1

2

3

4

5

6

7

8

14

15

16

17

24

25

26

27

28

If constant growth begins at Time 0:

29

30

31

32

33

34

35

36

37

38

39

40

57

58

59

60

61

62

63

64

65

66

78

A B C D E F G H I J K L

11/20/2018

Situation

Features of Common Stock

Data for charts

Column1

10

Mkt. Sec.

1

Claims on Value

Pref. Stk.

1

Debt

3

If constant growth begins at Time 1:

Chapter 7 Mini Case

Your employer, a mid-sized human resources management company, is considering expansion into related fields, including the

acquisition of Temp Force Company, an employment agency that supplies word processor operators and computer programmers

a. Describe briefly the legal rights and privileges of common stockholders.

d. Suppose the free cash flow at Time 1 is expected to grow at a constant rate of gL forever. If gL < WACC, what is a formula for

the present value of expected free cash flows when discounted at the WACC? If the most recent free cash flow is expected to

grow at a constant rate of gL forever (and gL < WACC), what is a formula for the present value of expected free cash flows when

discounted at the WACC?

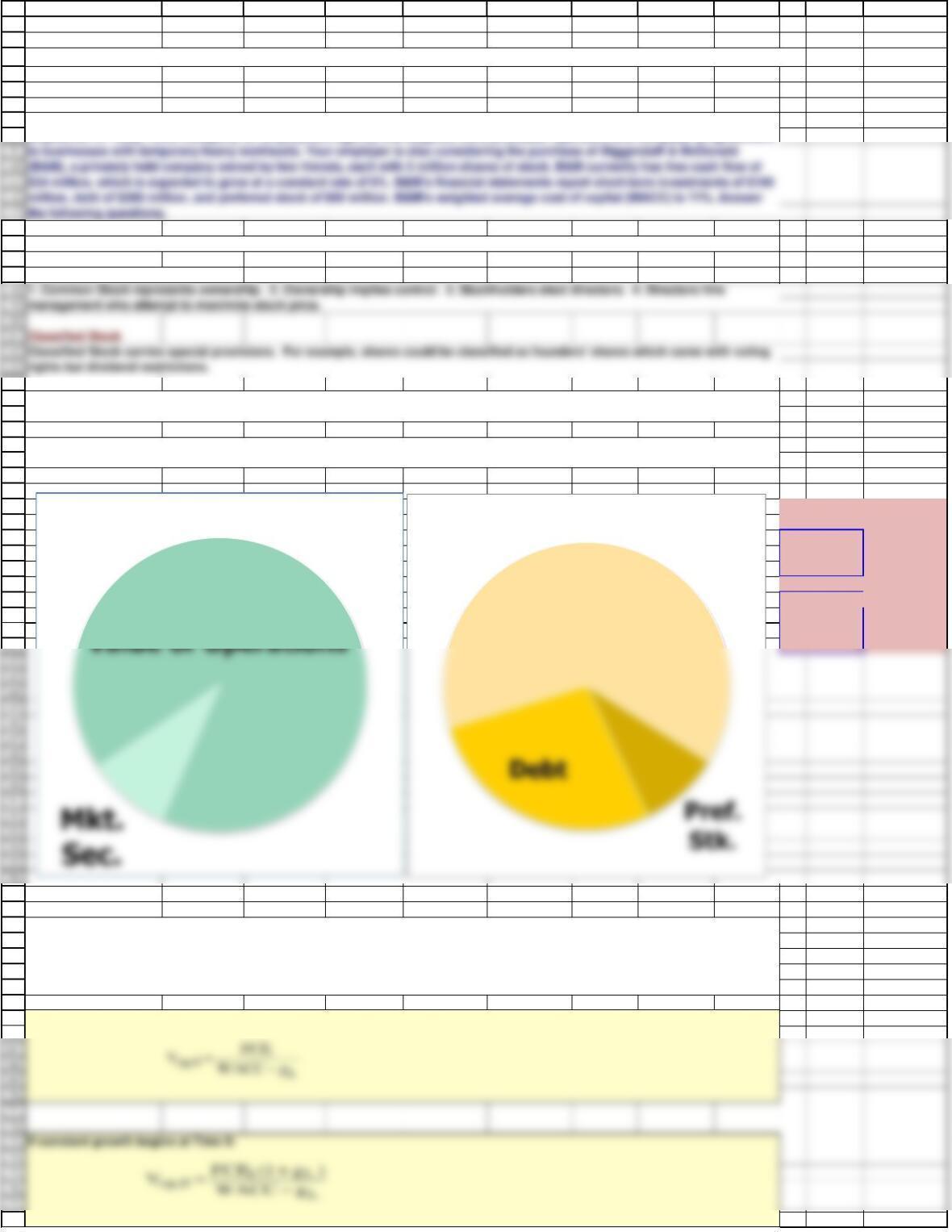

c. Use a pie chart to illustrate the sources that comprise a hypothetical company’s total value. Using another pie chart, show the

claims on a company’s value. How is equity a residual claim? Answer: See Chapter 7 Mini Case Show

b. What is free cash flow (FCF)? What is the weighted average cost of capital? What is the free cash flow valuation model?

Answer: See Chapter 7 Mini Case Show

Equity

Classified Stock

79

80

81

82

83

84

85

86

92

93

94

95

96

97

98

101

102

103

104

105

106

107

116

117

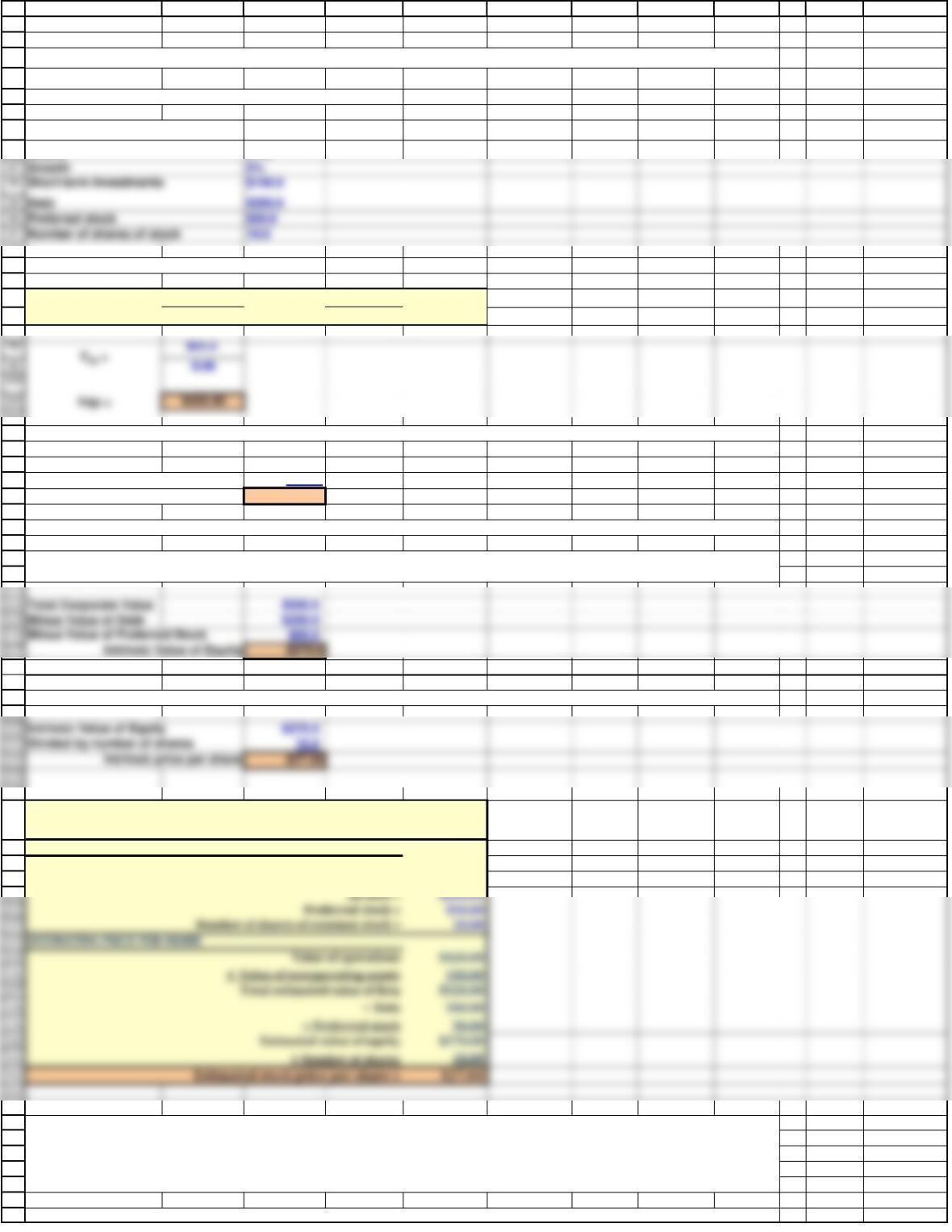

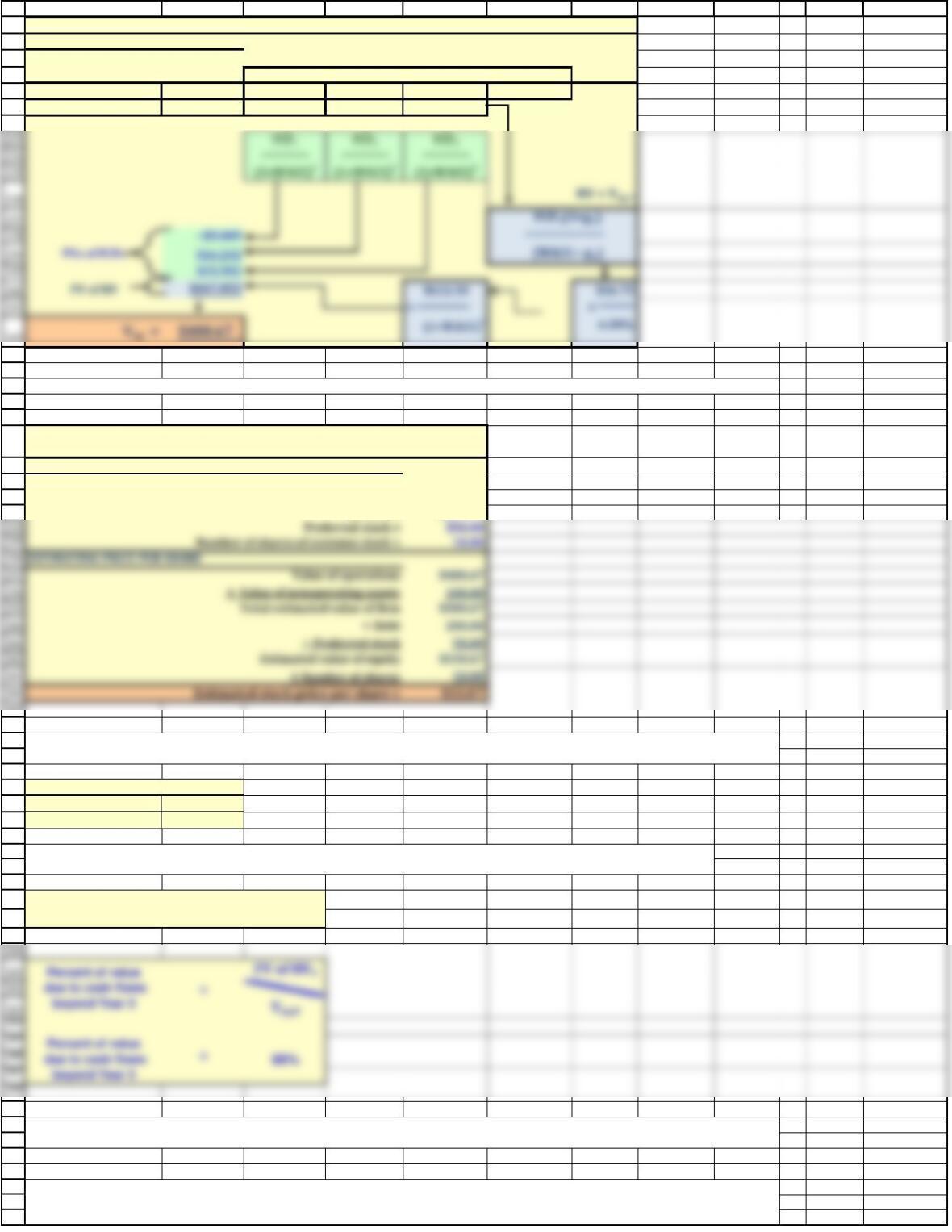

Total Corporate Value $520.0

Minus Value of Debt $200.0

Minus Value of Preferred Stock $50.0

108

109

110

111

112

123

124

Intrinsic Value of Equity $270.0

Divided by number of shares 10.0

118

119

120

126

127

128

133

134

129

130

144

145

146

147

148

149

150

151

A B C D E F G H I J K L

INPUT DATA SECTION: Data used for valuation (in millions)

$24.0

11%

(1) What is its estimated value of operations?

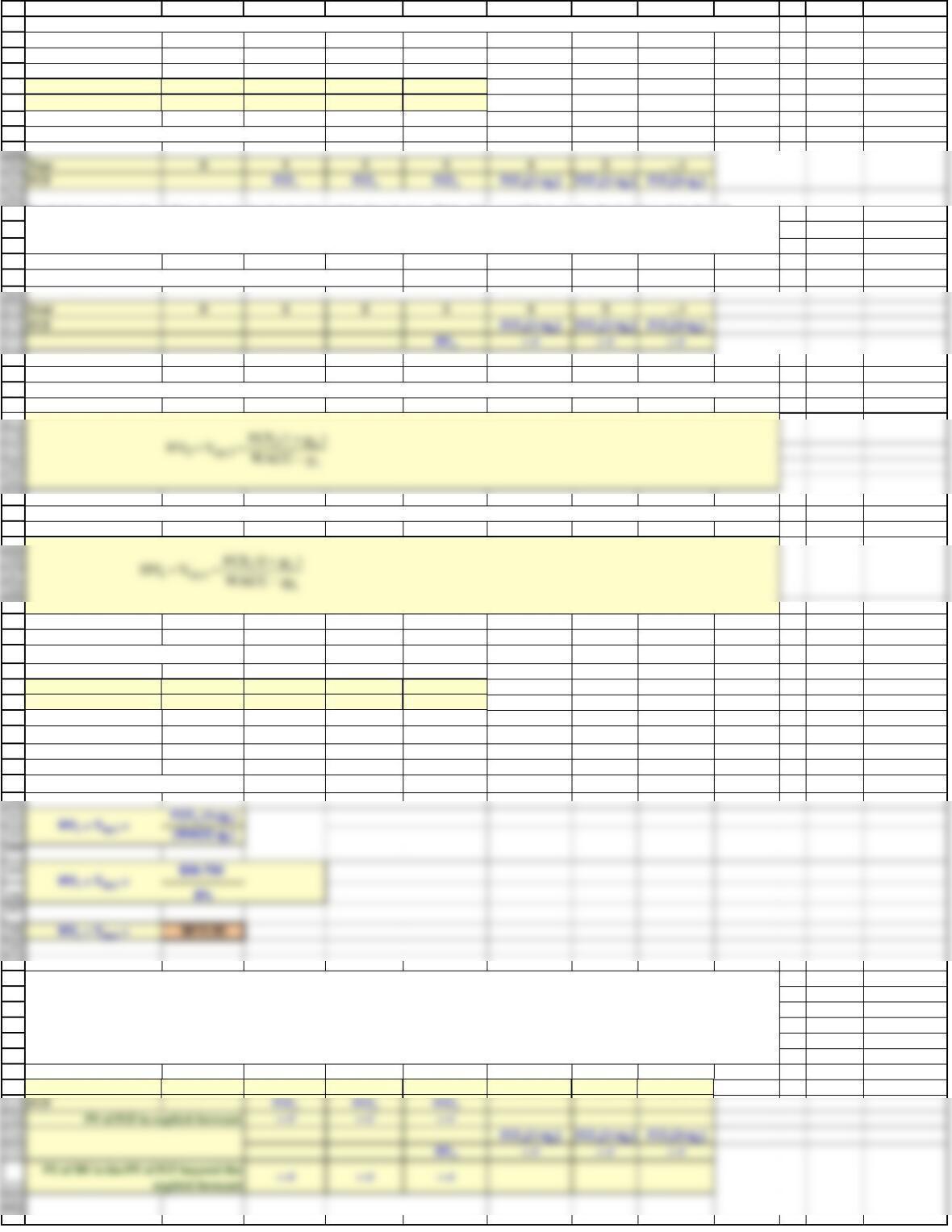

FCF1 FCF0 (1+gL)

(WACC-gL) (WACC-gL)

Value of Operation $420.0

Plus Value of Non-operating Assets $100.0

Total Corporate Value $520.0

INPUTS:

Value of operations = $420.00

Value of nonoperating assets = $100.00

(4) What is its estimated intrinsic stock price per share?

=

Vop =

(2) What is its estimated total corporate value?

(3) What is its estimated intrinsic value of equity?

Estimating the Value of R&R’s Stock Price (Millions, Except for Per Share

Data)

f. You have just learned that B&M has undertaken a major expansion that will change its expected free cash flows to −$10 million

in 1 year, $20 million in 2 years, and $35 million in 3 years. After 3 years, free cash flow will grow at a rate of 5%. No new debt or

preferred stock were added, the investment was financed by equity from the owners. Assume the WACC is unchanged at 11% and

it that there are still has 10 million shares of stock outstanding.

(1.) What is its horizon value (i.e., its value of operations at year three)? What is its current value of operations (i.e., at time

zero)?

Debt holders have the first claim on corporate value. Preferred stockholders have the next claim and the remaining is left to

common stockholders.

e. Use B&M’s data and the free cash flow valuation model to answer the following questions.

Free cash flow

WACC

88

Number of shares of stock 10.0

Debt

Preferred stock

Growth

0 1 2 3 4 5 … t

152

153

154

155

156

157

158

159

164

165

166

167

168

173

174

175

176

182

183

184

189

190

191

192

193

194

195

196

197

198

199

200

FCF1FCF2FCF3

210

211

212

213

214

215

216

217

218

225

A B C D E F G H I J K L

Explicit forecast:

Year

0 1 2 3

FCF

FCF1FCF2FCF3

Constant growth from Year 3 and afterwards:

HV3 = Vop,3 = PV of FCF4 and beyond discounted back to Year 3

R&R’s explicit forecast:

Year

0 1 2 3

FCF

−$10.00 $20.00 $35.00

After Year 3, gL = 5%

WACC = 11%

R&R’s horizon value:

Year

0 1 2 3 4 5 … t

Explicit forecast ends at Year 3, so make the horizon date Year 3, too. (Note: it is possible to make the horizon date Year 2

because FCF3 is known and grows at a constant rate, but it is easy to make mistakes if horizon year is not set equal to end of

explicit forecast.)

After estimating the horizon value, you can estimate the current value of operations by following these steps: (1) Find the present

value of the FCFs from the explicit forecast, discounted back to Time 0 at the WACC; (2) find the present value of the horizon

value, discounted back to Time 0 at the WACC; and (3) sum the PV of the FCFs and the PV of the horizon value. This sum is the

present value of all future FCF from Time 0 to infinity, discounted back to Time 0. Therefore, this sum is the current value of

operations, Vop,0.

Because free cash flows are constant from Year 4 and beyond, we can apply the constant growth model at Year 3:

The general horizon value formula is:

(1.) What is its horizon value (i.e., its value of operations at year three)? What is its current value of operations (i.e., at time

zero)?

0 1 2 3 4 5 … t

FCF1FCF2FCF3FCF3(1+gL) FCF4(1+gL) FCFt(1+gL)

226

227

228

229

230

231

232

244

245

246

247

248

249

250

255

256

251

252

253

265

266

267

268

269

270

271

272

273

274

275

276

277

278

279

289

290

291

292

293

294

295

296

A B C D E F G H I J K L

B&M’s Value of Operations (Millions of Dollars)

INPUTS:

gL = 5.00%

WACC = 11.00%

Year 0 1 2 3 4

FCF −$10.00 $20.00 $35.00

↓ ↓ ↓

INPUTS:

Value of operations = $480.67

Value of nonoperating assets = $100.00

All debt = $200.00

INPUTS:

Vop,0 = $480.67

HV3 = $612.50

PV of HV3 = HV3 / (1+WACC)3

PV of HV3 = $447.85

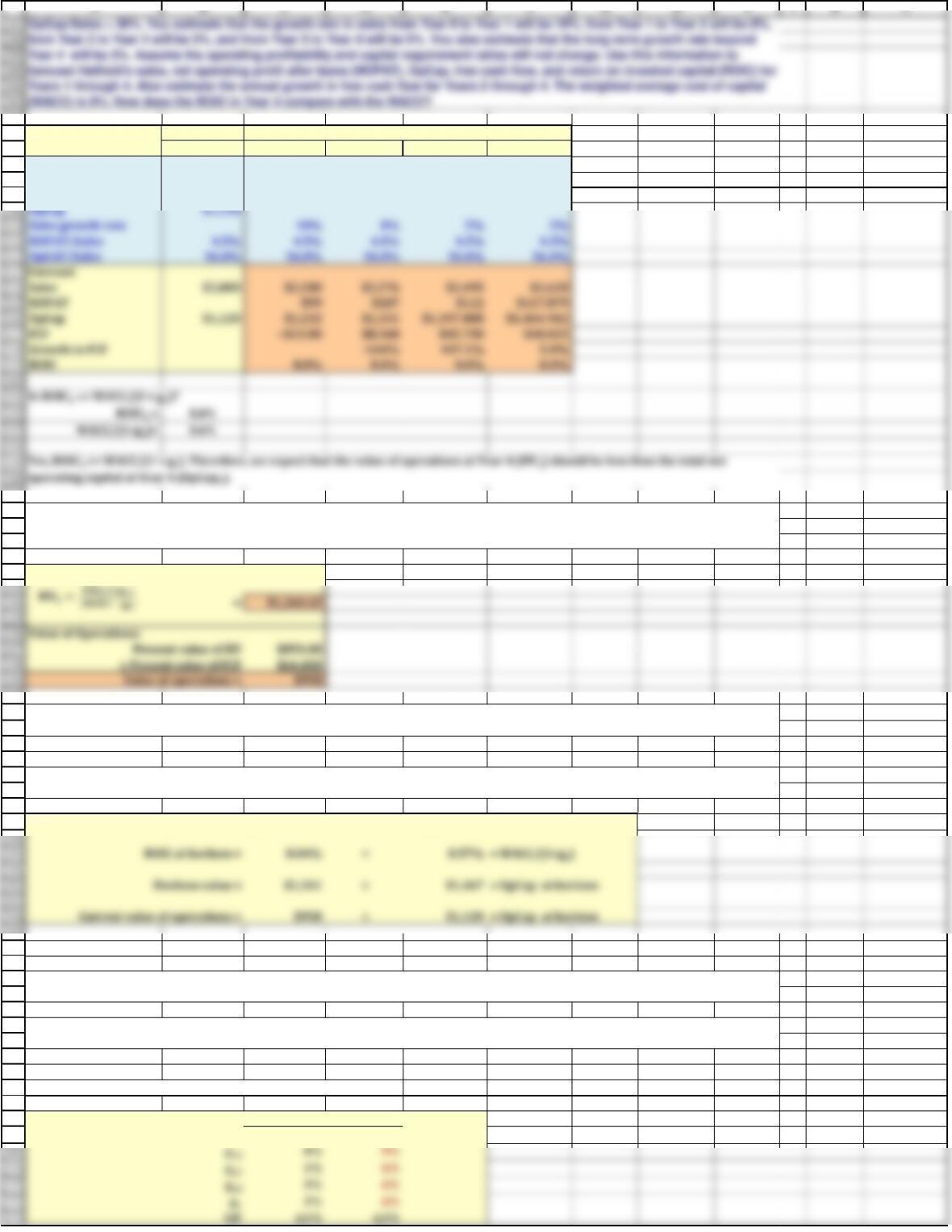

i. Your employer also is considering the acquistion of Hatfield Medical Supplies. You have gathered the following data regarding

Hatfield, with all dollars reported in millions: (1) most recent sales of $2,000; (2) most recent total net operating capital, OpCap =

$1,120; (3) most recent operating profitability ratio, OP = NOPAT/Sales = 4.5%; and (4) most recent capital requirement ratio, CR =

OpCap/Sales = 56%. You estimate that the growth rate in sales from Year 0 to Year 1 will be 10%, from Year 1 to Year 2 will be 8%,

from Year 2 to Year 3 will be 5%, and from Year 3 to Year 4 will be 5%. You also estimate that the long-term growth rate beyond

Year 4 will be 5%. Assume the operating profitability and capital requirement ratios will not change. Use this information to

forecast Hatfield’s sales, net operating profit after taxes (NOPAT), OpCap, free cash flow, and return on invested capital (ROIC) for

Years 1 through 4. Also estimate the annual growth in free cash flow for Years 2 through 4. The weighted average cost of capital

(WACC) is 9%. How does the ROIC in Year 4 compare with the WACC?

h. Based on your answer to the previous question, what are two reasons why managers often emphasize short-term earnings?

Answer: See Chapter 7 Mini Case Show

First, calculate the present value of the horizon value. Then divide the Year 0 value of operations by the present value of the

horizon value. This will show what percent of value is due to cash flows occurring 4 or more years in the future.

g. If B&M undertakes the expansion, what percent of B&M’s value of operations at Year 0 is due to cash flows from Years 4 and

beyond? Hint: use the horizon value at t = 3 to help answer this question.

Estimating the Value of B&M’s Stock Price (Millions, Except for Per Share

Data)

(2.) What is its value of equity on a price per share basis?

Projections

240

Value of Operations:

g1,2 8% 9%

g2,3 5% 6%

g3,4 5% 6%

303

304

305

306

307

308

327

328

329

330

331

332

340

341

342

343

344

345

346

347

348

355

356

357

358

359

360

361

362

363

364

365

366

367

368

No Change Actual Forecast

Year 0 1 2 3 4

Inputs

WACC 9.0%

Sales $2,000

Horizon Value:

ROIC needed to make HV greater than Vop at horizon: ROIC = WACC/(1+gL)

Using the Scenario Manager, the new ROIC and value of operations are:

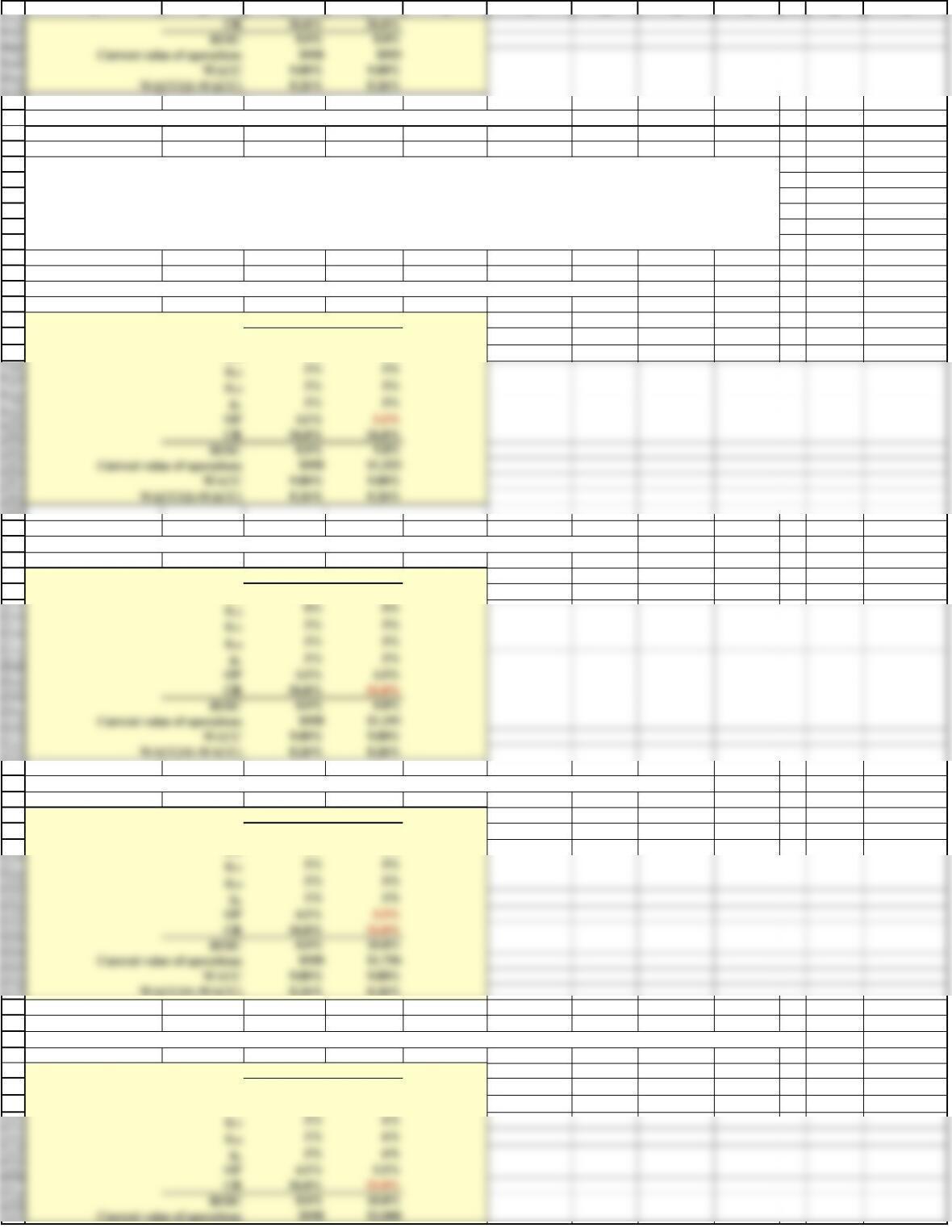

Scenario No Change Improve Growth

g0,1 10% 11%

i. Your employer also is considering the acquistion of Hatfield Medical Supplies. You have gathered the following data regarding

Hatfield, with all dollars reported in millions: (1) most recent sales of $2,000; (2) most recent total net operating capital, OpCap =

k. What are value drivers? What happens to the ROIC and current value of operations if expected growth increases by 1

percentage point relative to the original growth rates (including the long-term growth rate)? What can explain this? Hint: Use

j. What is the horizon value at Year 4? What is the value of operations at Year 0? How does the value of operations compare with

the current total net operating capital?

Note that the horizon value at Year 4 (HV4 = $958) is less than the total net operating capital at Year 4 (OpCap4 = $1,466.94). This is

expected because ROIC4 < WACC/(1+gL).

Value drivers are the inputs to the free cash flow valuation model that managers are able to influence: sales growth rates, operating profitability,

capital requirements, and the cost of capital.

The value of operations at Year 0 is less than the total net operating capital at Year 0 because the ROIC is too low when compared

to the WACC. ROIC must be greater than WACC/(1+gL) before the horizon value exceeds the total net operating capital.

Years 1 through 4. Also estimate the annual growth in free cash flow for Years 2 through 4. The weighted average cost of capital

(WACC) is 9%. How does the ROIC in Year 4 compare with the WACC?

g2,3 5% 5%

g1,2 8% 8%

g2,3 5% 5%

g3,4 5% 5%

g2,3 5% 5%

g3,4 5% 5%

g2,3 5% 6%

g3,4 5% 6%

379

380

381

382

383

384

385

386

387

388

389

390

391

392

393

394

395

405

406

407

408

409

410

421

422

423

424

425

426

436

437

438

439

440

441

442

A B C D E F G H I J K L

Growth hurts value because the ROIC is too low. Growth will only help value if ROIC>WACC/(1+WACC).

Using the Scenario Manager and improving operating profitability, the new ROIC and value of operations are:

Scenario No Change Improve OP

g0,1 10% 10%

g1,2 8% 8%

Using the Scenario Manager and improving capital requirements, the new ROIC and value of operations are:

Scenario No Change Improve CR

g0,1 10% 10%

Using the Scenario Manager and improving operating profitability and capital requirements, the new ROIC and value of operations are:

Scenario No Change Improve OP and CR

g0,1 10% 10%

g1,2 8% 8%

Using the Scenario Manager and improving growth rates, operating profitability, and capital requirements, the new ROIC and value of operations are:

Scenario No Change Improve All

g0,1 10% 11%

g1,2 8% 9%

l. Assume growth rates are at their original levels. What happens to the ROIC and current value of operations if the operating

profitability ratio increases to 5.5%? Now assume growth rates and operating profitability ratios are at their original levels. What

happens to the ROIC and current value of operations if the capital requirement ratio decreases to 51%? Assume growth rates are

at their original levels. What is the impact of simultaneous improvements in operating profitability and capital requirements?

What is the impact of simultaneous improvements in the growth rates, operating profitability, and capital requirements? Hint: Use

Scenario Manager.

450

451

452

453

454

455

456

457

458

462

463

464

465

466

467

468

469

470

471

472

473

474

475

484

485

486

487

488

489

490

491

492

growth, we are trying to find the average of the good times and the bad times, and we assume that we will see both scenarios

over the firm’s life. In addition to assuming a constant growth rate, we will be estimating a long-term required return for the

stock. By assuming these variables are constant, our price equation for common stock simplifies to the following expression:

503

504

505

A B C D E F G H I J K L

WACC

9.00% 9.00%

WACC/(1+WACC)

8.26% 8.26%

Notice that small changes in ROIC and growth cause large changes in value.

ROIC

m. What insight does the free cash flow valuation model give provide us about possible reasons for market volatility? Hint: Look

at the value of operations for the combinations of ROIC and gL in the previous questions.

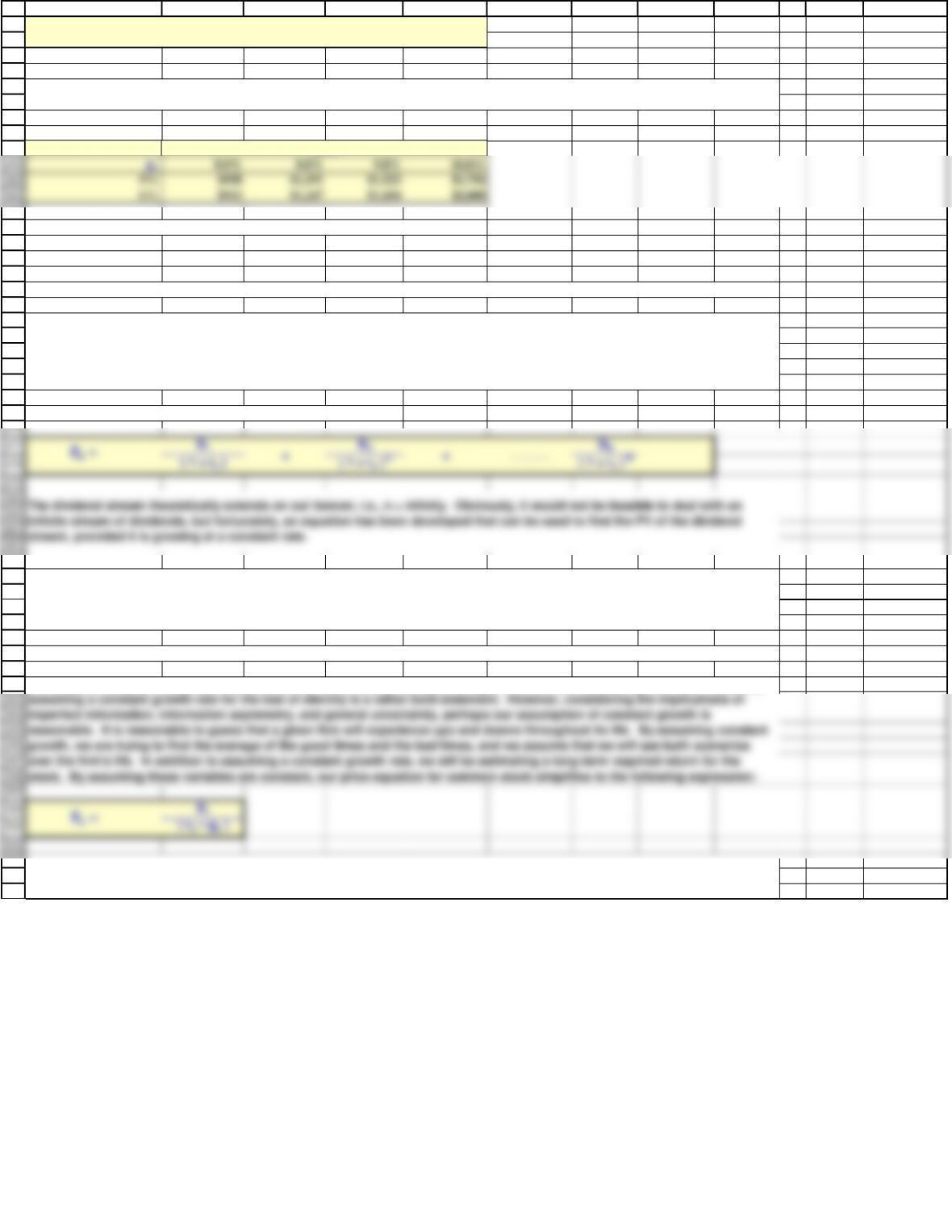

Naturally, trying to estimate an infinite series of dividends and interest rates forever would be a tremendously difficult task. Now,

we are charged with the purpose of finding a valuation model that is easier to predict and construct. That simplification comes in

the form of valuing stocks on the premise that they have a constant growth rate.

n. (2.) What is a constant growth stock? How are constant growth stocks valued?

n. (1.) Write out a formula that can be used to value any dividend-paying stock, regardless of its dividend pattern.

The value of any financial asset is equal to the present value of future cash flows provided by the asset. When an investor buys a

share of stock, he or she typically expects to receive cash in the form of dividends and then, eventually, to sell the stock and to

receive cash from the sale. Moreover, the price any investor receives is dependent upon the dividends the next investor expects

to earn, and so on for different generations of investors. Thus, the stock’s value ultimately depends on the cash dividends the

company is expected to provide and the discount rate used to find the present value of those dividends.

In this stock valuation model, we first assume that the dividend and stock will grow forever at a constant growth rate. Naturally,

In this equation, the long-run growth rate (g) can be approximated by multiplying the firm’s return on assets by the retention ratio.

Generally speaking, the long-run growth rate of a firm is likely to fall between 5% and 8% a year.

Here is the basic dividend valuation equation:

506

507

508

509

523

524

525

539

526

527

528

529

541

542

543

544

545

546

547

548

549

550

551

559

560

565

566

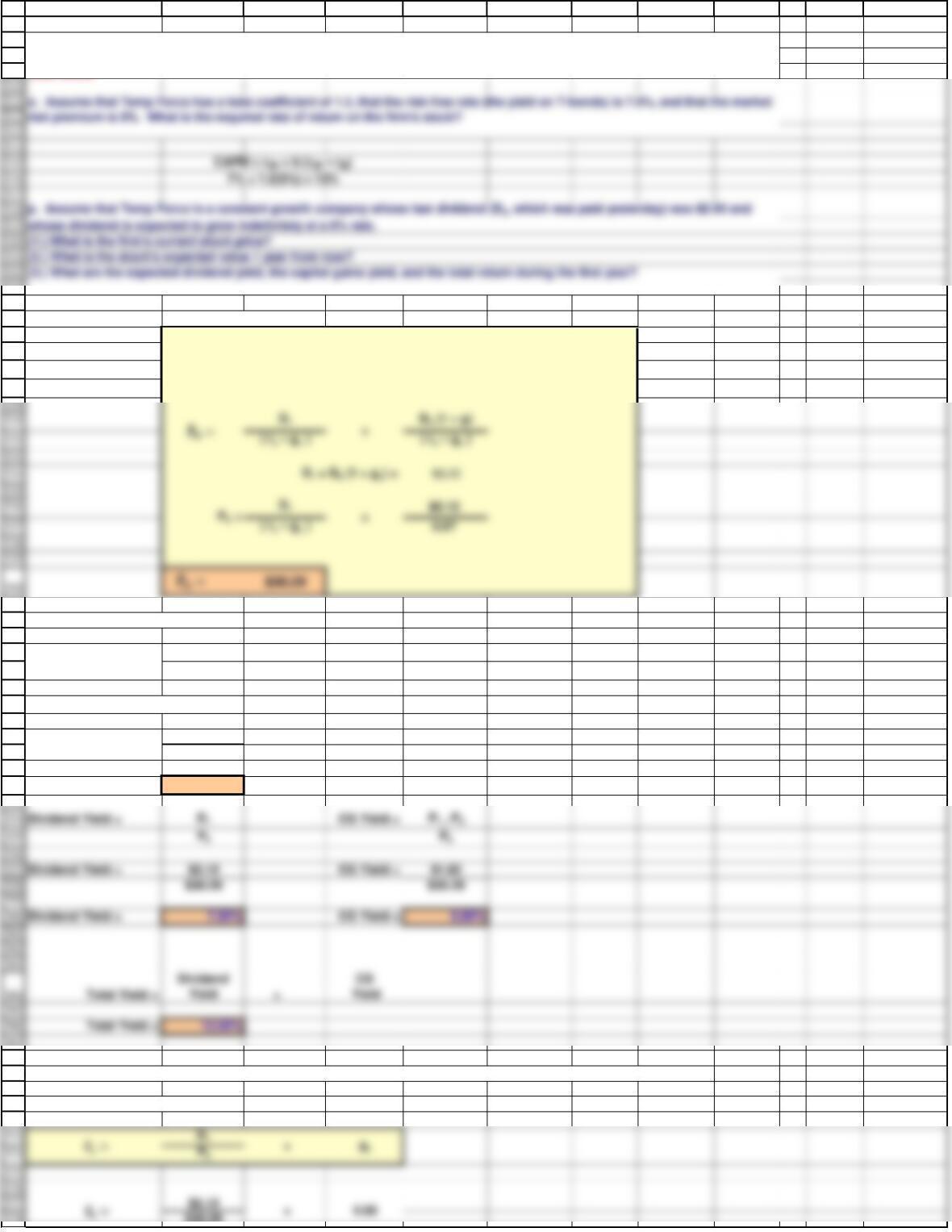

D1CG Yield = P1 – P0

Dividend Yield = $2.12 CG Yield = $1.82

552

567

568

569

570

571

572

D1

578

A B C D E F G H I J K L

Constant Growth Model:

INPUTS:

D0 = $2.00

gL = 6%

rs =13.0%

Stock Price 1 year from now:

D2

( rs – gL )

D2 = D1 (1+gL) = $2.2472

$2.2472

0.07

P1 = $32.10

Rearrange to rate of return formula

$30.29

n. (3.) What happens if a company has a constant gL which exceeds rs? Will many stocks have expected growth greater than the

required rate of return in the short run (i.e., for the next few years)? In the long run (i.e., forever)? Answer: See Chapter 7 Mini

Case Show.

q. Now assume that the stock is currently selling at $30.29. What is its expected rate of return?

P1 =

P1 =

511

512

522

whose dividend is expected to grow indefinitely at a 6% rate.

579

580

581

582

583

584

585

586

587

588

589

590

601

602

603

604

605

606

628

629

630

631

632

633

634

635

639

640

641

642

643

644

651

Expected Dividend and CG Yields at t = 3

Dividend Yield = 0.0%

CG Yield = 13.0%

Total Return = 13.0%

636

A B C D E F G H I J K L

13%

Process for Finding the Value of a Nonconstant Growth Stock

INPUTS:

D0 = $2.00 Last dividend the company paid.

rs = 13.0% Stockholders’ required return.

Expected Dividend and CG Yields at t = 0

Dividend Yield = 5.6%

CG Yield = 7.4%

Total Return = 13.0%

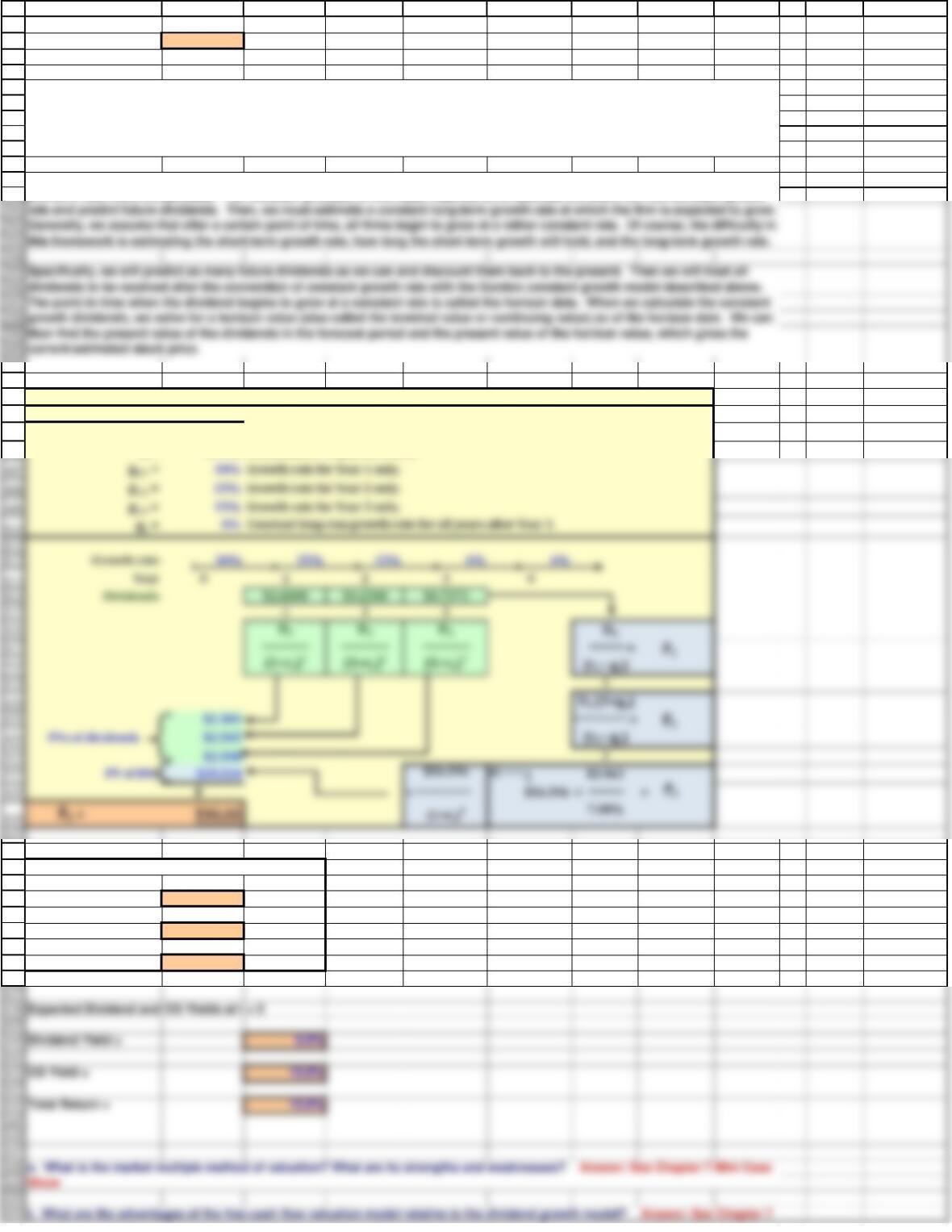

For many companies, it is unreasonable to assume that it grows at a constant growth rate. Hence, valuation for these companies

proves a little more complicated. The valuation process, in this case, requires us to estimate the short-run non-constant growth

r. Now assume that Temp Force’s dividend is expected to experience nonconstant growth of 30% from Year 0 to Year 1, 25% from

Year 1 to Year 2, and 15% from Year 2 to Year 3. After Year 3, dividends will grow at a constant rate of 6%. What is the stock’s

intrinsic value under these conditions? What are the expected dividend yield and capital gains yield during the first year? What

are the expected dividend yield and capital gains yield during the fourth year (from Year 3 to Year 4)?

Mini Case Show

ො

𝐫𝐬=

595

dividends to be received after the convention of constant growth rate with the Gordon constant growth model described above.

The point in time when the dividend begins to grow at a constant rate is called the horizon date. When we calculate the constant

652

653

654

655

656

A B C D E F G H I J K L

u. What is preferred stock? Suppose a share of preferred stock pays a dividend of $2.10 and investors require a return of 7%.

What is the estimated value of the preferred stock?

t. What are the advantages of the free cash flow valuation model relative to the dividend growth model? Answer: See Chapter 7

Mini Case Show