Answers and Solutions: 6 – 1

Chapter 6

Risk and Return

ANSWERS TO END-OF-CHAPTER QUESTIONS

6-1 a. Stand-alone risk is only a part of total risk and pertains to the risk an investor takes by

holding only one asset. Risk is the chance that some unfavorable event will occur. For

instance, the risk of an asset is essentially the chance that the asset’s cash flows will be

unfavorable or less than expected. A probability distribution is a listing, chart or graph

of all possible outcomes, such as expected rates of return, with a probability assigned

to each outcome. When in graph form, the tighter the probability distribution, the less

uncertain the outcome.

e. A risk averse investor dislikes risk and requires a higher rate of return as an inducement

to buy riskier securities. A realized return is the actual return an investor receives on

their investment. It can be quite different than their expected return.

Answers and Solutions: 6 – 2

i. Correlation is the tendency of two variables to move together. A correlation coefficient

(ρ) of +1.0 means that the two variables move up and down in perfect synchronization,

while a coefficient of -1.0 means the variables always move in opposite directions. A

correlation coefficient of zero suggests that the two variables are not related to one

another; that is, they are independent.

l. The security market line (SML) represents in a graphical form, the relationship between

the risk of an asset as measured by its beta and the required rates of return for individual

securities. The SML equation is essentially the CAPM, ri = rRF + bi(RPM). It can also

be written in terms of the required market return: ri = rRF + bi(rM – rRF).

Answers and Solutions: 6 – 3

n. Equilibrium is the condition under which the expected return on a security is just equal

to its required return,

r

= r, and the market price is equal to the intrinsic value. The

Efficient Markets Hypothesis (EMH) states (1) that stocks are always in equilibrium

and (2) that it is impossible for an investor to consistently “beat the market.” In essence,

the theory holds that the price of a stock will adjust almost immediately in response to

any new developments. In other words, the EMH assumes that all important

information regarding a stock is reflected in the price of that stock. Financial theorists

generally define three forms of market efficiency: weak-form, semistrong-form, and

strong-form.

o. The Fama-French 3-factor model has one factor for the excess market return (the

market return minus the risk free rate), a second factor for size (defined as the return

on a portfolio of small firms minus the return on a portfolio of big firms), and a third

factor for the book–to-market effect (defined as the return on a portfolio of firms with

a high book-to-market ratio minus the return on a portfolio of firms with a low book–

to-market ratio).

6-2 a. The probability distribution for complete certainty is a vertical line.

b. The probability distribution for total uncertainty is the X axis from – to +.

Answers and Solutions: 6 – 4

6-4 The risk premium on a high beta stock would increase more.

6-5 According to the Security Market Line (SML) equation, an increase in beta will increase a

company’s expected return by an amount equal to the market risk premium times the

change in beta. For example, assume that the risk-free rate is 6 percent, and the market

Answers and Solutions: 6 – 5

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

6-1 Investment Beta

$20,000 0.7

6-2 rRF = 4%; rM = 12%; b = 0.8; rs = ?

6-3 rRF = 5%; RPM = 7%; rM = ?

rM = 5% + (7%)1 = 12% = rs when b = 1.0.

6-5

r

= (0.1)(-50%) + (0.2)(-5%) + (0.4)(16%) + (0.2)(25%) + (0.1)(60%)

= 11.40%.

Answers and Solutions: 6 – 6

6-6 a.

r

m= (0.3)(15%) + (0.4)(9%) + (0.3)(18%) = 13.5%.

r

j= (0.3)(20%) + (0.4)(5%) + (0.3)(12%) = 11.6%.

6-7 a. rA = rRF + (rM – rRF)bA

12% = 5% + (10% – 5%)bA

12% = 5% + 5%(bA)

Answers and Solutions: 6 – 7

6-8 a. ri = rRF + (rM – rRF)bi = 5% + (12% – 5%)1.4 = 14.8%.

b. 1. rRF increases to 6%:

The slope of the SML is equal to the market risk premium, RPM, which does not

c. 1. rM increases to 14%:

If the risk-free rate does not change but they required return on the market does

change, then the market risk premium changes. For rRF = 5% and rM = 14%, the

new market risk premium is 9%: RPM = rM – rRF = 14% – 5% = 9%. The required

return on the stock is:

Answers and Solutions: 6 – 8

6-9 Old portfolio beta =

5,0007$

000,70$

(b) +

5,0007$

000,5$

(0.8)

1.2 = 0.9333b + 0.0533

1.1467 = 0.9333b

1.229 = b.

Answers and Solutions: 6 – 9

6-10 Portfolio beta =

$4,000,000

$400,000

(1.50) +

$4,000,000

$600,000

(-0.50)

+

$4,000,000

$1,000,000

(1.25) +

$4,000,000

$2,000,000

(0.75)

= 0.1)(1.5) + (0.15)(-0.50) + (0.25)(1.25) + (0.5)(0.75)

= 0.15 – 0.075 + 0.3125 + 0.375 = 0.7625.

Stock Investment Beta r = rRF + (rM – rRF)b Weight

A $ 400,000 1.50 18% 0.10

B 600,000 (0.50) 2 0.15

C 1,000,000 1.25 16 0.25

D 2,000,000 0.75 12 0.50

Total $4,000,000 1.00

rp = 18%(0.10) + 2%(0.15) + 16%(0.25) + 12%(0.50) = 12.1%.

6-11 First, calculate the beta of what remains after selling the stock:

6-12 We know that bR = 1.50, bS = 0.75, rM = 13%, rRF = 7%.

ri = rRF + (rM – rRF)bi = 7% + (13% – 7%)bi.

6-13 The answers to a, b, and c are given below:

¯rA ¯rB Portfolio

2015 (20.00%) (5.00%) (12.50%)

2016 42.00 15.00 28.50

6-14 a. bX = 1.3471; bY = 0.6508. These can be calculated with a spreadsheet.

b. rX = 6% + (5%)1.3471 = 12.7355%.

rY = 6% + (5%)0.6508 = 9.2540%.

Answers and Solutions: 6 – 11

SOLUTION TO SPREADSHEET PROBLEM

6-15 The detailed solution for the spreadsheet problem is available in the file Ch06-P15 Build

a Model Solution.xlsx on the textbook’s Web site.

Mini Case: 6 – 12

Assume that you recently graduated and landed a job as a financial planner with Cicero

Services, an investment advisory company. Your first client recently inherited some assets

and has asked you to evaluate them. The client owns a bond portfolio with $1 million invested

in zero coupon Treasury bonds that mature in 10 years. The client also has $2 million

invested in the stock of Blandy, Inc., a company that produces meat-and-potatoes frozen

dinners. Blandy’s slogan is “Solid food for shaky times.”

Unfortunately, Congress and the president are engaged in an acrimonious dispute over the budget

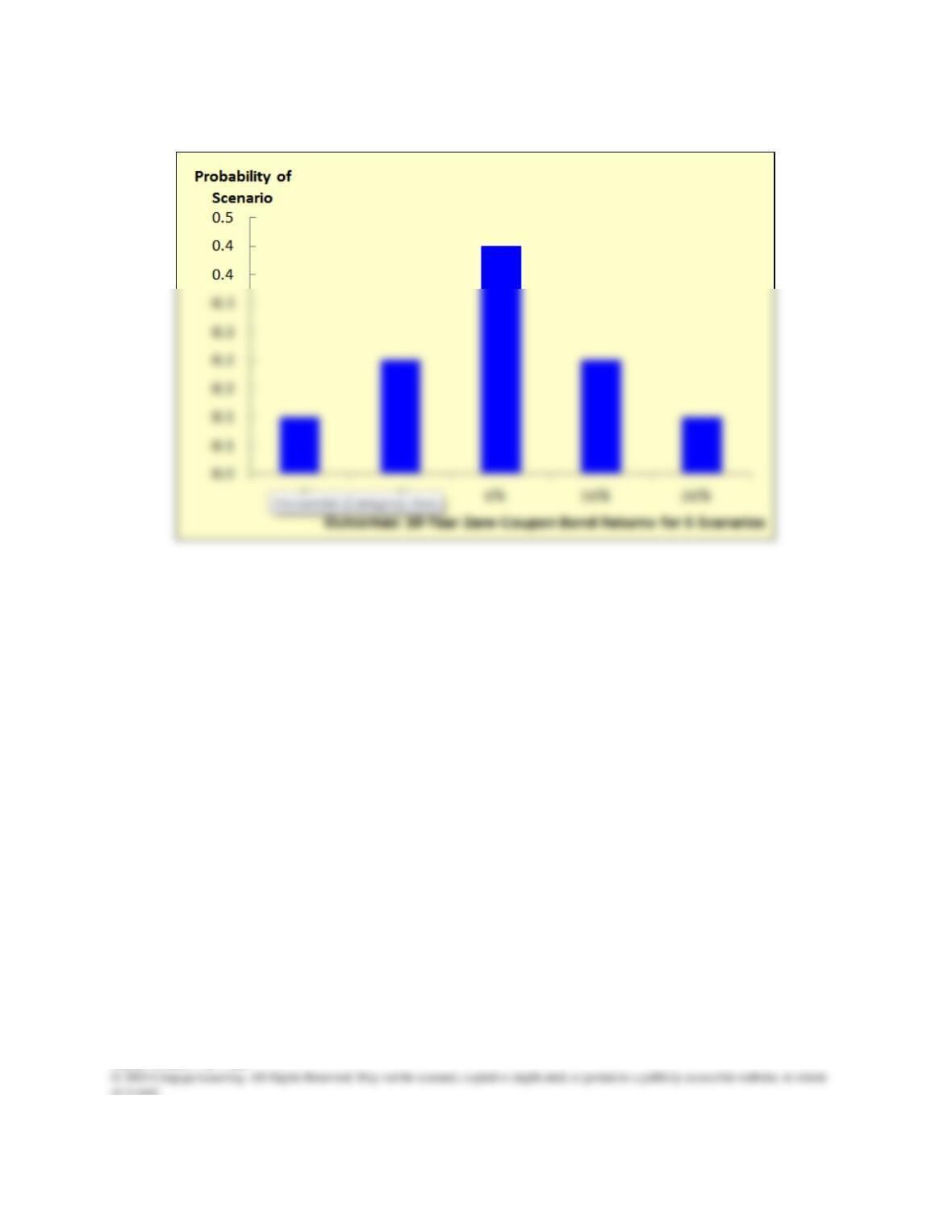

Scenario

Probability

of Scenario

Return on a 10-Year Zero

Coupon Treasury Bond

During the Next Year

Worst Case

0.10

−14%

Poor Case

0.20

−4%

Most Likely

0.40

6%

Good Case

0.20

16%

Best Case

0.10

26%

1.00

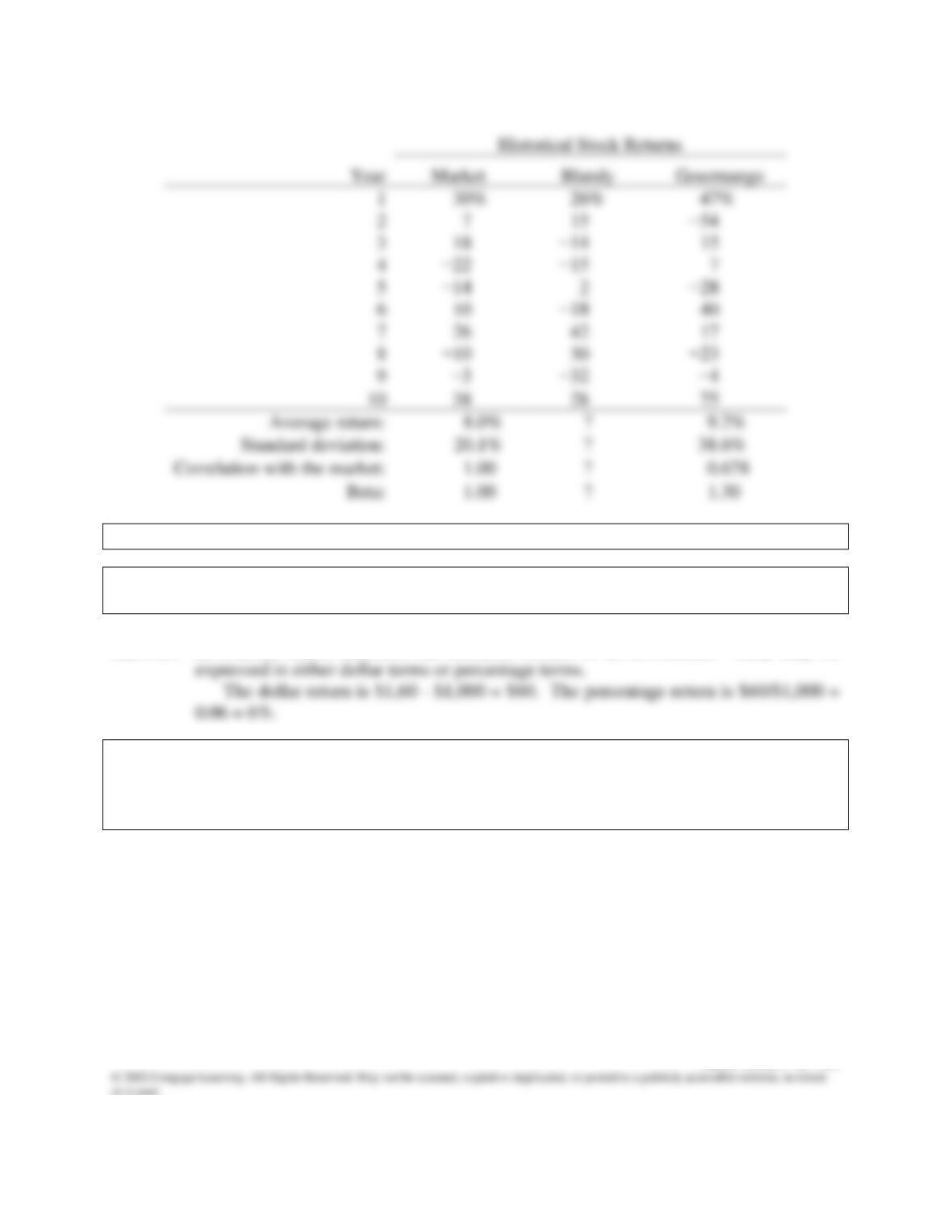

You have also gathered historical returns for the past 10 years for Blandy, Gourmange

Corporation (a producer of gourmet specialty foods), and the stock market.

MINI CASE

Mini Case: 6 – 13

The risk-free rate is 4% and the market risk premium is 5%.

a. What are investment returns? What is the return on an investment that costs

$1,000 and is sold after 1 year for $1,060?

Answer: Investment return measures the financial results of an investment. They may be

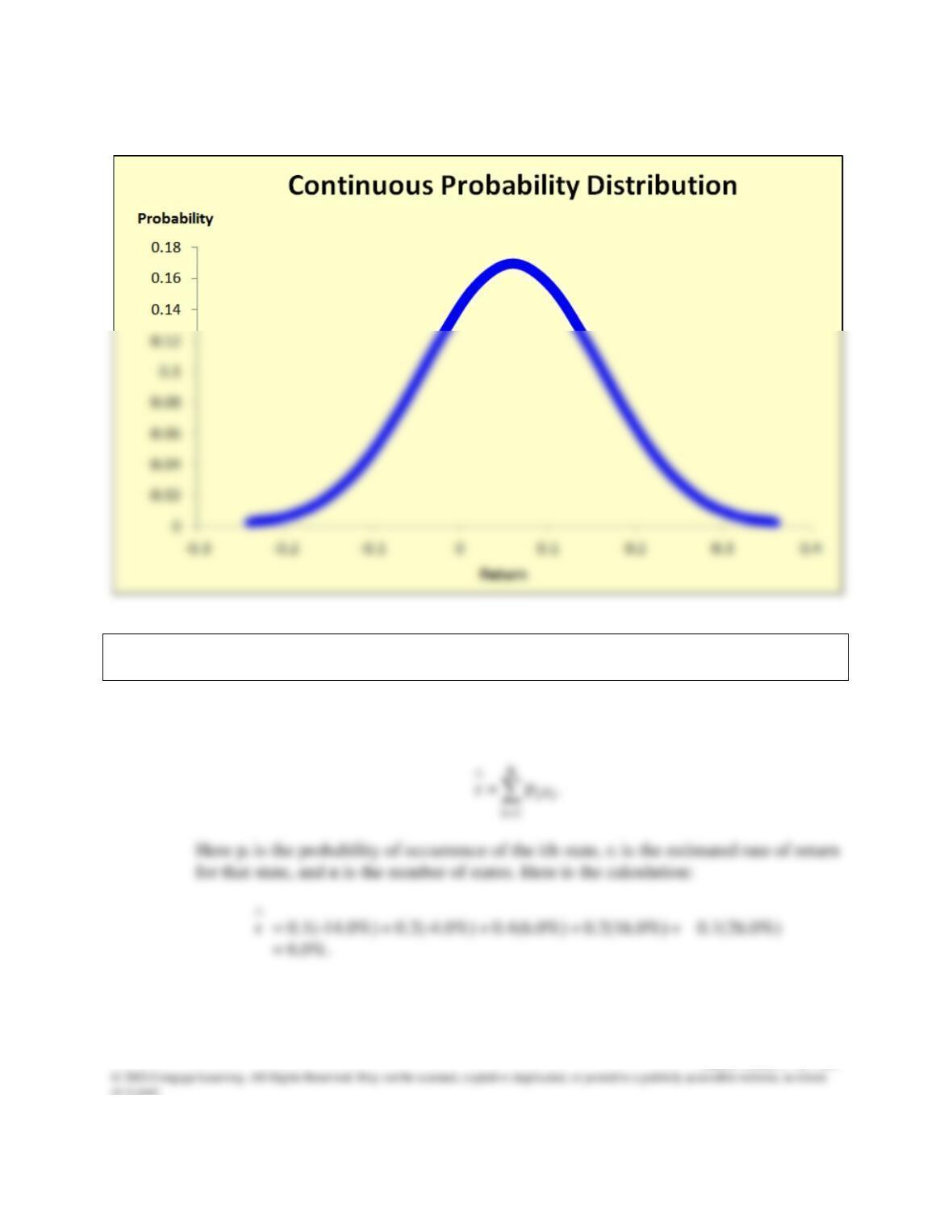

b. Graph the probability distribution for the bond returns based on the 5 scenarios.

What might the graph of the probability distribution look like if there were an

infinite number of scenarios (i.e., if it were a continuous distribution and not a

discrete distribution)?

Mini Case: 6 – 14

Answer: Here is the probability distribution for the five possible outcomes:

Mini Case: 6 – 15

A continuous distribution might look like this:

c. Use the scenario data to calculate the expected rate of return for the 10-year zero

coupon Treasury bonds during the next year.

Answer: The expected rate of return,

r

, is expressed as follows:

r

Mini Case: 6 – 16

d. What is stand-alone risk? Use the scenario data to calculate the standard deviation

of the bond’s return for the next year.

Answer: Stand-alone risk is the risk of an asset if it is held by itself and not as a part of a portfolio.

Standard deviation measures the dispersion of possible outcomes, and for a single asset,

the stand-alone risk is measured by standard deviation.

The variance and standard deviation are calculated as follows: