MTB PROPOSED PLAN

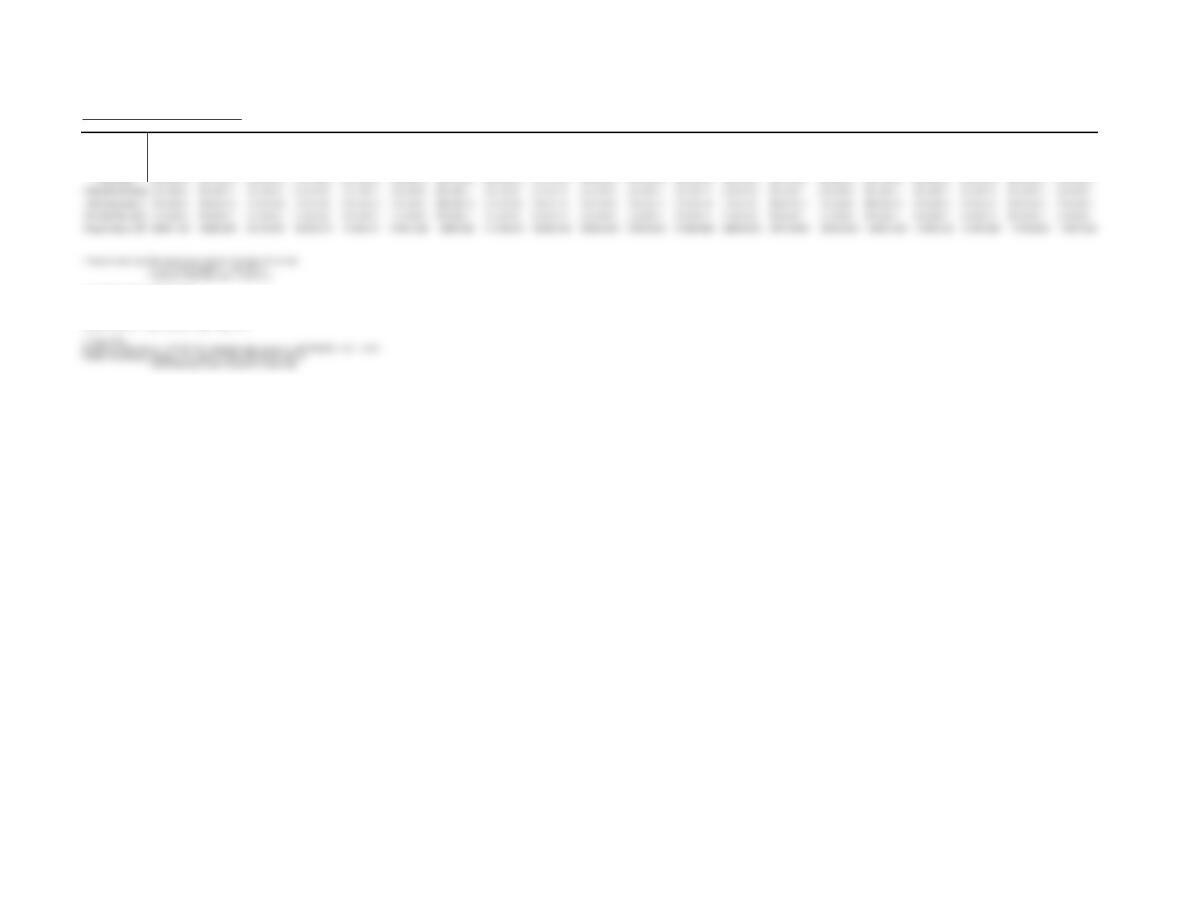

YEAR –> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

∆ Revenue $1,510,056.50 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00 $658,984.00

∆ Costs $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40 $415,705.40

Unit Price is based off average unit price of 1 adult, 2 children:

Unit Price = ($5.00 + $3.50 + $3.50) / 3 = $4.00

∆ Revenue = 34,642 adults @ $5.00 = $173,210.00

69,284 children @ $3.50 = $242,494.00

∆ Costs = $212,000.00 Operation Costs + $203,705.40 Revenue Bond Payment (PMT) = $415,705.40

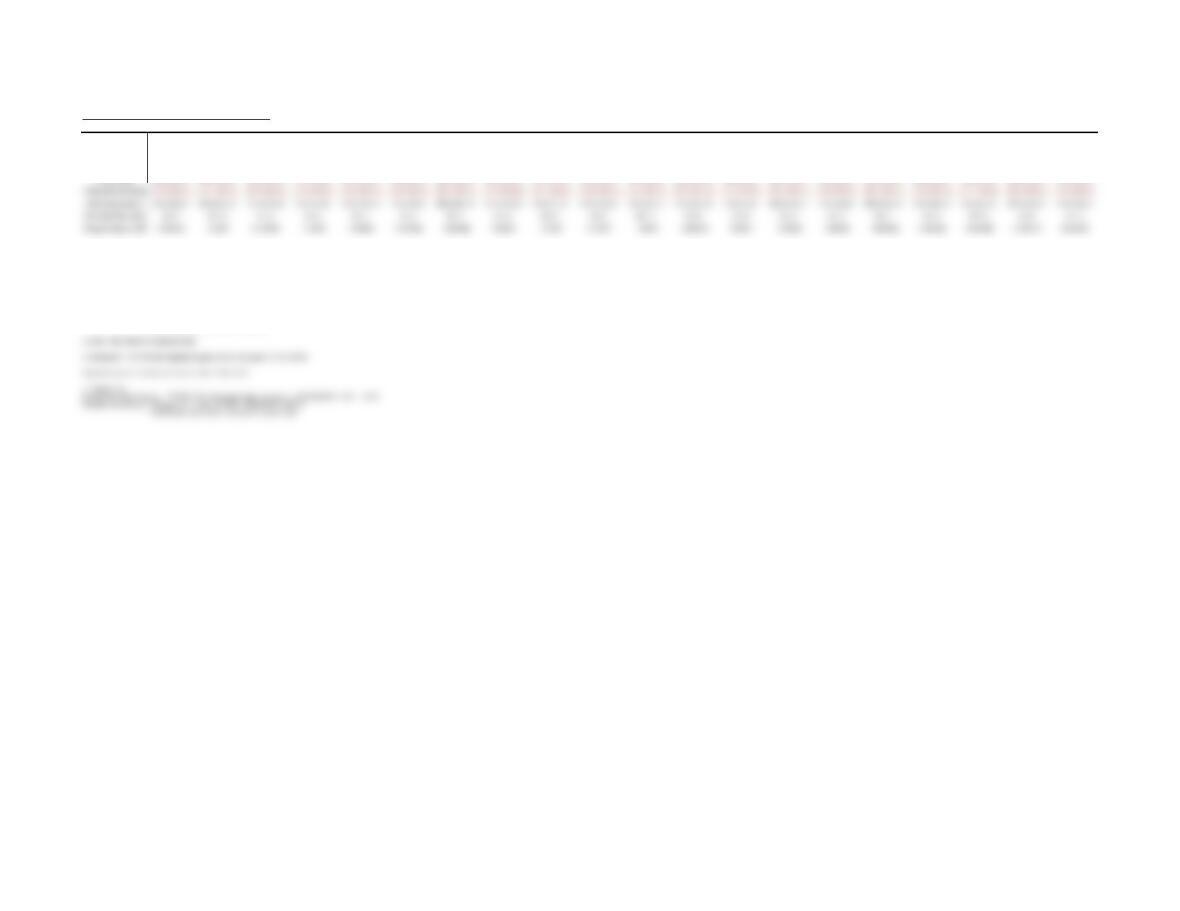

REVENUE BOND – BREAK EVEN ANALYSIS

YEAR –> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

∆ Revenue $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01 $588,865.01

∆ Costs $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00

Revenue Bond Payment = PVA / PVFA 20 years @8% = $3,700,000.00 / 9.8181 = $376,855.00

∆ Revenue based upon Break Even Analysis (1/3 adults, 2/3 children)

Break Even Attendance = ($212,000.00 Operating Costs + $376,855.00 Revenue Bond Payment (PMT)) / $4.00 Unit Price

Break Even Attendance = $588,855.00 / $4.00 = 147,213.75 or 147,214 people

Unit Price is based off average unit price of 1 adult, 2 children:

Present Value of CF = Net Cash Flow x (Year “X” @ 8%)

REVENUE BOND – MAX ATTENDANCE

YEAR –> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

∆ Revenue $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01

∆ Costs $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00 $588,855.00

Revenue Bond Payment = PVA / PVFA 20 years @8% = $3,700,000.00 / 9.8181 = $376,855.00

∆ Revenue based upon Max Attendance of 250,000 (1/3 adults, 2/3 children)

∆ Costs = $212,000.00 Operation Costs + $376,855.00 Revenue Bond Payment (PMT) = $588,855.00

∆ Depreciation = $3,700,000 Revenue Bond / 20 years = $185,000.00

Present Value of CF = Net Cash Flow x (Year “X” @ 8%)

########

GENERAL OBLIGATION BOND – MAX ATTENDANCE

YEAR –> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

∆ Revenue $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01 $950,000.01

∆ Costs $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00

∆ Depreciation $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00

∆ Total Costs $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00

∆ Costs = $212,000.00 Operation Costs

∆ Depreciation = $3,700,000 General Obligation Bond / 20 years = $185,000.00

Present Value of CF = Net Cash Flow x (Year “X” @ 7.5%)

GENERAL OBLIGATION BOND – BREAK EVEN ATTENDANCE

YEAR –> 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

∆ Revenue $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15 $212,000.15

∆ Costs $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00 $212,000.00

∆ Depreciation $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00 $185,000.00

∆ Total Costs $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00 $397,000.00

∆ Revenue based upon Break Even Analysis (1/3 adults, 2/3 children)

Break Even Attendance = ($212,000.00 Operating Costs) / $4.00 Unit Price

Break Even Attendance = 53,000

Unit Price is based off average unit price of 1 adult, 2 children:

Unit Price = ($5.00 + $3.50 + $3.50) / 3 = $4.00

∆ Revenue = 17,666.67 adults @ $5.00 = $88,333.50

35,333.33 children @$3.50 = $123,666.65