201

Chapter 8 Capital Budgeting Process and Decision Criteria

Chapter Overview

The Opening Focus presents the story of the capital investment project by Candente Copper

Corporation. It purchased mines in Peru with the net present value of the investment being an

outstanding one billion dollars. The estimated value the mines copper, silver and gold would

produce an 18% IRR or return on their investment. Nice return for stockholders!

Opening Focus Discussion Questions

1. How does a project with a high return relate to the concept of maximizing shareholder wealth?

In other words, what is the direct relationship between returns and wealth generation?

This chapter, after introducing the basic capital budgeting problem, covers:

8-1. Introduction of Capital Budgeting

8-2. Payback Methods

Technology

1. Smart Practices Video. Dan Carter, executive vice president and chief financial officer of

Charlotte Russe, talks about decision metrics that his company uses.

3. Smart Concepts Animation provides a step-by-step explanation of the conflicts between the

NPV and IRR criteria when firms evaluate mutually exclusive projects.

4. Smart Practices Video. Beth Acton, former vice president and treasurer of Ford, notes that

6. Smart Solutions provide a step-by-step solution to Problem 8-21, which compares two

competing projects using NPV, IRR, and PI techniques.

202 Instructor’s Manual

Lecture Guide

Firm management makes two basic decisions – the financing and the capital budgeting decisions.

This chapter provides tools that managers can use to evaluate projects that will add to shareholder

wealth.

An Introduction To Capital Budgeting

While few finance classes extensively discuss the choice of capital budgeting projects,

clearly this is of utmost importance to a firm. A firm that is unable to find and implement value-

increasing projects will not stay in business very long. Similarly, a firm that does not have good

evaluative controls in effect will have difficulty continuing its business. After a project has been

chosen and implemented, managers must continually monitor that project, ensuring that it is

meeting its stated milestones for revenue and cash flow generation. If a project is not performing

as expected, then why? Were revenues lower than expected or costs higher than expected? If a

project is exceeding expectations, then why is this happening? Is this success something that can

be repeated in another project?

The capital budgeting decision should be separate from the financing decision. Project cash

8.1a Traits of an Ideal Investment Criteria

This section brings information from prior chapters into the capital budgeting process. A

sound capital budgeting process must take time value of money – the magnitude and timing of the

cash flows into account. It also must appropriately account from relevant risk. The focus should

8.1b A Capital Budgeting Problem

This section introduces the fictitious company Global Wireless Incorporated and walks the

students through a capital budgeting investment for the firm. This is a nice problem to walk the

students through from beginning to end. Be sure to emphasize the timeline aspect of the investment

as depicted in Figure 8.1. Global Wireless .

This chapter follows Global Wireless Inc.’s fictitious capital budgeting problem. The

chapter looks at how this project would be evaluated using various capital budgeting techniques

Chapter 8 Capital Budgeting Process and Decision Criteria 203

and under what circumstances the project would be acceptable to Global Wireless. This chapter

provides the relevant cash flows, focusing on evaluation techniques, not how to generate cash

flows for capital budgeting, which is covered later in the textbook.

These slides provide students with the calculation of payback period for Global Wireless

and summarize the advantages and disadvantages of the payback method, discussed above.

• Student Interaction: Ask students under what circumstances is discounted payback

worse for a company? (When the company uses discounted payback, but doesn’t

Fig 8.1 Global Wireless Investment Proposals

8.2 Payback Methods

8.2a Payback Decision Rule

8.2b Pros and Cons of the Payback Method

This section summarizes the pros and cons of this method. Point out the advantages to

payback:

• Simple to compute and understand.

• Student Interaction: Ask students if they would rather explain payback or NPV to

a manager who has no finance background.

Show how easily payback can be misused, and lead to incorrect answers:

Consider two projects, A and B

204 Instructor’s Manual

• Student Interaction: Ask students to take a side and tell us why we should or

should not use the Payback Method.

o Project A has a payback in 1 year, yet without doing any calculations, it is

8.2c Discounted Payback

In an effort to correct the problems associated with the payback decision method. The

8-3. Accounting Based Methods

8.3a Accounting Rate of Return (ARR)

The accounting rate of return for a project has serious limitations because it does not take

time value of money into account and it uses accounting numbers, not cash flows.

While this method may be popular because managers are accustomed to thinking in terms of

returns, and this gives them a percent return, accounting based methods are very flawed. It is very

8.4 Net Present Value

• Student Interaction: Ask students if they would want a project/investment where someone

gives them $100 and they immediately give back $110. Students will say no, because of

the time value of money. They, like the company, want time to invest the money and earn

Chapter 8 Capital Budgeting Process and Decision Criteria 205

Point out that NPV provides correct answers to capital budgeting decisions because it

incorporates both market-determined risk and the time value of money. The rule of acceptance of

this method is also very simple and intuitive. If the NPV>0, then the company should accept the

8.4a Net Present Value Calculations

Note that this kind of calculation was made in previous chapters. The only addition to

previous chapter problems is an initial cost. In previous problems, students computed present

value – given a series of future cash flows, they applied a discount rate and calculated present

Fig. 8.2 The NPV Rule and Shareholder Wealth

Fig. 8.3a NPV of Global Wireless’s Projects at 18%

Fig. 8.3b NPV of Global Wireless’s Projects at 18%

8.4b Pros and Cons of NPV

NPV is the most theoretically correct model to use in capital budgeting. Its main drawback – that

8.4c Economic Value Added

Recently a variant of NPV has been used – Economic Value Added. Economic Value

8.5 Internal Rate of Return

Figure 8.4 NPV Profile

206 Instructor’s Manual

8.5a Finding a Project’s IRR

Possibly the most popular of the alternative methods of capital budgeting decision-making,

IRR is intuitive and easy to use with today’s technology.

• Student Interaction: Point out to students that they have done IRR calculations in

Fig. 8.5a and 8.5b Calculating IRRs for Global Wireless Projects

Using information given in the text, this slide shows IRR for the Western Europe and Southeast

8.5b Advantages of the IRR Method

IRR has many of the same advantages as IRR. In addition, many managers are used to

thinking of their investments as a percent return. IRR provides this internal measure of

8.5c Problems with the Internal Rate of Return

Lending vs Borrowing

Timing of the cash flows can cause problems. The book gives the example of timber

cutting firms. These firms will cut and sell the timber immediately, but will have to pay to replant

Fig. 8.6 Lending vs Borrowing

Chapter 8 Capital Budgeting Process and Decision Criteria 207

Multiple IRRs

• Student Interaction: Ask students for examples of projects with non-conventional cash

Fig. 8.7 NPV Profile of a Project with Multiple IRRs

No Real Solution

• Student Interaction: Ask students for examples of projects with no IRRs. While

mathematically one can devise projects with no IRR (try Cash flow 0 = $100, Cash flow 1

8.5d IRR and NPV and Mutually Exclusive Projects

Point out that differences in answers for mutually exclusive projects result from size and

timing differences. Projects with lower initial investments that return their cash flows earlier tend

The Scale Problem

If two projects give positive returns that exceed the hurdle rate – size and scale of the

The Timing Problem

This section is a graphical representation of the conflict between mutually exclusive projects. The

instructor can point to the discount rates (below the crossover point) and which the long term

IRR.

• Student Interaction: Have students speculate about why IRR is so popular, even

though finance textbooks clearly point out its flaws. There is no definitive answer to

208 Instructor’s Manual

Fig. 8.8 NPV Profiles Demonstrating the Timing Problem

8.6 Profitability Index

8.7 A New Investment Problem

This last section give an example using many of the capital budgeting methods introduced

Fig. 8.9 Net Present Value of Two Gas Chromatographs

Summary: Capital Budgeting

Enrichment Exercises

1. Tell students they’re in a job where they’re boss doesn’t like all those fancy finance theories.

How will you convince him (without being fired) that NPV is the best method to use in capital

Answers to Concept Review Questions

1. Other things being equal, managers would prefer (1) an easily applied capital budgeting

2. Payback is popular because it is very easy to compute and to understand and because it gives

4. Managers focus on the impact that an investment will have on reported earnings because

earnings or earnings per share are widely reported in the business press and companies (and

Chapter 8 Capital Budgeting Process and Decision Criteria 209

5. Among the factors that determine whether the annual accounting rate of return on a given

6. A project having an NPV of $1million means that $1 million in shareholder value (market

capitalization) is being added to the firm.

1. Both EVA and NPV provide a measure of value added, so it should not be surprising that these

methods are quite similar. EVA uses the same basic cash flows as NPV and evaluates the

9. IRR and NPV are related in that both use the time value of money and take risk into account.

10. If a single project with conventional cash flows has an IRR that exceeds the firm’s hurdle rate

11. You will recall that the “scale problem” indicates that we should use practical sense along with

IRR analysis: we should choose the investment that offers the best ABSOLUTE payoff to

maximize shareholder wealth, regardless of its percentage payoff. The “timing problem” has

12. NPV, IRR, and PI capital budgeting approaches are related because they adjust for the time

13. Both suffer from a scale problem, which the IRR and PI don’t take into consideration. When

choosing between two projects, the one that requires the larger funding but with the

210 Instructor’s Manual

Answers to Self-Test Problems

ST8-1. Nader International is considering investing in two assets – A and B. The initial outlay,

annual cash flows, and annual depreciation for each asset is shown in the table below for

Asset A

Asset B

Year

Cash Flow

Depreciation

Cash Flow

Depreciation

0

-$200,000

-$180,000

1

$70,000

$40,000

$80,000

$36,000

3

5

100,000

a. Calculate the payback period for each asset, assess its acceptability, and indicate which

asset is best using the payback period.

b. Calculate the discounted payback for each asset, assess its acceptability, and indicate

a. Accounting rate of return

Asset A

Asset B

Year

NPAT

NPAT

1

$70,000 − $40,000 = $30,000

$80,000 − $36,000 = $44,000

2

$80,000 − $40,000 = $40,000

$90,000 − $36,000 = $54,000

3

$90,000 − $40,000 = $50,000

4

$90,000 − $40,000 = $50,000

5

2.50

a. Payback

2.56 years / Not acceptable

2.33 years / Acceptable

3.17 years/Acceptable

3.62 years / Not Acceptable

Chapter 8 Capital Budgeting Process and Decision Criteria 211

c:

Asset A

Asset B

Year

CF

12% PV

Depr.

CF

12% PV

Depr.

0

-$200,000

-$180,000

1

$ 70,000

62,500

$40,000

$80,000

71,429

$36,000

2

63,776

40,000

90,000

71,747

3

4

57,196

40,000

40,000

25,420

5

d. They should take asset A because its accounting rate of return is acceptable as is its

discounted payback.

ST8-2. JK Products, Inc. is considering investing in either of two competing projects that will

allow the firm to eliminate a production bottleneck and meet the growing demand for its

products. The firm’s engineering department narrowed the alternatives down to tow –

Status Quo (SQ) and High Tech (HT). Working with the accounting and finance personnel,

the firm’s CFO developed the following estimates of the cash flows for SQ and HT over

the relevant 6-year time horizon. The firm has an 11 percent required return and views

these projects as equally risky.

Project SQ

Project HT

Year

Cash Flows

0

-$670,000

-$940,000

1

2

3

4

5

6

a. Calculate the net present value (NPV) of each project, assess its acceptability, and

indicate which project is best using NPV.

b. Calculate the internal rate of return (IRR) of each project, assess its acceptability, and

indicate which project is best using IRR.

212 Instructor’s Manual

A:

Project SQ

Project HT

a. NPV

$87,313.87

$142,254.07*

b. IRR

16.07%*

15.17%

c. PI

1.13

1.15*

All measures indicate project acceptability:

*Indicates the preferred project using each measure.

d.

Project

Rate

SQ

HT

0%

$360,000

$710,000

$142,254.07

16.07%

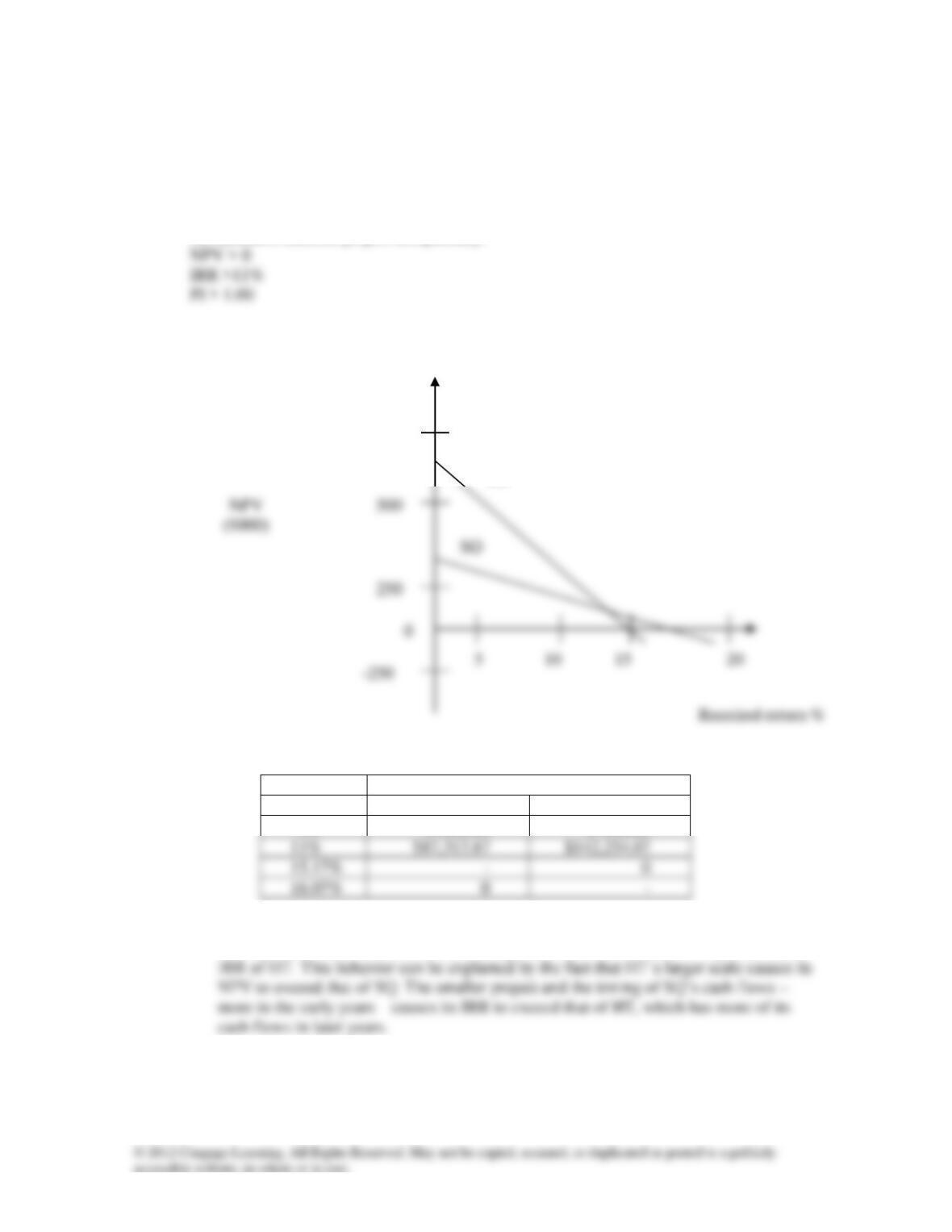

At 11% HT is preferred over SQ, but because the profiles cross somewhere beyond

11% and before the functions cross the required return axis the IRR of SQ exceeds the

e. Project HT is recommended because it has the higher NPV, the better technique. In

addition its PI is higher than that of Project SQ.

Required return %

250

0

-250

HT

750

Chapter 8 Capital Budgeting Process and Decision Criteria 213

Answers to End-of-Chapter Questions

Q8–1. Can you name some industries where the payback period is unavoidably long?

A8-1. Payback period is unavoidably long in industries with long-lasting projects, for example,

the oil exploration industry, where it might take a long time to find acceptable oil fields

and make them produce. Some agricultural products take a long time – for example starting

an apple orchard would have a long payback, waiting for the trees to grow, mature and

finally produce maximum produce.

Q8–2. In statistics, you learn about Type I and Type II errors. A Type I error occurs when a

statistical test rejects a hypothesis when the hypothesis is actually true. A Type II error

occurs when a test fails to reject a hypothesis that is actually false. We can apply this type

A8-2. a. Payback could lead to Type 1 errors when it rejects a good project that has large cash

flows after the payback period cutoff.

Q8–3. Holding the cutoff period fixed, which method has a more severe bias against long-lived

projects, payback or discounted payback?

A8-3. Discounted payback has a more severe bias – discounted cash flows will be smaller,

making it even harder for a project to pass the payback hurdle.

Q8–5. “Cash flow projections more than a few years out are not worth the paper they’re written

on. Therefore, using payback analysis, which ignores long-term cash flows, is more

reasonable than making wild guesses as one has to do in the NPV approach.” Respond to

this comment.

214 Instructor’s Manual

A8-5. NPV automatically adjusts for project time by using an exponentially smaller discount rate

applied to later cash flows. It gives these cash flows less importance in the final answer.

Q8–6. “Smart analysts can massage the numbers in NPV analysis to make any project’s NPV look

A8-6. Any method can be manipulated. It would be hard to argue that accounting numbers can’t

Q8–7. In what way is the NPV consistent with the principle of shareholder wealth maximization?

What happens to the value of a firm if a positive-NPV project is accepted? If a negative–

NPV project is accepted?

A8-7. The NPV approach is consistent with shareholder maximization because it suggests that

firms should only accept projects which earn returns above the opportunity costs of the

Q8–8. A particular firm’s shareholders demand a 15% return on their investment, given the firm’s

risk. However, this firm has historically generated returns in excess of shareholder

expectations, with an average return on its portfolio of investments of 25%.

a. Looking back, what kind of stock-price performance would you expect to see for this

firm?

A8-8. a. A firm that consistently earns returns higher than its opportunity cost of capital is

adding value to the firm, and its stock price should increase.

Q8-9. What are the potential faults in using the IRR as a capital budgeting technique? Given these

faults, why is this technique so popular among corporate managers?

A8-9. The IRR suffers from several problems. The IRR is not well suited to ranking projects with

very different scales or projects with very different cash flow timing patterns. The IRR

Q8-10. Why is the NPV considered to be theoretically superior to all other capital budgeting

techniques? Reconcile this result with the prevalence of the use of IRR in practice. How

Chapter 8 Capital Budgeting Process and Decision Criteria 215

would you respond to your CFO if she instructed you to use the IRR technique to make

capital budgeting decisions on projects with cash flow streams that alternate between

inflows and outflows?

Q8-11. Outline the differences between NPV, IRR, and PI. What are the advantages and

disadvantages of each technique? Do they agree with regard to simple accept or reject

decisions?

A8-11. The NPV is calculated by discounting all of a project’s cash flows to the present. The IRR

is calculated by finding the discount rate which equates the NPV to zero. The profitability

Q8-12. Under what circumstances will the NPV, IRR, and PI techniques provide different capital

budgeting decisions? What are the underlying causes of the differences often found in the

ranking of mutually exclusive projects using NPV and IRR?

A8-12. IRR, NPV, and PI can lead to different decisions when they are used to rank projects or to

Solutions to End-of-Chapter Problems

Payback Methods

P8-1. Suppose that a 30-year U.S. Treasury bond offers a 4% coupon rate, paid semiannually.

The market price of the bond is $1,000, equal to its par value.

a. What is the payback period for this bond?

b. With such a long payback period, is the bond a bad investment?

c. What is the discounted payback period for the bond assuming its 4% coupon rate is the

required return? What general principle does this example illustrate regarding a

project’s life, its discounted payback period, and its NPV?

A8-1. a. Payback on this bond is 25 years. You pay $1,000. You receive $40 a year for 25

216 Instructor’s Manual

P8-2. The cash flows associated with three different projects are as follows:

Cash Flows

Alpha

($ in millions)

Beta

($ in millions)

Gamma

($ in millions)

Initial Outflow

– 1.5

– 0.4

– 7.5

Year 1

0.3

0.1

2.0

Year 2

0.5

0.2

3.0

Year 3

0.5

0.2

2.0

Year 4

0.4

0.1

1.5

Year 5

0.3

– 0.2

5.5

a. Calculate the payback period of each investment.

b. Which investments does the firm accept if the cutoff payback period is three years?

Four years?

e. One of these almost certainly should be rejected, but might be accepted if the firm uses

payback analysis. Which one?

f. One of these projects almost certainly should be accepted (unless the firm’s

opportunity cost of capital is very high), but might be rejected if the firm uses payback

analysis. Which one?

A8-2. a. Payback of Alpha = 3.5 years, payback of Beta = 2.5 years, payback of Gamma = 3.3

years

e. Project Beta should be rejected. You must pay out a total of .6 million and take in .6