CFIN6 – CHAPTER 9

INTEGRATIVE PROBLEM SOLUTION

a. Capital budgeting is the process of analyzing additions to fixed assets. Capital budgeting is important

because, more than anything else, fixed asset investment decisions chart a company’s course for the

future. Conceptually, the capital budgeting process is identical to the decision process used by

individuals making investment decisions. These steps are involved:

(2) Assess the riskiness of the cash flows.

(3) Determine the appropriate discount rate, based on the riskiness of the cash flows and the

(5) If the PV of the inflows is greater than the PV of the outflows (the NPV is positive), or if the

calculated rate of return (the IRR) is higher than the project cost of capital, accept the project.

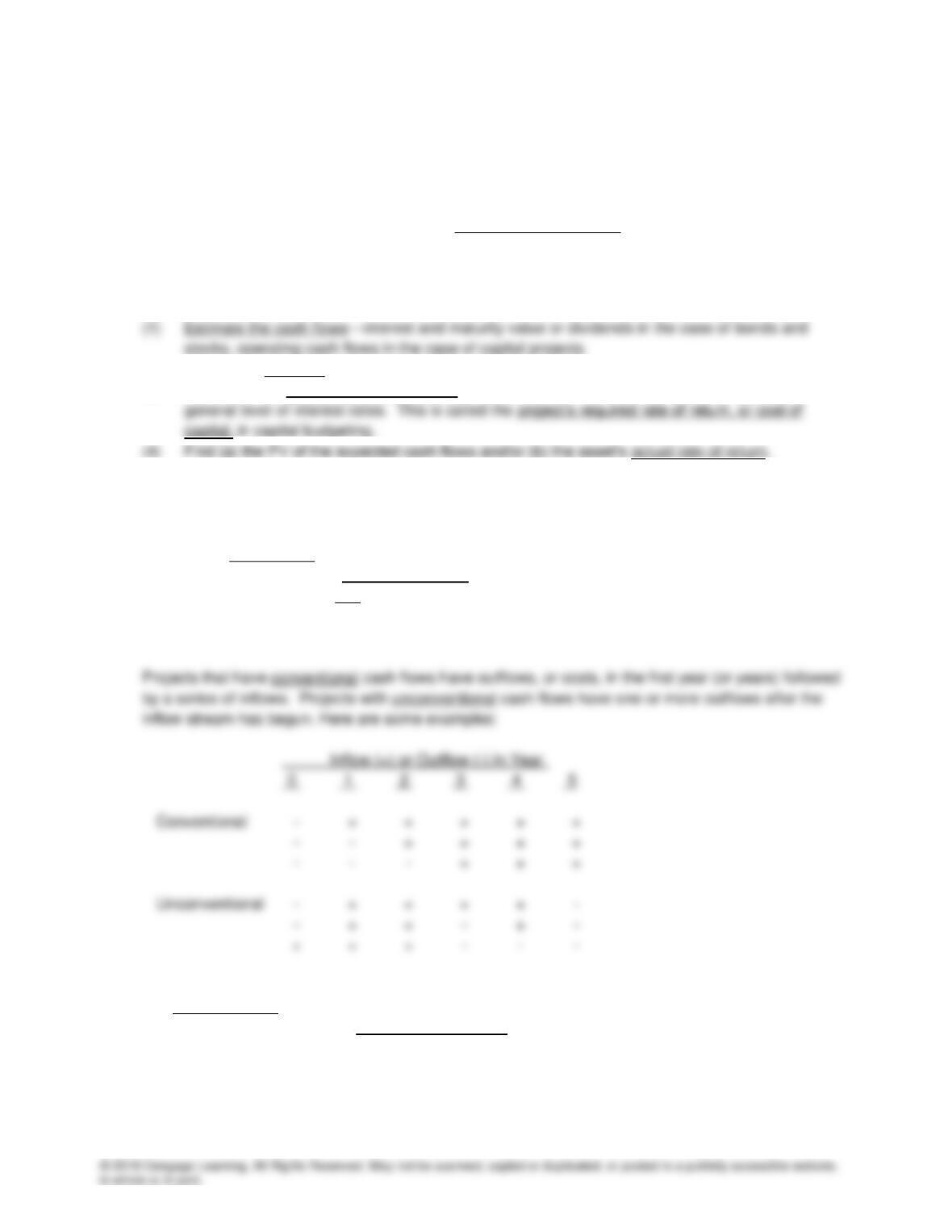

b. Projects are independent if the cash flows of one are not affected by the acceptance of the other.

Conversely, two projects are mutually exclusive if acceptance of one impacts adversely the cash flows

of the other; that is, at most one of two or more such projects can be accepted. Put another way, when

projects are mutually exclusive it means that they do the same job. For example, a forklift truck versus

a conveyor system to move materials, or a bridge versus a ferryboat.

c(1). The payback period is the expected number of years required to recover a project’s cost. We calculate

the payback by developing the cumulative cash flows as shown below for Project F (in thousands of

dollars):

Expected NCF

Year Annual Cumulative

0 ($100) ($100)

1 10 (90)

2 60 (30)

3 80 50

Project F’s $100 investment has not been recovered at the end of Year 2, but it has been more than

recovered by the end of Year 3. Thus, the recovery period is between two and three years. If we

assume that the cash flows occur evenly over the year, then the investment is recovered $30/$80 =

0.375 ≈ 0.4 into Year 3. Therefore, PBF = 2.4 years. Similarly, PBN = 1.6 years.

c(3). Discounted payback is similar to the traditional payback except that discounted rather than

nondiscounted cash flows are used.

Setup for Project F’s discounted payback, assuming a 10% required rate of return:

Expected NCF

Year Annual Discounted Cumulative

0 ($100) ($100.00) ($100.00)

1 10 9.09 ( 90.91)

c(4). The traditional payback measure has two critical deficiencies: (1) It ignores the time value of money,

and (2) it ignores the cash flows that occur after the payback period. Discounted payback does

consider the time value of money, but it still fails to consider cash flows after the payback period;

2 < PB < 3

d(1). The net present value (NPV) is simply the sum of the present values of a project’s cash flows:

.

)

k + (1

CF

=NPV t

t

n

0=t

Project F’s NPV is $18.79:

NPVs are easy to determine using a financial calculator. Enter the cash flows sequentially into the

cash flow registers, with outflows entered as negatives; enter the required rate of return; and then

press the NPV button to obtain the project’s NPV, $18.78 (note the rounding difference). The NPV of

Project N is NPVN = $19.98.

d(2). The rationale behind the NPV method is straightforward: If a project has NPV = $0, then the project

generates exactly enough cash flows (1) to recover the cost of the investment and (2) to enable

$18.79 left over on a present value basis. This $18.79 excess PV belongs to the shareholders—the

debtholders’ claims are fixed—so the shareholders’ wealth will be increased by $18.79 if Project F is

d(3). The NPV of a project is dependent on the required rate of return used. Thus, if the required rate of

return changed, the NPV of each project would change. NPV declines as r increases, and vice versa.

Note that the IRR equation is the same as the NPV equation, except that to find the IRR the equation

is solved for the particular discount rate, IRR, that forces the project’s NPV to equal zero rather than

using the required rate of return (r) in the denominator and finding NPV. Thus, the two approaches

differ in only one respect: In the NPV method, a discount rate is specified (the project’s required rate

of return) and the equation is solved for NPV, whereas in the IRR method, the NPV is specified to

equal zero and the discount rate (IRR) that forces this equality is found.

Project F’s IRR is 18.1%:

Therefore, IRRF = 18.1%.

e(2). The IRR is to a capital project what the YTM is to a bond—it is the expected rate of return on the project,

just as the YTM is the promised rate of return on a bond.

e(3). IRR measures a project’s profitability in the rate of return sense: If a project’s IRR equals its required

rate of return, then its cash flows are just sufficient to provide investors with their required rates of

return. An IRR greater than r implies an economic profit, which accrues to the firm’s shareholders,

Projects’ IRRs are compared to their required rates of return, or costs of capital, which are the projects’

hurdle rates. Because Projects F and N both have a hurdle rate of 10%, and because both have IRRs

greater than that hurdle rate, both should be accepted if they are independent. However, if they are

mutually exclusive, Project N would be selected, because it has the higher NPV.

e(4). IRRs are independent of the required rate of return. The IRR gives the return that would be earned if a

f(1). The NPV profiles are plotted in the figure below.

NPV ($)

30

40

50

Crossover point = 8.7%

Note the following points:

(1) The Y-intercept is the project’s NPV when r = 0%. This is $50 for F and $40 for N.

f(2). The NPV profiles show that the IRR and NPV criteria lead to the same accept/reject decision for any

independent project. Consider Project F. It intersects the x-axis at its IRR, 18.1%. According to the IRR

rule, F is acceptable if r is less than 18.1%. Also, at any r less than 18.1%, F’s NPV profile will be

g(1). For projects with conventional cash flow patterns, the NPV profiles will cross only if one project has

both a higher vertical axis intercept and a steeper slope than the other. A project’s vertical axis

intercept typically depends on (1) the size of the project and (2) the size and timing pattern of the cash

g(2). The underlying cause of ranking conflicts is the reinvestment rate assumption. All discounted cash flow

methods implicitly assume that cash flows can be reinvested at some rate, regardless of what actually

g(3). Whether NPV or IRR gives better rankings depends on which has the better reinvestment rate

assumption. Normally, the NPV’s assumption is better. The reason is as follows: A project’s cash

inflows generally are used as substitutes for outside capital, that is, projects’ cash flows replace

outside capital and, hence, save the firm the cost of outside capital. Therefore, in an opportunity cost

sense, a project’s cash flows are reinvested at the required rate of return (cost of capital). To see this

graphically, think of the following situation: Assume the firm’s required rate of return is a constant 10%

within the relevant range of financing considered, and it has projects available as shown in the graph

below:

25

20

15

IRR = 25%

A

IRR = 20%

B

IRR = 15%

C

%

(1) What projects will be accepted, by either NPV or IRR? Answer: A, B, C, and D

(2) If the same situation exists year after year, at what rate of return will cash flows from earlier

years’ investments be reinvested?

ANSWER: Capital budgeting decisions are made in this sequence: (a) The company would say,

h(1). The MIRR is the rate of return that equates a project’s terminal value to the present value of its cash

outflows. Cash inflows are compounded to the end of the project’s life at the firm’s required rate of

return, cash outflows are discounted at the firm’s required rate of return, and then the rate at which

%9.16169.00.1

100

70.159

MIRR

)MIRR1(

70.159

)MIRR1(

)10.1(20)10.1(50)10.1(70

100

3/1

S

3

S

3

S

012

==−

=

+

=

+

++

=

Financial calculator solution: N = 3, PV = -100, PMT = 0, FV = 159.70; compute I/Y = ? = 16.9% =

MIRRN

h(2). The modified IRR has a significant advantage over the traditional IRR measure. MIRR assumes that

cash flows are reinvested at the required rate of return, whereas the traditional IRR measure assumes

h(3). The cash outflows are discounted at the firm’s required rate of return, and the cash inflows are

compounded at the firm’s required rate of return. Thus, the MIRRs would change if the firm’s required

rate of return is changed, because both the present value of the cash outflows and the terminal value

would change.