Year 4

Year 5

Year 6

Year 7

Revenues

$538,095.24

$538,095.24

$538,095.24

$538,095.24

Costs

319,272.80

316,232.10

313,220.37

310,237.32

Depreciation

76,393.80

72,756.00

69,291.43

65,991.84

EBT

$142,428.64

$149,107.13

$155,583.44

$161,866.08

We can also find the NPV using real cash flows and the nominal required return. This will allow us to

find the operating cash flow using the tax shield approach. Both the revenues and expenses are growing

annuities, but growing at different rates. This means we must find the present value of each separately.

We also need to account for the effect of taxes, so we will multiply by one minus the tax rate. So, the

present value of the aftertax revenues using the growing annuity equation is:

first year is a nominal value, so we can find the present value of the depreciation tax shield as an

ordinary annuity using the nominal required return. So, the present value of the depreciation tax shield

will be:

PV of depreciation tax shield = ($650,000/7)(.24)(PVIFA12.35%,7)

PV of depreciation tax shield = $100,587.68

Taxes

34,182.87

35,785.71

37,340.03

38,847.86

Net income

$108,245.77

$113,321.42

$118,243.41

$123,018.22

$184,639.57

$186,077.42

$187,534.84

$189,010.06

Capital spending

Total cash flow

$184,639.57

$186,077.42

$187,534.84

$189,010.06

27. Here we have a project in which the quantity sold each year increases. First, we need to calculate the

quantity sold each year by increasing the current year’s quantity by the growth rate. So, the quantity

sold each year will be:

Year 1 quantity = 10,400

Year 2 quantity = 10,400(1 + .08) = 11,232

Now we can calculate the sales revenue and variable costs each year. The pro forma income statements

and operating cash flow each year will be:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Revenues

$634,400.00

$685,152.00

$739,964.16

$799,161.29

$863,094.20

Fixed costs

125,000.00

125,000.00

125,000.00

125,000.00

125,000.00

Variable costs

Depreciation

EBT

Taxes

Net income

$155,472.00

$183,077.76

$212,891.98

$245,091.34

$279,866.65

$270,472.00

$298,077.76

$327,891.98

$360,091.34

$394,866.65

Capital spending

NWC

Total cash flow

$270,472.00

$298,077.76

$327,891.98

$360,091.34

$439,866.65

So, the NPV of the project is:

NPV = –$620,000 + $270,472/1.18 + $298,077.76/1.182 + $327,891.98/1.183

+ $360,091.34/1.184 + $439,866.65/1.185

We could also calculate the cash flows using the tax shield approach, with growing annuities and

ordinary annuities. The sales and variable costs increase at the same rate as sales, so both are growing

annuities. The fixed costs and depreciation are both ordinary annuities. Using the growing annuity

equation, the present value of the revenues is:

And the present value of the variable costs will be:

PV of variable costs = $706,900.48

The fixed costs and depreciation are both ordinary annuities. The present value of each is:

PV of fixed costs = C({1 – [1/(1 + r)]t}/r)

PV of fixed costs = $125,000(PVIFA18%,5)

Now, we can use the depreciation tax shield approach to find the NPV of the project, which is:

28. We will begin by calculating the aftertax salvage value of the equipment at the end of the project’s

life. The aftertax salvage value is the market value of the equipment minus any taxes paid (or

refunded), so the aftertax salvage value in four years will be:

Taxes on salvage value = (BV – MV)tC

Taxes on salvage value = ($0 – 310,000)(.23)

NWC

–225,000

225,000

Total cash flow

–$4,525,000

$1,389,210

$1,635,867

$1,663,591

$2,650,593

Notice the calculation of the cash flow at Time 0. The capital spending on equipment and investment

Revenues

$2,165,500

$2,409,500

$2,806,000

$1,860,500

Fixed costs

375,000

375,000

375,000

375,000

Net income

$1,160,051

29. The aftertax salvage value will be the same as the previous problem, $238,700. We need to calculate

the operating cash flow each year. Note, we assume that the net working capital cash flow occurs

immediately. Using the bottom up approach to calculating operating cash flow, we find:

Year 0

Year 1

Year 2

Year 3

Year 4

Revenues

$2,165,500

$2,409,500

$2,806,000

$1,860,500

Fixed costs

375,000

375,000

375,000

375,000

Capital spending

–$3,400,000

238,700

Land

–900,000

1,200,000

NWC

225,000

Total cash flow

$1,910,570

$1,288,268

$1,547,777

$2,592,647

Notice the calculation of the cash flow at Time 0. The capital spending on equipment and investment

30. Replacement decision analysis is the same as the analysis of two competing projects; in this case, keep

the current equipment, or purchase the new equipment. We will consider the purchase of the new

machine first.

Purchase new machine:

The initial cash outlay for the new machine is the cost of the new machine. We can calculate the

Variable costs

361,425

420,900

279,075

Depreciation

EBT

Taxes

384,807

462,323

277,478

Net income

$1,288,268

$1,547,777

$928,947

end of five years, so we need to include this in the cash flows analysis. The aftertax salvage value will

be:

Sell machine

$900,000

Taxes

–189,000

Total

$711,000

The NPV of purchasing the new machine is:

could sell the old machine. Also, if the company sells the old machine at its current value, it will incur

taxes. Both of these cash flows need to be included in the analysis. So, the initial cash flow of keeping

the old machine will be:

Keep machine

–$2,800,000

Taxes

252,000

Total

Maintenance cost

Depreciation

EBT

–$1,250,000

Taxes

Net income

Next, we can calculate the operating cash flow created if the company keeps the old machine. We need

to account for the cost of maintenance, as well as the cash flow effects of depreciation. The pro forma

income statement, adding depreciation to net income to calculate the operating cash flow will be:

Maintenance cost

$855,000

Depreciation

320,000

EBT

–$1,175,000

The old machine also has a salvage value at the end of five years, so we need to include this in the

cash flows analysis. The aftertax salvage value will be:

Sell machine

$140,000

Taxes

–29,400

Total

The company should buy the new machine since it has a greater NPV.

There is another way to analyze a replacement decision that is often used. It is an incremental cash

flow analysis of the change in cash flows from the existing machine to the new machine, assuming the

new machine is purchased. In this type of analysis, the initial cash outlay would be the cost of the new

machine, and the cash inflow (including any applicable taxes) of selling the old machine. In this case,

the initial cash flow under this method would be:

Purchase new machine

–$4,500,000

Sell old machine

Taxes on old machine

Total

–$1,952,000

Taxes

Net income

The cash flows from purchasing the new machine would be the difference in the operating expenses.

We would also need to include the change in depreciation. The old machine has a depreciation of

the new machine, and incur taxes on the sale in five years. However, we must also include the lost sale

of the old machine. Since we assumed we sold the old machine in the initial cash outlay, we lose the

ability to sell the machine in five years. This is an opportunity loss that must be accounted for. So, the

salvage value is:

Sell machine

$900,000

Taxes

Total

$600,400

Depreciation

EBT

Taxes

31. The project has a sales price that increases at 3 percent per year, and a variable cost per unit that

increases at 4 percent per year. First, we need to find the sales price and variable cost for each year.

The table below shows the price per unit and the variable cost per unit each year.

Year 1

Year 2

Year 3

Year 4

Year 5

Using the sales price and variable cost, we can now construct the pro forma income statement for each

year. We can use this income statement to calculate the cash flow each year. We must also make sure

to include the net working capital outlay at the beginning of the project, and the recovery of the net

working capital at the end of the project. The pro forma income statement and cash flows for each year

will be:

Year 0

Year 1

Year 2

Year 3

Year 4

Year 5

Revenues

$1,175,000.00

$1,210,250.00

$1,246,557.50

$1,283,954.23

$1,322,472.85

Fixed costs

235,000.00

235,000.00

235,000.00

235,000.00

235,000.00

Var. costs

425,000.00

442,000.00

459,680.00

478,067.20

497,189.89

Depreciation

EBT

Taxes

Net income

Cap. spend.

–$1,200,000

NWC

Total CF

With these cash flows, the NPV of the project is:

NPV = –$1,400,000 + $457,250/1.11 + $471,667.50/1.112 + $486,383.23/1.113

+ $501,400.75/1.114 + $716,723.54/1.115

Sales price

Cost per unit

The fixed costs and depreciation are both ordinary annuities. The present value of each is:

PV of fixed costs = C({1 – [1/(1 + r)]t}/r)

Challenge

32. Probably the easiest OCF calculation for this problem is the bottom up approach, so we will construct

an income statement for each year. Beginning with the initial cash flow at time zero, the project will

require an investment in equipment. The project will also require an investment in NWC of

$1,500,000. So, the cash flow required for the project today will be:

Capital spending

–$18,500,000

Year

1

2

3

4

5

Ending book value

$15,856,350

$11,325,700

$8,090,050

$5,779,400

$4,127,350

Sales

$23,725,000

$25,675,000

$27,300,000

$26,650,000

$22,100,000

Variable costs

10,585,000

11,455,000

12,180,000

11,890,000

9,860,000

Fixed costs

3,400,000

3,400,000

3,400,000

3,400,000

3,400,000

Depreciation

2,643,650

4,530,650

3,235,650

2,310,650

1,652,050

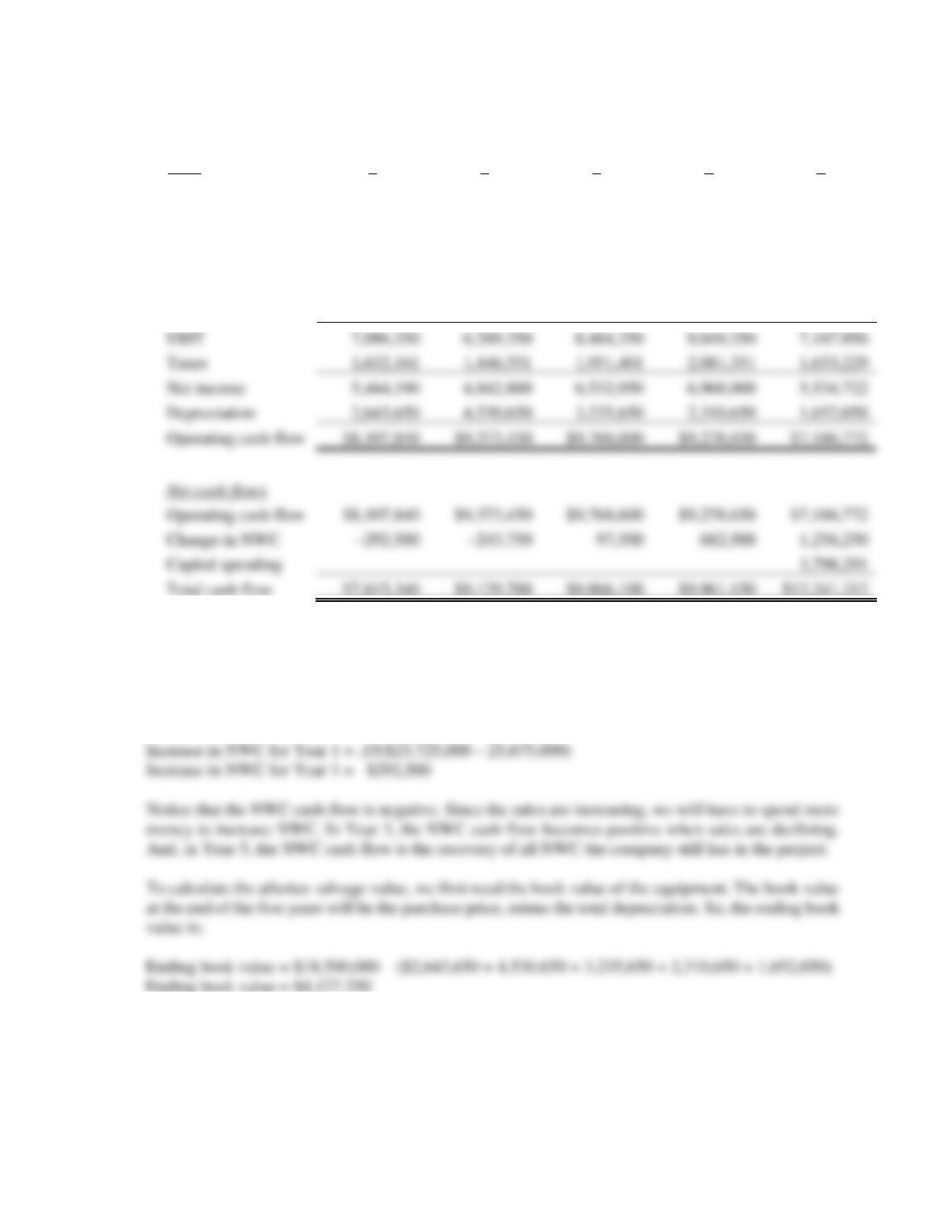

After we calculate the OCF for each year, we need to account for any other cash flows. The other cash

flows in this case are NWC cash flows and capital spending, which is the aftertax salvage of the

equipment. The required NWC is 15 percent of the sales increase in the next year. We will work

through the NWC cash flow for Year 1. The total NWC in Year 1 will be 15 percent of the sales

increase from Year 1 to Year 2, or:

The market value of the used equipment is 20 percent of the purchase price, or $3,700,000, so the

aftertax salvage value will be:

Aftertax salvage value = $3,700,000 + ($4,127,350 – 3,700,000)(.23)

Aftertax salvage value = $3,798,291

EBIT

7,096,350

6,289,350

8,484,350

9,049,350

7,187,950

Taxes

1,632,161

1,446,551

1,951,401

2,081,351

1,653,229

Net income

5,464,190

4,842,800

6,532,950

6,968,000

5,534,722

Depreciation

2,643,650

4,530,650

3,235,650

2,310,650

1,652,050

Operating cash flow

$8,107,840

$9,373,450

$9,768,600

$9,278,650

$7,186,772

Operating cash flow

Change in NWC

1,256,250

Capital spending

3,798,291

Total cash flow

$12,241,312

The aftertax salvage value is included in the total cash flows as capital spending. Now we have all of

the cash flows for the project. The NPV of the project is:

33. To find the initial pretax cost savings necessary to buy the new machine, we should use the tax shield

approach to find the OCF. We begin by calculating the depreciation each year using the MACRS

depreciation schedule. The depreciation each year is:

D1 = $645,000(.3333) = $214,978.50

D2 = $645,000(.4445) = $286,702.50

34. To find the bid price, we need to calculate all other cash flows for the project, and then solve for the

bid price. The aftertax salvage value of the equipment is:

Aftertax salvage value = $150,000(1 – .21)

Aftertax salvage value = $118,500

35. a. This problem is basically the same as the previous problem, except that we are given a sales

price. The cash flow at Time 0 for all three parts of this question will be:

Capital spending

–$2,100,000

Change in NWC

–325,000

Total cash flow

–$2,425,000

We will use the initial cash flow and the salvage value we already found in that problem. Using

the bottom up approach to calculating the OCF, we get:

Assume price per unit = $20 and units/year = 145,000

Year

1

2

3

4

5

Sales

$2,900,000

$2,900,000

$2,900,000

$2,900,000

$2,900,000

Variable costs

1,370,250

1,370,250

1,370,250

1,370,250

1,370,250

Fixed costs

650,000

650,000

650,000

650,000

650,000

Depreciation

EBIT

Taxes

Net Income

Depreciation

420,000

420,000

420,000

420,000

420,000

Operating CF

Year

1

2

3

4

5

Operating CF

Change in NWC

Capital spending

118,500

Total CF

$1,226,703