CFIN6 – CHAPTER 5

INTEGRATIVE PROBLEM SOLUTION

a. The dollar return is the amount in dollars that an investor would be paid if an investment is liquidated at

a particular period. For example, If you buy a stock for $40 today, you are paid a $5 dividend during

the year, and you sell the stock for $50 at the end of the year, the total dollar return is $15 = ($50 -$40)

+ $5. The percentage return is simply the dollar return stated as a ratio of the original purchase price of

the investment. In our example, the percentage return is 37.5% = $15/$40.

c. The interest rate is the price paid for borrowed capital, while the return on equity capital comes in the

form of dividends plus capital gains. The return that investors require on capital depends on (1)

production opportunities, (2) time preferences for consumption, (3) risk, and (4) inflation.

Production opportunities refer to the returns that are available from investment in productive assets:

the more productive a producer firm believes its assets will be, the more it will be willing to pay for the

capital necessary to acquire those assets.

Risk is also linked to the maturity and liquidity of a security. The longer the maturity and the less liquid

(marketable) the security, the higher the required rate of return, other things constant.

The preceding discussion related to the general level of money costs, but the level of interest rates

also will be influenced by such things as fed policy, fiscal and foreign trade deficits, and the level of

economic activity. Also, individual securities will have higher yields than the risk-free rate because of

the addition of various premiums as discussed below.

The real risk-free rate, r*, is the rate that would exist on default-free securities in the absence of

inflation.

The nominal risk-free rate, rRF, is equal to the real risk-free rate plus an inflation premium that is equal

to the average rate of inflation expected over the life of the security.

e. The inflation premium (IP) is a premium added to the real risk-free rate of interest to compensate for

expected inflation.

The default risk premium (DRP) is a premium based on the probability that the issuer will default on the

loan, and it is measured by the difference between the interest rate on a U.S. Treasury bond and a

corporate bond of equal maturity and marketability.

(1) Short-term treasury securities include only an inflation premium.

(2) Long-term treasury securities contain an inflation premium plus a maturity risk premium. Note

that the inflation premium added to long-term securities will differ from that for short-term

securities unless the rate of inflation is expected to remain constant.

(3) The rate on short-term corporate securities is equal to the real risk-free rate plus premiums for

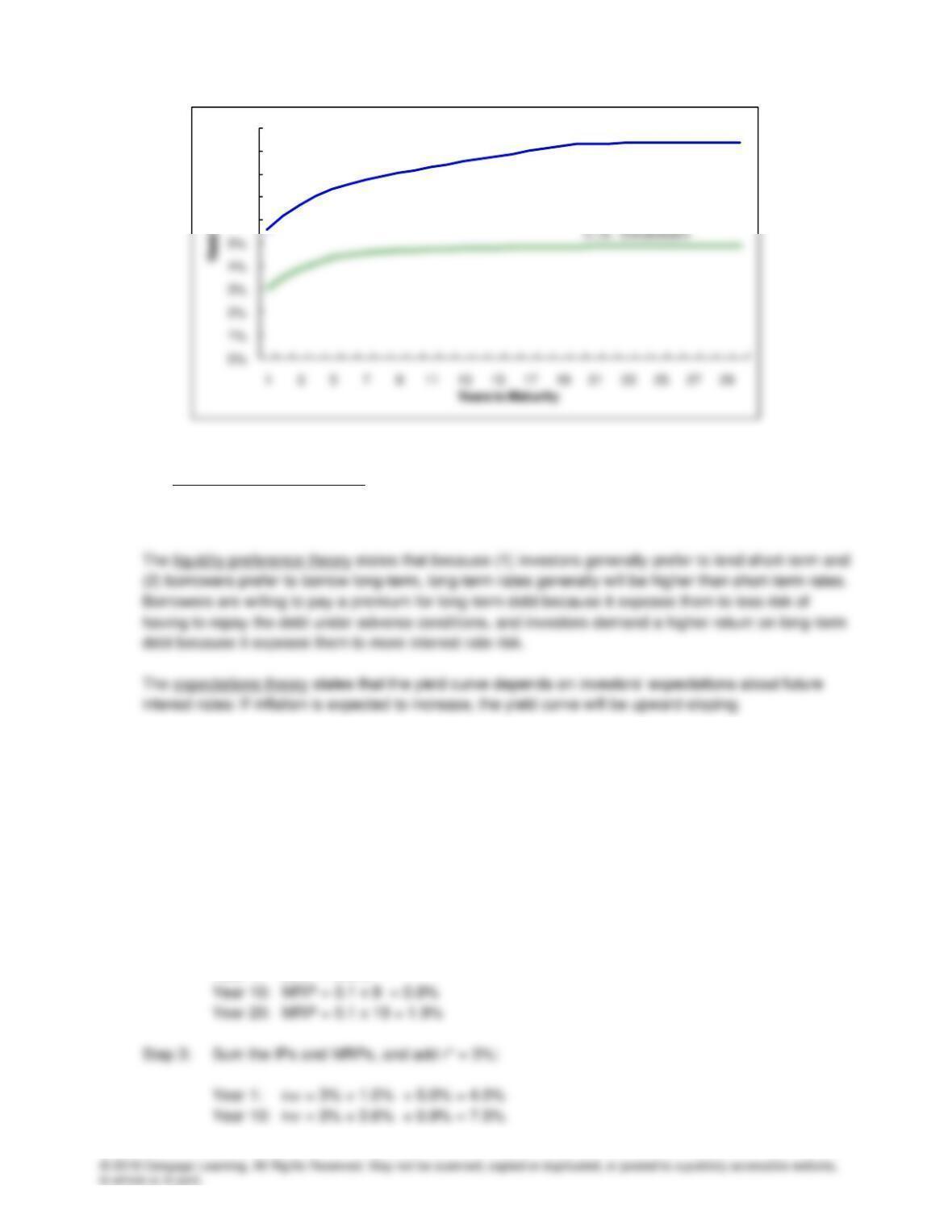

f. The term structure of interest rates is the relationship between interest rates, or yields, and the

maturities of securities. When this relationship is graphed, the resulting curve is called a yield curve.

The yield curve normally slopes upward, indicating that short–term interest rates are lower than

long-term interest rates.

6%

7%

8%

9%

10%

g. The market segmentation theory states that each borrower and lender has a preferred maturity, and

that the slope of the yield curve depends on the supply of and demand for funds in the long-term

market relative to the situation in the short-term market.

All three theories have merit, and each of these factors contribute to the shape of the yield curve.

h. Step 1: Find the average expected inflation rate over years 1 to 20:

Year 1: IP = 1.0%

Year 10: IP = (1 + 3 + 4 + 4 +…+ 4)/10 = 36/10 = 3.6%

Year 20: IP = (1 + 3 + 4 + 4 +…+ 4)/20 = 76/20 = 3.8%

Step 2: Find the maturity premium in each year:

Year 1: MRP = 0.0%

Microsoft

Year 20: rRF = 3% + 3.8% + 1.9% = 8.7%

The yield curve is based directly on, hence is consistent with, at least two of the theories: (1)

expectation and (2) liquidity preferences. It contains a maturity risk premium, which is the essence of

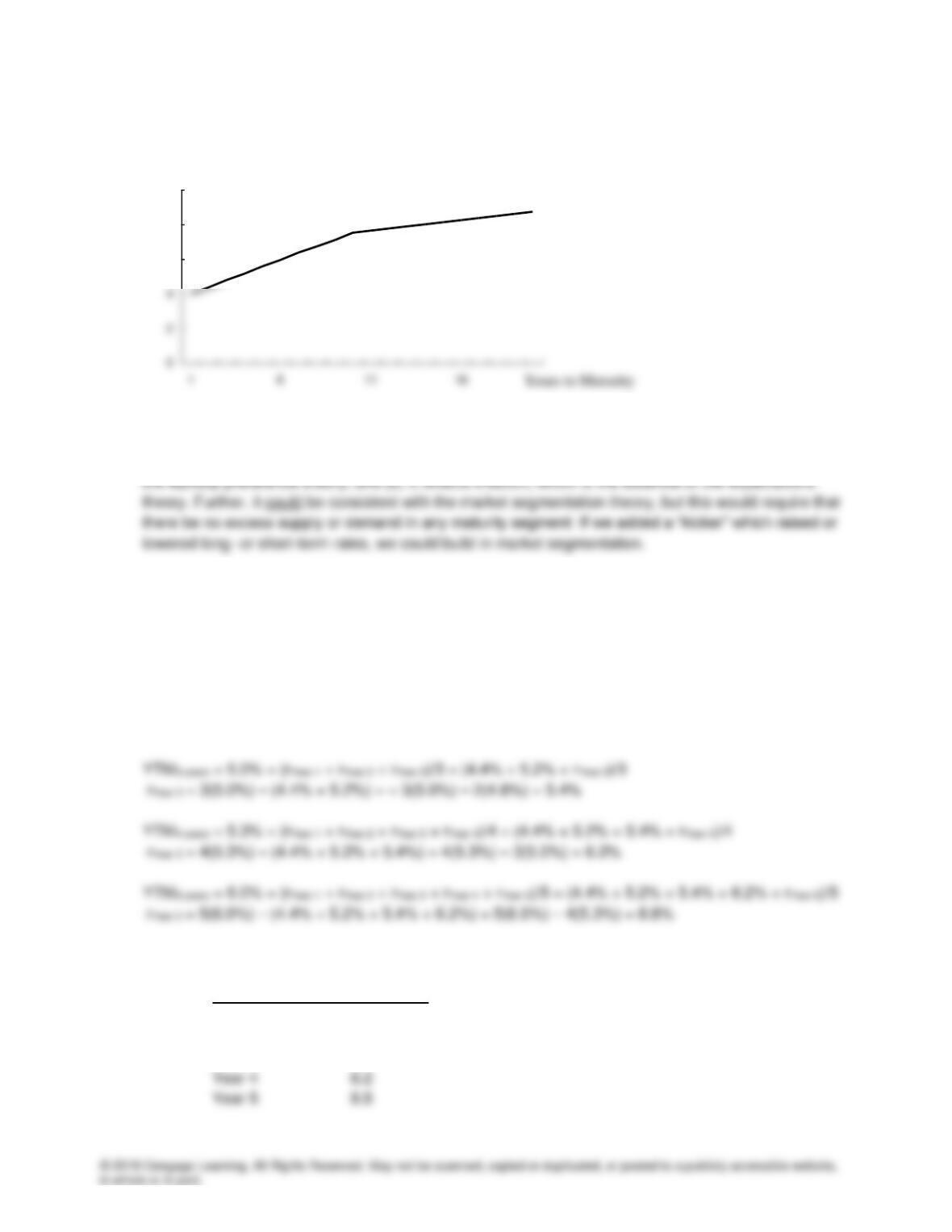

i. The yield to maturity represents the average of the one-year rates that are expected during the life of the

bond. As a result the annual rates that are expected for the next five years are computed as follows:

YTM1-year = 4.4% = rYear 1/1, so the expected interest rate next year is 4.4%

YTM2-years = 4.8% = (rYear 1 + rYear 2)/2 = (4.4% + rYear 2)/2

rYear 2 = 2(4.8%) – 4.4% = 5.2%

According to these computations, the expected rates each year for the next five years are:

Period One-Year Rate

Year 1 4.4%

Year 2 5.2

Year 3 5.4

Interest

(%)

6

8

10

Because the yields on the bonds represent the averages of the one-year rates, after one year has

passed, the yields on the bonds that remain outstanding are as follows:

Original Remaining

Life Life Yield

1 Year matured

After three years have passed, the yields on the bonds that remain outstanding are as follows:

Original Remaining

Life Life Yield

1 Year matured