Chapter 9 Cash Flow and Capital Budgeting 251

2016. With the marketing campaign, sales are expected to rise to the levels shown in the

sales forecast table for each of the next five years. The cost of goods sold is expected to

remain at 75 % of sales; general and administrative expense (exclusive of any marketing

campaign outlays) is expected to remain at 15 % of sales; and annual depreciation expense

is expected to remain at $2 million. Assuming a 40 % tax rate, find the cash flows over the

next five years associated with Premium Wines’ proposed marketing campaign.

Premium Wines Income Statement

for the Year ended

December 31, 2011

___________________________________________________________

Sales revenue $80,000,000

Less: Cost of goods sold (75%) 60,000,000

Gross profit $20,000,000

Premium Wines

Sales Forecast .

Year Sales Revenue

2012 $82,000,000

A9-7. Incremental operating cash flows:

Year

2012

2013

2014

2015

2016

Change in sales

$ 2,000,000

$ 4,000,000

$ 6,000,000

$10,000,000

$14,000,000

252 Instructor’s Manual

Incremental Cash Flows

P9-8. Identify each of the following situations as involving sunk costs, opportunity costs, and/or

cannibalization. Indicate what amount, if any, of these items would be relevant to the given

investment decision.

a. The investment requires use of additional computer storage capacity to create a data

d. Subleasing 100 parking spaces in your firm’s parking lot to the tenants in an adjacent

building that has inadequate off-street parking. You pay $20 per month for each space

under a non-cancelable 50-year lease. The sublessee will pay you $15 per month for

A9-8. a. $37,000 per year until the lease would have expired by itself is the opportunity cost to

the investment and it is relevant to the investment decision

e. Cannibalization of the existing products by the new one, even though they are not re-

lated, because the sales force will be overburdened and therefore invest less time in

P9-9. Barans Manufacturing is developing the incremental cash flows associated with the pro-

posed replacement of an existing stamping machine with a new, technologically advanced

Chapter 9 Cash Flow and Capital Budgeting 253

a. Barans could use the same dies and other tools (with a book value of $40,000) on the

new stamping machine that it used on the old one.

d. Barans can use a small storage facility, built by Barans at a cost of $120,000 three

years earlier, to store the increased output of the new stamping machine. Because of its

unique configuration and location, it is currently of no use to either Barans or any other

firm.

A9-9. a. Using the same dies and tools is not an incremental expense. This is a sunk cost and

not relevant to the project cash flows.

b. The $17,000 is an opportunity cost and is relevant. If the firm accepts the project, it

P9-10. Blueberry Electronics is exploring the possibility of producing a new handheld device that

will serve both as a basic PC with Internet access and as a cell phone. Which of the follow-

ing items are incremental costs for the project’s analysis?

a. Research and development funds that the company has spent while working on a pro-

A9-10. Sunk costs include:

a. Research and development funds already spent

Incremental costs include:

b. The impact on other products produced by the company. However, since it is expected

254 Instructor’s Manual

P9-11. New York Pizza is considering replacing an existing oven with a new, more sophisticated

oven. The old oven was purchased three years ago at a cost of $20,000, and this amount

was being depreciated under MACRS using a 5-year recovery period. The oven has five

years of usable life remaining. The new oven being considered costs $30,500, requires

New Oven .

Old Oven .

Year

Revenue

Expenses

(excluding

depreciation)

Revenue

Expenses

(excluding

depreciation)

a. Calculate the initial cash outflow associated with replacement of the old oven with a

new one.

A9-11. a.

Cost of new oven

$30,500

+ Installation costs

1,500

Total installed cost

$32,000

Proceeds from Sale of old oven

$22,000

Less tax on sale of old oven:

Sale price

$22,000

Book value (1 – .20 – .32 – .192) $20,000

Gain on sale of old oven

$16,240

Tax rate

Tax on sale of old oven

After tax proceeds from sale of old oven

Chapter 9 Cash Flow and Capital Budgeting 255

5-Year

MACRS %

Installed

Cost

Depreciation

20

$32,000

$ 6,400.00

32

11.52

11.52

New Oven: Year:

1

2

3

4

5

6

Sales

$300,000

$300,000

$300,000

$300,000

$300,000

$ 0

– Expenses

288,000

288,000

288,000

288,000

288,000

0

– Depreciation

Taxable income

Earnings

(Earn + Depr)

5-Year

MACRS %

Installed

Cost

Depreciation

19.2

11.52

11.52

20

$20,000

$4,000.00

Old Oven: Year:

1

2

3

4

5

6

Sales

$270,000

$270,000

$270,000

$270,000

$270,000

0

– Expenses

264,000

264,000

264,000

264,000

264,000

0

– Depreciation

2,304

2,304

1,152

0

0

0

Taxable income

0

– Taxes (40%)

0

Earnings

$ 2,218

0

0

256 Instructor’s Manual

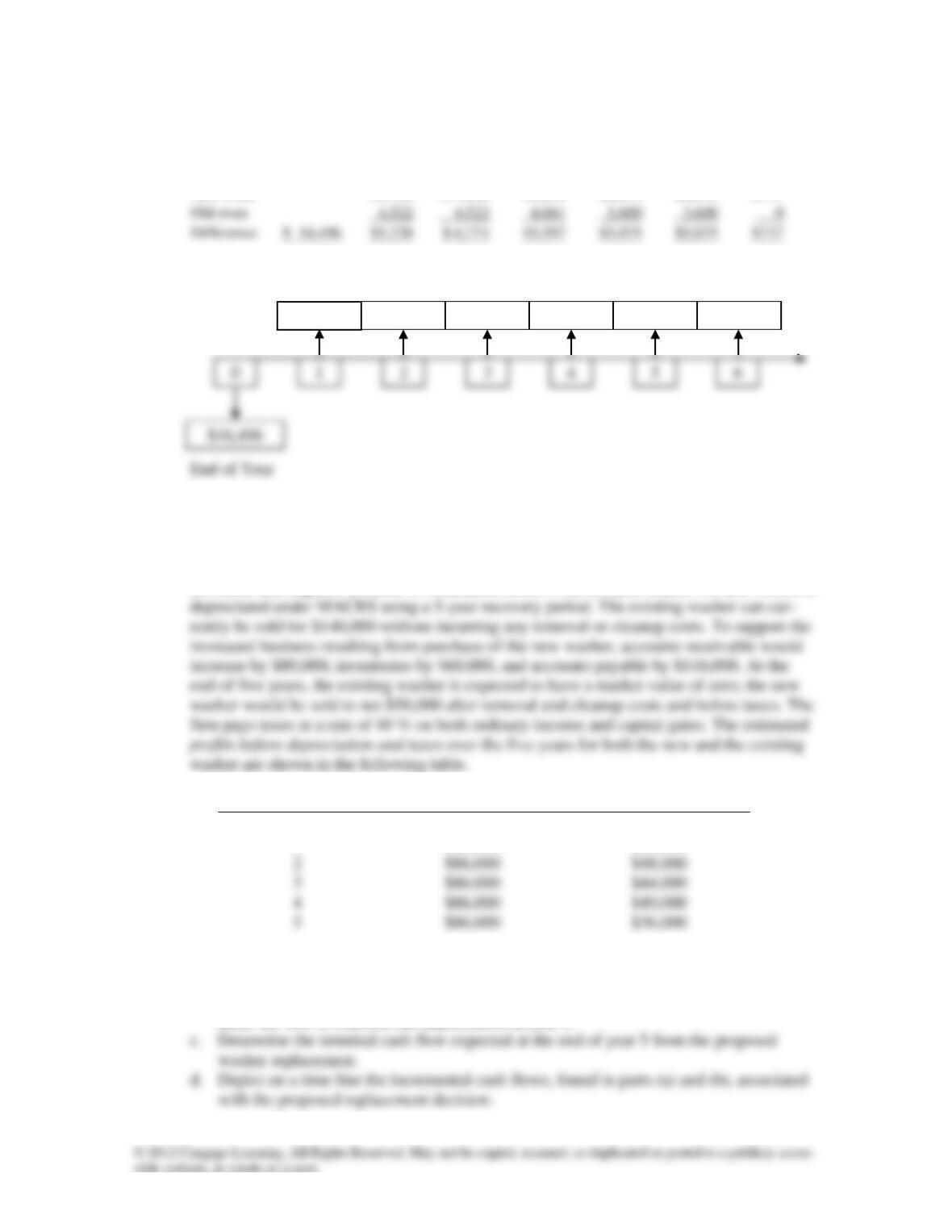

Incremental cash flows:

Year:

0

1

2

3

4

5

6

New oven

$9,760

$11,296

$9,658

$8,675

$8,675

$737

Difference

$5,238

$5,597

$5,075

$5,075

$737

c.

P9-12. Speedy Auto Wash is contemplating the purchase of a new high-speed washer to replace

the existing washer. The existing washer was purchased two years ago at an installed cost

of $120,000; it was being depreciated under MACRS using a 5-year recovery period. The

existing washer is expected to have a usable life of five more years. The new washer costs

$210,000 and requires $10,000 in installation costs; it has a 5-year usable life and would be

Profits before Depreciation and Taxes

Year

New Washer

Existing Washer

1

$86,000

$52,000

3

$86,000

$44,000

a. Calculate the initial cash outflow associated with the replacement of the existing wash-

er with the new one.

b. Determine the incremental cash flows associated with the proposed washer replace-

ment. Be sure to consider the depreciation in year 6.

$5,238

$6,774

$5,597

$4,474

$5,074

$737

Chapter 9 Cash Flow and Capital Budgeting 257

A9-12. a.

Cost of new washer

$210,000

+ Installation cost

10,000

Total installed cost

$220,000

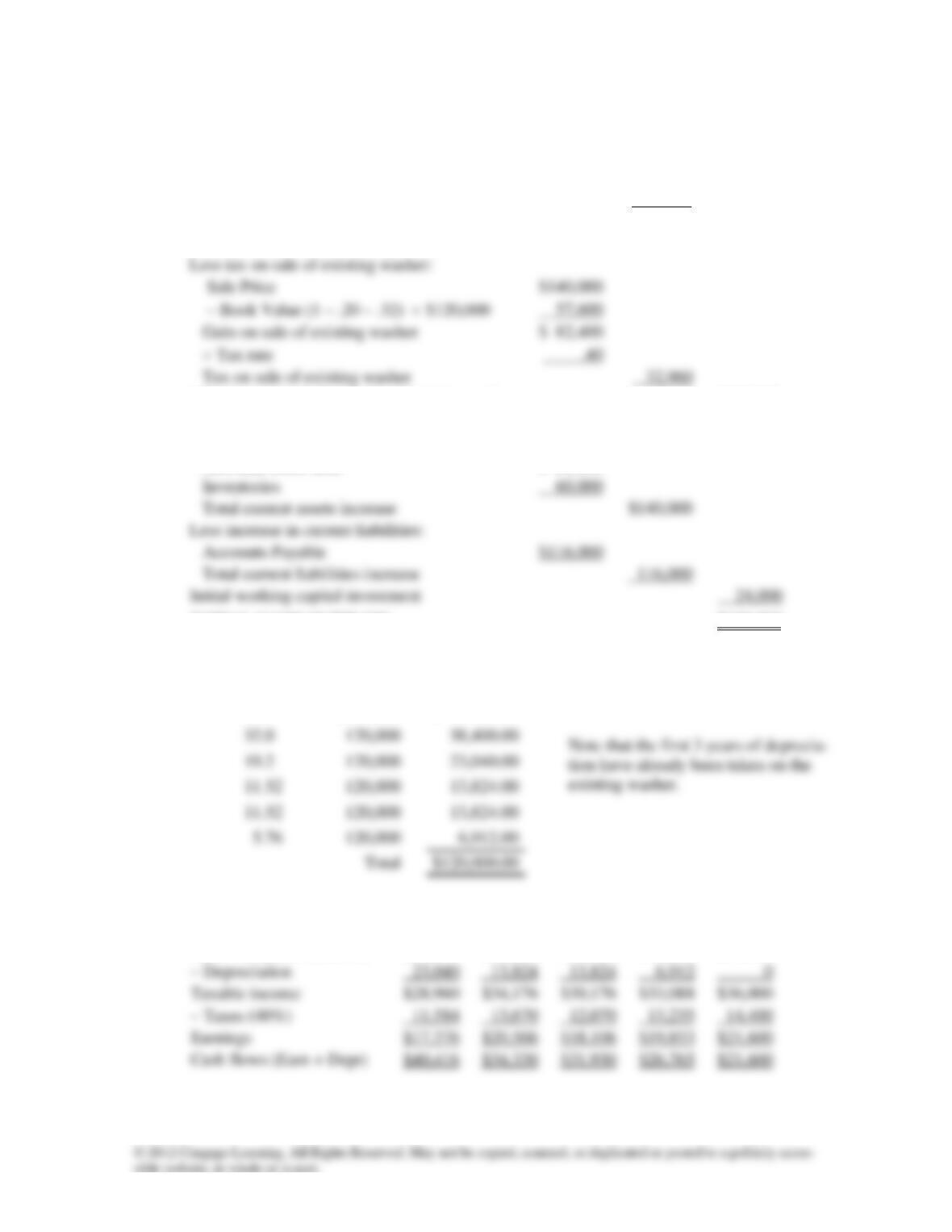

Proceeds from sale of existing washer

$140,000

Less tax on sale of existing washer:

Sale Price

$140,000

– Book Value (1 – .20 – .32) $120,000

Gain on sale of existing washer

$ 82,400

Tax on sale of existing washer

After tax proceeds from sale of existing washer

(107,040)

+ Initial working capital investment

Increase in current assets:

Accounts receivable

$ 80,000

Inventories

60,000

Total current assets increase

$140,000

Less increase in current liabilities:

Accounts Payable

$116,000

Total current liabilities increase

116,000

Initial working capital investment

24,000

INITIAL CASH OUTFLOW

$136,960

b.

5-Year

MACRS %

Installed

Cost

Depreciation

11.52

20.0

$120,000

$ 24,000.00

Existing Washer: Year:

1

2

3

4

5

Sales – Expenses (PBOT)

$52,000

$48,000

$44,000

$40,000

$36,000

23,040

13,824

13,824

6,912

0

Taxable income

$28,960

$34,176

$30,176

$33,088

$36,000

11,584

13,670

12,070

13,235

14,400

Earnings

$17,376

$20,506

$18,106

$19,853

$21,600

Cash flows (Earn + Depr)

$40,416

$34,330

$31,930

$26,765

$21,600

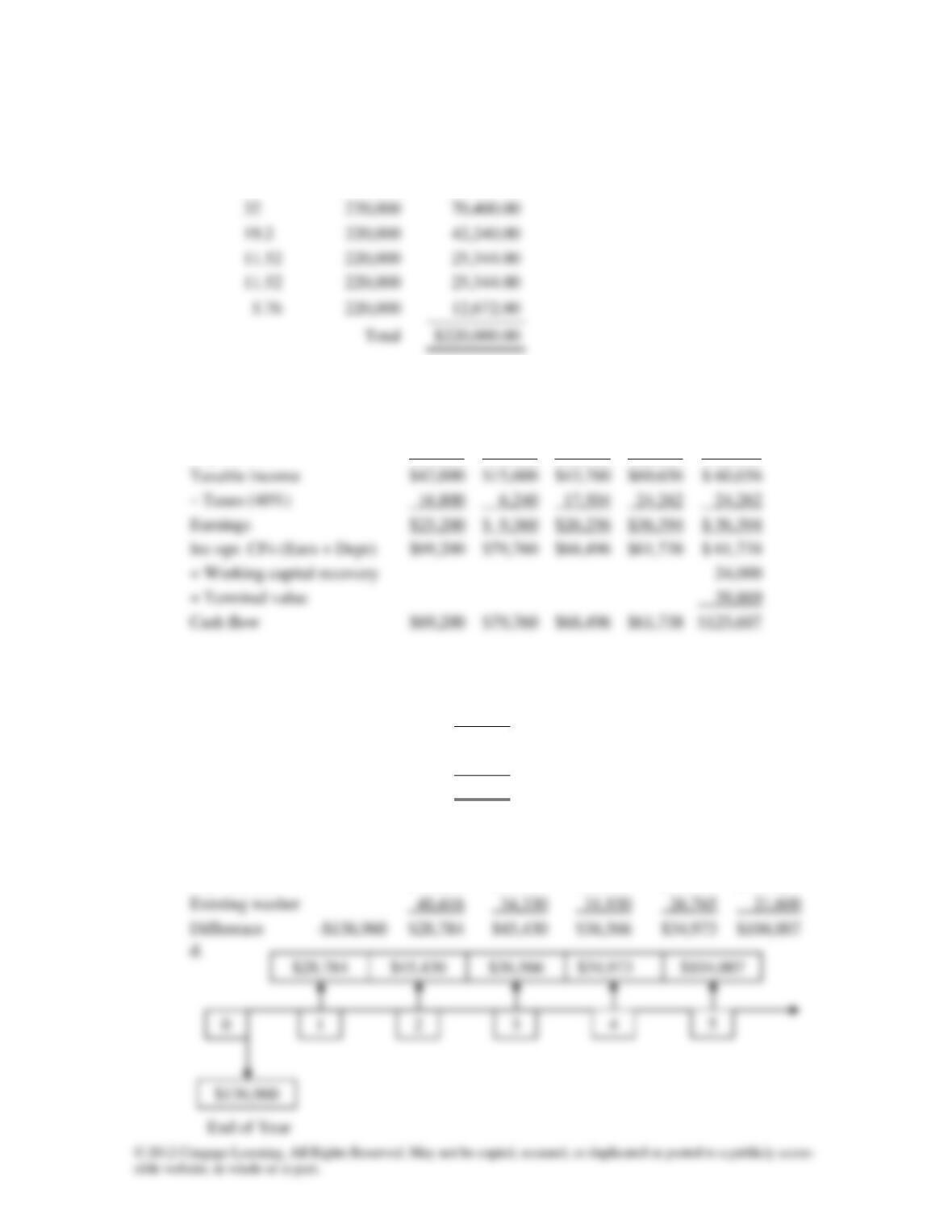

258 Instructor’s Manual

5-Year

MACRS %

Installed

Cost

Depreciation

20

$220,000

$ 44,000.00

New Washer: Year:

1

2

3

4

5

Machine cost

– Sales-Expenses (PBDT)

$86,000

$86,000

$86,000

$86,000

$ 86,000

Depreciation

44,000

70,400

42,240

25,344

25,344

Taxable income

$42,000

$15,600

$43,760

$60,656

$ 60,656

16,800

6,240

17,504

24,262

24,262

Earnings

$25,200

$ 9,360

$26,256

$36,394

$ 36,394

Inc opr. CFs (Earn + Depr)

$69,200

$79,760

$68,496

$61,738

$ 61,738

+ Working capital recovery

+ Terminal value

39,869

Cash flow

$69,200

$79,760

$68,496

$61,738

$125,607

c. Terminal value of new washer in year 5

Sale price

$58,000

– Book value (0.0576 x 220,000)

12,672

(year 6 depr)

Gain on sale

$45,328

– Taxes (40%)

18,131

Terminal value (sale price – taxes)

$39,869

Incremental cash flows:

Year:

0

1

2

3

4

5

New washer

$69,200

$79,760

$68,496

$61,738

$125,607

Existing washer

40,416

34,330

31,930

26,765

21,600

Difference

Chapter 9 Cash Flow and Capital Budgeting 259

P9-13. TransPacific Shipping is considering replacing an existing ship with one of two newer,

more efficient ones. The existing ship is three years old, cost $32 million, and is being de-

preciated under MACRS using a 5-year recovery period. Although the existing ship has

only three years (years 4, 5, and 6) of depreciation remaining under MACRS, it has a re-

maining usable life of five years. Ship A, one of the two possible replacement ships, costs

Profits before Depreciation and Taxes

Year

Ship A

Ship B

Existing Ship

1

$21,000,000

$22,000,000

$14,000,000

3

$21,000,000

$26,000,000

$14,000,000

5

$21,000,000

$26,000,000

$14,000,000

The existing ship can currently be sold for $18 million and will not incur any removal or

cleanup costs. At the end of five years, the existing ship can be sold to net $1 million be-

fore taxes. Ships A and B can be sold to net $12 million and $20 million before taxes, re-

spectively, at the end of the 5-year period. The firm is subject to a 40 % tax rate on both

ordinary income and capital gains.

260 Instructor’s Manual

A9-13. a.

Ship A

Ship B

Cost of new ship

$40,000,000

$54,000,000

Installation

8,000,000

6,000,000

Total installed cost

$48,000,000

$60,000,000

Less proceeds from selling existing ship

$18,000,000

Less tax on sale of existing ship:

Sale price

$18,000,000

9,216,000

Tax on sale of existing ship

After-tax proceeds from sale of existing ship

(14,486,400)

(14,486,400)

+ Initial working capital investment

4,000,000

6,000,000

INITIAL CASH OUTFLOW

$37,513,600

$51,513,600

b and c.

Ship A:

5-Year

MACRS %

Installed

Cost

Depreciation

20.0

$48,000,000

$ 9,600,000

$48,000,000

Year:

1

2

3

4

5

Sales – Expenses (PBDT)

$21,000,000

$21,000,000

$21,000,000

$21,000,000

$21,000,000

– Depreciation

9,600,000

15,360,000

9,216,000

5,529,600

5,529,600

– Taxes (40%)

4,560,000

2,256,000

4,713,600

6,188,160

6,188,160

Working capital recovery

8,305,920

Chapter 9 Cash Flow and Capital Budgeting 261

Terminal value of Ship A in year 5:

Sale price

$12,000,000

(Year 6 Depr.)

Gain on sale

Taxes (40%)

Ship B:

5-Year

MACRS %

Installed

Cost

Depreciation

20.0

$60,000,000

$12,000,000

32.0

$60,000,000

19,200,000

19.2

$60,000,000

11,520,000

11.52

$60,000,000

11.52

$60,000,000

$60,000,000

Year:

1

2

3

4

5

Sales–Expenses

$22,000,000

$24,000,000

$26,000,000

$26,000,000

$26,000,000

– Depreciation

12,000,000

19,200,000

11,520,000

6,912,000

6,912,000

Taxable income

$10,000,000

$14,480,000

$19,088,000

$19,088,000

– Taxes (40%)

5,792,000

7,635,200

7,635,200

Earnings

$ 6,000,000

$ 2,880,000

$11,452,800

$11,452,800

Working capital recovery

Terminal value

13,382,400

Cash flow

$18,000,000

$22,080,000

$20,208,000

$18,364,800

$37,747,200

Terminal value of Ship B in year 5:

Sale price

$20,000,000

Gain on sale

$16,544,000

Taxes (40%)

6,617,600

Terminal value (sale price – taxes)

$13,382,400

262 Instructor’s Manual

Existing Ship:

5-Year

MACRS %

Installed

Cost

Depreciation

19.2

$32,000,000

11.52

$32,000,000

$32,000,000

1,843,200.00

Total

$ 32,000,000

20.0

$32,000,000

$ 6,400,000.00

32.0

$32,000,000

10,240,000.00

Year:

1

2

3

4

5

Sales – Expenses (PBDT)

$14,000,000

$14,000,000

$14,000,000

$14,000,000

$14,000,000

– Depreciation

3,686,400

3,686,400

1,843,200

0

0

Taxable income

$10,313,600

$10,313,600

$12,156,800

$14,000,000

$14,000,000

Earnings

$ 6,188,160

$ 6,188,160

$ 7,294,080

$ 8,400,000

$ 8,400,000

Oper. CFs (Earn + Depr)

$ 9,874,560

$ 9,874,560

$ 9,137,280

$ 8,400,000

$ 8,400,000

Terminal value

Cash flow

Terminal value of existing ship in year 5:

Sale price

$1,000,000

(Fully depreciated)

Gain on sale

$1,000,000

Terminal value

$ 600,000

Incremental cash flows:

Year:

0

1

2

3

4

5

Ship A

$16,440,000

$18,744,000

$16,286,400

$14,811,840

$27,117,760

Existing ship

Incremental cash flows:

Year:

0

1

2

3

4

5

Ship B

$18,000,000

$22,080,000

$20,208,000

$18,364,800

$37,747,200

Old ship

Difference

Chapter 9 Cash Flow and Capital Budgeting 263

d. The time lines

Ship A:

$37,513,600

Ship B:

$51,513,600

P9-14. The management of Kimco is evaluating replacing their large mainframe computer with a

modern network system that requires much less office space. The network would cost

A9-14.

Year:

0

1

2

3

4

5

Network cost

$–500,000

Operating cash flows

$125,000

$125,000

$125,000

$125,000

$125,000

Cash flows

$–480,000

$125,000

$125,000

$125,000

$125,000

$125,000

NPV at 10%

P9-15. Pointless Luxuries Inc. (PLI) produces unusual gifts targeted at wealthy consumers. The

company is analyzing the possibility of introducing a new device designed to attach to the

collar of a cat or dog. This device emits sonic waves that neutralize airplane engine noise,

so that pets traveling with their owners can enjoy a more peaceful ride. PLI estimates that

$6,565,440

$8,869,440

$7,149,120

$6,411,840

$18,117,600

$8,125,440

$12,205,440

$11,070,720

$9,964,800

$28,747,200

264 Instructor’s Manual

developing this product will require up-front capital expenditures of $10 million. These

costs will be depreciated on a straight-line basis for five years. PLI believes that it can sell

the product initially for $250. The selling price will increase to $260 in years 2 and 3 be-

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Accounts receivable

$0

$200,000

$250,000

$300,000

$150,000

$0

Inventory

0

500,000

650,000

780,000

600,000

0

The firm faces a tax rate of 34 percent. Assume that cash flows arrive at the end of each

year, except for the initial $10 million outlay.

a. Calculate the project’s contribution to net income each year.

b. Calculate the project’s cash flows each year.

c. Calculate two NPVs, one using a 10 percent discount rate and one using a 15 percent

discount rate.

d. A PLI financial analyst reasons as follows: “With the exception of the initial outlay,

A9-15. a and b.

Year:

1

2

3

4

5

Units sales

20,000

25,000

30,000

36,000

41,400

Price/Unit

$250

$260

$260

$245

$240

Revenue

$5,000,000

$6,500,000

$7,800,000

$8,820,000

$9,936,000

Net income

$ 300,000

$1,125,000

$1,750,000

$1,960,000

$2,347,000

+ Depreciation

2,000,000

2,000,000

2,000,000

2,000,000

2,000,000

Operating CF

$2,198,000

$2,742,500

$3,155,000

$3,293,600

$3,549,020

Working capital*

–700,000

–200,000

–180,000

330,000

750,000

Cash flow

$1,498,000

$2,542,500

$3,623,600

$4,299,020

* Year-to-year change in investment in A/R and inventories