To calculate the HPY, we need to find the interest rate that equates the price we paid for the bond

with the cash flows we received. The cash flows we received were $54 each year for two years,

31. The price of any bond (or financial instrument) is the PV of the future cash flows. Even though Bond

M makes different coupons payments, to find the price of the bond, we find the PV of the cash flows.

The PV of the cash flows for Bond M is:

32. In general, this is not likely to happen, although it can (and did). The reason this bond has a negative

YTM is that it is a callable U.S. Treasury bond. Market participants know this. Given the high coupon

33. To find the present value, we need to find the real weekly interest rate. To find the real return, we need

to use the effective annual rates in the Fisher equation. So, we find the real EAR is:

(1 + R) = (1 + r)(1 + h)

1 + .075 = (1 + r)(1 + .032)

r = .0417, or 4.17%

34. To answer this question, we need to find the monthly interest rate, which is the APR divided by 12.

We also must be careful to use the real interest rate. The Fisher equation uses the effective annual rate,

so, the real effective annual interest rates and the monthly interest rates for each account are:

Stock account:

(1 + R) = (1 + r)(1 + h)

1 + .07 = (1 + r)(1 + .04)

r = .0288, or 2.88%

APR = m[(1 + EAR)1/m – 1]

APR = 12[(1 + .0288)1/12 – 1]

APR = .0285, or 2.85%

Now we can find the future value of the retirement account in real terms. The future value of each

account will be:

Stock account:

FVA = C {(1 + r )t – 1]/r}

Bond account:

FVA = C {(1 + r )t – 1]/r}

The total future value of the retirement account will be the sum of the two accounts, or:

Account value = $1,196,731.96 + 170,316.78

Account value = $1,367,048.74

Now we need to find the monthly interest rate in retirement. We can use the same procedure that we

used to find the monthly interest rates for the stock and bond accounts, so:

Now we can find the real monthly withdrawal in retirement. Using the present value of an annuity

equation and solving for the payment, we find:

PVA = C({1 – [1/(1 + r)]t }/r )

35. In this problem, we need to calculate the future value of the annual savings after the five years of

operations. The savings are the revenues minus the costs, or:

Savings = Revenue – Costs

Since the annual fee and the number of members are increasing, we need to calculate the effective

growth rate for revenues, which is:

The revenue will grow at 9.18 percent, and the costs will grow at 2 percent, so the savings each year

for the next five years will be:

Year

Revenue

Costs

Savings

1

$305,704.00

$127,500.00

$178,204.00

2

333,767.63

130,050.00

203,717.63

3

364,407.50

132,651.00

231,756.50

4

397,860.10

135,304.02

262,556.08

5

434,383.66

138,010.10

296,373.56

Now we can find the value of each year’s savings using the future value of a lump sum equation, so:

FV = PV(1 + r)t

Year

Future Value

1

$178,204.00(1 + .09)4 =

$251,549.49

2

$203,717.63(1 + .09)3 =

263,820.24

3

$231,756.50(1 + .09)2 =

275,349.89

4

5

Total future value of savings =

He will spend $500,000 on a luxury boat, so the value of his account will be:

Value of account = $1,373,279.31 – 500,000

1.

a.

Enter

40

3%

$1,000

N

I/Y

PV

PMT

FV

Solve for

b.

Enter

40

4%

$1,000

N

I/Y

PV

PMT

FV

Solve for

Enter

40

5%

$1,000

Solve for

2.

a.

Enter

30

3.5%

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

b.

Enter

30

4.5%

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

Enter

30

2.5%

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

3.

Enter

26

±$980

$31

$1,000

N

I/Y

PV

PMT

FV

Solve for

4.

Enter

23

$1,000

N

I/Y

PV

PMT

FV

Solve for

$37.49

$37.49 2 = $74.97

5.

6.

Enter

Solve for

16.

P0

Enter

40

2.85%

$1,000

N

I/Y

PV

PMT

FV

Solve for

Enter

38

2.85%

$1,000

N

I/Y

PV

PMT

FV

Solve for

17. Miller Corporation

P0

Enter

26

2.65%

$32.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,111.71

P1

Enter

24

2.65%

$32.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,105.55

P3

Enter

20

2.65%

$32.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,092.22

P8

Enter

10

2.65%

$32.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,052.11

Enter

2.65%

$32.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,011.54

Enter

Solve for

Modigliani Company

P0

Enter

26

3.25%

$26.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$895.76

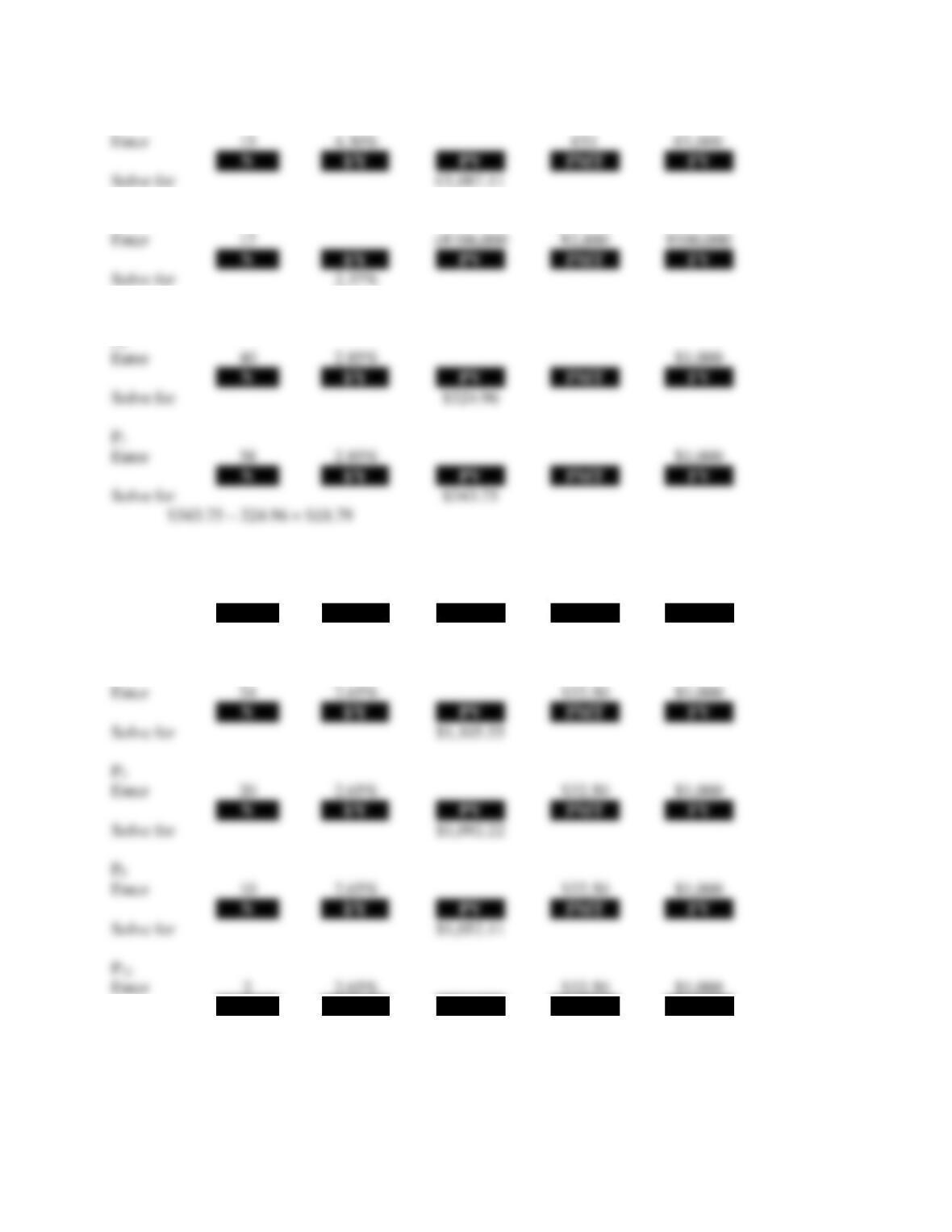

18. If both bonds sell at par, the initial YTM on both bonds is the coupon rate, 5.8 percent. If the YTM

suddenly rises to 7.8 percent:

PLaurel

Enter

6

3.90%

$29

$1,000

N

I/Y

PV

PMT

FV

Solve for

$947.41

PHardy

Enter

40

3.90%

$29

$1,000

N

I/Y

PV

PMT

FV

Solve for

PLaurel

Enter

6

1.90%

$29

$1,000

N

I/Y

PV

PMT

FV

Solve for

P1

Enter

24

3.25%

$26.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$901.07

P3

Enter

20

3.25%

$26.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$912.76

P8

Enter

10

3.25%

$26.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$949.47

P12

Enter

3.25%

$26.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$988.56

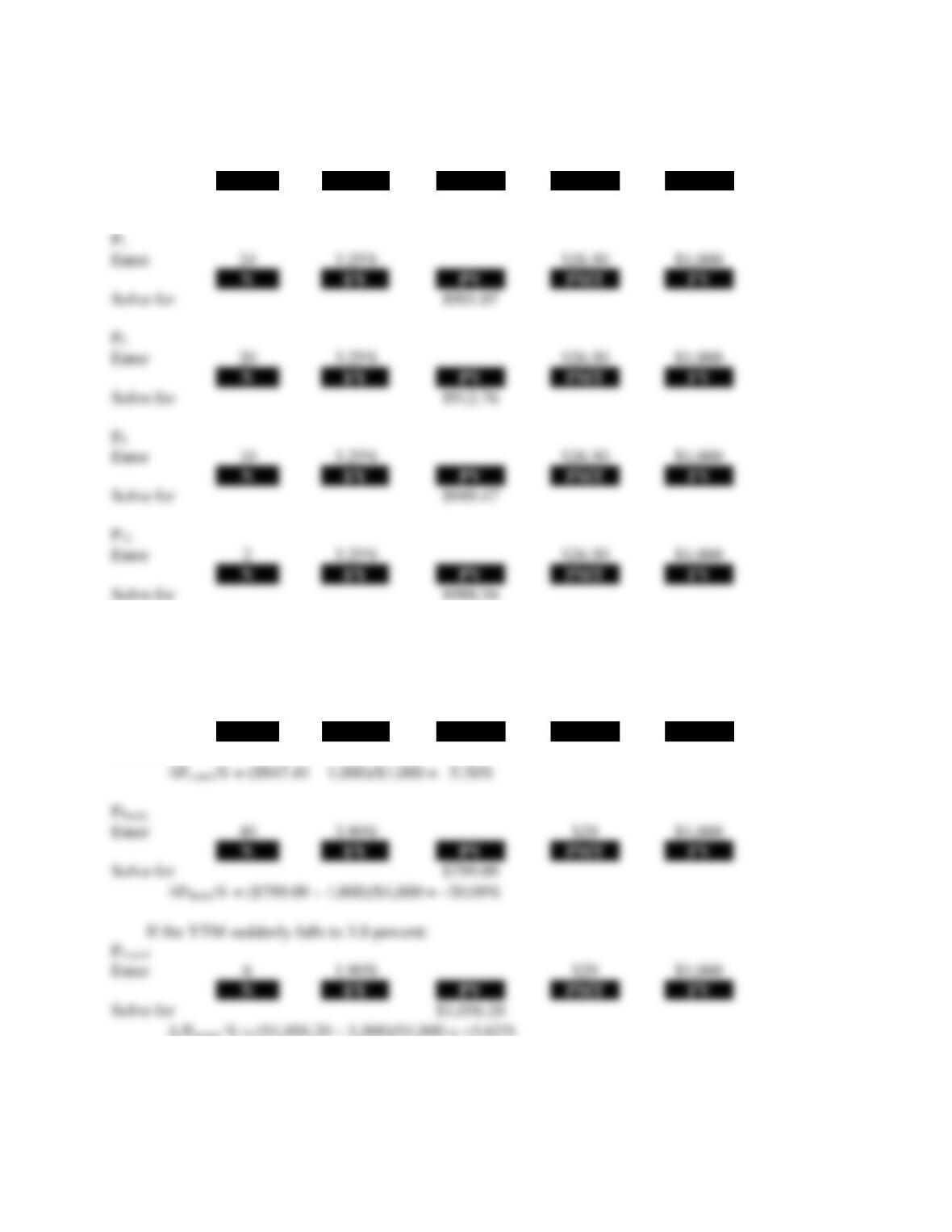

19. Initially, at a YTM of 9 percent, the prices of the two bonds are:

PFaulk

Enter

24

4.5%

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

$855.05

PYoo

Enter

24

4.5%

$55

$1,000

N

I/Y

PV

PMT

FV

Solve for

Enter

N

I/Y

PV

PMT

FV

Solve for

PYoo

Enter

Solve for

Enter

Solve for

PYoo

Enter

24

3.5%

$55

$1,000

N

I/Y

PV

PMT

FV

Solve for

Enter

Solve for

20.

21. The company should set the coupon rate on its new bonds equal to the required return; the required

return can be observed in the market by finding the YTM on outstanding bonds of the company.

Enter

40

$28.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

24. Current yield = .0842 = $90/P0 ; P0 = $1,068.88

Enter

7.81%

±$1,068.88

$90

$1,000

N

I/Y

PV

PMT

FV

Solve for

25.

Enter

24

±$964.12

$36.20

$1,000

N

I/Y

PV

PMT

FV

Solve for

27.

a. Po

Enter

50

5.9%/2

$1,000

N

I/Y

PV

PMT

FV

Solve for

b. P1

Enter

48

5.9%/2

$1,000

N

I/Y

PV

PMT

FV

Solve for

P24

Enter

2

5.9%/2%

$1,000

N

I/Y

PV

PMT

FV

Solve for

Enter

26

$29.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

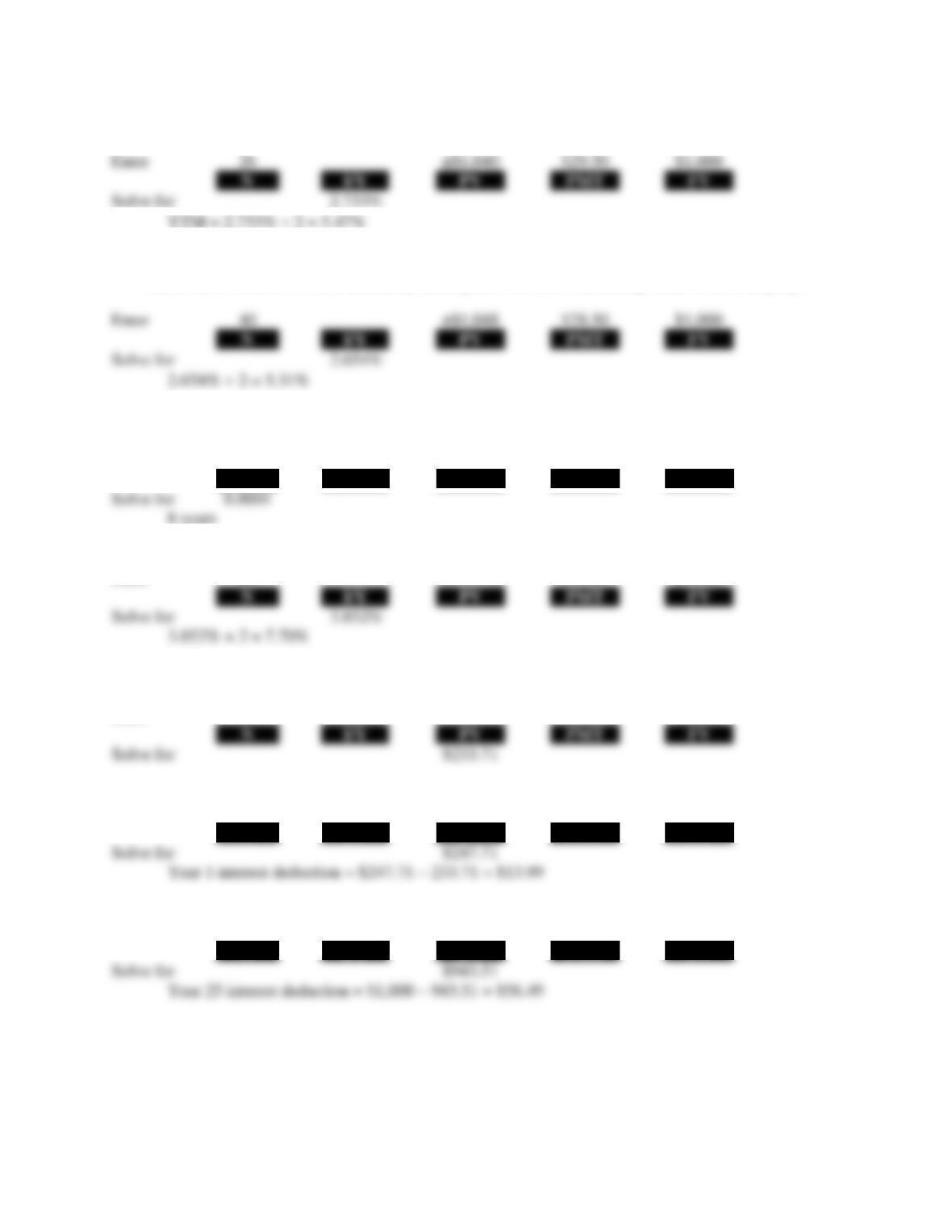

28. a. The coupon bonds have a 7% coupon rate, which matches the 7% required return, so they will

sell at par; # of bonds = $50,000,000/$1,000 = 50,000.

For the zeroes:

Enter

60

7%/2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$126.93

$50,000,000/$126.93 = 393,905 will be issued.

Enter

58

7%/2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$135.98

Year 1 interest deduction = $135.98 – 126.93 = $9.04

29.

Bond P

P0

Enter

10

6.5%

$80

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,107.83

P1

Enter

6.5%

$80

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,099.84

P0

Enter

N

I/Y

PV

PMT

FV

Solve for

$892.17

30.

a.

Enter

10

±$940

$54

$1,000

N

I/Y

PV

PMT

FV

Solve for

6.22%

Enter

5.22%

N

I/Y

PV

PMT

FV

Solve for

Enter

Solve for

9.37%

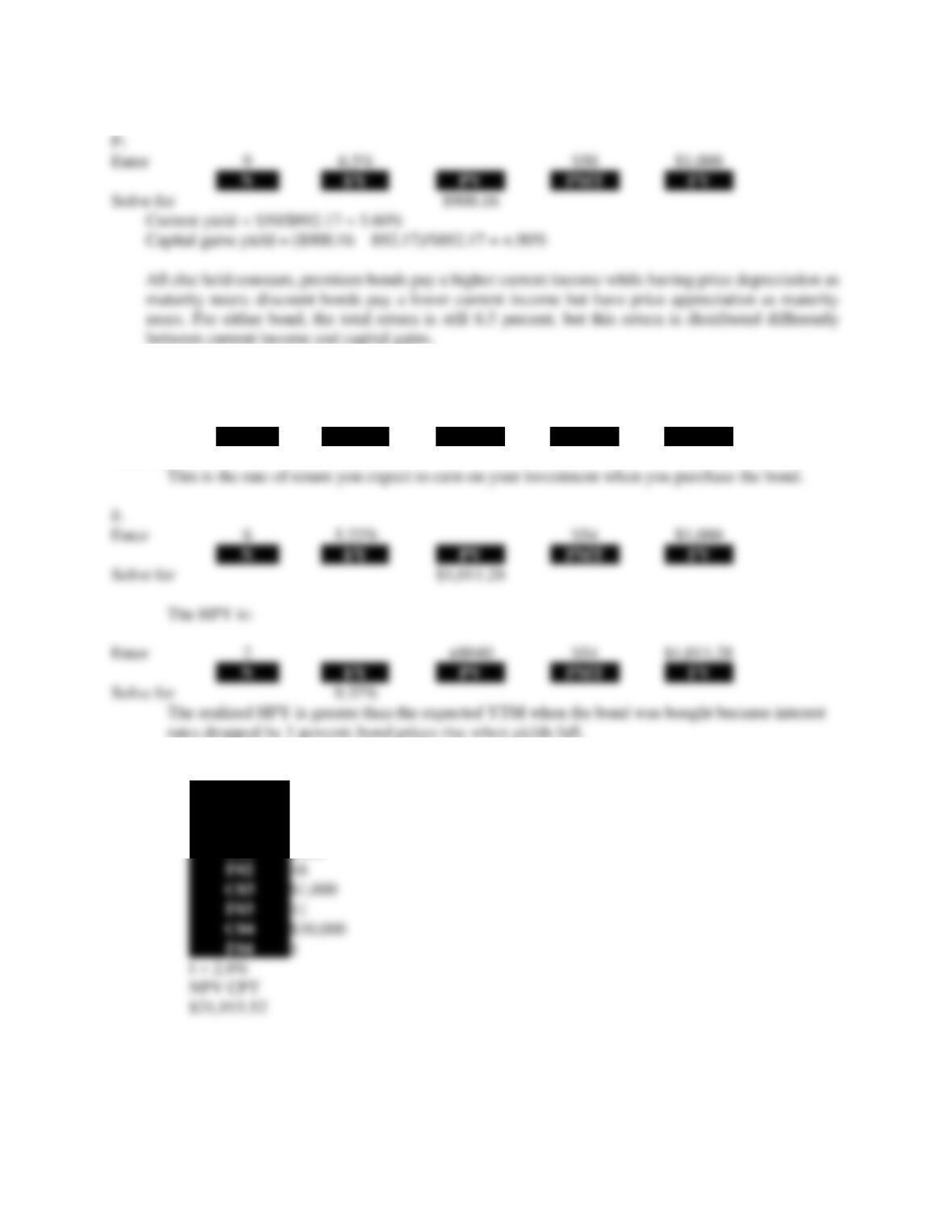

31.

PM

CFo

$0

C01

$0

F01

12

C02

$800

16

C03

$1,000

11

C04

$30,000

1

I = 2.8%

NPV CPT

$21,915.52

P1

Enter

Solve for

PN

Enter

40

2.8%

$30,000

N

I/Y

PV

PMT

FV

Solve for

$9,940.24

Enter

7.69%

12

NOM

EFF

C/Y

Solve for

Enter

2.88%

12

NOM

EFF

C/Y

Solve for

2.85%

Enter

3.85%

12

NOM

EFF

C/Y

Solve for

3.78%

Stock portfolio value:

Enter

12 × 30

7.43%/12

$900

N

I/Y

PV

PMT

FV

Solve for

$1,196,731.96

Enter

12 × 30

2.85%/12

$300

N

I/Y

PV

PMT

FV

Solve for

Retirement withdrawal:

Enter

25 × 12

3.78%/12

$1,367,048.74

N

I/Y

PV

PMT

FV

Solve for

$7,050.75

Enter

30 + 25

$7,050.75

N

I/Y

PV

PMT

FV

Solve for

35.

Future value of savings:

Year 2:

Enter

3

9%

$203,717.63

N

I/Y

PV

PMT

FV

Solve for

$263,820.24

Year 3:

Enter

2

9%

$231,756.50

N

I/Y

PV

PMT

FV

Solve for

$275,349.89

Enter

1

9%

$262,556.08

N

I/Y

PV

PMT

FV

Solve for

$286,186.13

Enter

9%

$873,279.31

N

I/Y

PV

PMT

FV

Solve for

Enter

4

9%

N

I/Y

PV

PMT

FV

Solve for

$251,549.49