Mini Case: 5 – 32

l. What is a bond spread and how is it related to the default risk premium? How

are bond ratings related to default risk? What factors affect a company’s bond

rating?

Answer: A “bond spread” is often calculated as the difference between a corporate bond’s yield

and a Treasury security’s yield of the same maturity. Therefore:

Mini Case: 5 – 33

m. What is interest rate (or price) risk? Which bond has more interest rate risk, an annual

payment 1-year bond or a 10-year bond? Why?

Answer: Interest rate risk, which is often just called price risk, is the risk that a bond will lose

value as the result of an increase in interest rates. Earlier, we developed the following

values for a 10 percent, annual coupon bond:

Maturity

rd 1-Year Change 10-Year Change

5% $1,048 $1,386

38.6%

Mini Case: 5 – 34

n. What is reinvestment rate risk? Which has more reinvestment rate risk, a 1-year

bond or a 10-year bond?

Answer: Investment rate risk is defined as the risk that cash flows (interest plus principal

repayments) will have to be reinvested in the future at rates lower than today’s rate. To

o. How are interest rate risk and reinvestment rate risk related to the maturity risk

premium?

Answer: Long-term bonds have high interest rate risk but low reinvestment rate risk. Short-term

Mini Case: 5 – 35

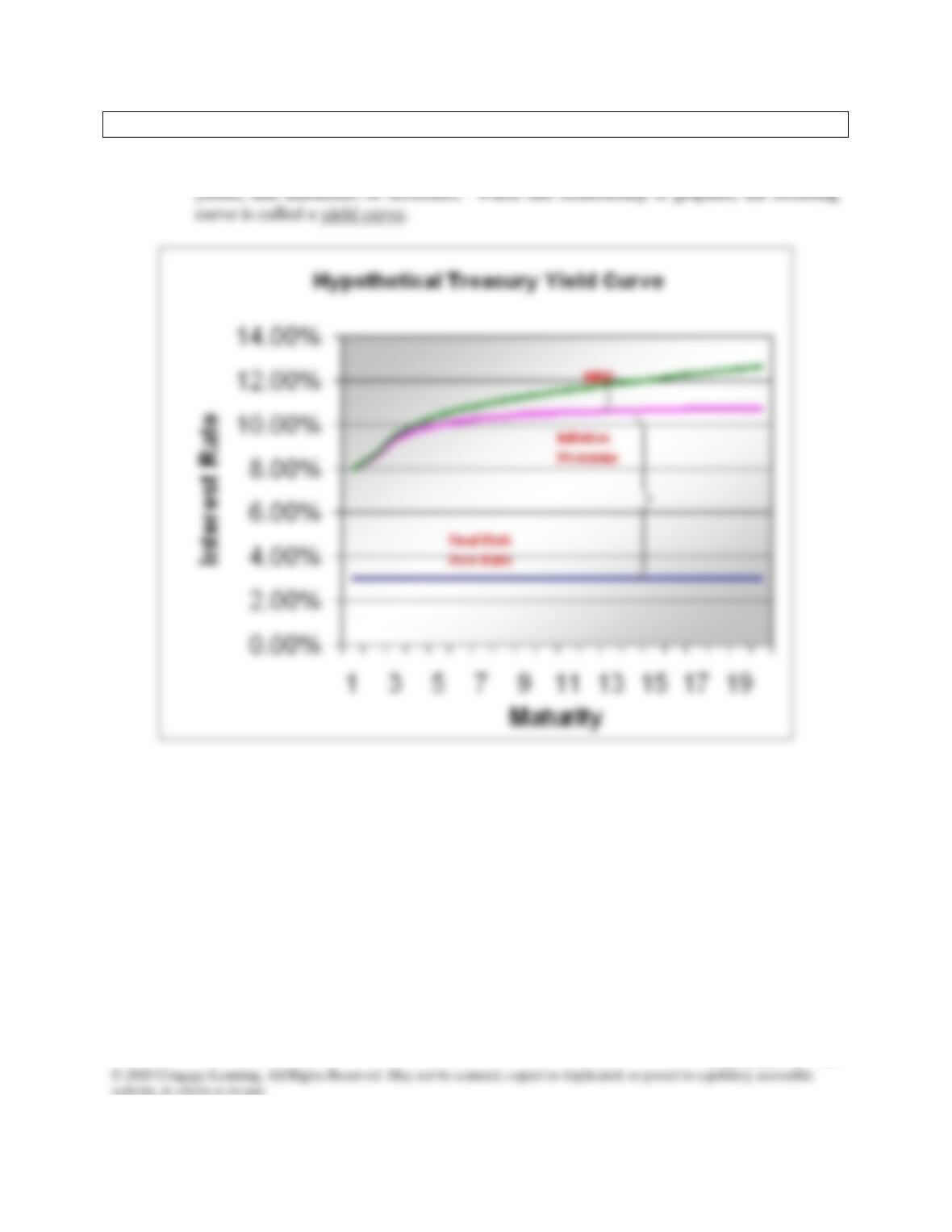

p. What is the term structure of interest rates? What is a yield curve?

Answer: The term structure of interest rates is the relationship between interest rates, or

Mini Case: 5 – 36

q. Briefly describe bankruptcy law. If this firm were to default on the bonds, would

the company be immediately liquidated? Would the bondholders be assured of

receiving all of their promised payments?

Answer: When a business becomes insolvent, it does not have enough cash to meet scheduled

interest and principal payments. A decision must then be made whether to dissolve the

firm through liquidation or to permit it to reorganize and thus stay alive.

Web Solutions: 5 – 37

Web Appendix 5A

A Closer Look at Zero Coupon Bonds, Other OID Bonds,

and Premium Bonds

Answers to Questions

5A-1 No, not all original issue discount bonds have zero coupons. Zero coupon bonds are just

one type of original issue discount bond. Any nonconvertible bond whose coupon rate is

set below the going market rate at the time of its issue will sell at a discount, and its will

be classified (for tax and other purposes) as an OID bond.

5A-3 Treasury zeros are not protected from interest rate (price) risk, because the principal is

totally susceptible to interest rate movements. You can see this by changing interest rates

and seeing what happens to the value of the zero bond. However, since Treasury zeros

generally are not callable and because there are no coupon payments to reinvest, Treasury

zeros are completely protected against reinvestment risk (the risk of having to invest cash

flows from a bond at a lower rate because of a decline in interest rates).

Web Solutions: 5 – 38

Solutions to Problems

5A-1

Year

0

1

2

3

4

Accrued value

$735.03

$793.83

$857.34

$925.93

$1,000.00

Accrued interest

–

$58.80

$63.51

$68.59

$74.07

Tax savings (25%)

–

$14.70

$15.88

$17.15

$18.52

Cash flow

$735.03

$14.70

$15.88

$17.15

($981.48)

Tax savings = Interest(T).

Web Solutions: 5 – 39

5A-2

Year

0

1

2

3

4

Accrued value

$683.01

$751.31

$826.45

$909.09

$1,000.00

Accrued interest

–

$68.30

$75.13

$82.64

$90.91

Tax expense (35%)

–

$23.91

$26.30

$28.93

$31.82

Cash flow

−$683.01

−$23.91

−$26.30

−$28.93

$968.18

Tax expense = Interest(T).

Note that in Year 4, the investor receives the maturity value of the bond; however, he must

pay taxes on the interest income in Year 4. Thus, cash flow in Year 4 equals $1,000 –

Taxes.

To solve for the IRR of this cash flow stream, using a financial calculator, enter the

individual cash flows into the cash flow register and solve for the IRR. IRR = 6.5%.

Alternatively, the after-tax return can be calculated as 0.10(1 – T) = 0.10(1 – 0.35) = 6.5%.

5A-3

Web Solutions: 5 – 40

5A-5 First find the yields on one-year and two-year zero coupon bonds, so you can find the

implied rate on a one-year bond, one year from now. Then use this implied rate to find its

price.

1-Year:

Using a financial calculator, enter the following data: N = 1; PV = -938.9671; PMT = 0;

FV = 1000; and then solve for I/YR = 6.5%.

Now find the price of a 1-year zero, 1 year from now:

Using a financial calculator, enter the following data: N = 1; I/YR = 7.5; PMT = 0; FV =

1000; and then solve for PV = -$930.23.

5A-6 0 10 50

-87.2037 1,000

(1.05)10 = 142.0457

1.10

156.2503

Web Solutions: 5 – 41

Web Appendix 5D

The Pure Expectations Theory and Estimation of Forward

Rates

Solutions to Problems

5D-1 rT1 = 5%; 1rT1 = 6%; rT2 = ?

(1 + rT2)2 = (1.05)(1.06)

(1 + rT2)2 = 1.113

1 + rT2 = 1.055

rT2 = 5.5%.

5D-3 a. (1.045)2 = (1.03)(1 + X)

1.092/1.03 = 1 + X

X = 6%.

b. For riskless bonds under the expectations theory, the interest rate for a bond of any

maturity is

rN = r* + average inflation over N years. If r* = 1%, we can solve for IPN:

Web Solutions: 5 – 42

5D-4 r* = 2%; MRP = 0%; r1 = 5%; r2 = 7%; X = ?

X represents the one-year rate on a bond one year from now (Year 2).