Mini Case: 7 – 19

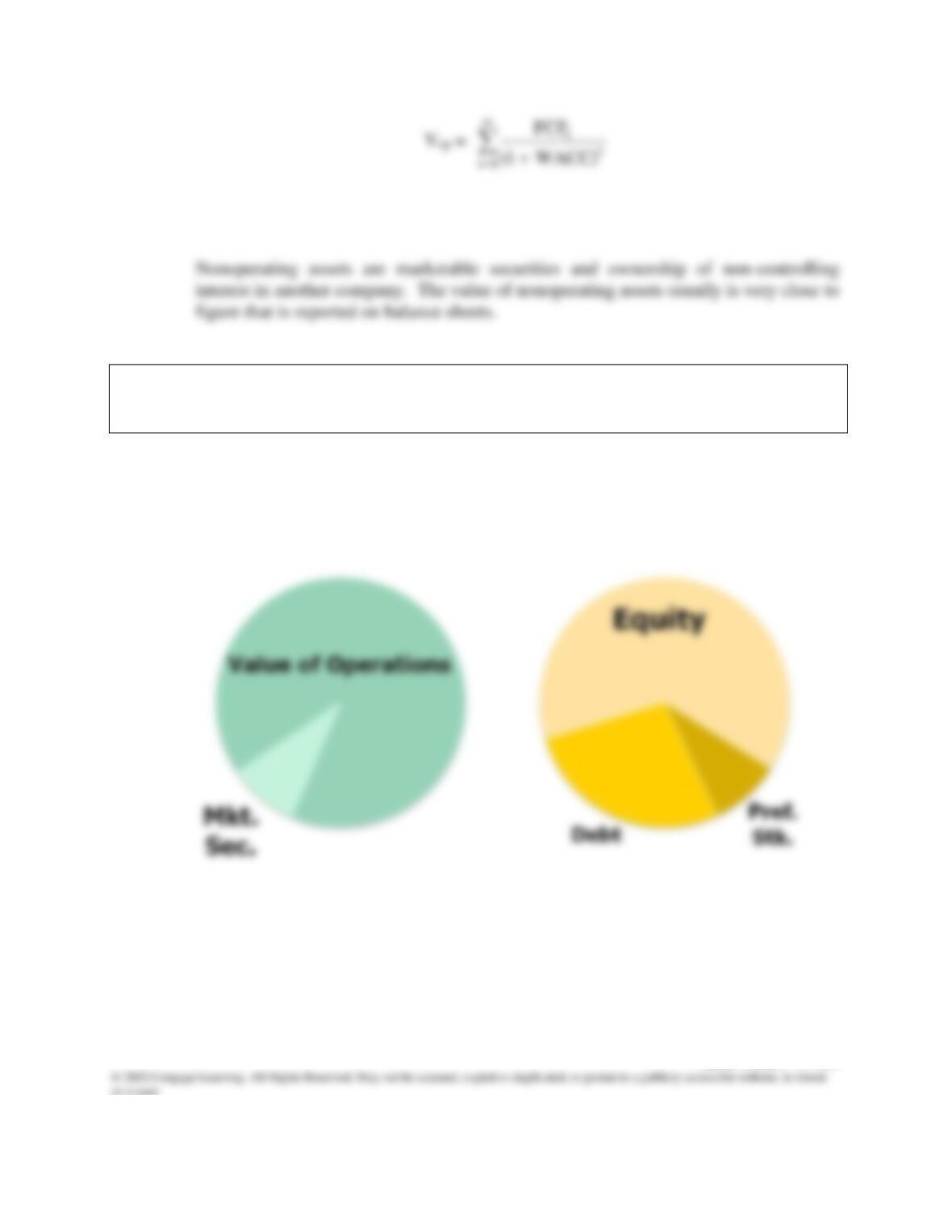

c. Use a pie chart to illustrate the sources that comprise a hypothetical company’s total

value. Using another pie chart, show the claims on a company’s value. How is equity

a residual claim?

Answer: Total corporate value is sum of value of operations and value of nonoperating assets.

Some company’s also have growth options, but assume they are negligible for this

company. Debt holders have first claim. Preferred stockholders have the next claim.

Any remaining value belongs to stockholders.

Mini Case: 7 – 20

d. 1. Suppose the free cash flow at Time 1 is expected to grow at a constant rate of gL

forever. If gL < WACC, what is a formula for the present value of expected free

cash flows when discounted at the WACC?

Answer:

d. 2. If the most recent free cash flow is expected to grow at a constant rate of gL forever

(and gL < WACC), what is a formula for the present value of expected free cash

flows when discounted at the WACC?

Answer:

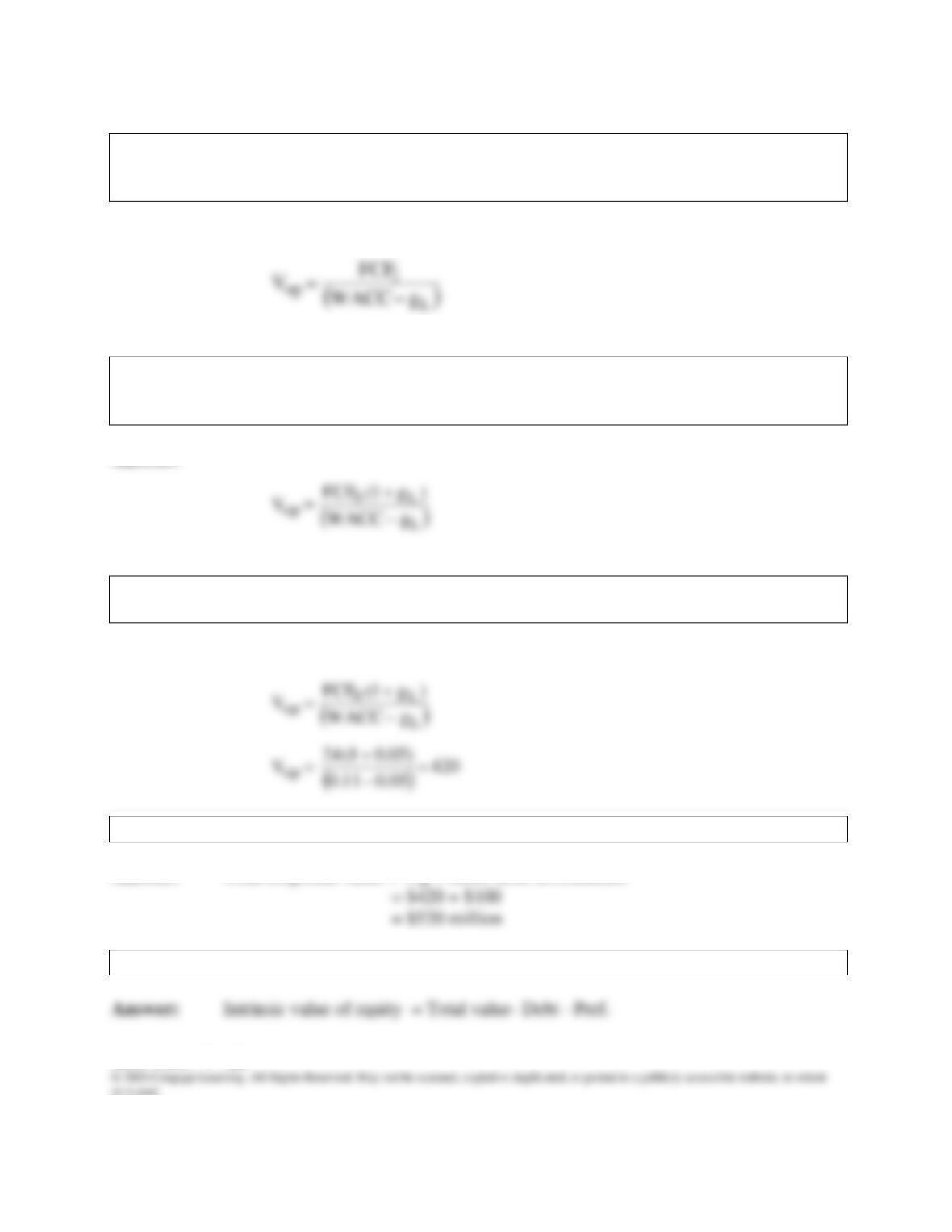

e. 1. Use B&M’s data and the free cash flow valuation model to answer the following

questions. What is its estimated value of operations?

Answer:

e. 2. What is its estimated total corporate value? (This is the entity value.)

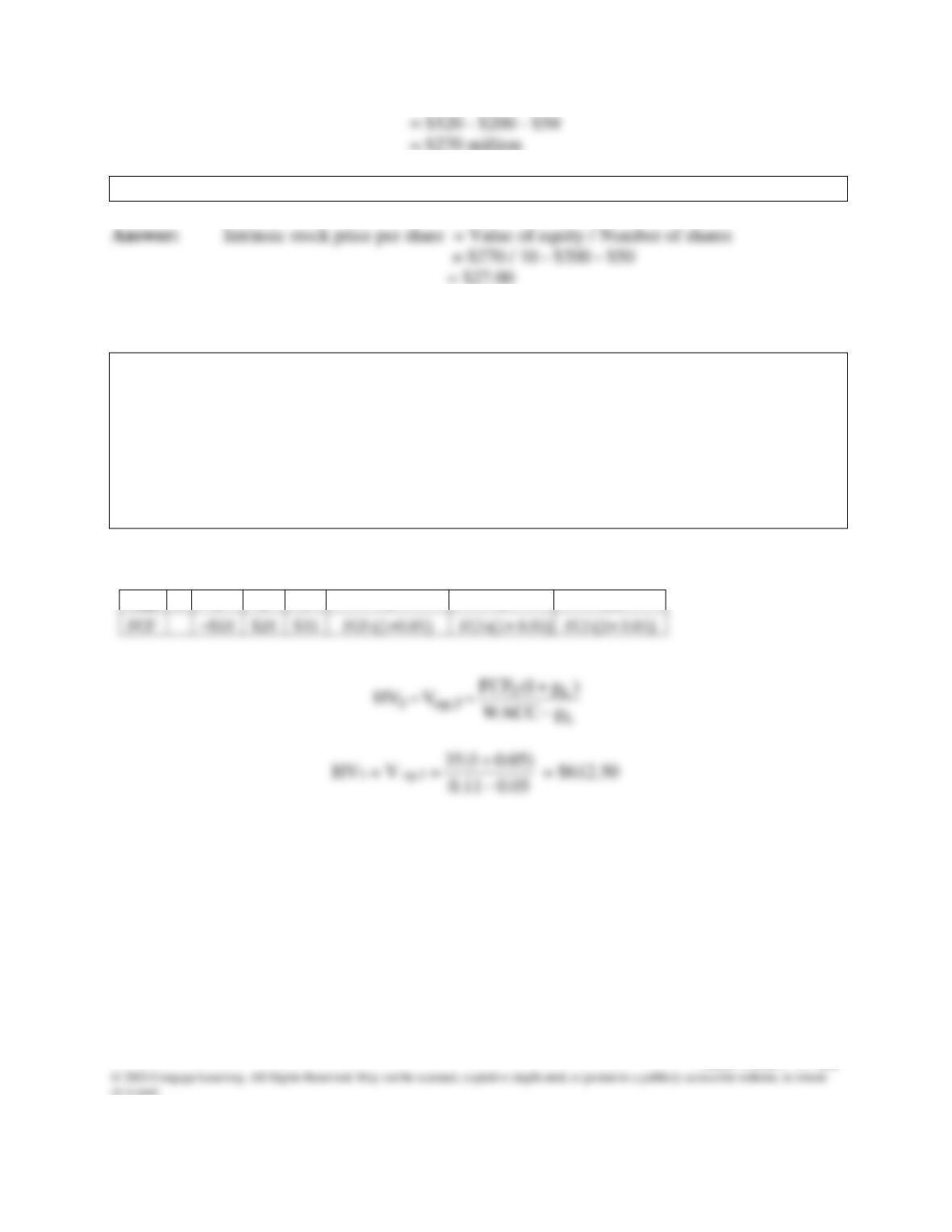

Answer: Total corporate value = Vop + Short-term investments.

e. 3. What is its estimated intrinsic value of equity?

Mini Case: 7 – 21

e. 4. What is its estimated intrinsic stock price per share?

f. 1. You have just learned that B&M has undertaken a major expansion that will

change its expected free cash flows to −$10 million in 1 year, $20 million in 2

years, and $35 million in 3 years. After 3 years, free cash flow will grow at a rate

of 5%. No new debt or preferred stock were added, the investment was financed

by equity from the owners. Assume the WACC is unchanged at 11% and that

there are still 10 million shares of stock outstanding. What is its horizon value (i.e.,

its value of operations at year three)? What is its current value of operations (i.e.,

at time zero)?

Answer:

Year

0

1

2

3

4

5

… t

Mini Case: 7 – 22

f. 2. What is its value of equity on a price per share basis?

Answer:

Value of operations

$480.67

$580.67

$330.67

Mini Case: 7 – 23

g. If B&M undertakes the expansion, what percent of B&M’s value of operations at

Year 0 is due to cash flows from Years 4 and beyond? Hint: use the horizon value

at t = 3 to help answer this question.

Answer: First, calculate the present value of the horizon value. Then divide the present value

of the horizon value by the Year 0 value of operations. This will show what percent

of value is due to cash flows occurring 4 or more years in the future.

h. Based on your answer to the previous question, what are two reasons why

managers often emphasize short-term earnings?

Answer: 1. Changes in quarterly earnings can signal changes future in cash flows. This would

affect the current stock price.

Mini Case: 7 – 24

i. Your employer also is considering the acquisition of Hatfield Medical Supplies.

You have gathered the following data regarding Hatfield, with all dollars reported

in millions: (1) most recent sales of $2,000; (2) most recent total net operating

capital, OpCap = $1,120; (3) most recent operating profitability ratio, OP =

NOPAT/Sales = 4.5%; and (4) most recent capital requirement ratio, CR =

OpCap/Sales = 56%. You estimate that the growth rate in sales from Year 0 to

Year 1 will be 10%, from Year 1 to Year 2 will be 8%, from Year 2 to Year 3 will

be 5%, and from Year 3 to Year 4 will be 5%. You also estimate that the long–

term growth rate beyond Year 4 will be 5%. Assume the operating profitability

and capital requirement ratios will not change. Use this information to forecast

Hatfield’s sales, net operating profit after taxes (NOPAT), OpCap, free cash flow,

and return on invested capital (ROIC) for Years 1 through 4. Also estimate the

annual growth in free cash flow for Years 2 through 4. The weighted average cost

of capital (WACC) is 9%. How does the ROIC in Year 4 compare with the

WACC?

Answer:

The operating items are forecast as follows: Sales1 = $2,000(1+0.10) = $2,200;

NOPAT1 = $2,200(0.045) = $99; and OpCap1 = $2,200(0.56) = $1,232. The operating

items for the other years are forecast in a similar manner.

Mini Case: 7 – 25

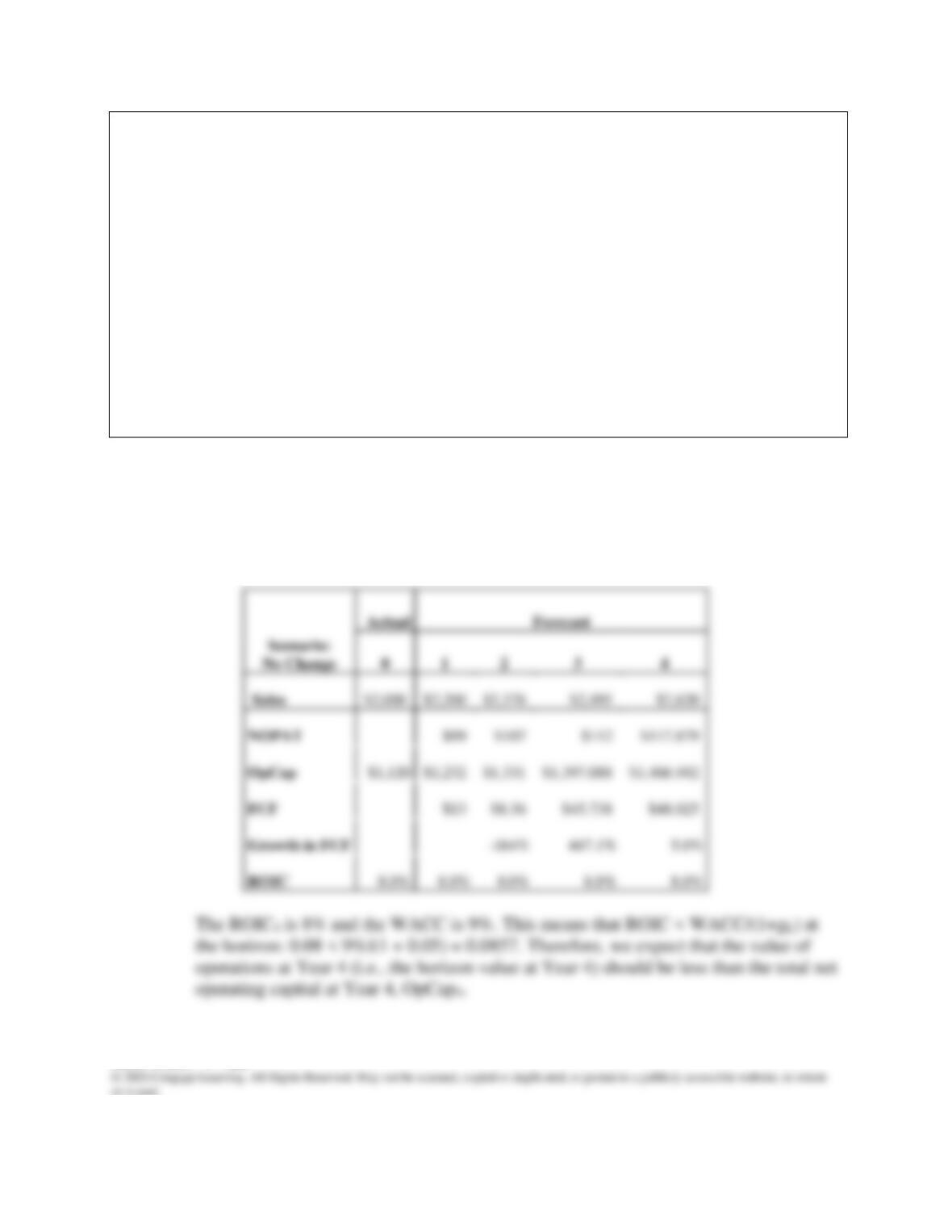

j. What is the horizon value at Year 4? What is the total net operating capital at

Year 4? Which is larger, and what can explain the difference? What is the value

of operations at Year 0? How does the Year-0 value of operations compare with

the Year-0 total net operating capital?

Answer:

HV4= FCF4(1 + gL)

(WACC − gL)=$48.025(1 + 0.05)

(0.09 − 0.05)= $1,260.65

The value of operations is the sum of the PV of the horizon value plus the PVs of the

FCFs:

Value of Operations:

Present value of HV

$893.08

+ Present value of FCF

$64.45

Mini Case: 7 – 26

k. What are value drivers? What happens to the ROIC and current value of

operations if expected growth increases by 1 percentage point relative to the

original growth rates (including the long-term growth rate)? What can explain

this? Hint: Use Scenario Manager.

Answer: Value drivers are the inputs to the FCF valuation model that managers are able to

influence: sales growth rates, operating profitability, capital requirements, and cost of

capital.

Scenario

No Change

Improve Growth

g0,1

10%

11%

g1,2

g2,3

g3,4

l. Assume growth rates are at their original levels. What happens to the ROIC and

current value of operations if the operating profitability ratio increases to 5.5%?

Now assume growth rates and operating profitability ratios are at their original

levels. What happens to the ROIC and current value of operations if the capital

requirement ratio decreases to 51%? Assume growth rates are at their original

levels. What is the impact of simultaneous improvements in operating profitability

and capital requirements? What is the impact of simultaneous improvements in

the growth rates, operating profitability, and capital requirements? Hint: Use

Scenario Manager.

Mini Case: 7 – 27

Answer: .

Scenario

No Change

Improve OP

g0,1

10%

10%

g1,2

8%

8%

g2,3

5%

5%

g3,4

5%

5%

5%

5%

Scenario

No Change

Improve CR

g0,1

10%

10%

g1,2

8%

8%

g2,3

5%

5%

g3,4

5%

5%

5%

5%

Mini Case: 7 – 28

g0,1

10%

10%

g1,2

8%

8%

g2,3

5%

5%

g3,4

5%

5%

gL

5%

5%

OP

4.5%

5.5%

8.0%

The improvements in operating profitability and capital requirements increased the ROIC, so

growth now adds substantial value.

Scenario

No Change

Improve All

g0,1

10%

11%

g1,2

8%

9%

g2,3

5%

6%

g3,4

5%

6%

gL

5%

6%

OP

4.5%

5.5%

8.0%

Mini Case: 7 – 29

m. What insight does the free cash flow valuation model give provide us about

possible reasons for market volatility? Hint: Look at the value of operations for

the combinations of ROIC and gL in the previous questions.

Answer: .

ROIC

n. 1. Write out a formula that can be used to value any dividend-paying stock,

regardless of its dividend pattern

Answer: The value of any stock is the present value of its expected dividend stream:

Mini Case: 7 – 30

n. 2. What is a constant growth stock? How are constant growth stocks valued?

Answer: A constant growth stock is one whose dividends are expected to grow at a constant rate

forever. “Constant growth” means that the best estimate of the future growth rate is

some constant number, not that we really expect growth to be the same each and every

n. 3. What happens if a company has a constant gL that exceeds its rs? Will many stocks

have expected growth greater than the required rate of return in the short run

(i.e., for the next few years)? In the long run (i.e., forever)?

Answer: The model is derived mathematically, and the derivation requires that rs > gL. If gL is

greater than rs, the model gives a negative stock price, which is nonsensical. The model

Mini Case: 7 – 31

o. Assume that Temp Force has a beta coefficient of 1.2, that the risk-free rate (the

yield on T-bonds) is 7%, and that the market risk premium is 5%. What is the

required rate of return on the firm’s stock?

Answer: Here we use the SML to calculate temp force’s required rate of return:

p. Assume that Temp Force is a constant growth company whose last dividend (D0,

which was paid yesterday) was $2.00 and whose dividend is expected to grow

indefinitely at a 6% rate.

p. 1. What is the firm’s current stock price?

Answer: We could extend the time line on out forever, find the value of Temp Force’s dividends

for every year on out into the future, and then the PV of each dividend, discounted at r

Mini Case: 7 – 32

p. 2. What is the stock’s expected value one year from now?

Answer: After one year, D1 will have been paid, so the expected dividend stream will then be

D2, D3, D4, and so on. Thus, the expected value one year from now is $32.10:

Mini Case: 7 – 33

p. 3. What are the expected dividend yield, the capital gains yield, and the total return

during the first year?

Answer: The expected dividend yield in any year n is

Dividend Yield =

1n

n

P

ˆ

D

−

06.013.0

12.2$

−

q. Now assume that the stock is currently selling at $30.29. What is its expected rate

of return?

Answer: The constant growth model can be rearranged to this form:

Mini Case: 7 – 34

r. Now assume that Temp Force’s dividend is expected to experience nonconstant

growth of 30% from Year 0 to Year 1, 20% from Year 1 to Year 2, and 10% from

Year 2 to Year 3. After Year 3, dividends will grow at a constant rate of 6%. What

is the stock’s intrinsic value under these conditions? What are the expected

dividend yield and capital gains yield during the first year? What are the expected

dividend yield and capital gains yield during the fourth year (from Year 3 to Year

4)?

Answer: Temp Force is no longer a constant growth stock, so the constant growth model is not

applicable. Note, however, that the stock is expected to become a constant growth

stock in 3 years. Thus, it has a nonconstant growth period followed by constant growth.

The easiest way to value such nonconstant growth stocks is to set the situation up on a

time line as shown below:

Mini Case: 7 – 35

s. What is the market multiple method of valuation? What are its strengths and

weaknesses?

Answer: Analysts often use the P/E multiple (the price per share divided by the earnings per

share) or the P/CF multiple (price per share divided by cash flow per share, which is

the earnings per share plus the dividends per share) to value stocks. For example,

Mini Case: 7 – 36

t. What are the advantages of the free cash flow valuation model relative to the

dividend growth model?

Answer: You can apply FCF model in more situations, such as privately held companies,

u. What is preferred stock? Suppose a share of preferred stock pays a dividend of

$2.10 and investors require a return of 7%. What is the estimated value of the

preferred stock?