So, the sensitivity of the NPV to changes in the price of the new club is:

NPV/P = ($15,165,779.21 – 16,795,335.05)/($950 – 960)

NPV/P = $162,955.58

For every dollar increase (decrease) in the price of the clubs, the NPV increases (decreases) by

$162,955.58.

To calculate the sensitivity of the NPV to changes in the quantity sold of the new club, we need to

change the quantity sold. We will choose 51,000 units, but the choice is irrelevant as the sensitivity

will be the same no matter what quantity we choose.

For the variable costs, we must include the units gained or lost from the existing clubs. Note that the

variable costs of the expensive clubs are an inflow. If we are not producing the sets any more, we will

save these variable costs, which is an inflow. So:

Var. costs

New clubs

–$415 51,000 = –$21,165,000

Exp. clubs

The pro forma income statement will be:

Sales

$41,100,000

Variable costs

18,375,000

Fixed costs

9,400,000

Depreciation

EBT

Taxes

Net income

Using the bottom up OCF calculation, we get:

Sales

Cheap clubs

The NPV at this quantity is:

NPV = –$29,400,000 – $2,400,000 + $11,135,000(PVIFA14%,7) + $2,400,000/1.147

17. a. The base-case NPV is:

b. We would abandon the project if the cash flow from selling the equipment is greater than the

present value of the future cash flows. We need to find the sale quantity where the two are equal,

so:

$810,000 = ($43)Q(PVIFA16%,9)

18. a. If the project is a success, the present value of the future cash flows will be:

PV future CFs = $43(9,100)(PVIFA16%,9)

PV future CFs = $1,802,540.62

From the previous question, if the quantity sold is 3,700, we would abandon the project, and the

cash flow would be $810,000. Since the project has an equal likelihood of success or failure in

b. If we couldn’t abandon the project, the present value of the future cash flows when the quantity

is 3,800 will be:

PV future CFs = $43(3,700)(PVIFA16%,9)

PV future CFs = $732,901.13

19. If the project is a success, the present value of the future cash flows will be:

PV future CFs = $43(18,200)(PVIFA16%,9)

PV future CFs = $3,605,081.24

If the sales are only 3,700 units, from Problem #17, we know we will abandon the project, with a value

of $810,000. Since the project has an equal likelihood of success or failure in one year, the expected

20. a. The accounting break-even is the aftertax sum of the fixed costs and depreciation charge divided

by the contribution margin (selling price minus variable cost). In this case, there are no fixed

QA = 610.17, or about 610 units

b. When calculating the financial break-even point, we express the initial investment as an

equivalent annual cost (EAC). The initial investment is the $20,000 in licensing fees. Dividing

the initial investment by the three-year annuity factor, discounted at 12 percent, the EAC of the

initial investment is:

EAC = Initial Investment/PVIFA12%,3

EAC = $20,000/2.4018

21. The payoff from taking the lump sum is $25,000, so we need to compare this to the expected payoff

from taking 1.25 percent of the profit. The decision tree for the movie project is:

Big audience

40%

$45,000,000

Movie is

good

Make

The value of 1.25 percent of the profits is as follows. There is a 40 percent probability the movie is

good, and the audience is big, so the expected value of this outcome is:

Value = $45,000,000 × .40

Value = $18,000,000

The value if the movie is good, and has a big audience, assuming the script is good is:

Script is

60%

No profit

22. We can calculate the value of the option to wait as the difference between the NPV of opening the

mine today and the NPV of waiting one year to open the mine. The remaining life of the mine is:

33,600 ounces/4,200 ounces per year = 8 years

This will be true no matter when you open the mine. The aftertax cash flow per year if opened today

is:

CF = 4,200($900) = $3,780,000

23. a. The NPV of the project is the sum of the present value of the cash flows generated by the project.

The cash flows from this project are an annuity, so the NPV is:

b. The company should abandon the project if the PV of the revised cash flows for the next nine

years is less than the project’s aftertax salvage value. Since the option to abandon the project

occurs in Year 1, discount the revised cash flows to Year 1 as well. To determine the level of

expected cash flows below which the company should abandon the project, calculate the

C2 = $5,456,329.25

24. a. The NPV of the project is sum of the present value of the cash flows generated by the project.

The annual cash flow for the project is the number of units sold times the cash flow per unit,

which is:

Annual cash flow = 20($235,000)

Annual cash flow = $4,700,000

b. The company will abandon the project if unit sales are not revised upward. If the unit sales are

revised upward, the aftertax cash flows for the project over the last four years will be:

New annual cash flow = 30($235,000)

New annual cash flow = $7,050,000

25. To calculate the unit sales for each scenario, we multiply the market sales times the company’s market

share. We can then use the quantity sold to find the revenue each year, and the variable costs each

year. After doing these calculations, we will construct the pro forma income statement for each

scenario. We can then find the operating cash flow using the bottom up approach, which is net income

plus depreciation. Doing so, we find:

Pessimistic

Expected

Optimistic

Units per year

22,000

27,600

33,000

EBT

$5,666.67

$653,666.67

$1,326,000.00

Tax

1,190.00

137,270.00

278,460.00

Net income

$4,476.67

$516,396.67

$1,047,540.00

OCF

$387,810.00

$874,730.00

$1,372,540.00

Note that under the pessimistic scenario, the taxable income is negative. We assumed a tax credit in

26. a. Using the tax shield approach, the OCF is:

OCF = [($375 – 295)(26,000) – $345,000](.76) + .24($2,900,000/5)

OCF = $1,457,800

And the NPV is:

NPV = –$2,900,000 – 500,000 + $1,457,800(PVIFA13%,5)

Revenue

$3,058,000.00

$3,946,800.00

$4,851,000.00

Variable costs

Fixed costs

Depreciation

b. In the worst-case, the OCF is:

OCFworst = {[($375)(.9) – 295](26,000) – $345,000}(.76) + .24($3,335,000/5)

OCFworst = $737,680

And the worst-case NPV is:

27. To calculate the sensitivity to changes in quantity sold, we will choose a quantity of 27,000. The

OCF at this level of sales is:

OCF = [($375 – 295)(27,000) – $345,000](.76) + .24($2,900,000/5)

OCF = $1,457,800

The sensitivity of changes in the OCF to quantity sold is:

OCF/Q = ($1,457,800 – 1,518,600)/(26,000 – 27,000)

OCF/Q = +$60.80

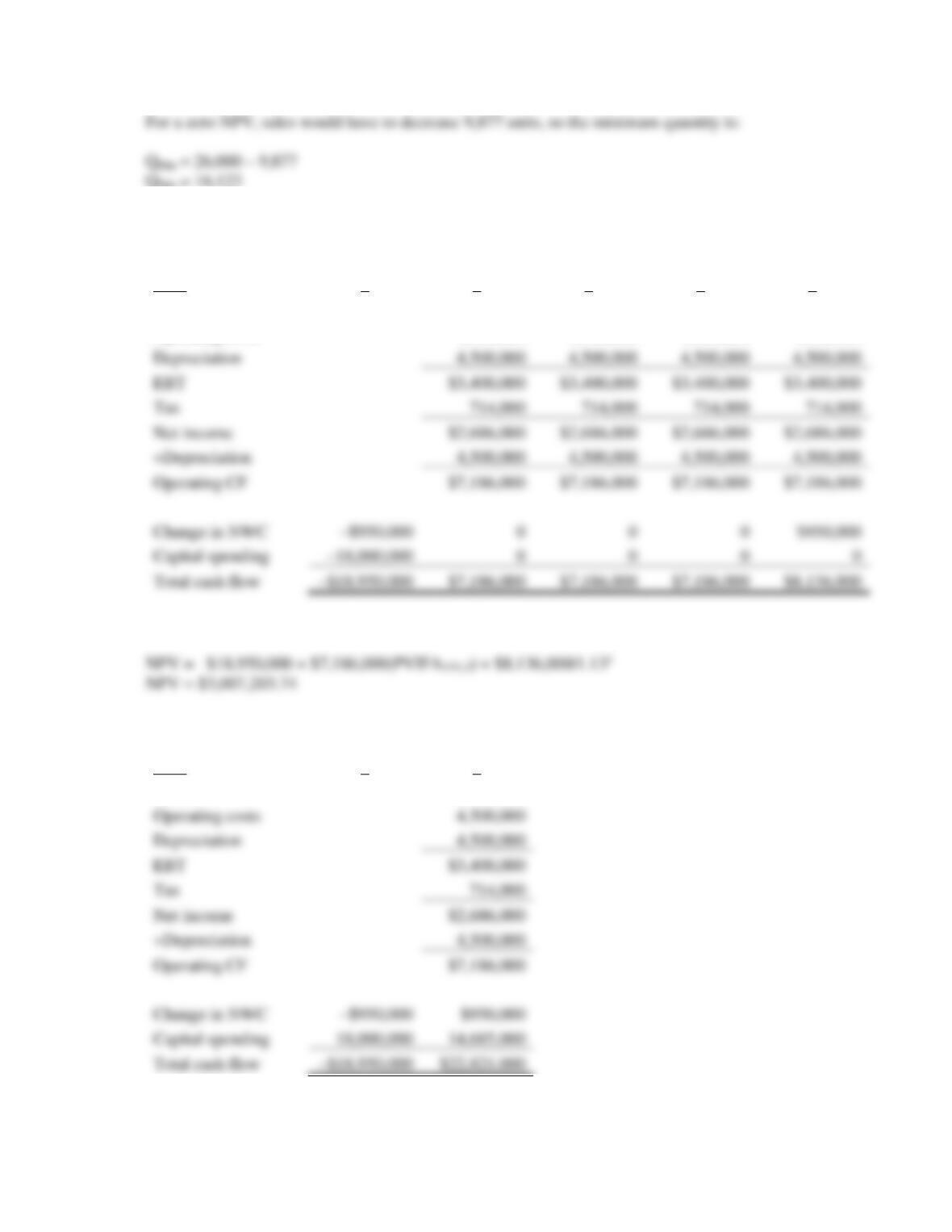

28. We will use the bottom up approach to calculate the operating cash flow. Assuming we operate the

project for all four years, the cash flows are:

Year

0

1

2

3

4

Sales

$12,400,000

$12,400,000

$12,400,000

$12,400,000

Operating costs

4,500,000

4,500,000

4,500,000

4,500,000

Depreciation

4,500,000

4,500,000

4,500,000

4,500,000

Tax

Net income

+Depreciation

Operating CF

Change in NWC

Capital spending

Total cash flow

There is no salvage value for the equipment. The NPV is:

The cash flows if we abandon the project after one year are:

Year

0

1

Sales

$12,400,000

Operating costs

4,500,000

Depreciation

4,500,000

EBT

Tax

Net income

+Depreciation

Operating CF

Change in NWC

Capital spending

Total cash flow

The book value of the equipment is:

Book value = $18,000,000 – (1)($18,000,000/4)

Book value = $13,500,000

So the taxes on the salvage value will be:

If we abandon the project after two years, the cash flows are:

Year

0

1

2

Sales

$12,400,000

$12,400,000

Operating costs

4,500,000

4,500,000

Depreciation

4,500,000

4,500,000

EBT

$3,400,000

$3,400,000

Tax

714,000

714,000

Net income

$2,686,000

$2,686,000

+Depreciation

4,500,000

4,500,000

Operating CF

Change in NWC

Capital spending

Total cash flow

This makes the aftertax salvage value:

If we abandon the project after three years, the cash flows are:

Year

0

1

2

3

Sales

$12,400,000

$12,400,000

$12,400,000

Operating costs

4,500,000

4,500,000

4,500,000

Depreciation

4,500,000

4,500,000

4,500,000

EBT

Tax

Net income

+Depreciation

Operating CF

Change in NWC

–$950,000

0

0

950,000

Capital spending

–18,000,000

0

0

7,660,000

Total cash flow

–$18,950,000

$7,186,000

$7,186,000

$15,796,000

The book value of the equipment is:

29. a. The NPV of the project is the sum of the present value of the cash flows generated by the project.

The cash flows from this project are an annuity, so the NPV is:

b. The company will abandon the project if the value of abandoning the project is greater than the

value of the future cash flows. The present value of the future cash flows if the company revises

its sales downward will be:

30. First, determine the cash flow from selling the old harvester. When calculating the salvage value,

remember that tax liabilities or credits are generated on the difference between the resale value and

the book value of the asset. Using the original purchase price of the old harvester to determine annual

depreciation, the annual depreciation for the old harvester is:

DepreciationOld = $65,000/15

Aftertax salvage value = Market value + TC(Book value – Market value)

Aftertax salvage value = $21,000 + .22($43,333.33 – 21,000)

Aftertax salvage value = $25,913.33

Next, we need to calculate the incremental depreciation. We need to calculate the depreciation tax

shield generated by the new harvester less the forgone depreciation tax shield from the old harvester.

The present value of the incremental depreciation tax shield will be:

The new harvester will generate year-end pre-tax cash flow savings of $13,000 per year for 10 years.

We can find the aftertax present value of the cash flows savings as:

PVSsavings = C1(1 – TC)(PVIFA15%,10)