COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

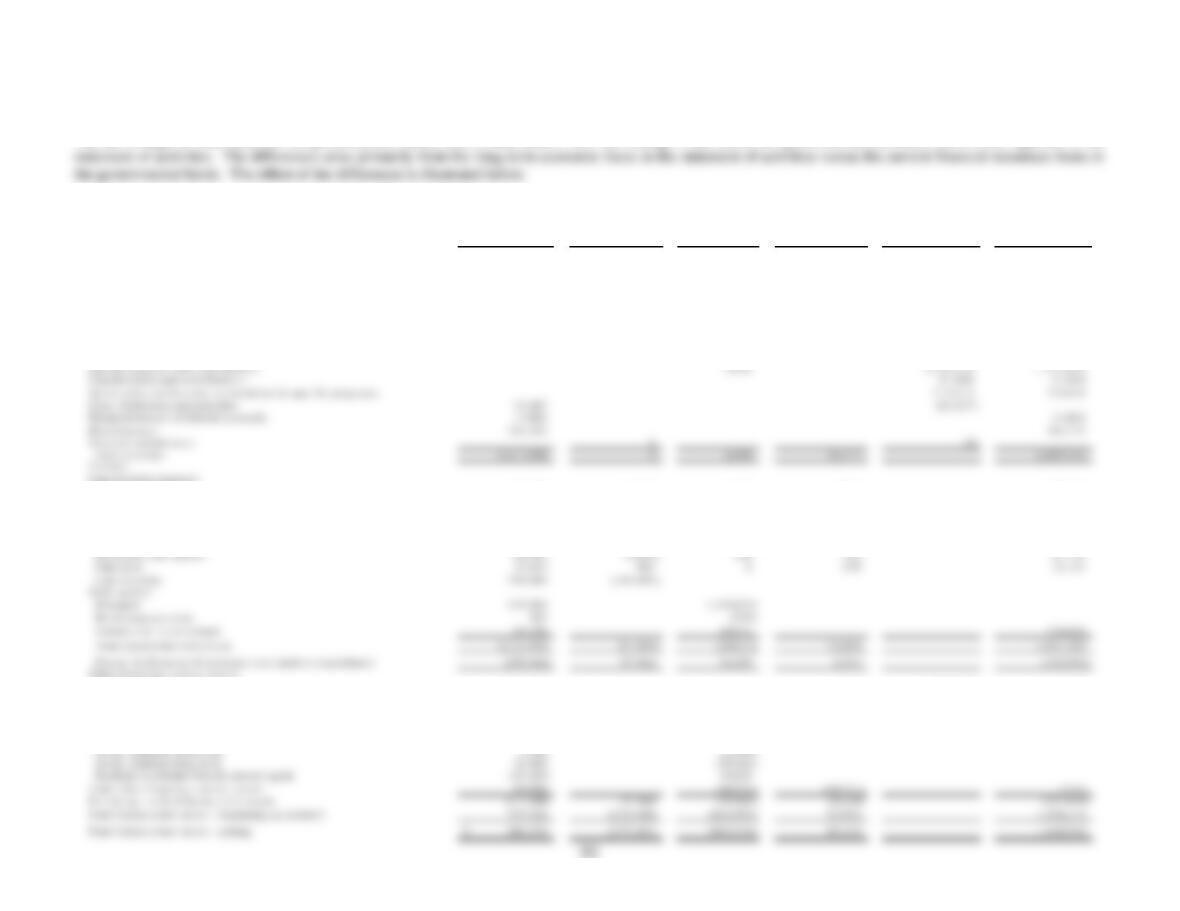

The net change in fund balances for governmental funds, $(211,140), differs from the change in net assets for governmental activities, $(187,438) reported in the

Statement of Revenues, Expenditures and Changes in Fund Balances/Statement of Activities

Tota l Ca pita l- L ong–ter m In ter n al Re cla ssifi cat ions

G ov er nm en ta l Rel ated Revenues, Se rv ic e and St atem e n t of

Fund s Ite m s (3) E xp en se s (4 ) Fu n ds ( 5 ) Eli mi n atio n s Ac tivities

Revenue s:

Taxes:

Property $ 475,629 475,629

Sal es / use 69,225 69,225

Transie nt oc cu p an c y 5,311 5,311

Use of m o ne y a n d pr o p ert y 4 9 ,10 8 696 49,804

Li censes and permit s 41,762 (41,762)

In te rg o ve rn m en ta l 1,419,783 10,682 1,069 (1,431,534)

Charges for sales and se rvic es 197,378 (9,219) 74,452 80,790 343,401

General government 171,945 2,132 2,146 9,740 185,963

Public a ssistance 689,891 362 4,279 9,884 704,416

Pu blic p r o tec tio n 683,099 13,302 16,631 31,040 744,072

He alth a nd sa n itati on 681,774 26,347 7,605 8,940 724,666

Public ways and facilities 102,254 10,056 (1,531) 13,220 123,999

Transf er s i n 174,740 263 (174,767) 236

Transf er s o u t (156,475) (11,014) 174,767 7,278

Issuance of debt 80,006 (80,006)

Refunding debt issued 49,760 (49,760)

Swap, Lehmen termination payment (23,019) 23,019

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

(b) Explanation of certain differences between the governmental funds statement of revenues, expenditures, and changes in fund balances and the government-wide

statement of activities.

(3)

When capital assets that are to be used in governmental activities are purchased or constructed, the resources expended for those assets are reported as

expenditures in governmental funds. However, in the statement of activities, the cost of those assets is allocated over their estimated useful lives and

re

p

orted as de

p

reciation ex

p

ense. As a result, fund balance decreases b

y

the amount of financial resources ex

p

ended, whereas net assets decrease b

y

the

de

This is the amount amortized during the year. $ (934)

Bond issuance costs are expended in governmental funds when paid, and are capitalized and amortized over the life of the corresponding bonds for

purposes of the statement of activities. This amount is the net between bond issuance costs ($335) incurred and amortization for the year $1,059 . (724)

Repayment of bond principal is reported as an expenditure in the governmental funds and, thus, has the effect of reducing fund balance because current

53

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Bon

which are expended within the funds statements. (71,735)

Change in compensated absences

Change in Other post employment benefits (OPEB)

Some expenses reported in the statement of activities do not require the use of current financial resources and therefore are not reported as expenditures

in governmental funds.

(5,628)

(872)

communications and office of communications and technology to individual funds. The adjustments for internal service funds close those funds by

charging additional amounts to participating governmental activities to completely cover the internal service funds‘ costs for the year. $ (8,420)

54

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

NOTE 3 – BUDGETARY PRINCIPLES

As required by the laws of the State of California, the County prepares and legally adopts a final balanced operating budget on or before August 30 of each fiscal year.

The Board may, by resolution, extend on a permanent basis or for a limited period, the date from August 30 to October 2. Due to the uncertainty of State budget

impacts, on September 3, 2008 the Board of Supervisors approved by resolution to extend the date of the final adoption of the County’s Fiscal Year 2008-2009 Budget

Resolutions until sixty days after the adoption of the California State Budget, which occurred on September 23, 2008. The final budget for fiscal year 2008-09 was

adopted on November 12, 2008. Until the adoption of a final balanced budget, operations were governed by the proposed budget approved by the Board of Supervisors

on June 10, 2008. Public hearings were conducted on the proposed final budget to review all appropriations and the sources of financing. Because the final budget must

be balanced, any shortfall in revenue requires an equal reduction in financing requirements.

Operating budgets are adopted for the General Fund, special revenue funds, debt service funds, and capital projects funds on the modified accrual basis of accounting.

Budgetary control and the legal level of control are at the budget unit and object level, which classifies expenditures by organizational unit, and by type of goods

purchased and services obtained. The statement/schedules of revenues and expenditures – budget and actual presents revenues at the source level and expenditures at

the function level.

modified accrual basis of accounting.

NOTE 4 – CASH, INVESTMENTS, AND RESTRICTED ASSETS

All investments are reported on the statement of net assets/balance sheet in accordance with GASB Statement No. 31, at fair value, except for the investment

agreement(s) which are carried at cost. The County maintains two cash and investment pools. The primary cash and investment pool (Treasurer’s Pool) is available for

use by all funds. The portion of this pool applicable to each fund type is displayed on the statements of net assets/balance sheets as “cash and investments.” The share

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

in the Treasurer’s Pool. (A separately issued report of County Treasurer’s Internal and External Pools is available at

http://www.finance.saccounty.net/Investments/RptQuarterly.asp

Cash and investments held by fiscal agents are restricted as to its use. It includes funds for the construction/acquisition of plant and equipment and funds designated by

b. Credit risk

c. Custodial credit risk

d. Concentration of credit risk

Specific restrictions of investment are noted below:

Section 53601 lists the investments in which the Treasurer may purchase. These include bonds issued by the County; United States Treasury notes, bonds, bills or

receivable backed bonds, not to exceed maturity of five years, subject to the credit rating of the issuer and not to exceed 20% of the portfolio; shares of beneficial

interest issued by a joint powers authority organized pursuant to Section 6509.7 that invests in the securities and obligations authorized previously.

56

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

In addition to the restrictions and guidelines cited in the Government Code, the County Board of Supervisors annually adopts an “Annual Investment Policy for the

Pooled Investment Fund” (The Policy). The Policy is prepared by the Department of Finance and is based on criteria cited in the Government Code. The Policy adds

further specificity to investments permitted, reducing concentration within most permitted investment types and reducing concentration of investments with any broker,

dealer or issuer.

Credit Risk – This is the risk that an issuer or other counterparty to a debt instrument will not fulfill its obligations. The County is permitted to hold investments of

issuers with a short term rating of superior capacity and a minimum long term rating of upper medium grade by the top two nationally recognized statistical rating

organizations (rating agencies). For short-term rating, the issuers’ rating must be A-1 and P-1, and the long-term rating must be A- and A3, respectively by Standard &

Poor’s and Moody’s rating agencies. In addition, the County is permitted to invest in the State’s Local Agency Investment Fund, collateralized certificates of deposits

55.5% of total investments at year-end are in U.S. Government and Agency securities, there is no limitation on amounts invested in these types of issues, and 18.6% of

the portfolio is invested in commercial paper or guaranteed investment contracts. As of June 30, 2009, more than 5% of the portfolio is invested as shown below:

Federal Farm Credit Bank/FFCB Discount notes $ 221,723

Federal Home Loan Banks/FHLB Discount notes 868,822

Federal National Mortgage Association/FNMA Discount notes 707,081

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

The following schedule indicates the credit and interest rate risk at June 30, 2009. For purposes of this schedule, NR is defined as not rated. The credit ratings listed

are for Standard and Poor’s and Moody’s Investor Services, respectively. Guaranteed investment contracts are subject to the credit rating disclosure requirements but

Imprest cash

are normally unrated.

Credit

Rat ing

Under 30

Days

31-180

Days

181-365

Days

Maturity

1-5

Years

Over 5

Years

$

Fair Value

337

Cash in banks 837

Federal National Mortgage Association Discount Notes

FHLB Discount Notes

FHLMC Discount Notes

FHLMC

Commercial paper

Negotiable certificates of deposit

P-1/A-1+

P-1/A-1+

P-1/A-1+

Aaa/AAA

P-1/A-1+

P-1/A-1+

394,000

183,142

167,170

4,999

25,003

137,934

244,923

167,709

3,885

122,944

141,223

2,662

10,069

20,359

40,200

109,238

534,596

438,134

334,879

133,482

127,943

Total investments held by fiscal agents 39,567 39,567

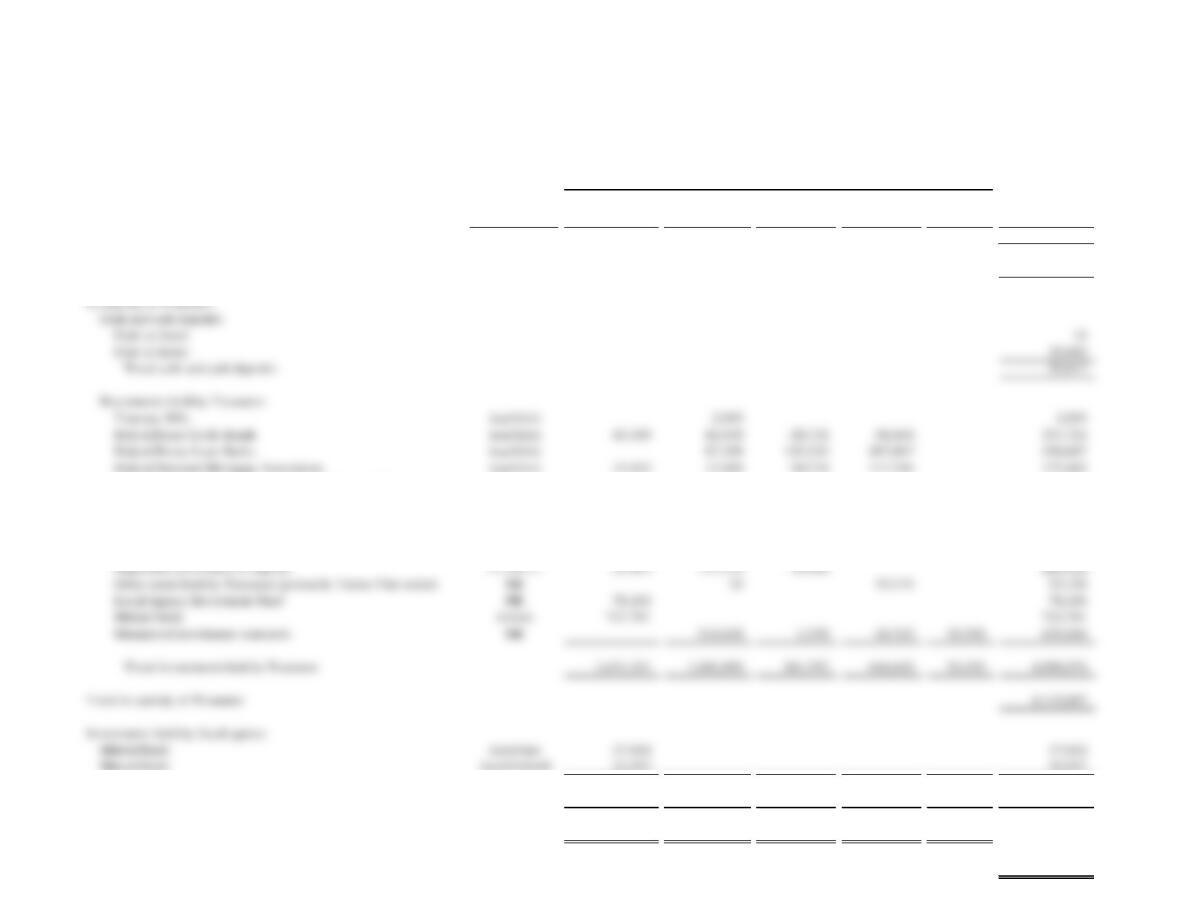

T otal investments 1$ ,670,898 1,498,993 261,792 644,602 53,352

T otal cash, investments, and rest ricted asset s

58

4,156,628 $

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

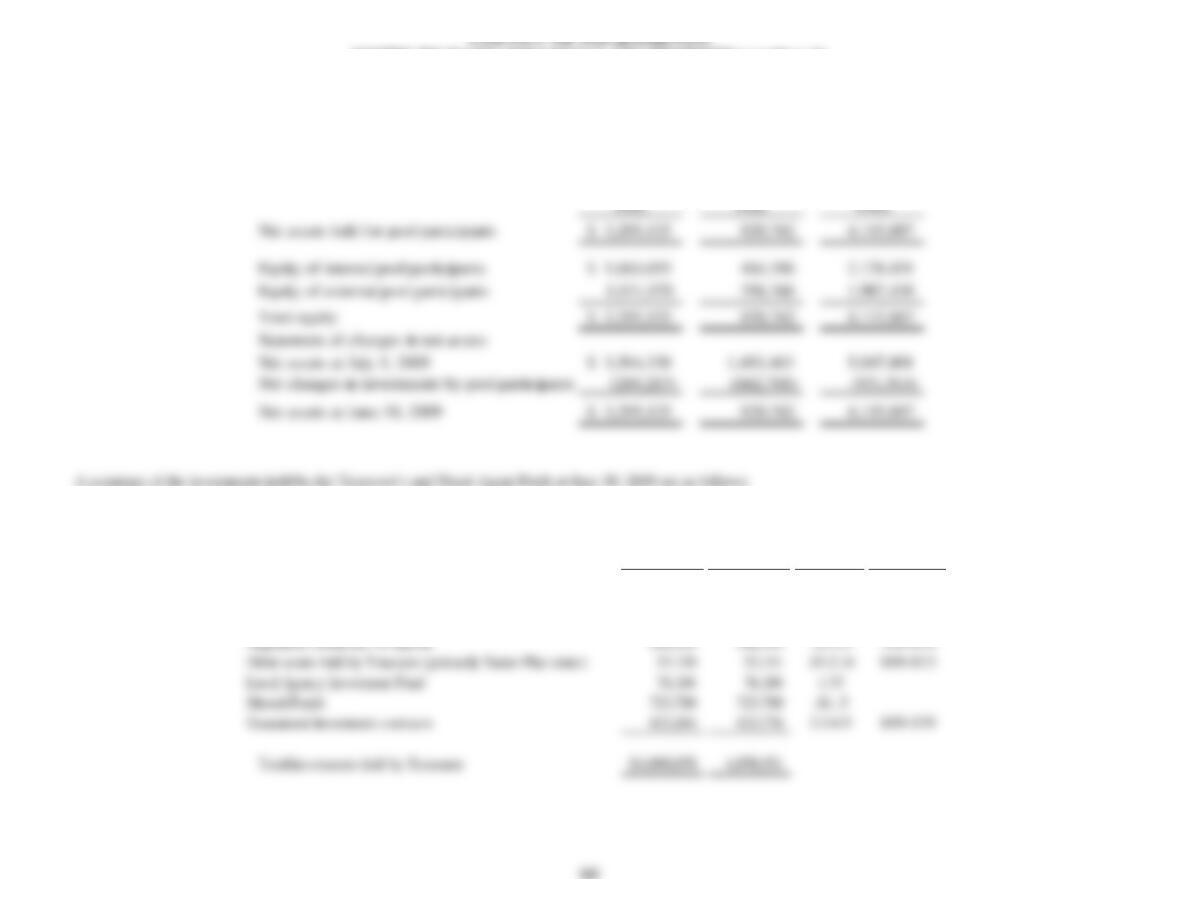

The County did not participate in any security lending transactions or enter into any reverse repurchase agreements during FY 2008-09. The County’s investment with

the State’s Local Agency Investment Fund (LAIF) is $76,104; this investment is included in the State’s Pooled Money Investment Account (a separately issued report of

LAIF is available at http://www.treasurer.ca.gov/pmia-laif/index.asp). As of June 30, 2009 the total amount invested by all public agencies in the State’s Pooled Money

Investment Account is $51.0 billion. Of that $51.0 billion managed by the State Treasurer, 100 percent is invested in non-derivative financial products. The Pooled

Money Investment Accrual Portfolio has not invested in, nor will it invest in Derivative Products as defined in FASB 133. The average maturity of PMIA investments

was 235 days as of June 30, 2009. The Local Investment Advisory Board (Board) has oversight responsibility for LAIF. The Board consists of five members as

designated by state statute. The value of the pool shares in LAIF, which may be withdrawn, is determined on an amortized cost basis, which is different than the fair

value of the County’s portion in the pool.

Cash, investments, and restricted assets as shown on the basic financial statements at June 30, 2009, are as follows:

Government–wide statement of net assets:

Cash and investments

Restricted assets, included in current assets

$ 1,502,636

57,612

394,172

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

The following are condensed statements of net assets and changes in net assets for the Treasurer’s Pool and Fiscal Agent Pool at June 30, 2009:

Statement of net assets Treasurer’s Fiscal Agent

Interest

Rate Maturity

Fair Value Cost Range (%) Range

Government securities $ 2,268,982 $ 2,249,392 .13-7.4 7/09-5/14

Commercial paper 127,944 127,949 .19-.45 7/09-8/09

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

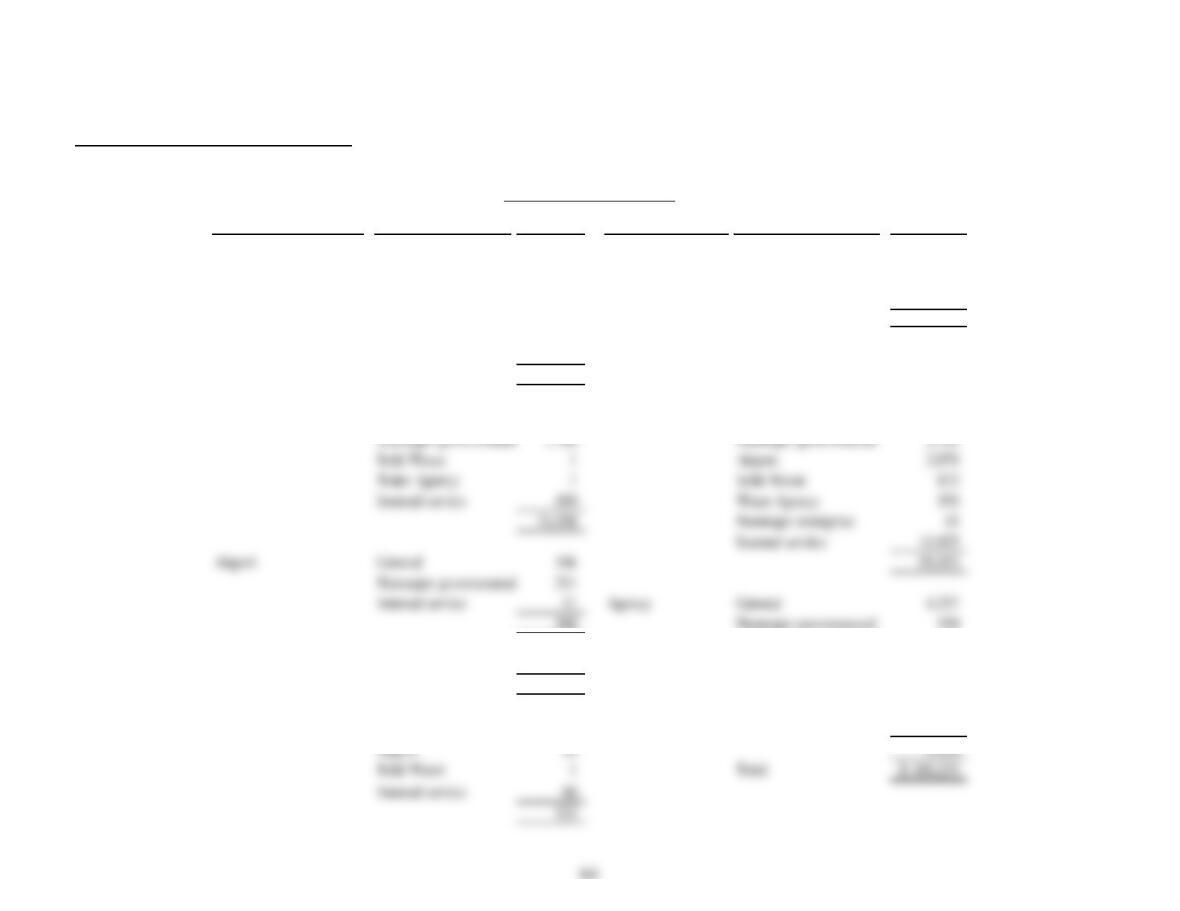

NOTE 5 – LONG-TERM RECEIVABLES

Governmental funds report deferred revenues in connection with receivables for revenues not expected to be collected within one year per GASB 33. Governmental

and enterprise funds also defer revenue recognition in connection with resources that have been received as of year-end, but not yet earned.

Nonmajor T otal

$ 23,306 23,306

Deferred revenue and unearned revenue reported were as follows:

Unavailable Unearned T otal

Governmental Activities:

Gen eral Fun d

Internal Service Funds 2,923 2,923

Swap premiums 26,234 26,234

T otal Governmental Activities 60,065 60,065

Business-type act ivit ies:

Airport 1,053 1,053

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

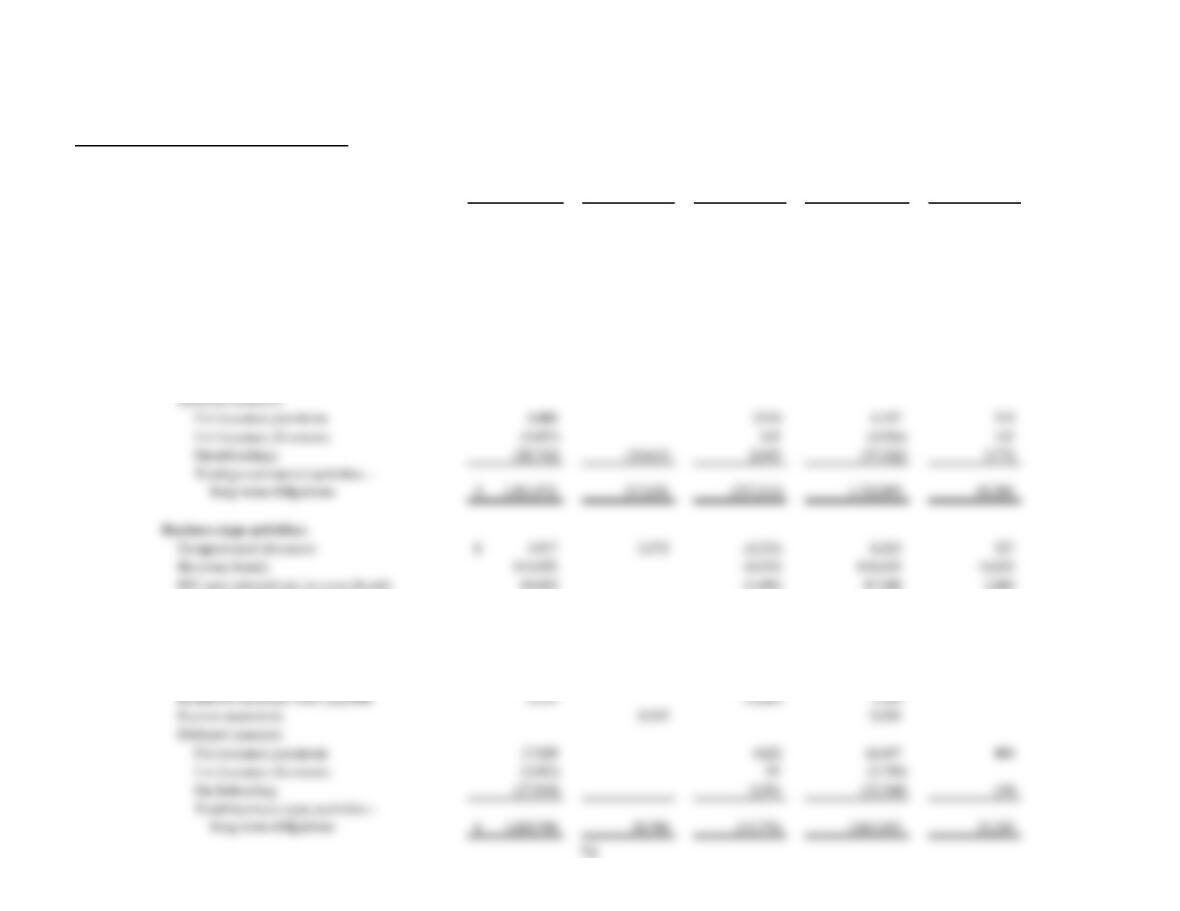

NOTE 6 – CAPITAL ASSETS

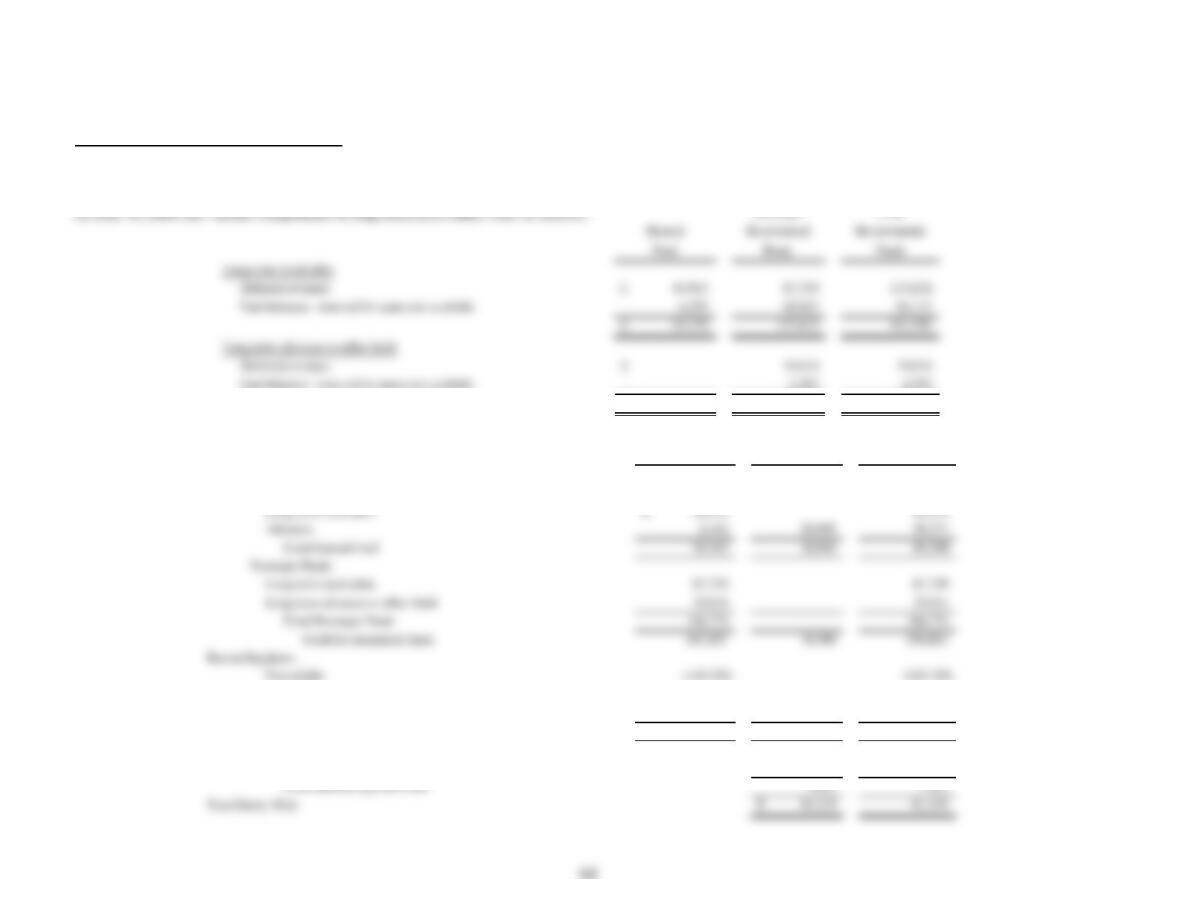

Capital assets activity for the year ended June 30, 2009, is as follows:

Restated

Balance Balance

June 30, 2008 Additions Deletions June 30, 2009

Gove rn m e n tal a cti vi ti e s :

Capital assets, not being depreciated:

Land $ 110,377 2,950 (214) 113,113

Equipment (198,073) (23,289) 17,878 (203,484)

Total accumulated depreciation (2,316,770) (90,093) 18,978 (2,387,885)

Total capital assets, being depreciated, net 1,438,490 64,913 (2,252) 1,501,151

Sub-total governmental activities $ 1,760,980 123,428 (71,580) 1,812,828

Business–type activities:

Less accumulated depreciation for:

Buildings and improvements (273,516) (31,085) 170 (304,431)

Water facility rights (1,494) (308) (1,802)

Infrastructure (13,775) (2,441) (16,216)

Equipment (52,289) (7,730) 3,673 (56,346)

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Depreciation expense and amortization was charged to functions/programs of the primary government as follows:

Governmental activities:

Depreciation

Expense

General government $8,405

Public assistance 525

Public protection 13,237

Health and sanitation 3,269

Water Agency 8,316

County Transit

Total depreciation expense – business–type activities $

134

41,564

63

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

NOTE 7 – INTERFUND TRANSACTIONS

The following summarizes interfund receivables and payables, advances to / from other funds, and transfers as of and for the year ended June 30, 2009:

Due From / To Other Funds

Receivable Fund Payable Fund Amount Receivable Fund Payable Fund Amount

General Nonmajor governmental

Airport

Solid Waste

$ 13,378

949

4,708

Nonmajor enterprise General

Nonmajor governmental

Internal service

36

3

8

Water Agency

Nonmajor enterprise

1

12

47

Internal service 7,152

26,200

Nonmajor governmental General 14,106 Internal service General 36,279

Airport 321

Solid Was te Internal service 215 Solid Waste 1

215 Water Agency 11

Nonmajor enterprise 10

Water Agency Nonmajor governmental 2

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Amounts due the General Fund are related to: 1) Principal and interest due from Public Facilities Fixed Asset Financing Program (nonmajor governmental), 2) To

fund community services activities pending reimbursement from federal, state and local government, 3) Sheriff security & Department of Environmental Review

and Assessment services provided to the Airports, and 4) Reimbursement due from Liability/Property Internal Service Fund for the final quarter of the fiscal year

ending June 30, 2009.

Amounts due the nonmajor governmental funds are a result of: 1) Transactions to repay the Public Facilities Fixed Asset Financing Program for year end

purchases, 2) Teeter excess, net penalty and interest revenue remaining after debt service interest costs are paid.

Total $ 59,166

Amounts advanced from nonmajor governmental funds are related to the Fixed Asset Financing Program which has financed $19,014 for major capital projects

(General Fund), major bulk automobile purchases (internal service and enterprise funds) and $4,292 were advances to the general fund. Amounts advanced from

internal service funds, $38,860 related to General fund advances. The advances were needed due to the decrease in revenues attributed to the economic recession.

The advances will be repaid within five years by the General Fund beginning in fiscal year 2010/11.

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Transfers From / To Other Funds

Between funds within governmental activities:

Transfer From Transfer To

General Nonmajor governmental

Nonmajor governmental General

$

Amount

82,549

32,909

Transfer to cover debt service payments, economic

development and community development programs

Transfers for Transient Occupancy Taxand Teeter Property

Tax

Nonmajor governmental Nonmajor governmental

40,754

Transfer to cover debt service payments and capital project

Total $ 175,003

66

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

NOTE 8 – LEASES

Lease Obligations

During the year ended June 30, 2008, the County entered into the following capital lease agreements:

For energy conservation improvements and replacement of obsolete mechanical equipment at various county buildings entered into a 15 year lease in the amount of

$1,240, interest rate of 4.66 percent and annual lease payments of $115 through 2022.

For energy conservation improvements and replacement of obsolete mechanical equipment at various county buildings entered into a 15 year lease in the amount of

$1,088, interest rate of 4.66 percent and annual lease payments of $101 through 2022; lease was cancelled December 2008.

For energy conservation improvements and replacement of obsolete mechanical equipment at various county buildings entered into a 15 year lease in the amount of

2010.

Sunrise Recreation and Park District for an office trailer in the amount of $131 with an interest rate of 10.0 percent and annual lease payments of $30 through

November 2010.

67

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS (continued)

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

During the year ended June 30, 2006, the County of Sacramento entered into a capital lease agreement for an energy conservation retro fit project in the amount of $837

with an interest rate of 4.30 percent per annum and semi-annual lease payments of $22 through September 2017.

As of June 30, 2009, the future minimum lease payments under capital leases are as follows:

Capital Lease Agreements

Year ending June 30 County

2010 $ 1,756

2011 1,756

2012 1,274

2013 1,274

2014 1,201

Structures and improvements 12,779

Equipment 1,539

14,991

Less: Accumulated depreciation

Structures and improvements $ (1,856)

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

The County also leases buildings and equipment under operating leases, some of which contain escalation clauses. Future minimum non-cancelable operating lease

payments for governmental and proprietary fund types as of June 30, 2009, are as follows:

Operating Leases Commitment

Year Ending June 30 Governmental Proprietary

2010 $ 35,491 1,615

2011 32,531 912

2012 29,582 862

The Airport System derives a substantial portion of its revenues from charges to air carriers and concessionaires. Substantially all of the assets classified under capital

assets in the Statement of Net Assets for the Airport are held for the purpose of rental or related use.

The Airport System, as lessor, leases land, buildings and terminal space to air carriers and concessionaires on a fixed fee as well as a contingent basis. All leases of the

Airport System are treated as operating leases for accounting purposes. Most of the leases provide for an annual review and re-determination of the rental amounts.

In fiscal year 2009 the Airport System received approximately $3,241, for contingent rental payments in excess of stated minimums. The following is a schedule of

future minimum rentals receivable on non-cancelable operating leases as of June 30, 2009.

2025-2029 3,160

2030-2034 1,368

2035-2039 410

Total future minimum rentals receivable $ 86,315

69

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

NOTE 9 – SHORT–TERM DEBT ACTIVITY

The County issues tax and revenue anticipation notes in advance of property tax and other revenue collections. The notes are issued to supplement County cash flows

until taxes and other revenues are collected.

Short-term debt activity for the year ended June 30, 2009 was as follows:

70

COUNTY OF SACRAMENTO

NOTES TO BASIC FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2009

(amounts expressed in thousands)

Amounts

Balance Balance Due Within

July 1, 2008 Additions Retirements June 30, 2009 One Year

Governmental activities:

Compens ated absences $ 100,197 94,117 (88,215) 106,099 6,498

Certificates of participation 340,480 (15,305) 325,175 16,885

Teeter notes 51,335 80,006 (81,541) 49,800 11,635

Pension obligation bonds 960,926 49,760 (66,048) 944,638 13,185

Revenue bonds 350,627 (5,485) 345,142 1,620

Accreted Interest 5,801 1,929 7,730

OPEB Liablility 4,370 964 5,334

Other long-term debt 3,615 1,475 5,090 5,090

Capital leas e obligations 13,933 (2,747) 11,186 1,213

Certificates of participation 26,900 (1,895) 25,005 1,960

Reimburs ement agreements 92 4,932 (3,159) 1,865 1,116

Us age fee – City 561 9,569 (1,380) 8,750 847

OPEB Liablility 225 181 406

Water rights – Smud assignment 4,000 4,000

NOTE 10 – LONG-TERM OBLIGATIONS

The following is a summary of long-term obligation transactions for the year ended June 30, 2009: