Chapter 07 – Capital Structure

CHAPTER 7

Capital Structure

1. If Googles’ executives believe that Google stock is overvalued, then considerations of

market timing would lead them to sell new stock, even if they have no immediate need for

the cash. In line with the remark made by Amgen’s first CEO, George Rathmann, Google

3.14159265), a number representing the ratio of the circumference of a circle to its diameter.

This is intended as an inside joke by Google executives for quantitatively oriented investors.

2. Broadly speaking, the experience is typical. The average market response to the

announcement of an open market repurchase is 3.5 percent. In the case of Cypress, the

market response was 2.5 percent (=0.25/(10.125-0.25)). As was mentioned in the chapter,

2

©2018 McGraw-Hill Education. All rights reserved. Authorized only for instructor use in the classroom. No

reproduction or further distribution permitted without the prior written consent of McGraw–Hill Education.

12.1 percent. This was roughly the case with Cypress, in that its stock outperformed the S&P

500 by 16 percent for the four years after the repurchase.

3. Share repurchases make sense when the firm’s managers perceive their firms to be

undervalued in the market. And the market generally does interpret a share repurchase to

mean that the firm’s managers perceive the stock of their firm to be underpriced, especially if

4. Sun was a cash rich firm. Both theory and empirical evidence suggests that excessively

5. The APV of the project is the sum of the project NPV and the value of the side effects

associated with new financing. NPV is given as $48 million.

Chapter 07 – Capital Structure

3

©2018 McGraw-Hill Education. All rights reserved. Authorized only for instructor use in the classroom. No

reproduction or further distribution permitted without the prior written consent of McGraw–Hill Education.

AutoNation’s managers have concluded that the minimum that new shareholders should

demand for the $200 million is 5.3 percent of the firm. Therefore, managers estimate that

new investors overpay by $11.4 million (= (0.053 – 0.050) x $3.8 billion). This overpayment

represents the side effect of equity financing, and is captured by the firm’s original

shareholders. Therefore the APV of equity financing is $48 million + $11.4 million = $59.4

million

The financing side effect associated with mispricing of debt is zero, in that the debt is

intrinsically priced. The traditional formula for the value of the tax shields is the product of

the corporate tax rate and the size of the debt. This product is $70 million = 0.35 x $200

million. Therefore, the APV associated with financing with debt is $118 million.

Because financing with debt features a higher APV than financing with equity, the

firm’s managers will create more value for the firm’s original shareholders by financing with

debt than with equity, even though the equity is overvalued.

6. Managers believe that new shareholders underpay by $949 million = (0.285 – 0.212) x $13

billion). Therefore the financing side effect associated with equity funding is -$949 million.

7. The leveraged buyout left J. Crew with high leverage, and its executives with substantial

ownership of the firm’s equity. Leverage amplifies equity returns, and therefore its CEO

Millard Drexler bore a lot of risk. The chapter explains that excessively optimistic,

Chapter 07 – Capital Structure

4

©2018 McGraw-Hill Education. All rights reserved. Authorized only for instructor use in the classroom. No

reproduction or further distribution permitted without the prior written consent of McGraw–Hill Education.

overconfident executives underestimate the expected costs of financial distress, which can

induce them to take on imprudent levels of debt for their firm, despite the agency benefits

that debt brings in respect to management discipline.

The text states: “The general finding is that excessive optimism and overconfidence

are positively related to both leverage and investment activity. This feature is accentuated by

the finding that leverage and investment debt levels increase in the years following the start-

date of CFOs who are excessively optimistic and overconfident.”

A possible indication of Millard Drexel being overconfident is his having received a

special industry award by the Council of Fashion Designers of America, which described him

as “the Merchant Prince.” In commenting on the firm’s prospects, Drexel sent out an emailed

statement to say that he continues “to have confidence” in the company’s future growth, and

that the company is making the adjustments necessary to deliver the products its customers

want.”

The text states: “Given the experimental findings, it is perhaps not surprising that the

Duke/CFO survey evidence indicates that CFOs’ estimates of internal rate of return (IRR) for

Chapter 07 – Capital Structure

5

book leverage, measured as the ratio of total debt to total capital employed, relative to a

sample mean of 22.3 percent. For long-term overprecision, the effect is approximately half

8. The text in Chapter 7 describes the evidence that firms with excessively optimistic

overconfident CEOs overinvest and take on imprudent debt. Solyndra’s high debt and

investment are consistent with these features. However, that alone would not explain

Chapter 07 – Capital Structure

6

Minicase

Case Analysis Questions

1. The Forbes story contains a description of Schrader, stating that “implacable self-

2. BPV is a subjective measure of value from the perspective of the managers (and possibly

board). Therefore, it reflects managers’ perception of value creation, balanced across the

short-term and long-term, including the effects of catering and market timing as well as

financing and investment.

Consistent with being run by an excessively optimistic and overconfident CEO,

PSINet made very large investments, including a new headquarters building, corporate jet,

selling its stock, had Wall Street been willing to buy. However, Wall Street was unwilling to

buy without a major discount for subscribing investors, suggesting a general awareness that

the stock was overpriced.

Taking on debt typically signals managers’ confidence in the future prospects of their

firms. Notably, such signaling is premised on the idea that managers make rational choices

7

©2018 McGraw-Hill Education. All rights reserved. Authorized only for instructor use in the classroom. No

reproduction or further distribution permitted without the prior written consent of McGraw–Hill Education.

about their firm’s debt levels. This case is not rational managers operating in an environment

of market inefficiency, but a case of non-rational managers operating in an environment of

market inefficiency. The combination of investors not being receptive to a new equity issue,

and the rating of PSINet’s debt as being below investment grade testifies to the market’s lack

of confidence in the firm’s future cash flow stream. Ignoring those signals is suggestive of

confirmation bias (motivated reasoning).

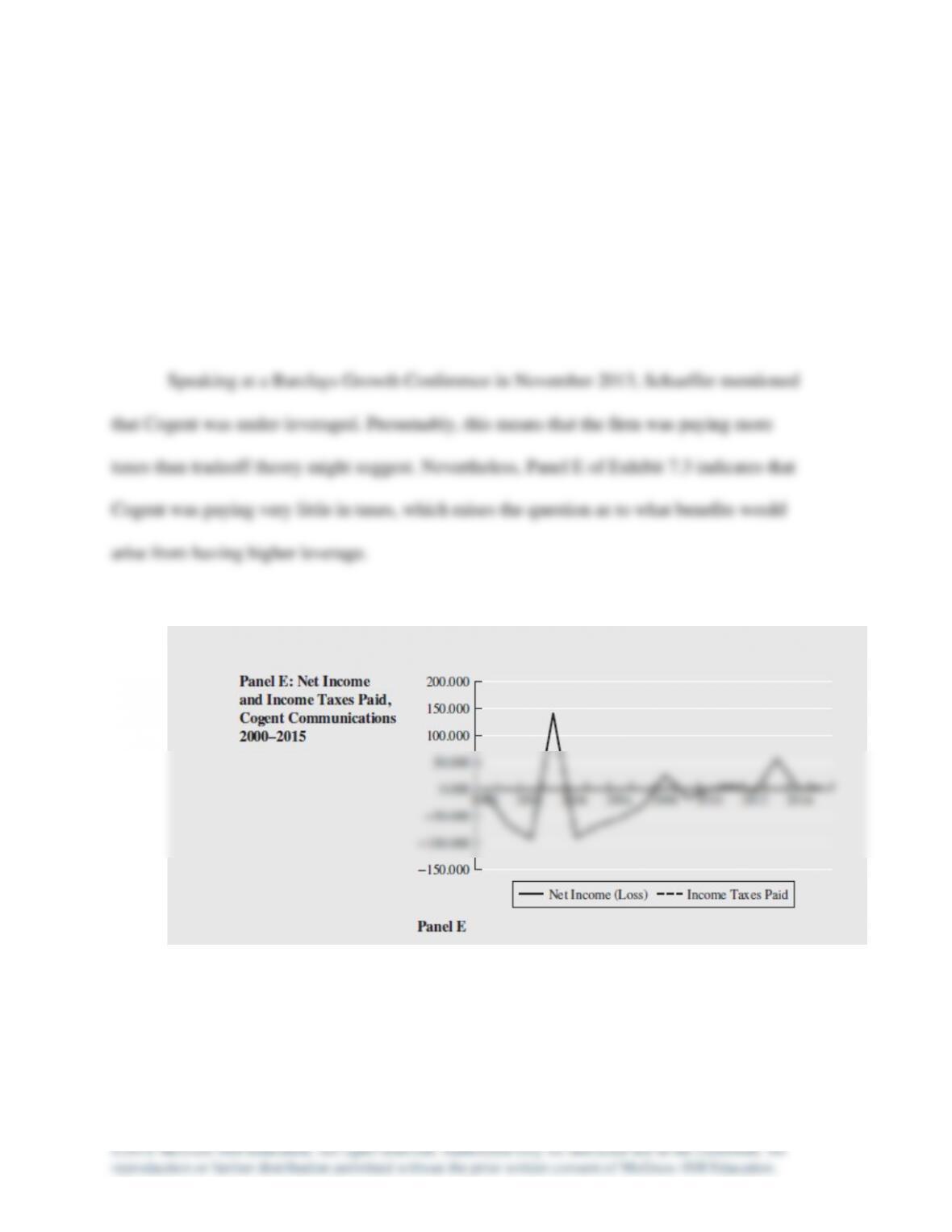

3. Schaeffer spent less to build his firm’s network than he originally estimated, did so

shrewdly, and was conservative about leverage. These outcomes are not consistent with

behavior driven by excessive optimism and overconfidence. Even if there were grounds for

4. Cogent initially raised $26 million from six venture capital firms, and obtained a $409

credit line from vendor Cisco Systems. The credit line tied the amount of credit to equipment

Chapter 07 – Capital Structure

8

collateralizing at least some of the debt, as well as extending the notion of financing

associated with accounts payable.

Cogent might have engaged in some market timing in its acquisition policy, such as

in merging with Allied Riser by trading 13 percent of Cogent for $132 million in cash, and

purchasing 100 percent of Allied Riser’s fiber network. A similar statement applies to its

acquisition of the assets of NetRail.

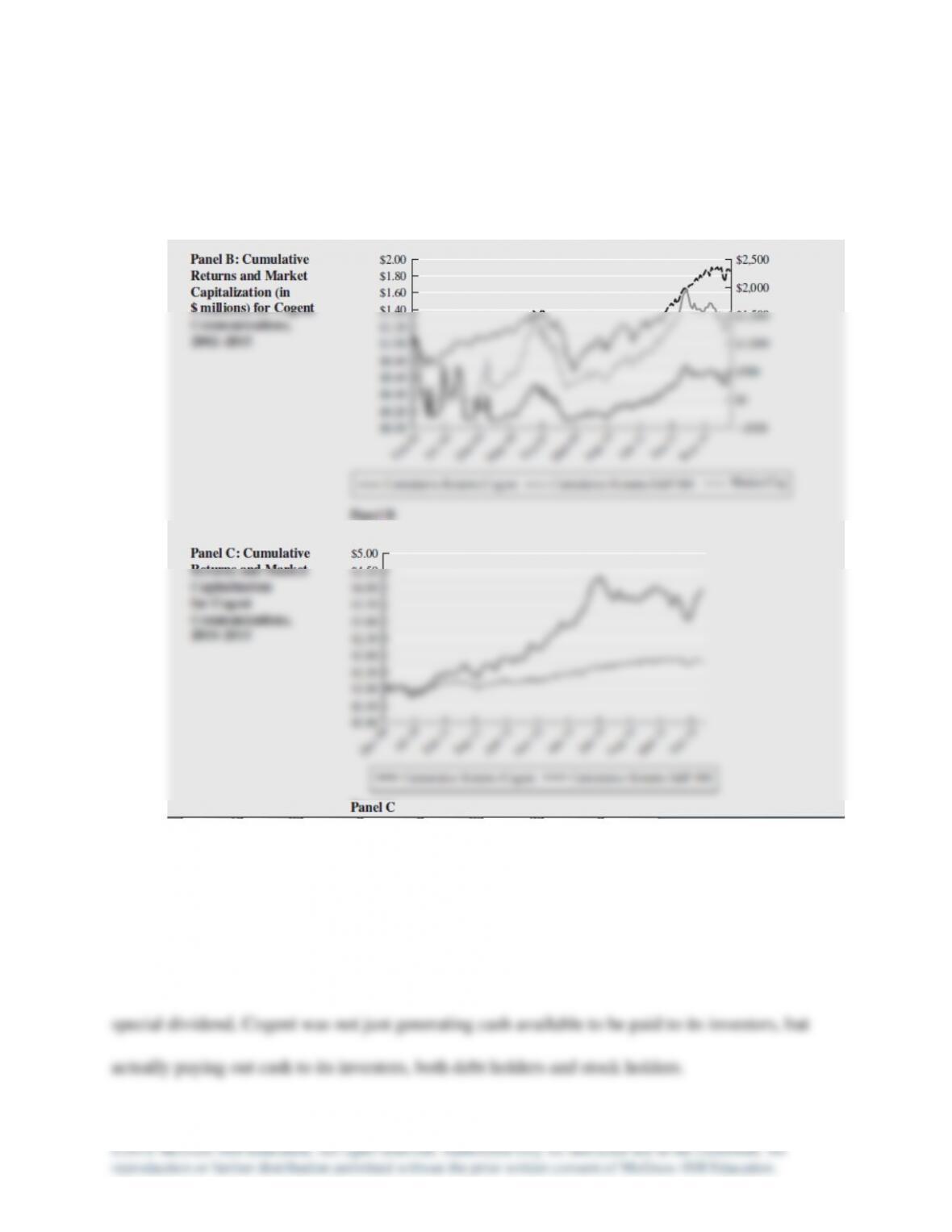

Panels B and C of Exhibit 7.3 indicate that Cogent’s stock underperformed the S&P

500 before 2010, and outperformed the S&P 500 after 2010. One possibility is market

Chapter 07 – Capital Structure

9

signaling, with Cogent signaling that its prospects remained strong, and that returns would be

amplified by having higher leverage. In other words, the under-leveraging might have

stemmed from catering behavior, and the same might be true of move to increase leverage.

CEO Schaeffer commented that Cogent had generated free cash for the previous six

years, which Panel A of Exhibit 7.3 bears out. In buying back 15 percent of its “float,” and

paying out an additional $10 million to investors every quarter either through a buyback or a

10

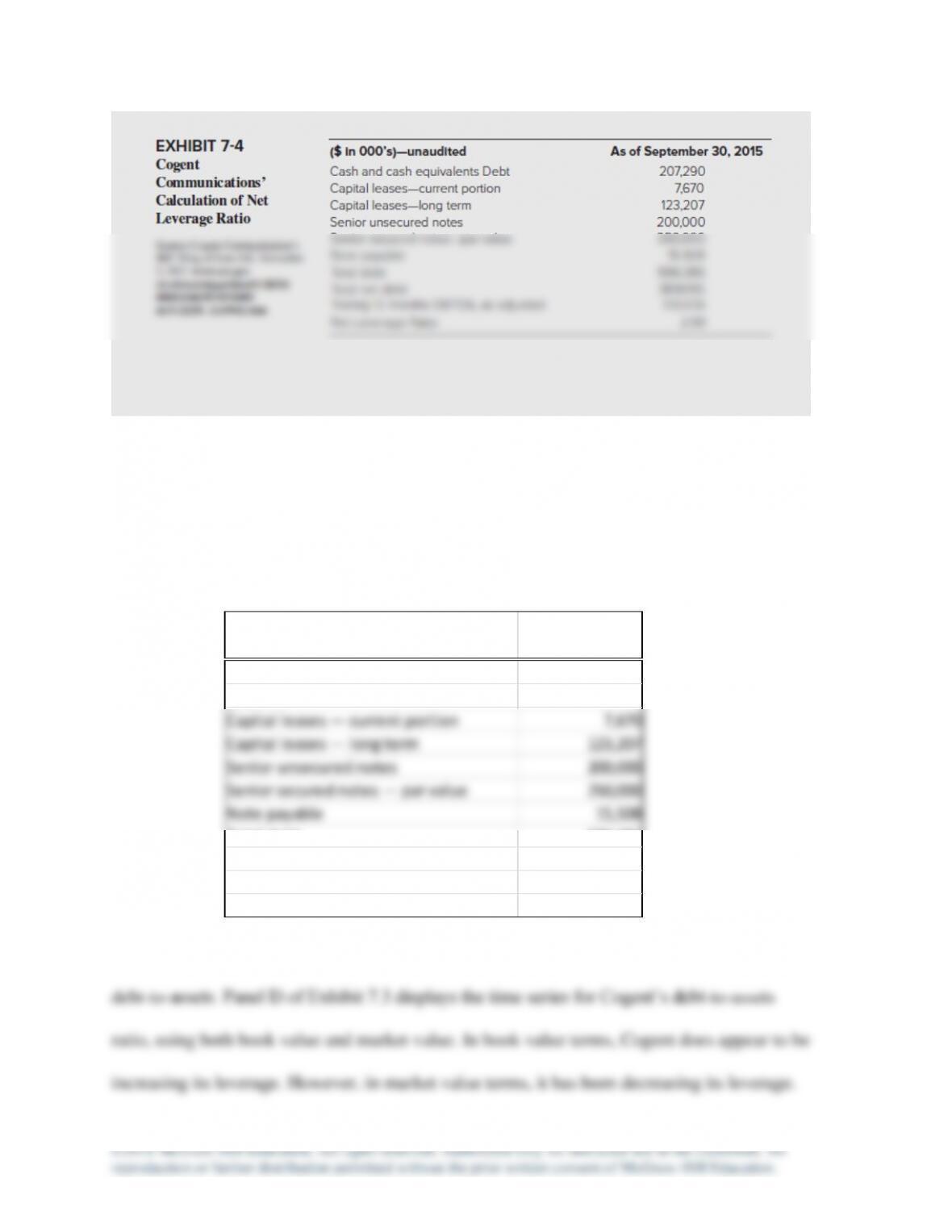

5. Schaeffer noted that he measured leverage as the ratio of net debt –to-trailing 12-month

EBITDA, where net debt is defined as debt minus cash. He then stated that the target value

for the ratio is 2.5, while the current value of the ratio is 1.6. The ratio net debt-to-EBITDA is

akin to the inverse of coverage ratio times burden covered (TBC) as TBC is the ratio of EBIT

to interest obligations and repayment of principal (scaled to reflect the non-tax deductibility

thereby raising the question as to whether Cogent is now slightly over-leveraged.

Chapter 07 – Capital Structure

11

The misplacement typo in Exhibit 7-4 masks the computational structure. The term “Debt” in

the first line belongs on its own line below. Total debt is the subtotal of the Debt items above

it. Total net debt subtracts Cash and cash equivalents from Total debt. Net leverage ratio is

the ratio of Total Net Debt to Trailing 12 months EBITDA, as adjusted.

Leverage is also measured using ratios such as assets over equity, debt-to-equity, and

($in000’s)—unaudited

As of September

30, 2015

Cash and cash equivalents 207,290

Debt

Capitalleases—currentportion 7,670

Capitalleases—longterm 123,207

Senior unsecured notes 200,000

Seniorsecurednotes—parvalue 250,000

Note payable 15,508

Total debt 596,385

Total net debt 389,095

Trailing 12 months EBITDA, as adjusted 130,439

Net Leverage Ratio 2.98