c los u r e 8 ,2 7 9 8 , 2 7 9

Kiefer Wetlands Preserve 862 862

Debt service 29,260 29,260

The notes to the basic financial statements are an integral part of this statement.

33

COUNTY OF SACRAMENTO

PROPRIETARY FUNDS

STATEMENT OF REVENUES, EXPENSES

AND CHANGES

IN FUND NET ASSETS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Business–type Activities – Enterprise F unds

Governmental

Nonmajor Act ivities–Internal

Air port Solid Waste Wa ter Agency Enterprise Funds Total Service Funds

Operating revenues:

Charges for sales and services 118,691 $ 60,895 39,935 3,037 222,558 407,314

Other 300 758 1,901 99 3,058 12,551

Total operating revenues 118,991 61,653 41,836 3,136 225,616 419,865

Operating expenses:

Salaries and benefits 32,126 23,704 7,299 542 63,671 164,730

Services and supplies 49,871 29,286 8,363 9,399 96,919 162,565

Passenger facility charges 21,490 21,490

Sales / use tax 483 483

Interest expense (18,204) (1,085) (2,428) (139) (21,856) (1,450)

Other (342) 1,644 1,048 15 2,365 (697)

Total nonoperating revenues (expenses) 10,080 2,260 (1,762) 2,223 12,801 (382)

34

Intentionally Blank

35

COUNTY OF SACRAMENTO

PROPRIETARY FUNDS

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Page 1 of 2

Business-t ype Activities – Ent erprise Funds

Go v er n m en t al

Nonmajor Activities–

Water Enterprise Internal Service

Airport Solid Waste Agency Funds T ot al Funds

CASH FLOWS FROM OPERATING ACT IVITIES:

Receipts from customers and users $ 117,282 54,538 36,090 3,099 211,009 62,832

Receipts from interfund services provided 121 121 381,962

Receipts from other operating activities 6,389 1,901 8,290 257

Payments to suppliers (40,430) (24,749) (10,492) (11,194) (86,865) (215,892)

Payments to employees (31,635) (23,486) (5,958) (589) (61,668) (169,811)

Interest paid on advances from other funds (1,450)

Transfers to/from other funds (1,514) (5,588) (412) (7,514) (10,751)

Net cash provided by (used for) noncapital financing activities (59) (3,715) (412) 2,723 (1,463) (48,813)

CASH FLOWS FROM CAPITAL AND RELAT ED FINANCING ACTIVIT IES:

Intergovernmental grants received 223 223

Purchase of investments (79,875) (7,700) (87,575)

Proceeds from sales and maturities of investments 244,443 72,042 316,485

Interest received on cash and investments 10,912 1,466 11,224 125 23,727 34

Net cash provided by (used for) investing activities 175,480 1,466 75,566 125 252,637 34

Net increase in cash and cash equivalents 26,070 (8,692) (71,678) (6,204) (60,504) (25,761)

COUNTY OF SACRAMENTO

PROPRIETARY FUNDS

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Page 2 of 2

Business-type Activities – Enterprise Funds

Nonmajor Activities–

Water Enterprise Internal Service

Airport Solid Waste Agency Funds Total Funds

RECONCILIATION OF CASH AND CASH EQUIVALENT S

Depreciation 25,750 7,126 8,418 418 41,712 14,716

Amortization 32 32

Recoveries for uncollectible accounts (25) (25)

Impact fee credits applied (2,541) (2,541)

Other nonoperating revenue 157 (262) (105)

Warrants payable (530) (236) (193) (18) (977) (3,337)

Compensated absences 327 108 808 (69) 1,174 341

Due to other funds 5,089 (37) (4) 5,048 3,447

Deferred revenues (560) (560) (893)

Due to other governments (1) (1) (1,748)

The notes to the basic financial statements are an integral part of this statement.

37

COUNTY OF SACRAMENTO

FIDUCIARY FUNDS

STATEMENT OF FIDUCIARY NET ASSETS

JUNE 30, 2009

(amounts expressed in thousands)

Investment

Agency Trust

Assets:

Cas h and inves tments $ 220,493 1,987,436

Receivables, net of allowance for uncollectibles:

Liabilities :

Warrants payable $ 12,942

COUNTY OF SACRAMENTO

FIDUCIARY FUNDS

STATEMENT OF CHANGES IN FIDUCIARY NET ASSETS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Investment Trust

Additions:

Contributions on pooled investments $ 8,765,473

Intentionally Blank

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

NOTE 1 – REPORTING ENTITY AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The financial statements of the County of Sacramento (County) have been prepared in conformity with accounting principles generally accepted in the United States of

Scope of Financial Reporting Entity

The County reporting entity includes all significant organizations, departments, and agencies over which the County is considered to be financially accountable. The

County is a political subdivision of the State of California, and as such can exercise the powers specified by the Constitution and laws of the State of California. The

County operates under a charter and is governed by a five-member Board of Supervisors. In addition, as required by GAAP, the financial statements present the

financial position of the County and its component units (entities for which the County is considered to be financially responsible).

Blended Component Units:

The Tobacco Securitization Authority (Authority) of Northern California is a public entity legally separate and apart from the County, and is considered a blended

component unit of the County. The Authority was created by a Joint Powers Agreement effective July 15, 2001 between the County and the County of San Diego.

The Authority was created for the purpose of empowering the Authority to finance the payments received by the County from the nation-wide Tobacco Settlement

Agreement (Payments) for such purposes, but not limited to, issuance, sale, execution and delivery of all Bonds secured by those Payments or the lending of money

based thereof, or to securitize, sell, purchase or otherwise dispose of some or all of such payments of the County. The debts and liabilities of the Authority belong

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

of obtaining financing for various designated redevelopment and housing projects in the greater Sacramento area. The debts and liabilities of the PFA belong solely to

it, and neither the County nor the Agency is any way responsible for those liabilities. However, the PFA has an agreement with the Agency in which the Agency will

pay back to the PFA those debt proceeds advanced to them. The PFA meets the criteria set forth in generally accepted accounting principles as a blended component

unit of the County because of the financial benefit/burden relationship of their activities and the governing body is the same as the County.

The County has created the Public Facilities Financing Corporation (Corporation) for the purpose of facilitating the financing of public projects within the County. The

Certain assets, principally cash and investments, of these separate legal entities held by the County in a custodial capacity are included in the investment trust funds.

Joint Power Authorities or Jointly Governed Organizations

The County of Sacramento is a member of several Joint Powers Agencies (JPA) and/or jointly managed agencies. These are:

AGENCY PURPOSE

Sacramento Area Council of Governments Regional planning (primarily transportation)

Sacramento County Regional Sanitation District Waste water conveyance, treatment and disposal

Sacramento Area Sewer District Sewer Service

Southeast Connector JPA Planning and development of the Elk Grove-Rancho Cordova-El Dorado Connector

Project

42

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Government-wide and fund financial statements presentation

Government–wide Financial Statements:

The Statement of Net Assets and the Statement of Activities display information about the primary government, the County and its component units. These

statements include financial activities of the overall government, except for fiduciary activities. Eliminations have been made to minimize the double counting of

internal activities. These statements distinguish between the governmental and business-type activities of the County. Governmental activities, which are normally

supported by taxes and intergovernmental revenues, are reported separately from business-type activities, which rely to a significant extent on fees charged to

2) grants and contributions that are restricted to meeting the operational or capital requirements of a particular function. Taxes and other items not properly

included among program revenues are reported instead as general revenues.

Fund Financial Statements:

The fund financial statements provide information about the County’s funds, including fiduciary funds and blended component units. Separate statements for each

fund category: governmental, proprietary and fiduciary are presented. The emphasis of fund financial statements is on major governmental and enterprise funds,

Internal service funds are used to account for the financing of goods, services, or facilities provided by one department to other departments of the County, or to other

governmental units, on a cost-reimbursement basis. Internal service funds include Public Works, General Services, Self-Insurance funds covering general liability and

property damage, workers’ compensation, dental and unemployment, Regional Communication for emergency communications services, Office of Communications

and Information Technology, and Facility Planning, Architecture and Real Estate.

43

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Investment trust funds account for the assets of legally separate entities that deposit cash with the County treasury. These entities include school districts, other

independent special districts governed by local boards, regional boards and authorities, and pass through for property tax collections for cities. These funds represent

assets, primarily cash and investments, held by the County in trust for these participants.

Agency funds account for the assets held by the County as an agent for various individuals, private organizations and other governmental agencies. These include Law

Enforcement, Unapportioned Tax Collection, and other.

Measurement focus and basis of accounting

The government-wide, proprietary and investment trust fund financial statements are reported using economic resources measurement focus and accrual basis

accounting. Revenues are recorded when earned and expenses are recorded at the time the liabilities are incurred, regardless of when the related cash flow takes place.

Non-exchange transactions, in which the County gives or receives value without directly receiving or giving equal value in exchange, include property and sales taxes,

grants, entitlements and donations. Revenues from sales tax are recognized when the underlying transactions take place. Revenues from grants, entitlements and

donations are recognized in the fiscal year in which all eligibility requirements have been satisfied.

and 3) capital grants and contributions, including special assessments. Internally dedicated resources are reported as general revenues rather than as program revenues.

Likewise, general revenues include all taxes.

Proprietary funds distinguish operating revenues and expenses from non-operating items. Operating revenues and expenses generally result from providing services

and producing and delivering goods in connection with a proprietary fund’s principal ongoing operations. The principal operating revenues of the County’s enterprise

funds are charges to customers for services including: water, solid waste, airline fees and charges, parking fees and public transit fees. The principal operating revenues

non-operating revenues and expenses.

When restricted assets become available, for their restricted purpose, they are used first, and then unrestricted assets are used as they are needed.

Cash and Cash Equivalents

For purposes of the statement of cash flows the County considers all short-term highly liquid investments (including restricted assets) to be cash equivalents.

Investments held in the County Treasurer’s Pool are available on demand to individual entities, thus they are considered highly liquid and cash equivalents for purposes

County which have been purchased by the Treasurer’s Pool. The terms of the notes include a variable interest rate, adjusted on a quarterly basis, equal to the rate of

interest on the U.S. Treasury Note for the number of years corresponding to the remaining term of each note.

For financial reporting purposes, a debt service fund was created to account for the proceeds, subsequent purchase of delinquent taxes of the taxing entities, and the

accumulation of financial resources to be used to repay the notes. Collections on the delinquent secured taxes including interest and penalties purchased from the

various taxing entities will be the primary funding source. The delinquent secured taxes are recorded as a long-term receivable in the debt service fund.

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

The respective grant agreements generally require the County to maintain accounting records and substantiating evidence sufficient to determine if all costs incurred

and claimed are proper and that the County is in substantial compliance with other terms of the grant agreements. These records are subject to audit by the appropriate

government agency. Any amounts disallowed will reduce future claims or be directly recovered from the County.

Inventory for governmental funds consist of pharmacy supplies. Inventories are valued at cost, using the first-in/first-out method. Inventories of proprietary funds are

recorded at the lower of cost computed by the weighted average method or market value. Inventory purchases made by governmental funds are recorded as

expenditures at the time of purchase.

Restricted Assets

Certain proceeds of proprietary fund obligations, as well as certain other resources set aside for obligation repayment and future construction or acquisition of assets,

period. Amortization of assets acquired under capital lease is included in depreciation and amortization. Structures and improvements, infrastructure and equipment of

the primary government, are depreciated using the straight line method over the following estimated used lives:

Assets Years

Buildings and Improvements 4 to 50

Infrastructure 20 to 50

Equipment 3 to 25

46

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Compensated Absences

County employees are granted vacation in varying amounts based on classification and length of service. Additionally, certain employees are allowed compensated

time-off in lieu of overtime compensation and/or for working on holidays.

Proprietary Funds – Proprietary funds accrue a liability for unused compensated absences earned through year-end. An expense is recognized for the increase

in liability from the prior year.

Sick leave is earned by regular, full-time employees. Any sick leave hours not used during the period are carried forward to future years, with no limit to the number of

Bond issuance costs are reported as deferred charges and amortized over the term of the related debt.

In the fund financial statements, governmental fund types recognize bond premiums and discounts as well as bond issuance costs, during the current period. The face

amount debt issued and premiums are reported as other financing sources while discounts on debt issuances are reported as other financing uses. Issuance costs,

whether or not withheld from the actual debt proceeds received, are reported as debt service expenditures.

Fund Equity

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Liability/Property and Workers Compensation ISF Deficit Net Assets

As of June 30, 2009, the Liability/Property and Workers Compensation ISF have deficit net assets of ($4,585) and ($52,808), respectively. These deficits in net

assets represent the county’s unfunded liability for the liability/property and workers compensation self insurance programs. The County is collecting additional

amounts from the departments to eliminate the unfunded liability.

Golf Special Revenue Fund Deficit Fund Balance

2008. GASB Statement No. 52 establishes standards for accounting and financial reporting for land and other real estate as investments by endowments. The

provisions of this Statement do not apply to the County of Sacramento.

GASB Statement No. 55

Effective March 2009, the County implemented statement No. 55, The Hierarchy of Generally Accepted Accounting Principles for State and Local Government,

effective March of 2009. The objective of the Statement is to incorporate the hierarchy of Generally Accepted Accounting Principles (GAAP) for state and local

rather incorporates the existing guidance (to the extent appropriate in a governmental environment) into the GASB standards.

48

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

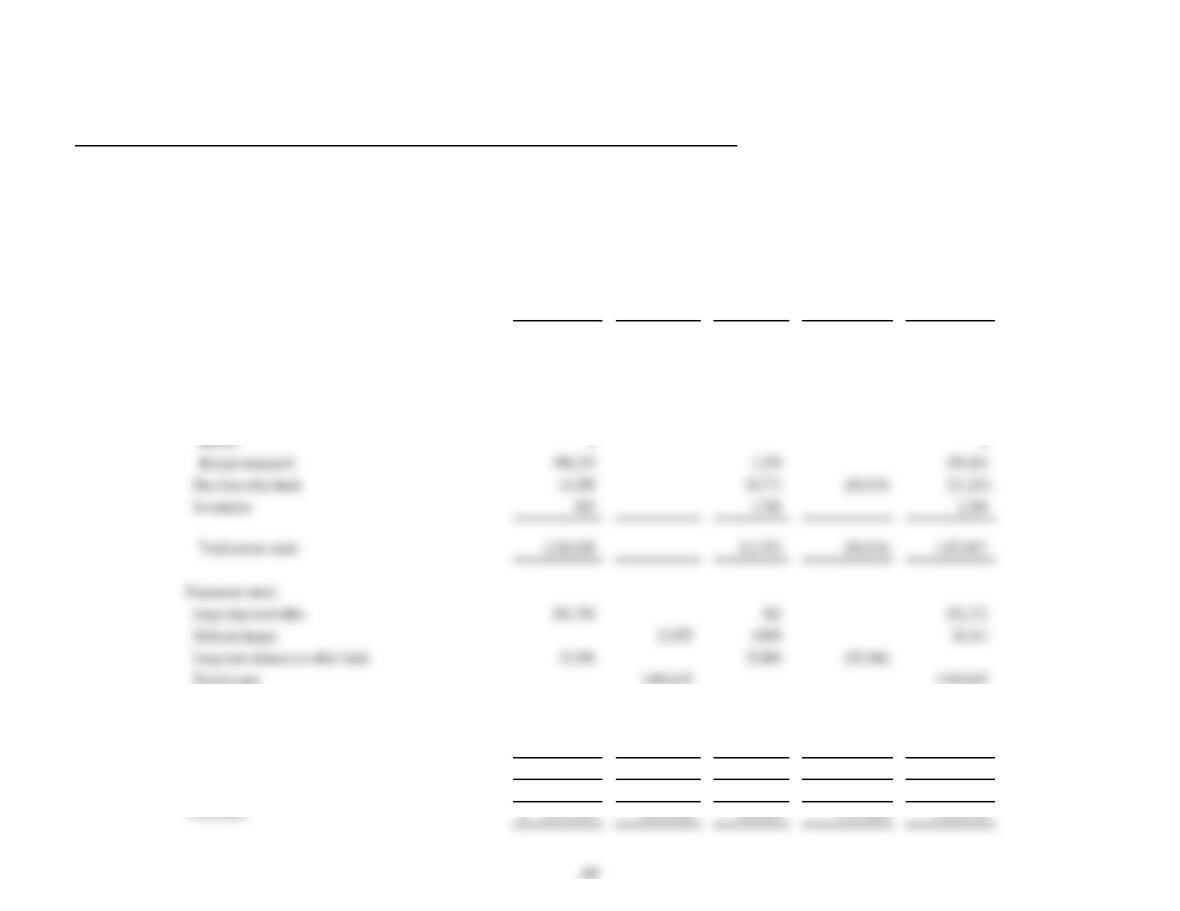

NOTE 2 – RECONCILIATION OF GOVERNMENT-WIDE AND FUND FINANCIAL STATEMENTS

Total fund balances of the County’s governmental funds, $586,174 differs from net assets of governmental activities, $1,510,705, reported financial resources. The

difference primarily results from the long-term economic focus in the statement of net assets versus the current financial resources focus in the governmental fund

balance sheets.

Page 1 of 2

Asset s:

T otal Long-term

Governmental Assets,

Funds Liabilities (1)

Balance Sheet/Statement of Net Assets

Internal

Service

Funds (2)

Reclassifications

and

Eliminations

Statement of

Net Assets

Current assets:

Cash and investments

Receivables, net of allowance for uncollectibles:

Billed

Interest

1,053,197 $

32,292

5

181,048

3,766

1,234,245

36,058

Capit al asset s:

Land and other nondepreciable assets 311,649 28 311,677

Facilities, infrastructure and equipment, net of depreciation 1,462,183 38,968 1,501,151

Total capital assets 1,773,832 38,996 1,812,828

Total noncurrent assets 215,096 2,834,022 80,147 (59,166) 3,070,099

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Page 2 of 2 Tota l

Governmental

Long–term

Assets,

Internal

Service

Re classi fic ations

and Statement of

Funds Liabilitie s (1) Funds (2) Elimina tions N et Assets

Li abiliti es:

Current li abiliti es:

Warrants payable 11,973 $ 5,896 17,869

Accrued liabilities 92,975 18,993 111,968

Tax and revenue anticipation notes 440,000 440,000

Intergovernmental payable 98,353 7,353 105,706

Compensated absences 82,669 16,932 99,601

Other post employment benefits 4,343 991 5,334

Long-term advances from other funds 43,096 15,579 (59,166) (491)

Tota l nonc urrent liabi litie s 43,096 2,009,452 154,044 (59,166) 2,147,426

Total liabilities 955,750 1,954,923 247,418 (147,680) 3,010,411

Rest ric ted fo r :

Debt service (287,430) 446,212 158,782

Capital projects (57,891) 118,467 60,576

Fire protection 1,544 1,544

Health programs 15,032 218,480 233,512

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

(a) Explanation of certain differences between the governmental funds balance sheet and the government-wide statement of net assets

(1)

Cost of capital assets

Accumulated depreciation

When capital assets (land, infrastructure, building, and equipment) that are to be used in governmental

activities are purchased or constructed, the costs of those assets are reported as expenditures in

governmental funds. However, the statement of net assets includes those capital assets among the assets of

the County as a whole.

$ 4,011,203

(2) Internal service funds are used by management to charge the costs of certain activities, related to public

works, general services, self–insurance, regional communications and office of communications and