1

2

3

4

5

6

7

8

9

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

A B C D E F G H I

11/20/2018

Amount invested $1,000

Amount received in one year $1,060

Dollar return (Profit) $60

Rate of return = Profit/Investment = 6%

Return on a 10–

Year Zero

Coupon

Treasury Bond

During Next

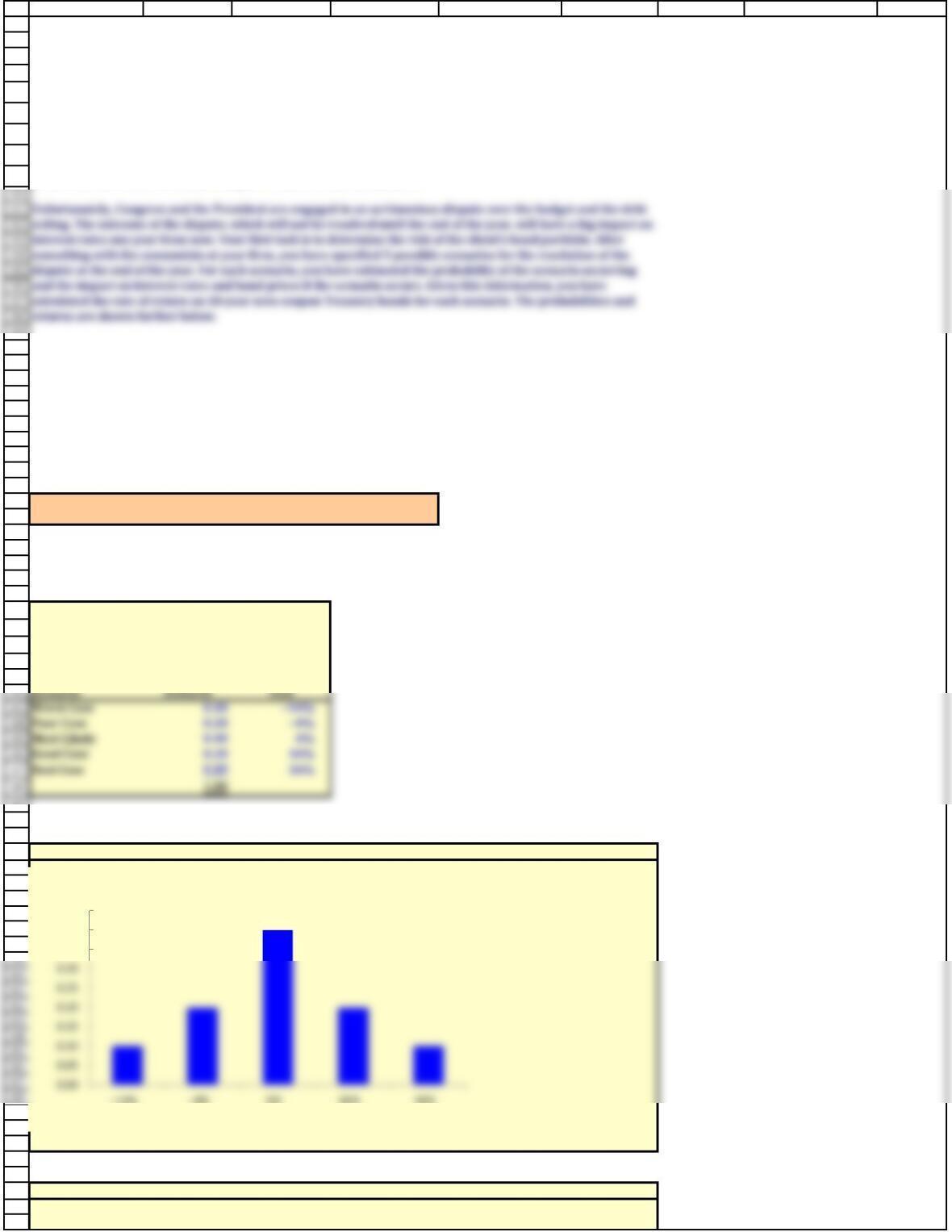

Probability of

Discrete Probability Distribution for 5 Scenarios

CHAPTER 6 MINI CASE

a. What are investment returns? What is the return on an investment that costs $1,000 and is sold after 1 year

for $1,060?

b. Graph the probability distribution for the 5 scenarios during the next year for the 10-year zero coupon bonds.

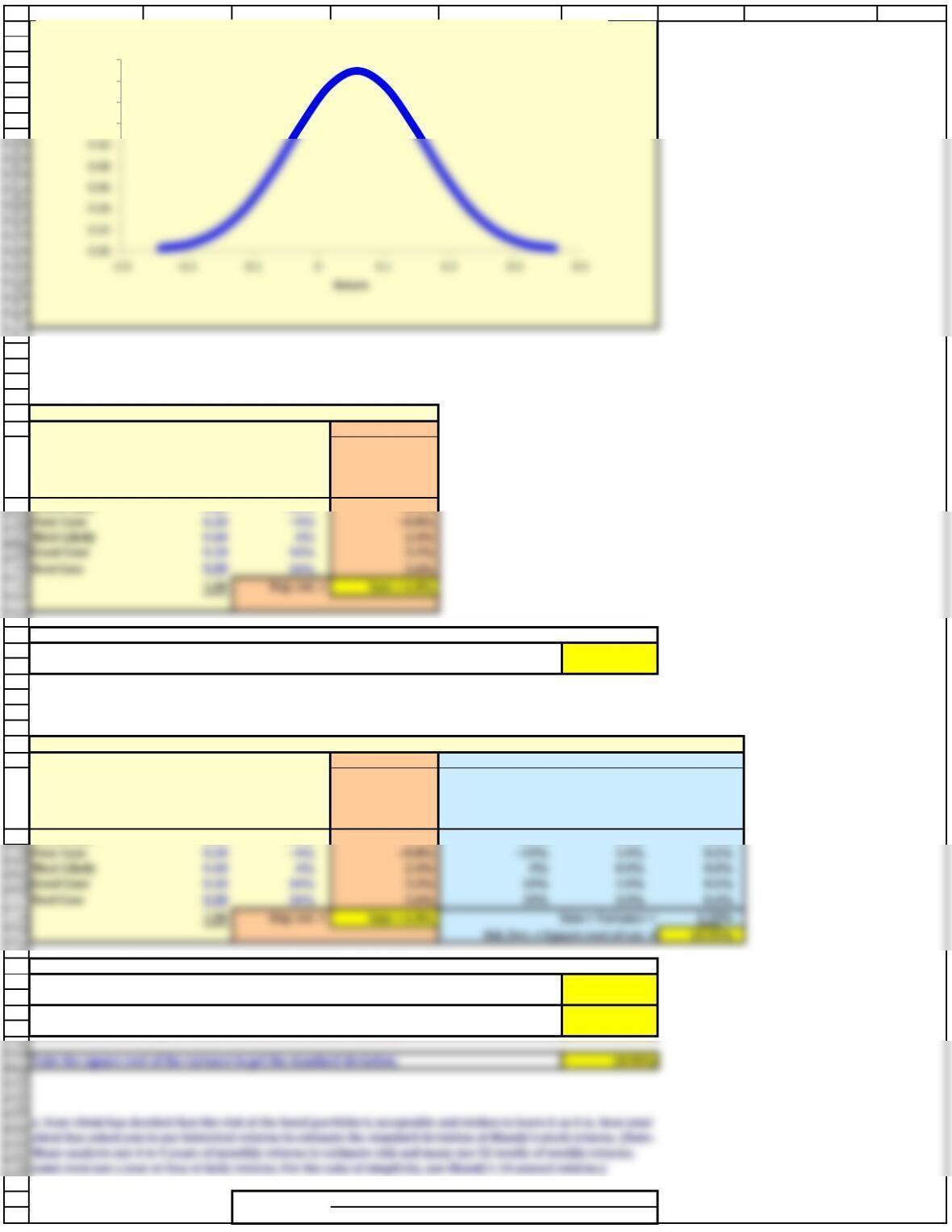

What might the graph of the probability distribution look like if there were an infinite number of scenarios (i.e.,

if it were a continuous distribution and not a discrete distribution)?

Continuous Probability Distribution for Infinite Number of Scenarios

You have also gathered historical returns for the past 10 years for Blandy, Gourmange Corporation (a producer

of gourmet specialty foods), and the stock market.

The risk-free rate is 4% and the market risk premium is 5%.

Assume that you recently graduated and landed a job as a financial planner with Cicero Services, an investment

advisory company. Your first client recently inherited some assets and has asked you to evaluate them. The

client presently owns a bond portfolio with $1 million invested in zero coupon Treasury bonds that mature in

10 years. The client also has $2 million invested in the stock of Blandy, Inc., a company that produces meat-and-

potatoes frozen dinners. Blandy’s slogan is “Solid food for shaky times.”

0.35

0.40

0.45

−14% −4% 6% 16% 26%

Probability of

Scenario

Outcomes: 10-Year Zero-Coupon Bond Returns for 5 Scenarios

Continuous Probability Distribution

10

11

12

13

14

15

16

17

18

dispute at the end of the year. For each scenario, you have estimated the probability of the scenario occurring

and the impact on interest rates and bond prices if the scenario occurs. Given this information, you have

calculated the rate of return on 10-year zero coupon Treasury bonds for each scenario. The probabilities and

returns are shown further below.

77

78

79

80

81

82

83

97

98

99

100

101

102

103

104

105

106

107

108

111

Poor Case 0.20 −4% −0.8%

Most Likely 0.40 6% 2.4%

Good Case 0.20 16% 3.2%

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

129

Poor Case 0.20 −4% −0.8% −10% 1.0% 0.2%

Most Likely 0.40 6% 2.4% 0% 0.0% 0.0%

Good Case 0.20 16% 3.2% 10% 1.0% 0.2%

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

Take the square root of the variance to get the standard deviation.

145

146

147

A B C D E F G H I

Calculating Expected Returns

Inputs: Expected Return

Scenario

Probability of

Scenario

(1)

Rate of Return

(2)

Product of

Probability and

Return

(1) x (2) = (3)

Worst Case 0.10 −14% −1.4%

Excel function for finding expected return of discrete events:

Calculating Expected Returns and Standard Deviations: Discrete Probabilities

Inputs: Expected Return

Scenario

Probability of

Scenario

(1)

Rate of Return

(2)

Product of

Probability and

Return

(1) x (2) = (3)

Deviation from

Expected Return

(2) − Exp. r = (4)

Squared

Deviation

(4)2 = (5)

Sq. Dev. ×

Prob.

(1) x (5) = (6)

Worst Case 0.10 −14% −1.4% −20% 4.0% 0.4%

Excel functions for finding expected return and standard deviation of discrete events

Year Market Blandy Gourmange

Use SUMPRODUCT to find expected return by putting probabilities in first argument array and

rates of return in the second argument array.

Use SUMPRODUCT to find expected return by putting probabilities in first argument array and

rates of return in the second argument array.

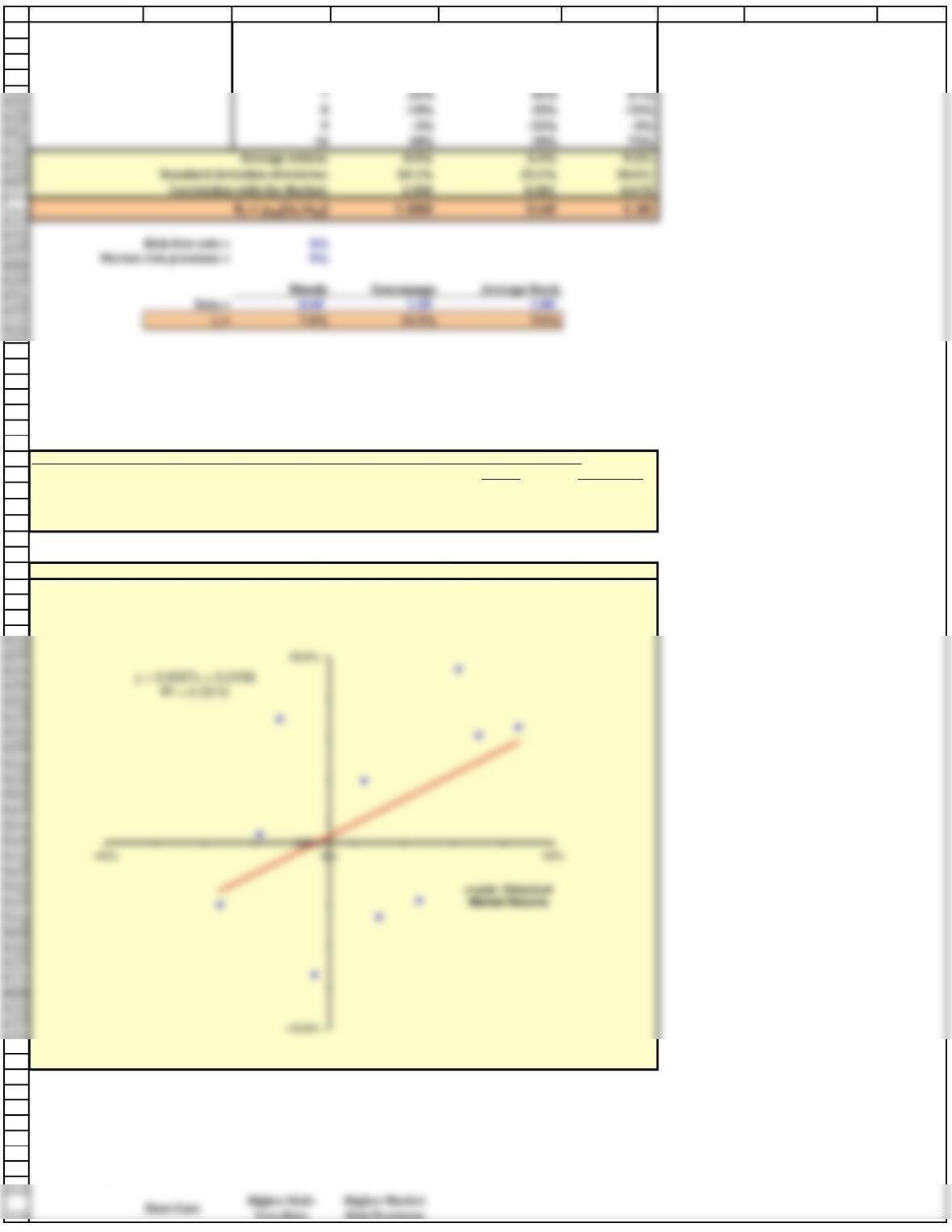

d. What is stand-alone risk? Use the scenario data to calculate the standard deviation of the bond’s return for the

next year.

6%

Standard Deviation

c. Use the scenario data to calculate the expected rate of return for the 10-year zero coupon Treasury bonds

during the next year.

6%

Use SUMPRODUCT to find variance by putting probabilities in first argument array and the

outcomes minus the expected value in the second and third arrays.

1.20%

Stock Returns

0.12

0.14

0.16

0.18

Probability

Continuous Probability Distribution

84

85

86

87

88

89

90

91

92

93

94

95

148

149

150

151

169

170

171

172

173

174

185

175

176

177

178

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

218

219

220

221

222

223

A B C D E F G H I

130% 26% 47%

27% 15% -54%

318% -14% 15%

4 -22% -15% 7%

Blandy Gourmange

Weight in : 75% 25%

Year Blandy Gourmange Portfolio

126% 47% 31.3%

215% -54% -2.3%

3 -14% 15% -6.8%

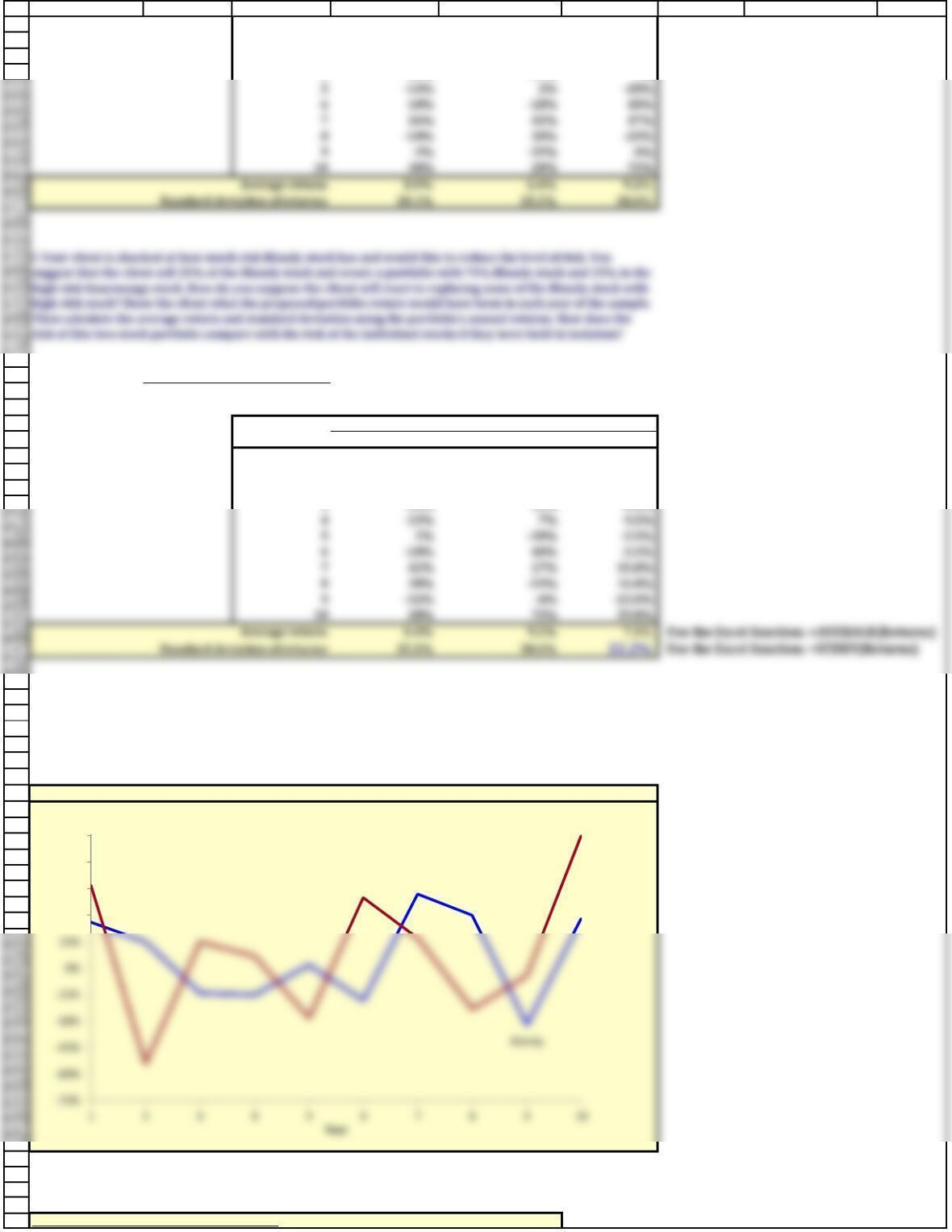

Notice that the historical returns for Blandy and Gourmange do not move in perfect lockstep.

Correlation between Blandy and Gourmange

Loosely speaking, correlation measures the tendency of two variables to move together.

g. Explain correlation to your client. Calculate the estimated correlation between Blandy and Gourmange. Does

this explain why the portfolio standard deviation was less than Blandy’s standard deviation?

Historical Stock Returns for Blandy and Gourmange

Stock Returns

Gourmange

30%

45%

60%

75%

Rate of Return

157

159

225

226

227

228

229

230

231

232

233

234

235

236

237

238

239

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

260

261

262

263

264

265

266

267

stock contributes to the standard deviation of a well-diversified portfolio.

j. According to the Capital Asset Pricing model, what measures the amount of risk that an individual stock

contributes to a well-diversified portfolio? Define this measurement.

268

269

270

271

272

273

274

275

276

277

279

280

281

282

284

285

286

287

288

289

290

291

292

293

294

295

296

298

300

return. Assume that the risk-free rate is 4% and the market risk premium is 5%. Use the SML to estimate

Blandy’s required return.

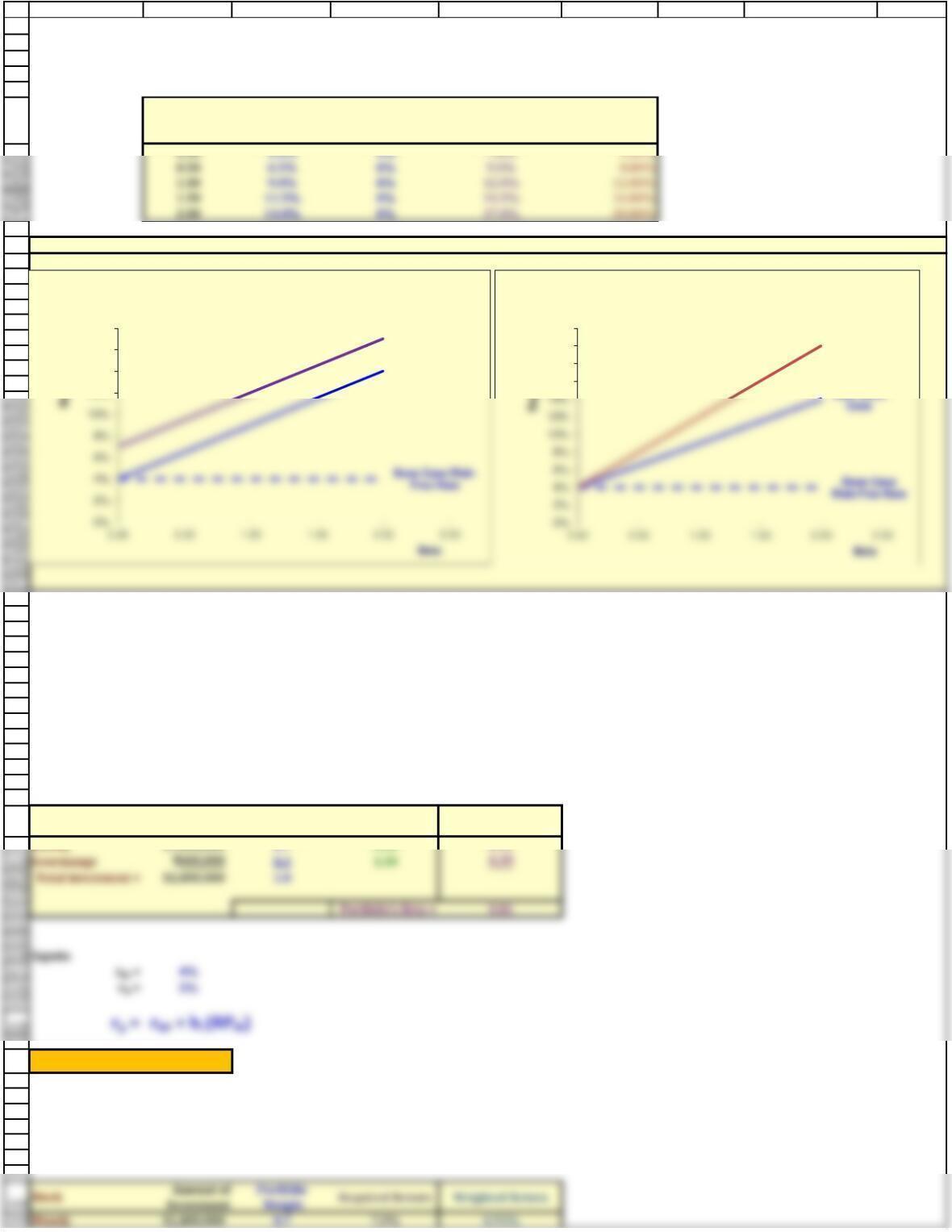

r = 0.11 Use the Excel function: =CORREL(Blandy_returns,Gourmange_returns)

Beta for Stock i = bi = riM(si/sM)

rRF The risk-free rate. It varies over time, but is constant for all firms at a given time.

ri = rRF + bi (RPM)

i. (1.) Should portfolio effects impact the way investors think about the risk of individual stocks? Answer: See Ch

06 Mini Case Show

(2.) If you decided to hold a 1-stock portfolio and consequently were exposed to more risk than diversified

investors, could you expect to be compensated for all of your risk; that is, could you earn a risk premium on that

part of your risk that you could have eliminated by diversifying? Answer: See Ch 06 Mini Case Show

h. Suppose an investor starts with a portfolio consisting of one randomly selected stock. As more and more

randomly selected stocks are added to the portfolio, what happens to the portfolio’s risk?

k. What is the Security Market Line? How is beta related to a stock’s required rate of return?

The SML shows the relationship between the stock’s beta and its required return, as predicted by the CAPM.

The SML predicts stock i’s required return to be:

224

301

302

303

304

321

322

323

324

325

326

327

328

329

330

331

332

333

334

335

336

337

338

339

340

341

342

343

344

345

346

347

348

349

350

351

352

353

354

355

356

357

358

359

360

361

362

363

364

365

366

367

368

369

370

371

372

373

374

375

376

A B C D E F G H I

318% -14% 15%

4 -22% -15% 7%

5 -14% 2% -28%

610% -18% 40%

Blandy Gourmange

bi = riM(si/sM)0.603 1.301 =SLOPE(y_values,x_values)

Intercept 0.016 -0.012 =INTERCEPT(y_values,x_values)

R squared 0.232 0.460 =RSQ(y_values,x_values)

Free Rate

Risk Premium

n. (1) Suppose interest rates go up by 3 percentage points over the current 4% risk-free rate. What effect would

higher interest rates have on the SML and on the returns required on high- and low-risk securities? (2) Suppose

instead that investors’ risk aversion increased enough to cause the market risk premium to increase by 3

percentage points. (Assume the risk-free rate remains constant.) What effect would this have on the SML and on

returns of high- and low-risk securities?

Calculating Beta as the Slope of a Regression Using Excel Functions (See Excel explanations to right)

m. Show how to estimate beta using regression analysis.

Stock Returns of Blandy and the Market: Estimating Beta

Beta can also be calculated as the slope of a regression of the stock (on the y-axis) and the market (on the x-axis).

This can be done using the SLOPE function or by plotting the returns and specifying that the chart show the

TRENDLINE.

y-axis: Historical

Blandy Returns

308

311

313

314

315

316

317

318

320

377

378

379

380

381

382

388

389

390

391

392

393

394

395

396

397

398

399

400

401

402

403

404

405

406

407

408

409

410

411

412

413

414

415

416

417

418

419

420

421

422

423

424

425

426

427

429

430

431

432

433

434

437

439

440

441

442

443

444

445

446

447

449

Amount of

Investment

Portfolio

Weight

A B C D E F G H I

rRF 4% 7% 4%

rM5% 5% 8%

Beta

SML: Base Case

Base Case Risk–

Free Rate

SML: Higher Risk–

Free Rate

SML: Higher

Market Risk

Premium

Stock

Amount of

Investment

Portfolio

Weight

Beta Weighted Beta

rp = 8.06%

Alternative Approach to Find Required Return on Porfolio

Changes to Inputs for the Security Market Line

The Security Market Line shows the projected changes in expected return, due to changes in the beta coefficient.

However, we can also look at the potential changes in the required return due to variations in other factors, for

example the market return and risk-free rate. In other words, we can see how required returns can be

influenced by changing inflation and risk aversion. The level of investor risk aversion is measured by the

market risk premium (rM – rRF), which is also the slope of the SML. Hence, an increase in the market return

results in an increase in the maturity risk premium, other things held constant.

o. Your client decides to invest $1.4 million in Blandy stock and $0.6 million in Gourmange stock. What are the

weights for this portfolio? What is the portfolio’s beta? What is the required return for this portfolio?

The required return on a portfolio is a weighted average of the required returns of the individual assets in the

portfolio.

SML: Base Case

SML: Higher

Risk-Free Rate

12%

14%

16%

18%

Impact of Increase in Risk-Free Rate

SML: Base

SML: Higher

Market Risk

Premium

16%

18%

20%

22%

Impact of Increase in Market Risk Premium

383

384

385

386

387

450

451

452

453

454

455

460

461

462

463

464

465

466

467

468

469

470

471

472

473

474

475

476

477

478

479

480

481

482

483

484

485

486

487

488

489

490

491

492

493

494

495

496

497

498

499

A B C D E F G H I

Gourmange $600,000 0.3 10.5% 3.15%

Total investment = $2,000,000 1.0

Portfolio’s Return = 8.06%

JJ CC

Portfolio beta = 0.7 1.4 0 2

Risk-free rate = 4% 4% 4% 4%

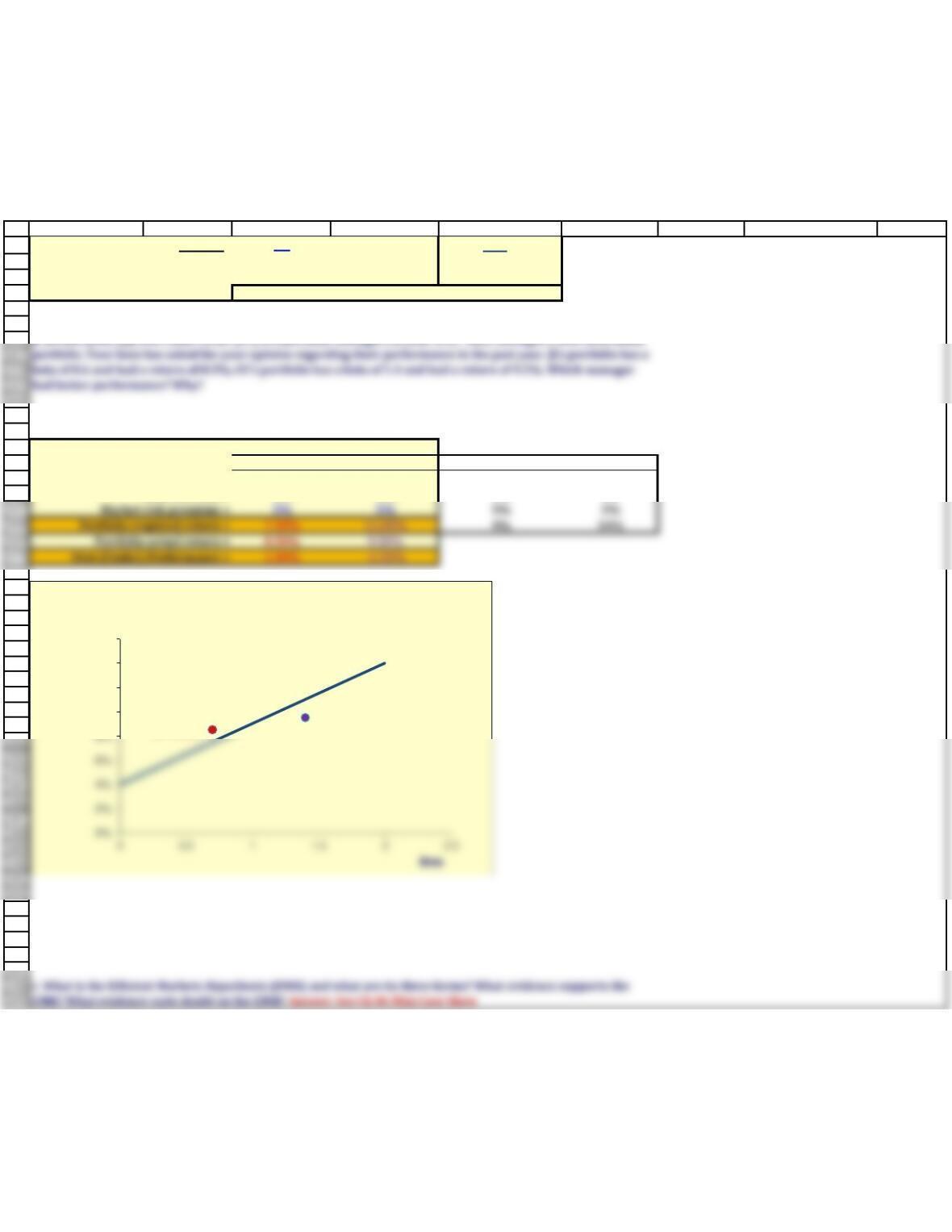

q. What does market equilibrium mean? If equilibrium does not exist, how will it be established? Answer: See Ch

06 Mini Case Show

Portfolio Manager

Additonal data for graph

SML

JJ-Actual CC-Actual

10%

12%

14%

16%

Required Return

Performance Evaluation

456

457

458