5Chapter 8 CFIN6

Chapter 8 Solutions

8-1 a.

r

ˆ

= (0.2)(19%) + (0.7)(9%) + (0.1)(4%) = 10.5%

8-2 a.

r

ˆ

= (0.45)(32%) + (0.35)(-4%) + (0.2)(–20%) = 9.0%

8-3 a.

A

ˆ

r

= (0.3)(30%) + (0.2)(10%) + (0.5)(-2%) = 10%

B

ˆ

r

= (0.3)(5%) + (0.2)(15%) + (0.5)(25%) = 17%

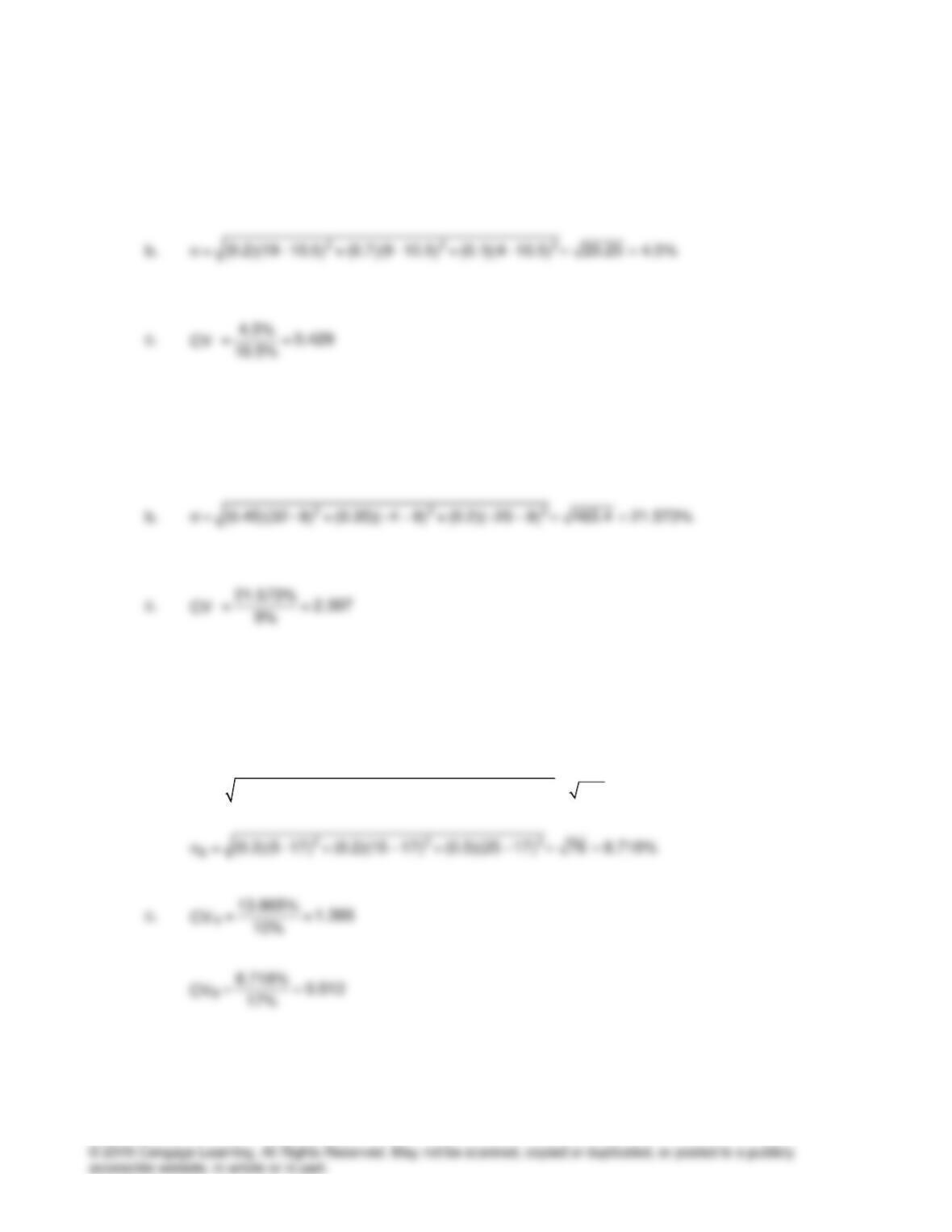

b.

2 2 2

A = (0.3)(30 –10 + (0.2)(10 10 + (0.5)( 2 10 192 13.856%

) ) )

− − − = =

Chapter 8 CFIN6

8-4 To answer the question, the coefficient of variation for each investment must be computed.

Investment

ˆ

r

CV

Stock M 6.0% 4.0% 0.667 = 4%/6%

8-5 To answer the question, the coefficient of variation for each investment must be computed.

Investment

ˆ

r

CV

F 16.0% 7.0% 0.438 = 7%/16%

G 27.0 13.0 0.481 = 13%/27%

8-6 $9,000 invested in one stock with an 18 percent expected return

$21,000 invested in a second stock with an 8 percent expected return

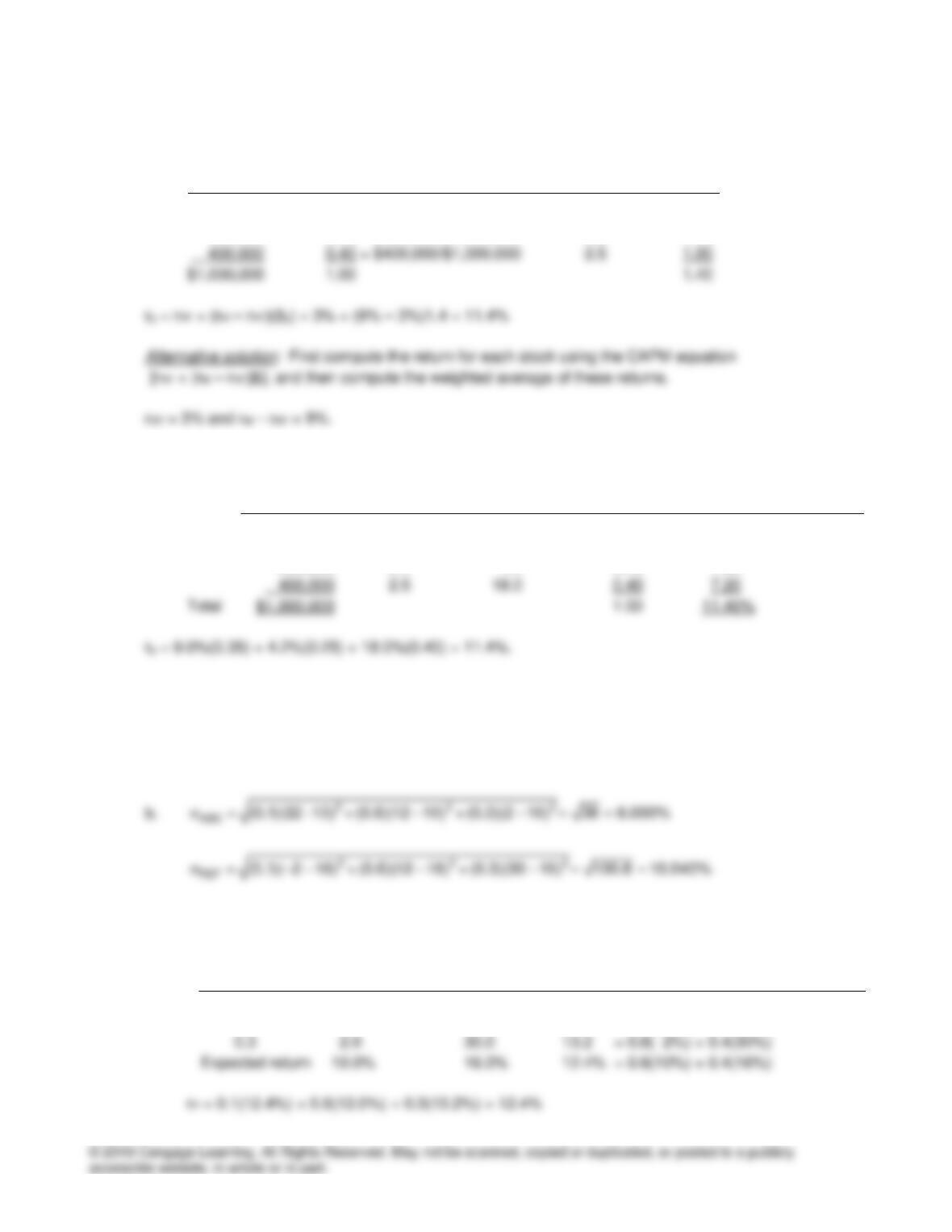

8-7 Portfolio return:

Amount Weight Return Portfolio Return

Investment (1) (2) (3) (4) = (2) x (3)

DEF $ 30,000 0.30 = $30,000/$100,000 4.0% 1.2%

Chapter 8 CFIN6

8-8 Portfolio beta:

Investment Weight Beta Portfolio beta

(1) (2) (3) (4) = (2) x (3)

$ 350,000 0.35 = $350,000/$1,000,000 1.0 0.35

250,000 0.25 = $250,000/$1,000,000 0.2 0.05

rj = rRF + (rM – rRF)βj

Investment Beta = 3% + (9% – 3%)βj Weight rP

(1) (2) (3) (4) (5) = (3) x (4)

$ 350,000 1.0 9.0% 0.35 3.15%

8-9 a.

ABC

ˆ

r

= (0.1)(22%) + (0.6)(12%) + (0.3)(2%) = 10.0%

RST

ˆ

r

= (0.1)(-2%) + (0.6)(12%) + (0.3)(30%) = 16.0%

c. Compute the expected return of the portfolio

Probability rABC rRST Portfolio Return: 60% ABC; 40% RST

0.1 22.0% –2.0% 12.4% = 0.6(22%) + 0.4(–2%)

0.6 12.0 12.0 12.0 = 0.6(12%) + 0.4(12%)

Chapter 8 CFIN6

2 2 2

P = (0.1)(12.4 –12.4 + (0.6)(12 12.4 + (0.3)(13.2 12.4 0.288 0.537%

) ) )

− − = =

8-10 Total investment = $60,000

ws = 0.40

wX = 0.60

βs = 1.5

βP = 2.1

8-11

new $40,000 $10,000

1.2 2.2 1.2(0.8) 2.2(0.2) 1.4

$40,000 $10,000 $40,000 $10,000

= + = + =

++

8-12 Information that is given:

Total current value $120,000

Number of stocks (current portfolio) 4

Beta coefficient, βCurrent 0.8

Chapter 8 CFIN6

8-13 Information that is given:

Total current value $200,000

Number of stocks (current portfolio) 6

Beta coefficient, βCurrent 1.5

Because the beta coefficient for the portfolio will be 1.3 after the stock is sold for $40,000, we know that

the remaining stocks, which are worth $160,000 = $200,000 – $40,000, must have a weighted average

8-14 rRF = 3%

RRM = 6%

β = 1.5

r = 3% + (6%)1.5 = 12%

8-15 rRF = 4%

8-16 rRF = ?

rM = 12.5%

β = 0.8

rZR = 11%

11% = rRF + (12.5% – rRF)0.8

Chapter 8 CFIN6

8-17 rRF = 5%

rM = 11%

βV = 2.0

βW = 0.5

8-18 Original information:

rQ = 11%

rRF = 4%

rM = 9%

Based on this information, we can compute the stock’s beta coefficient:

8-19 Given information:

rRF = 3.5%

RPM = 7%

βU = 0.9

U$1.75(1.04)

$28

In this case, the expected rate of return,

U

ˆ

r

, is greater than the required rate of return, rU, which means

the $28 selling price is too low. Investors should want to buy the stock, which will increase the price of

the stock to its equilibrium value of $31.38:

Chapter 8 CFIN6

0$1.75(1.04) $1.82

ˆ

P $31.38

0.098 0.04 0.058

= = =

−

8-20 Given information:

P0 = $37.50

D0 = $2

$37.50 0.106 g

=−

=−

=

= = =

$37.50 0.106 g

$39.50g $1.975

$1.975

g 0.05 5.0%

$39.50