With these cash flows, the NPV of the project is:

b. To find the minimum number of cartons sold to still break even, we need to use the tax shield

approach to calculating OCF, and solve the problem similar to finding a bid price. Using the

initial cash flow and salvage value we already calculated, the equation for a zero NPV of the

project is:

NPV = 0 = –$2,100,000 – 325,000 + OCF(PVIFA11%,5) + [($325,000 + 118,500)/1.115]

As a check, we can calculate the NPV of the project with this quantity. The calculations are:

Year

1

2

3

4

5

Sales

$2,424,189

$2,424,189

$2,424,189

$2,424,189

$2,424,189

Variable costs

1,145,429

1,145,429

1,145,429

1,145,429

1,145,429

Fixed costs

Depreciation

420,000

420,000

420,000

420,000

EBIT

$208,760

$208,760

$208,760

$208,760

Taxes

Net Income

$164,920

$164,920

$164,920

$164,920

Depreciation

420,000

420,000

420,000

420,000

Operating CF

Year

1

2

3

4

5

Operating CF

$584,920

$584,920

$584,920

$584,920

$584,920

Change in NWC

0

0

0

0

325,000

Capital spending

Total CF

c. To find the highest level of fixed costs and still break even, we need to use the tax shield approach

to calculating OCF, and solve the problem similar to finding a bid price. Using the initial cash

flow and salvage value we already calculated, the equation for a zero NPV of the project is:

NPV = 0 = –$2,100,000 – 325,000 + OCF(PVIFA11%,5) + [($325,000 + 118,500)/1.115]

As a check, we can calculate the NPV of the project with this quantity. The calculations are:

Year

1

2

3

4

5

Sales

$2,900,000

$2,900,000

$2,900,000

$2,900,000

$2,900,000

Variable costs

1,370,250

1,370,250

1,370,250

1,370,250

1,370,250

Fixed costs

Depreciation

EBIT

Taxes

Net Income

Depreciation

Operating CF

Year

1

2

3

4

5

Operating CF

Change in NWC

Capital spending

Total CF

36. We need to find the bid price for a project, but the project has extra cash flows. Since we don’t already

produce the keyboard, the sales of the keyboard outside the contract are relevant cash flows. Since we

know the extra sales number and price, we can calculate the cash flows generated by these sales. The

cash flow generated from the sale of the keyboard outside the contract is:

Year 1

Year 2

Year 3

Year 4

we include these here. Remember that we are not only trying to determine the bid price, but we are

also determining whether or not the project is feasible. In other words, we are trying to calculate the

NPV of the project, not just the NPV of the bid price. We will include these cash flows in the bid price

calculation. Whether we include these costs in this initial calculation is irrelevant since you will come

up with the same bid price if you include these costs in this calculation, or if you include them in the

Solving for the OCF, we get:

OCF = $1,748,613.12/PVIFA13%,4

OCF = $587,873.59

Now we can solve for the bid price as follows:

EBT

Tax

37. a. Since the two computers have unequal lives, the correct method to analyze the decision is the

EAC. We will begin with the EAC of the new computer. Using the depreciation tax shield

approach, the OCF for the new computer system is:

OCF = ($85,000)(1 – .21) + ($580,000/5)(.21) = $91,510

Notice that the costs are positive, which represents a cash inflow. The costs are positive in this

OCF = $90,000(.21)

OCF = $18,900

The initial cost of the old computer is a little trickier. You might assume that since we already

own the old computer there is no initial cost, but we can sell the old computer, so there is an

opportunity cost. We need to account for this opportunity cost. To do so, we will calculate the

Aftertax salvage value = $60,000 + ($90,000 – 60,000)(.21)

Aftertax salvage value = $66,300

Now we can calculate the PV of costs of the old computer as:

PV of costs = –$238,400 + $18,900(PVIFA14%,2) + $66,300/1.142

PV of costs = –$156,262.42

b. If we are only concerned with whether or not to replace the machine now, and are not worrying

about what will happen in two years, the correct analysis is NPV. To calculate the NPV of the

decision on the computer system now, we need the difference in the total cash flows of the old

computer system and the new computer system. From our previous calculations, we can say the

cash flows for each computer system are:

t

New computer

Old computer

Difference

0

–$580,000

–$238,400

–$341,600

1

91,510

18,900

72,610

4

91,510

91,510

5

38. To answer this question, we need to compute the NPV of all three alternatives, specifically, continue

to rent the building, Project A, or Project B. We would choose the project with the highest NPV. If all

three of the projects have a positive NPV, the project that is more favorable is the one with the highest

NPV

There are several important cash flows we should not consider in the incremental cash flow analysis.

The remaining fraction of the value of the building and depreciation are not incremental and should

We will begin by calculating the NPV of the decision of continuing to rent the building first.

Continue to rent:

Rent

$75,000

Since there is no incremental depreciation, the operating cash flow is the net income. So, the NPV of

the decision to continue to rent is:

Product A:

Next, we will calculate the NPV of the decision to modify the building to produce Product A. The

income statement for this modification is the same for the first 14 years, and in Year 15, the company

will have an additional expense to convert the building back to its original form. This will be an

expense in Year 15, so the income statement for that year will be slightly different. The cash flow at

time zero will be the cost of the equipment, and the cost of the initial building modifications, both of

which are depreciable on a straight-line basis. So, the pro forma cash flows for Product A are:

Initial cash outlay:

Building modifications

–$115,000

Equipment

–340,000

Total cash flow

–$455,000

Years 1-14

Year 15

Revenue

$275,000

$275,000

Expenditures

115,000

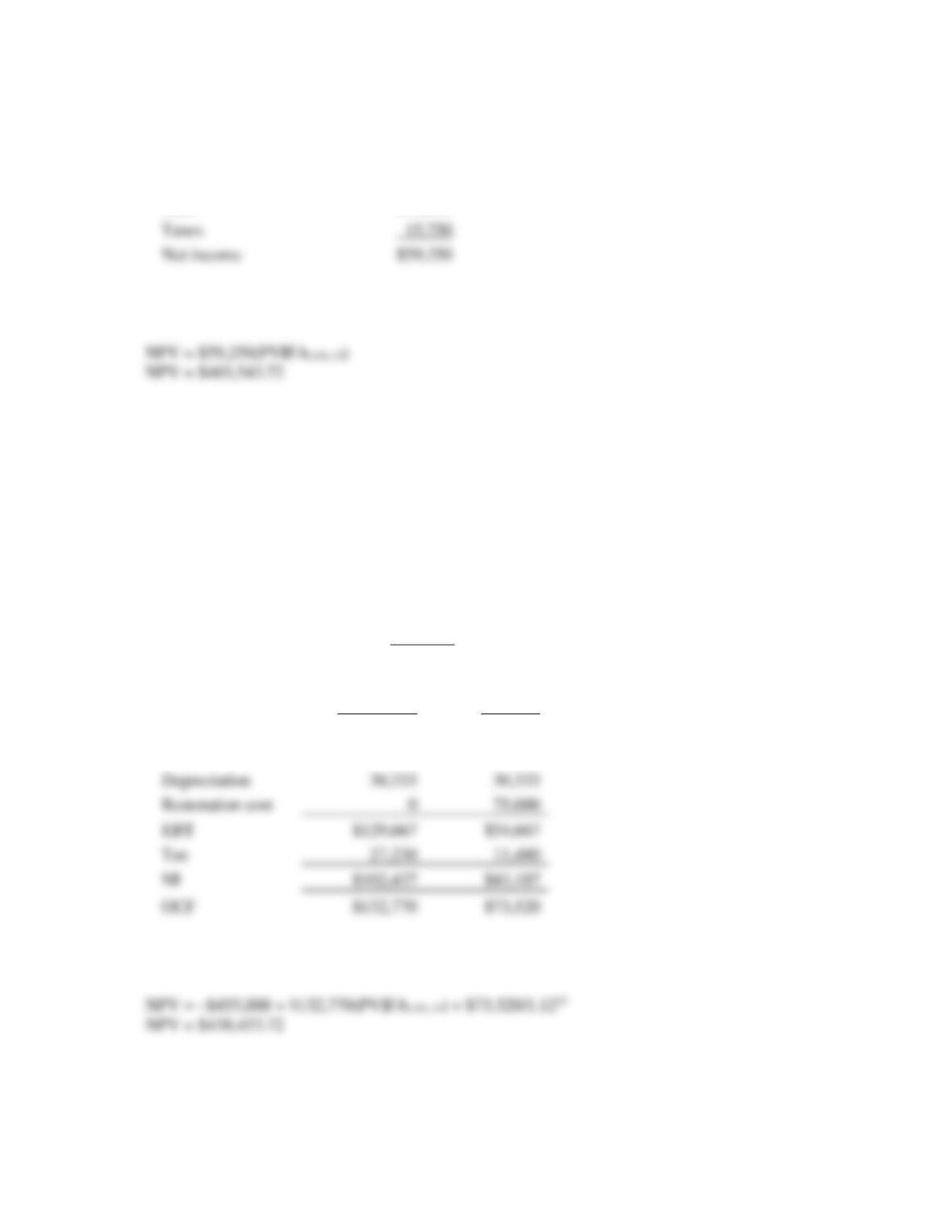

115,000

Depreciation

Restoration cost

EBT

$129,667

$54,667

Tax

The OCF each year is net income plus depreciation. So, the NPV for modifying the building to

manufacture Product A is:

Taxes

Net income

Product B:

Now we will calculate the NPV of the decision to modify the building to produce Product B. The

income statement for this modification is the same for the first 14 years, and in Year 15, the company

will have an additional expense to convert the building back to its original form. This will be an

expense in Year 15, so the income statement for that year will be slightly different. The cash flow at

time zero will be the cost of the equipment, and the cost of the initial building modifications, both of

which are depreciable on a straight-line basis. So, the pro forma cash flows for Product B are:

Initial cash outlay:

Building modifications

–$160,000

Years 1-14

Year 15

Revenue

$295,000

$295,000

Expenditures

130,000

130,000

Depreciation

33,667

33,667

Restoration cost

85,000

EBT

$131,333

Tax

27,580

$103,753

$70,270

The OCF each year is net income plus depreciation. So, the NPV for modifying the building to

manufacture Product B is:

Since Product A has the highest NPV, the company should choose that option.

We could have also done the analysis as the incremental cash flows between Product A and continuing

to rent the building, and the incremental cash flows between Product B and continuing to rent the

building. The results of this type of analysis would be:

NPV of differential cash flows between Product A and continuing to rent:

NPV of differential cash flows between Product B and continuing to rent:

NPV = NPVProduct B – NPVRent

Equipment

Total cash flow

39. The discount rate is expressed in real terms, and the cash flows are expressed in nominal terms. We

can answer this question by converting all of the cash flows to real dollars. We can then use the real

interest rate. The real value of each cash flow is the present value of the Year 1 nominal cash flows,

discounted back to the present at the inflation rate. So, the real value of the revenue and costs will be:

Revenue in real terms = $415,000/1.06 = $391,509.43

rate. Therefore, the lease payments form a growing perpetuity with a negative growth rate. The real

present value of the lease payments is:

PVLease payments = $150,943.40/[.10 – (–.06)] = $943,396.23

Now we can use the tax shield approach to calculate the net present value. Since there is no investment

in equipment, there is no depreciation; therefore, no depreciation tax shield, so we will ignore this in

40. We are given the real revenue and costs, and the real growth rates, so the simplest way to solve this

problem is to calculate the NPV with real values. While we could calculate the NPV using nominal

values, we would need to find the nominal growth rates, and convert all values to nominal terms. The

real labor costs will increase at a real rate of 2 percent per year, and the real energy costs will increase

at a real rate of 3 percent per year, so the real costs each year will be:

Depreciation is a nominal cash flow, so to find the real value of depreciation each year, we discount

the real depreciation amount by the inflation rate. Doing so, we find the real depreciation each year

is:

Year 1 real depreciation = $28,750,000/1.05 = $27,380,952.38

Year 2 real depreciation = $28,750,000/1.052 = $26,077,097.51

Now we can calculate the pro forma income statement each year in real terms. We can then add back

depreciation to net income to find the operating cash flow each year. Doing so, we find the cash flow

of the project each year is:

Year 0

Year 1

Year 2

Year 3

Year 4

Revenues

$60,175,000.00

$68,475,000.00

$74,700,000.00

$64,325,000.00

Labor cost

Energy cost

Depreciation

EBT

$14,349,047.62

$22,230,927.49

$26,540,877.29

$18,271,024.51

Taxes

3,013,300.00

4,668,494.77

5,573,584.23

3,836,915.15

Net income

Cap. spend.

Real labor cost each year

Real energy cost each year

41. Here we have the sales price and production costs in real terms. The simplest method to calculate the

project cash flows is to use the real cash flows. In doing so, we must be sure to adjust the depreciation,

which is in nominal terms. We could analyze the cash flows using nominal values, which would

require calculating the nominal discount rate, nominal price, and nominal production costs. This

method would be more complicated, so we will use the real numbers. We will first calculate the NPV

Sales

Production costs

11,520,000

11,520,000

11,520,000

Depreciation

EBT

$5,818,511

$6,082,438

$6,338,678

Tax

1,280,072

1,338,136

1,394,509

Net income

$4,538,439

$4,744,302

$4,944,169

OCF

$13,599,928

$13,541,864

$13,485,491

And the NPV of the headache only pill is:

Market value

Taxes

Total

year for the headache and arthritis pill will be:

Year 1

Year 2

Year 3

Sales

$40,425,000

$40,425,000

$40,425,000

Production costs

22,295,000

22,295,000

22,295,000

Depreciation

11,650,485

11,311,151

10,981,700

EBT

$6,479,515

$6,818,849

$7,148,300

Tax

Net income

$5,054,021

$5,318,702

$5,575,674

$16,704,507

$16,629,853

$16,557,374

42. Since the project requires an initial investment in inventory as a percentage of sales, we will calculate

the sales figures for each year first. The incremental sales will include the sales of the new table, but

we also need to include the lost sales of the existing model. This is an erosion cost of the new table.

The lost sales of the existing table are constant for every year, but the sales of the new table change

every year. So, the total incremental sales figure for the five years of the project will be:

New

Lost sales

Total

initial cash flow is the cost of the inventory. The company will have to spend money for inventory

with the new table, but will be able to reduce inventory of the existing table. So, the initial cash flow

today is:

New table

–$1,062,000

Old table

107,500

Total

So, the aftertax salvage value of the equipment in five years will be:

Sell equipment

$6,800,000

Taxes

461,328

Salvage value

$5,261,328

Next, we need to calculate the variable costs each year. The variable costs of the lost sales are included

$3,929,400

$4,693,450

$5,675,800

$5,130,050

$4,802,600

Sales

$9,545,000

VC

3,499,400

4,263,450

5,245,800

4,700,050

4,372,600

Fixed costs

2,050,000

2,050,000

2,050,000

2,050,000

2,050,000

Dep.

0

0

2,286,400

3,918,400

2,798,400

EBT

$3,995,600

$5,296,550

$4,682,800

$2,121,550

$2,684,000

Tax

839,076

1,112,276

983,388

445,526

563,640

NI

$3,156,524

$4,184,275

$3,699,412

$1,676,025

$2,120,360

+Dep.

0

0

2,286,400

3,918,400

2,798,400

Old table

–107,500

Change

–$206,500

–$265,500

$147,500

$88,500

$1,190,500

Notice that we recover the remaining inventory at the end of the project. We must also spend $138,000

for inventory since the 250 units per year in sales of the oak table will begin again. The total cash

flows for the project will be the sum of the operating cash flow, the capital spending, and the inventory

Equipment

Inventory

Total

The company should go ahead with the new table.

b. You can perform an IRR analysis, and would expect to find three IRRs since the cash flows

change signs three times.

c. The profitability index is intended as a “bang for the buck” measure; that is, it shows how much

shareholder wealth is created for every dollar of initial investment. This is usually a good measure