CFIN6 – CHAPTER 7

INTEGRATIVE PROBLEM SOLUTION

a. Preferred stock generally pays a constant dividend, whereas common stock often pays variable

dividends. Neither preferred stock nor common stock has a maturity. Whether preferred or common,

b. Classified stock is stock that is given some special designation. Those designations typically are Class

A, Class B, and so on, but any designation can be used. “Founders’ shares” is the name given to

classified stock that is owned by the firm’s founders. Founders‘ shares generally have sole voting

c(1). The value of any stock is the present value of its expected dividend stream:

c(2). A constant growth stock is one whose dividends are expected to grow at a constant rate forever.

“Constant growth” means that the best estimate of the future growth rate is some constant number, not

that we really expect growth to be the same each and every year. Many companies have dividends

that are expected to grow steadily into the foreseeable future, and such companies are valued as

constant growth stocks.

This is the well-known “Gordon,” or “constant–growth” model for valuing stocks. Here

1

ˆ

D

, is the next

expected dividend, which is assumed to be paid one year from now, rs is the required rate of return on

the stock, and g is the constant growth rate.

c(3). The model is derived mathematically, and the derivation requires that rs > g. If g is greater than rs, the

e(1). Because Bon Temps is a constant growth stock, its dividend is expected to grow at a constant rate of

6% per year. Expressed as a cash flow timeline, we have the following setup. Just enter $2 in your

calculator; then keep multiplying by 1 + g = 1.06 to get

1 2 3

ˆ ˆ ˆ

D , D , and D

2

ˆ

D

3

ˆ

D

:

0 1 2 3

1

D

ˆ

e(2). We could extend the cash flow timeline on out forever, find the value of Bon Temps’ dividends for

every year on out into the future, and then the PV of each dividend, discounted at rs = 16%. For

r

e(3). After one year,

1

D

ˆ

will have been paid, so the expected dividend stream will then be

2

ˆ

D

,

3

ˆ

D

,

4

ˆ

D

, and

so forth. Thus, the expected value one year from now is $22.47:

16%

e(4). The expected dividend yield in any year n is

n

n1

ˆ

D

Dividend

Yield ˆ

P−

=

f. The constant growth model can be rearranged to this form:

1

s0

ˆ

D

ˆ

r = + g

P

g. If Bon Temps’ dividends were not expected to grow at all, then its dividend stream would be a

perpetuity. Perpetuities are valued as shown below:

s

PMT $2

PVP $12.50

r 0.16

= = =

Note that preferred stock is generally a perpetuity, so it can be valued with this formula.

h. Bon Temps no longer is a constant growth stock, so the constant growth model is not applicable. Note,

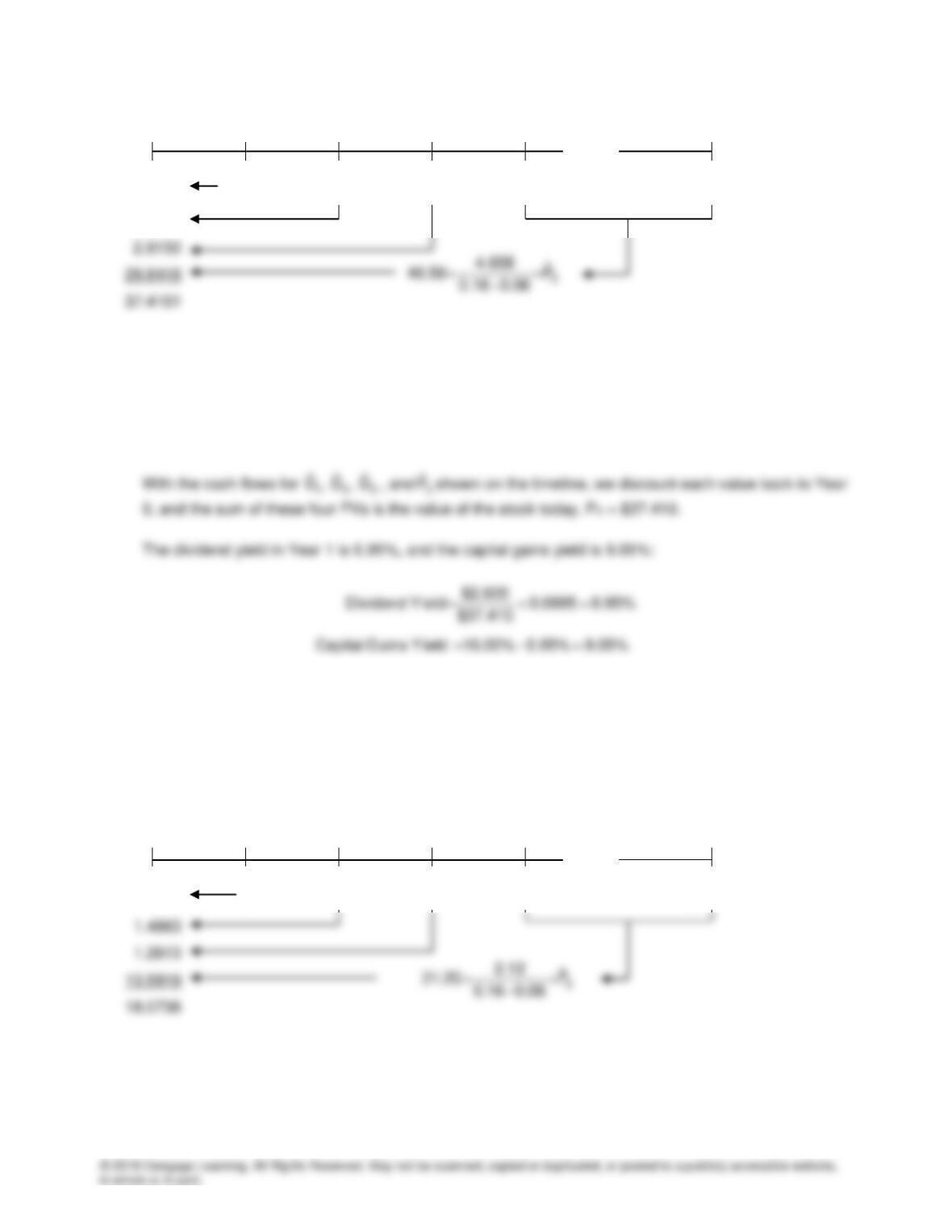

0 1 2 3 4 ∞

2.2414 2.600 3.380 4.394 4.658

3

ˆ

D

=2(1.06)∞-3

2.5119

Simply enter $2 and multiply by (1.30) to get

1

ˆ

D

= $2.60; multiply that result by 1.3 to get

2

ˆ

D

= $3.38,

and so forth. Then, recognize that after year 3, Bon Temps becomes a constant growth stock, and at

that point

3

ˆ

P

can be found using the constant growth model.

3

ˆ

P

3

ˆ

P

is the present value as of t = 3 of the

dividends in Year 4 and beyond.

During the nonconstant growth period, the dividend yields and capital gains yields are not constant,

and the capital gains yield does not equal g. However, after Year 3, the stock becomes a constant

growth stock, with g = capital gains yield = 6.0% and dividend yield = 16.0% – 6.0% = 10.0%.

i. Now we have this situation:

0 1 2 3 4 ∞

1.7241 2 2 2 2.12

3

ˆ

D

=2(1.06)∞-3

16%

…

16%

…

g2 = 0%

g3 = 0%

g1 = 0%

gn = 6%

g1=30%

g2=30%

g3=30%

gn=6%

During Year 1:

$2.00

Dividend Yield 0.1107 = 11.07%

$18.07

Capital Gains Yield 16.00% 11.07% = 4.93%

==

=−

Again, in Year 4 Bon Temps becomes a constant growth stock; hence g = capital gains yield = 6.0%

and dividend yield = 10.0%.

$1.88

Dividend Yield = = 0.220 = 22.0%

$8.55

The dividend and capital gains yields are constant over time, but a high (22.0%) dividend yield is needed to

offset the negative capital gains yield.

k(1). EVA = EBIT(1 – T) – (Cost of funds x Invested capital)

k(2). Bon Temps is producing a positive EVA, so it seems to be a good investment. However, if the firm

pays a dividend in excess of the EVA dividend, an investor should examine the company in much