Chapter 9

Valuing Stocks

9-1. Assume Evco, Inc., has a current price of $50 and will pay a $2 dividend in one year, and its

equity cost of capital is 15%. What price must you expect it to sell for right after paying the

dividend in one year in order to justify its current price?

9-2. Anle Corporation has a current price of $20, is expected to pay a dividend of $1 in one year, and

its expected price right after paying that dividend is $22.

a. What is Anle’s expected dividend yield?

b. What is Anle’s expected capital gain rate?

c. What is Anle’s equity cost of capital?

9-3. Suppose Acap Corporation will pay a dividend of $2.80 per share at the end of this year and $3

per share next year. You expect Acap’s stock price to be $52 in two years. If Acap’s equity cost

of capital is 10%:

a. What price would you be willing to pay for a share of Acap stock today, if you planned to

hold the stock for two years?

b. Suppose instead you plan to hold the stock for one year. What price would you expect to be

able to sell a share of Acap stock for in one year?

c. Given your answer in part (b), what price would you be willing to pay for a share of Acap

stock today, if you planned to hold the stock for one year? How does this compare to your

answer in part (a)?

9-4. Krell Industries has a share price of $22 today. If Krell is expected to pay a dividend of $0.88 this

year, and its stock price is expected to grow to $23.54 at the end of the year, what is Krell’s

dividend yield and equity cost of capital?

9-5. NoGrowth Corporation currently pays a dividend of $2 per year, and it will continue to pay this

dividend forever. What is the price per share if its equity cost of capital is 15% per year?

9-6. Summit Systems will pay a dividend of $1.50 this year. If you expect Summit’s dividend to grow

by 6% per year, what is its price per share if its equity cost of capital is 11%?

9-7. Dorpac Corporation has a dividend yield of 1.5%. Dorpac’s equity cost of capital is 8%, and its

dividends are expected to grow at a constant rate.

a. What is the expected growth rate of Dorpac’s dividends?

b. What is the expected growth rate of Dorpac’s share price?

9-8. Canadian-based mining company El Dorado Gold (EGO) suspended its dividend in March 2016

as a result of declining gold prices and delays in obtaining permits for its mines in Greece.

Suppose you expect EGO to resume paying annual dividends in two years time, with a dividend

of $0.25 per share, growing by 2% per year. If EGO’s equity cost of capital is 10%, what is the

value of a share of EGO today?

9-9. In 2006 and 2007, Kenneth Cole Productions (KCP) paid annual dividends of $0.72. In 2008,

KCP paid an annual dividend of $0.36, and then paid no further dividends through 2012.

Suppose KCP was acquired at the end of 2012 for $15.25 per share.

a. What would an investor with perfect foresight of the above been willing to pay for KCP at

the start of 2006? (Note: Because an investor with perfect foresight bears no risk, use a risk–

free equity cost of capital of 5%.)

b. Does your answer to (a) imply that the market for KCP stock was inefficient in 2006?

9-10. DFB, Inc., expects earnings at the end of this year of $5 per share, and it plans to pay a $3

dividend at that time. DFB will retain $2 per share of its earnings to reinvest in new projects

with an expected return of 15% per year. Suppose DFB will maintain the same dividend payout

rate, retention rate, and return on new investments in the future and will not change its number

of outstanding shares.

a. What growth rate of earnings would you forecast for DFB?

b. If DFB’s equity cost of capital is 12%, what price would you estimate for DFB stock today?

c. Suppose DFB instead paid a dividend of $4 per share at the end of this year and retained

only $1 per share in earnings. If DFB maintains this higher payout rate in the future, what

stock price would you estimate now? Should DFB raise its dividend?

9-11. Cooperton Mining just announced it will cut its dividend from $4 to $2.50 per share and use the

extra funds to expand. Prior to the announcement, Cooperton’s dividends were expected to grow

at a 3% rate, and its share price was $50. With the new expansion, Cooperton’s dividends are

expected to grow at a 5% rate. What share price would you expect after the announcement?

(Assume Cooperton’s risk is unchanged by the new expansion.) Is the expansion a positive NPV

investment?

9-12. Proctor and Gamble paid an annual dividend of $1.72 in 2009. You expect P&G to increase its

dividends by 8% per year for the next five years (through 2014), and thereafter by 3% per year.

If the appropriate equity cost of capital for Proctor and Gamble is 8% per year, use the

dividend-discount model to estimate its value per share at the end of 2009.

Since dividends are growing at the cost of capital over the next 5 years, the present value of the next 5

years’ dividends are:

Discounting this value to the present gives

9-13. Colgate-Palmolive Company has just paid an annual dividend of $1.50. Analysts are predicting

dividends to grow by $0.12 per year over the next five years. After then, Colgate’s earnings are

expected to grow 6% per year, and its dividend payout rate will remain constant. If Colgate’s

equity cost of capital is 8.5% per year, what price does the dividend-discount model predict

Colgate stock should sell for today?

PV of the first 5 dividends:

PV of the remaining dividends in year 5:

Discounting back to the present

9-14. What is the value of a firm with initial dividend Div, growing for n years (i.e., until year n + 1) at

rate g1 and after that at rate g2 forever, when the equity cost of capital is r?

9-15. Halliford Corporation expects to have earnings this coming year of $3 per share. Halliford plans

to retain all of its earnings for the next two years. For the subsequent two years, the firm will

retain 50% of its earnings. It will then retain 20% of its earnings from that point onward. Each

year, retained earnings will be invested in new projects with an expected return of 25% per year.

Any earnings that are not retained will be paid out as dividends. Assume Halliford’s share count

remains constant and all earnings growth comes from the investment of retained earnings. If

Halliford’s equity cost of capital is 10%, what price would you estimate for Halliford stock?

See the spreadsheet for Halliford’s dividend forecast:

138 Berk/DeMarzo, Corporate Finance, Fourth Edition

From year 5 on, dividends grow at constant rate of 5%. Therefore,

9-16. Suppose Amazon.com Inc. pays no dividends but spent $3 billion on share repurchases last year.

If Amazon’s equity cost of capital is 8%, and if the amount spent on repurchases is expected to

grow by 6.5% per year, estimate Amazon’s market capitalization. If Amazon has 450 million

shares outstanding, what stock price does this correspond to?

9-17. Maynard Steel plans to pay a dividend of $3 this year. The company has an expected earnings

growth rate of 4% per year and an equity cost of capital of 10%.

a. Assuming Maynard’s dividend payout rate and expected growth rate remains constant, and

Maynard does not issue or repurchase shares, estimate Maynard’s share price.

b. Suppose Maynard decides to pay a dividend of $1 this year and use the remaining $2 per

share to repurchase shares. If Maynard’s total payout rate remains constant, estimate

Maynard’s share price.

c. If Maynard maintains the same split between dividends and repurchases, and the same

payout rate, as in part (b), at what rate are Maynard’s dividends, earnings per share, and

share price expected to grow in the future?

9-18. Benchmark Metrics, Inc. (BMI), an all-equity financed firm, reported EPS of $5.00 in 2008.

Despite the economic downturn, BMI is confident regarding its current investment

opportunities. But due to the financial crisis, BMI does not wish to fund these investments

externally. The Board has therefore decided to suspend its stock repurchase plan and cut its

dividend to $1 per share (vs. almost $2 per share in 2007), and retain these funds instead. The

firm has just paid the 2008 dividend, and BMI plans to keep its dividend at $1 per share in 2009

as well. In subsequent years, it expects its growth opportunities to slow, and it will still be able to

fund its growth internally with a target 40% dividend payout ratio, and reinitiating its stock

repurchase plan for a total payout rate of 60%. (All dividends and repurchases occur at the end

of each year.)

Suppose BMI’s existing operations will continue to generate the current level of earnings per

share in the future. Assume further that the return on new investment is 15%, and that

reinvestments will account for all future earnings growth (if any). Finally, assume BMI’s equity

cost of capital is 10%.

a. Estimate BMI’s EPS in 2009 and 2010 (before any share repurchases).

b. What is the value of a share of BMI at the start of 2009?

9-19. Heavy Metal Corporation is expected to generate the following free cash flows over the next five

years:

After then, the free cash flows are expected to grow at the industry average of 4% per year.

Using the discounted free cash flow model and a weighted average cost of capital of 14%:

a. Estimate the enterprise value of Heavy Metal.

b. If Heavy Metal has no excess cash, debt of $300 million, and 40 million shares outstanding,

estimate its share price.

9-20. IDX Technologies is a privately held developer of advanced security systems based in Chicago.

As part of your business development strategy, in late 2008 you initiate discussions with IDX’s

founder about the possibility of acquiring the business at the end of 2008. Estimate the value of

IDX per share using a discounted FCF approach and the following data:

■ Debt: $30 million

■ Excess cash: $110 million

■ Shares outstanding: 50 million

■ Expected FCF in 2009: $45 million

■ Expected FCF in 2010: $50 million

■ Future FCF growth rate beyond 2010: 5%

■ Weighted-average cost of capital: 9.4%

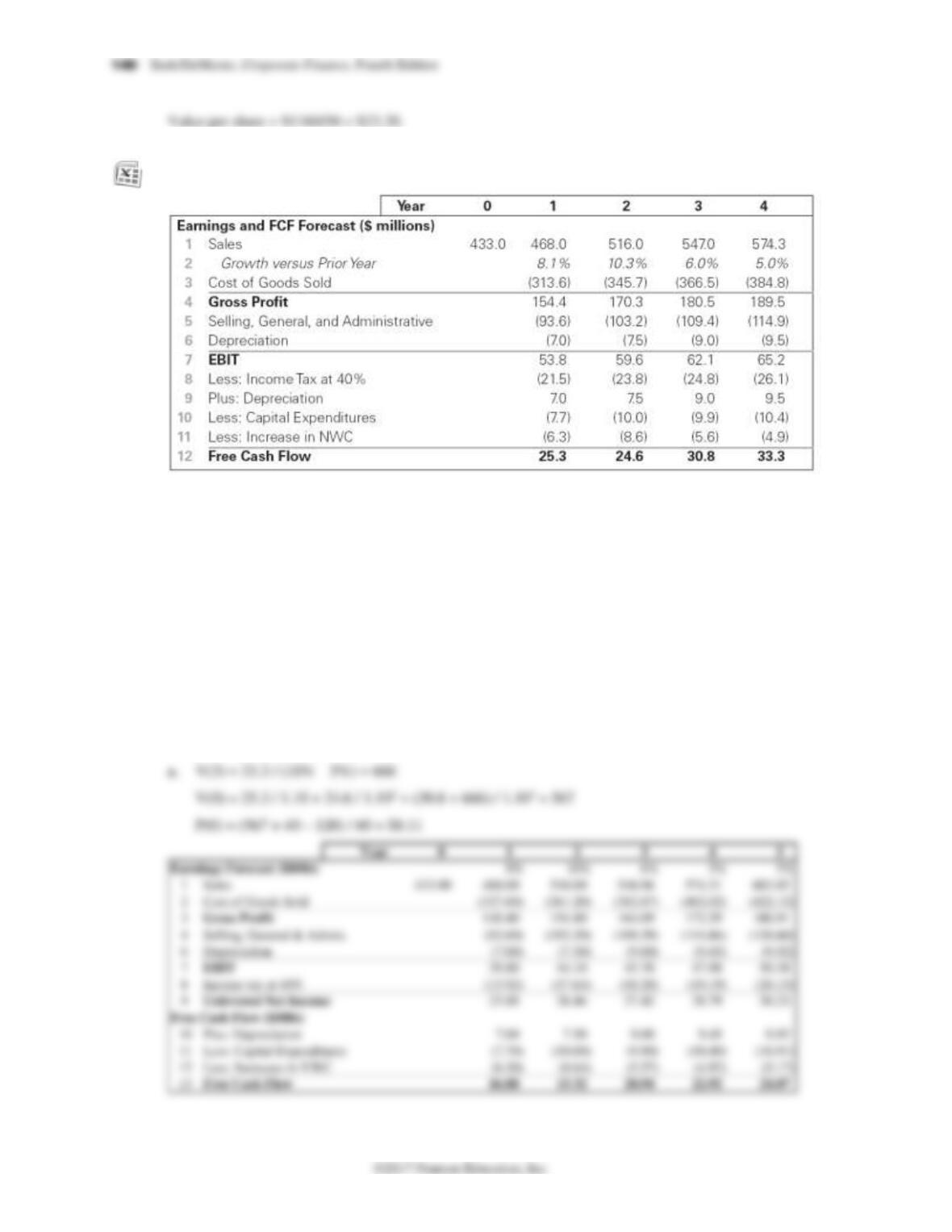

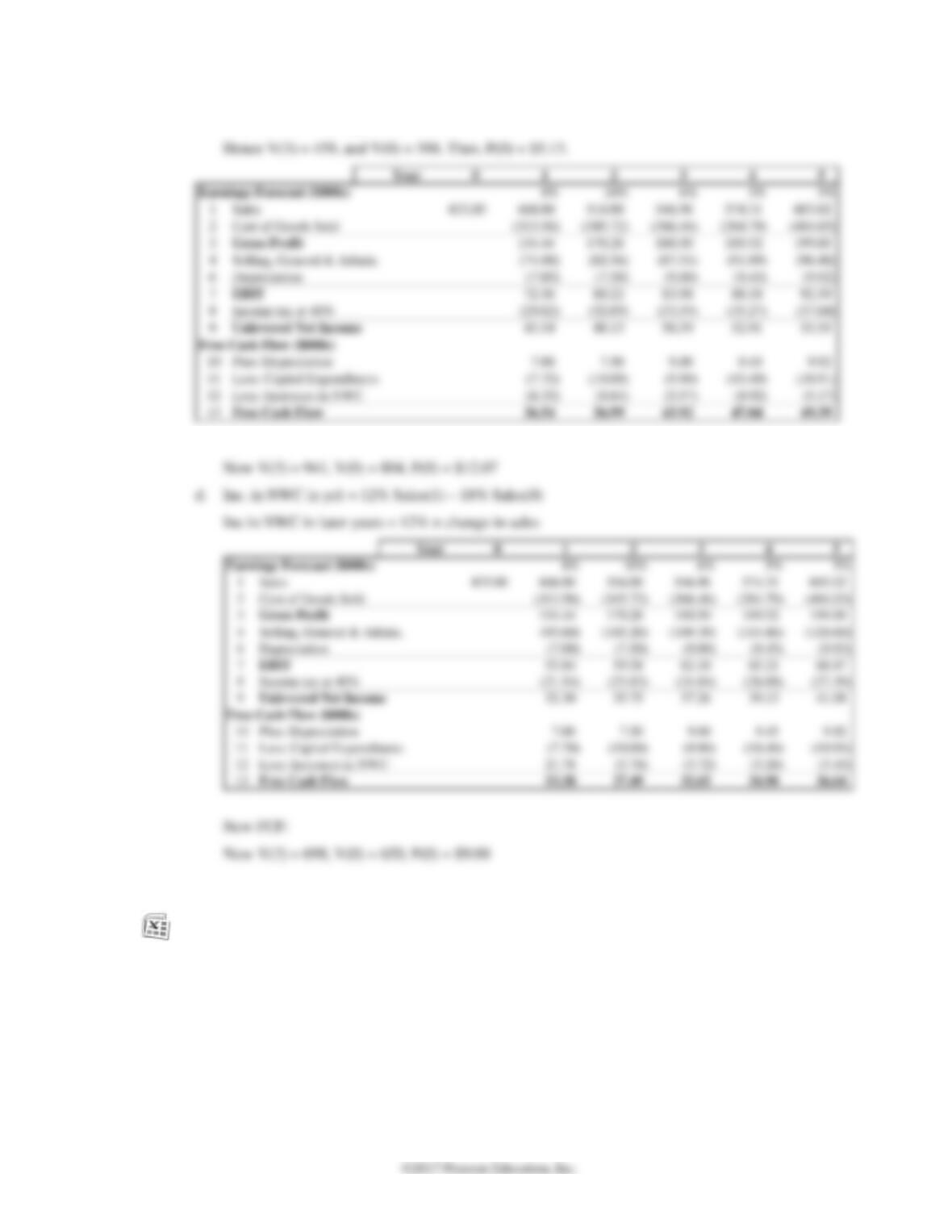

9-21. Sora Industries has 60 million outstanding shares, $120 million in debt, $40 million in cash, and

the following projected free cash flow for the next four years:

a. Suppose Sora’s revenue and free cash flow are expected to grow at a 5% rate beyond year 4.

If Sora’s weighted average cost of capital is 10%, what is the value of Sora’s stock based on

this information?

b. Sora’s cost of goods sold was assumed to be 67% of sales. If its cost of goods sold is actually

70% of sales, how would the estimate of the stock’s value change?

c. Let’s return to the assumptions of part (a) and suppose Sora can maintain its cost of goods

sold at 67% of sales. However, now suppose Sora reduces its selling, general, and

administrative expenses from 20% of sales to 16% of sales. What stock price would you

estimate now? (Assume no other expenses, except taxes, are affected.)

*d. Sora’s net working capital needs were estimated to be 18% of sales (which is their current

level in year 0). If Sora can reduce this requirement to 12% of sales starting in year 1, but all

other assumptions remain as in part (a), what stock price do you estimate for Sora? (Hint:

This change will have the largest impact on Sora’s free cash flow in year 1.)

Chapter 9/Valuing Stocks 141

b. Free cash flows change as follows:

c. New FCF:

9-22. Consider the valuation of Kenneth Cole Productions in Example 9.7.

a. Suppose you believe KCP’s initial revenue growth rate will be between 4% and 11% (with

growth slowing in equal steps to 4% by year 2011). What range of share prices for KCP is

consistent with these forecasts?

b. Suppose you believe KCP’s EBIT margin will be between 7% and 10% of sales. What range

of share prices for KCP is consistent with these forecasts (keeping KCP’s initial revenue

growth at 9%)?

c. Suppose you believe KCP’s weighted average cost of capital is between 10% and 12%. What

range of share prices for KCP is consistent with these forecasts (keeping KCP’s initial

revenue growth and EBIT margin at 9%)?

142 Berk/DeMarzo, Corporate Finance, Fourth Edition

d. What range of share prices is consistent if you vary the estimates as in parts (a), (b), and (c)

simultaneously?

9-23. Suppose Kenneth Cole Productions (KCP) is acquired at the end of 2012 for a purchase price of

$15.25 per share. KCP has 18.5 million shares outstanding, $45 million in cash, and no debt at

the time of the acquisition.

a. Given a weighted average cost of capital of 11%, and assuming no future growth, what level

of annual free cash flow would justify this acquisition price?

b. If KCP’s current annual sales are $480 million, assuming no net capital expenditures or

increases in net working capital, and a tax rate of 35%, what EBIT margin does your answer

in part (a) require?

9-24. You notice that PepsiCo (PEP) has a stock price of $72.62 and EPS of $3.80. Its competitor, the

Coca-Cola Company (KO), has EPS of $1.89. Estimate the value of a share of Coca-Cola stock

using only this data.

9-25. Suppose that in January 2006, Kenneth Cole Productions had EPS of $1.65 and a book value of

equity of $12.05 per share.

a. Using the average P/E multiple in Table 9.1, estimate KCP’s share price.

b. What range of share prices do you estimate based on the highest and lowest P/E multiples in

Table 9.1?

c. Using the average price to book value multiple in Table 9.1, estimate KCP’s share price.

d. What range of share prices do you estimate based on the highest and lowest price to book

value multiples in Table 9.1?

9-26. Suppose that in January 2006, Kenneth Cole Productions had sales of $518 million, EBITDA of

$55.6 million, excess cash of $100 million, $3 million of debt, and 21 million shares outstanding.

a. Using the average enterprise value to sales multiple in Table 9.1, estimate KCP’s share price.

b. What range of share prices do you estimate based on the highest and lowest enterprise value

to sales multiples in Table 9.1?

c. Using the average enterprise value to EBITDA multiple in Table 9.1, estimate KCP’s share

price.

d. What range of share prices do you estimate based on the highest and lowest enterprise value

to EBITDA multiples in Table 9.1?

9-27. In addition to footwear, Kenneth Cole Productions designs and sells handbags, apparel, and

other accessories. You decide, therefore, to consider comparables for KCP outside the footwear

industry.

a. Suppose that Fossil, Inc., has an enterprise value to EBITDA multiple of 9.73 and a P/E

multiple of 18.4. What share price would you estimate for KCP using each of these multiples,

based on the data for KCP in Problems 25 and 26?

b. Suppose that Tommy Hilfiger Corporation has an enterprise value to EBITDA multiple of

7.19 and a P/E multiple of 17.2. What share price would you estimate for KCP using each of

these multiples, based on the data for KCP in Problems 25 and 26?

9-28. Consider the following data for the airline industry for December 2015 (EV = enterprise value,

Book = tangible book value). Discuss the challenges of using multiples to value an airline.

CompanyName MarketCap EV EV/Sales EV/EBITDA EV/EBIT P/E P/Book

DeltaAirLines(DAL) 40,857 45,846 1.1x 6.0x 7.6x 15.0x 4.0x

9-29. Suppose Hawaiian Airlines (HA) has 53 million shares outstanding. Estimate Hawaiian’s share

value using each of the five valuation multiples in Problem 28, based on the median valuation

multiple of the other seven airlines shown.

144 Berk/DeMarzo, Corporate Finance, Fourth Edition

9-30. You read in the paper that Summit Systems from Problem 6 has revised its growth prospects

and now expects its dividends to grow at 3% per year forever.

a. What is the new value of a share of Summit Systems stock based on this information?

b. If you tried to sell your Summit Systems stock after reading this news, what price would you

be likely to get and why?

9-31. In mid-2015, Coca-Cola Company (KO) had a share price of $41. Its dividend was $1.32 per

year, and you expect Coca-Cola to raise this dividend by approximately 7% per year in

perpetuity.

a. If Coca–Cola’s equity cost of capital is 8%, what share price would you expect based on your

estimate of the dividend growth rate?

b. Given Coca–Cola’s share price, what would you conclude about your assessment of Coca–

9-32. Roybus, Inc., a manufacturer of flash memory, just reported that its main production facility in

Taiwan was destroyed in a fire. While the plant was fully insured, the loss of production will

decrease Roybus’ free cash flow by $180 million at the end of this year and by $60 million at the

end of next year.

a. If Roybus has 35 million shares outstanding and a weighted average cost of capital of 13%,

what change in Roybus’ stock price would you expect upon this announcement? (Assume the

value of Roybus’ debt is not affected by the event.)

b. Would you expect to be able to sell Roybus’ stock on hearing this announcement and make a

profit? Explain.

9-33. Apnex, Inc., is a biotechnology firm that is about to announce the results of its clinical trials of a

potential new cancer drug. If the trials were successful, Apnex stock will be worth $70 per share.

If the trials were unsuccessful, Apnex stock will be worth $18 per share. Suppose that the

morning before the announcement is scheduled, Apnex shares are trading for $55 per share.

a. Based on the current share price, what sort of expectations do investors seem to have about

the success of the trials?

b. Suppose hedge fund manager Paul Kliner has hired several prominent research scientists to

examine the public data on the drug and make their own assessment of the drug’s promise.

Would Kliner’s fund be likely to profit by trading the stock in the hours prior to the

announcement?

c. What would limit the fund’s ability to profit on its information?